A comprehensive medicare supplement plan comparison can feel like navigating a maze, but for most affluent retirees, the decision really boils down to two front-runners: Plan G and Plan N. With Plan F no longer an option for new enrollees, understanding the specific trade-offs between these two is the key to locking in solid coverage that protects your financial plan. It’s a choice that balances how much risk you’re willing to take on versus how much you’re willing to pay in monthly premiums.

Securing Your Portfolio with the Right Medigap Plan

For high-net-worth individuals, retirement planning is less about chasing returns and more about managing risk. And one of the biggest risks to a carefully built nest egg? Unpredictable healthcare costs. That makes choosing the right Medicare Supplement plan a critical part of protecting your wealth in 2026.

These plans, often called Medigap, plug the holes left by Original Medicare (Parts A and B). They're designed to cover the out-of-pocket costs like deductibles, copayments, and coinsurance that can otherwise pile up and eat into your assets. This guide will provide a detailed look at your options, helping you conduct a thorough medicare supplement plan comparison.

To cut through the noise, this table breaks down the two most popular and practical plans for new enrollees. It focuses on the coverage areas that matter most when you're thinking about asset protection.

Quick Look at Top Medigap Plans for Affluent Retirees in 2026

As you can see, both plans offer robust coverage, but the small differences are what drive the decision.

- Plan G is for those who want near-total cost predictability.

- Plan N offers a lower premium in exchange for some minor, predictable cost-sharing.

This isn't a niche strategy; it’s a mainstream approach to managing retirement risk. Back in 2022, 42% of all traditional Medicare beneficiaries — a staggering 12.5 million people — had a Medigap policy to keep their costs in check. The data shows these policyholders are often older, have higher incomes, and are in better health, which speaks volumes about the value these plans offer for asset protection.

Aligning Healthcare with Wealth Preservation

Ultimately, the goal is to find a plan that delivers financial predictability without limiting your access to the doctors and hospitals you want. This is where the difference between Plan G and Plan N really comes into focus. Plan G is the more comprehensive of the two, especially because it covers Part B excess charges. That makes it the go-to choice for anyone who wants to virtually eliminate surprise medical bills.

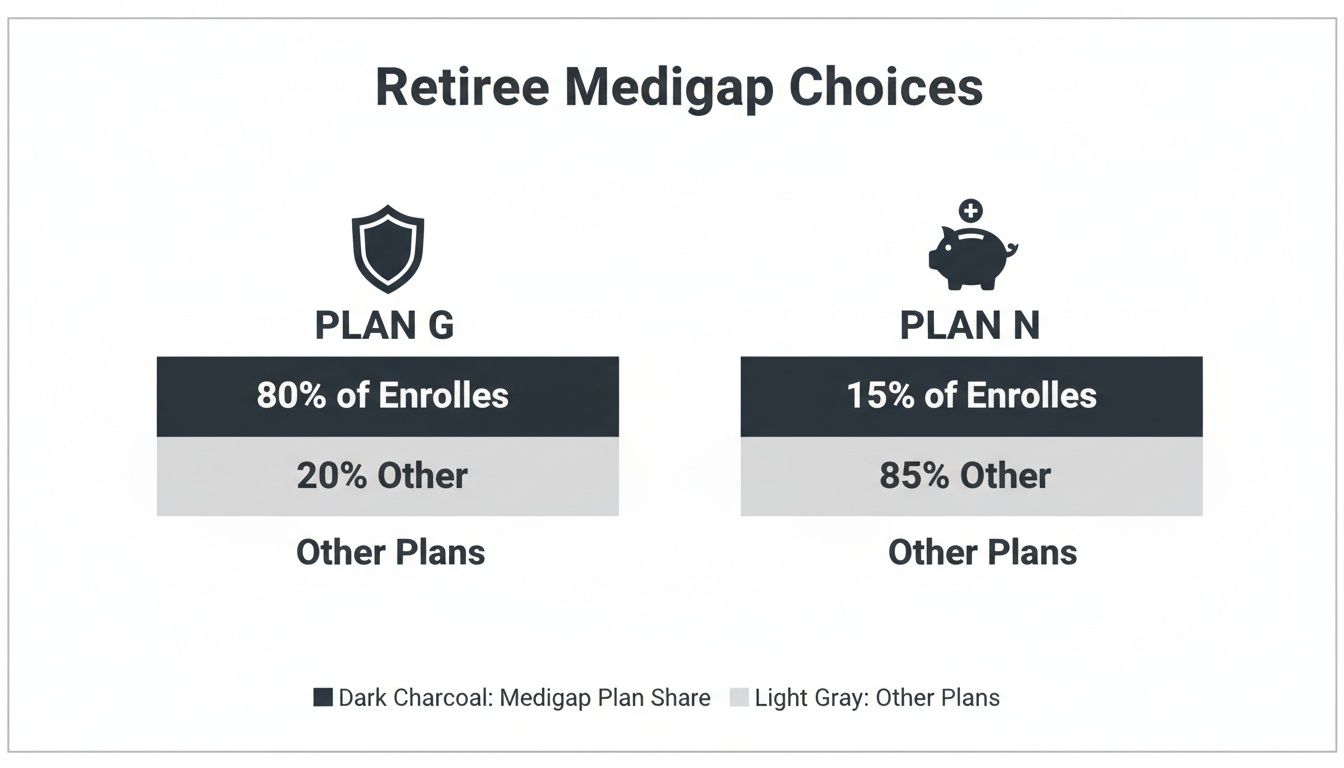

This infographic shows just how popular Plan G and Plan N have become for retirees making a fresh choice.

The chart makes it clear: Plan G dominates the market. This reflects a strong preference among retirees for comprehensive coverage that brings peace of mind and financial certainty.

Key Insight: Choosing the right Medigap plan isn't just about healthcare. It's an essential move to insulate your retirement portfolio from the volatility of medical expenses.

By making a smart decision now, you build a financial firewall that helps ensure your assets go toward your legacy, not toward unexpected hospital bills. This is a foundational piece of any long-term wealth strategy, and for a deeper look into other protective measures, you can read our guide on protecting assets from nursing home costs.

A Detailed Comparison of All 10 Medigap Plans

When you start digging into Medigap, you're hit with an alphabet soup of plans, from A through N. While there are ten standardized options, they are far from equal. A proper medicare supplement plan comparison goes beyond a simple feature list to show how these plans actually perform in the real world, impacting your finances for years to come.

The whole system is built on standardization. This is a huge advantage for consumers because it means a Plan G from one insurance company offers the exact same medical benefits as a Plan G from another. The only things that change are the monthly premium and the company's track record for service and rate increases.

This setup lets you cut through the marketing noise. You can focus on the one thing that matters most: picking the level of coverage that fits your health needs and financial strategy.

The Top-Tier Choices: Plan G and Plan F

For a long time, Plan F was the undisputed king of Medigap, covering every single gap left by Original Medicare. But a 2020 legislative change took it off the market for new beneficiaries. If you were eligible for Medicare before January 1, 2020, you might still be able to buy it, but for everyone else, there's a new leader.

For anyone new to Medicare today, Plan G is the new gold standard. It delivers the most comprehensive coverage you can buy, matching Plan F on nearly every front. There's just one small difference: you're responsible for the annual Medicare Part B deductible.

Crucial Takeaway: With Plan G, your only out-of-pocket cost for any Medicare-approved service is that single, predictable Part B deductible. Pay it once, and you have 100% coverage for the rest of the year. The cost predictability is unmatched.

This makes Plan G a go-to choice for retirees who want to eliminate surprise medical bills and lock in financial certainty.

A Key Detail: Understanding Part B Excess Charges

One of the most critical features that sets Plan G apart is its coverage of Part B excess charges. These are extra fees — up to 15% over the Medicare-approved amount — that some doctors can legally tack on if they don't accept Medicare's standard payment.

While not every doctor does this, having this coverage is essential if you want total freedom to see any specialist in the country without worrying about a surprise bill. For high-net-worth clients who travel or want access to top-tier medical experts, this protection is non-negotiable.

Here’s what that looks like in practice:

- Scenario: You see a specialist who doesn't accept Medicare assignment for a procedure with a $2,000 Medicare-approved cost.

- The Excess Charge: The doctor is allowed to bill an extra 15%, which comes to $300.

- With Plan G: This $300 charge is paid in full.

- With Plan N (and most others): You’d be on the hook for that $300.

The Cost-Sharing Plans: K, L, M, and N

If you're comfortable with some minor, predictable costs in exchange for a lower monthly premium, then Plans K, L, M, and N are worth a look.

- Plan N: This has become the most popular alternative to Plan G. You'll have small copayments for doctor visits (up to $20) and ER trips (up to $50, waived if you're admitted). The catch? It does not cover Part B excess charges.

- Plans K and L: These plans work on a cost-sharing basis. You pay a percentage of most costs until you hit an annual out-of-pocket maximum. For 2026, that limit is $8,000 for Plan K and $4,000 for Plan L.

- Plan M: This one offers a unique trade-off. It splits the cost of the Part A (hospital) deductible with you, covering 50% of it to lower your premium.

A quick look at official government data confirms why these distinctions matter. When you compare Medigap plan benefits, you see that only Plans F and G cover Part B excess charges at 100%. They also provide 80% coverage for foreign travel emergencies, a must-have for anyone planning to travel internationally.

The Basic Plans: A and B

At the other end of the spectrum, Plans A and B offer the most basic coverage. They come with the lowest premiums, but they also leave you exposed to some serious financial risk.

- Plan A: Covers only the bare-bones essentials, like Part A and B coinsurance. It leaves you to pay the large Part A hospital deductible, skilled nursing facility coinsurance, and offers no foreign travel emergency coverage.

- Plan B: It's identical to Plan A but does add coverage for the Medicare Part A deductible.

Because their protection is so limited, these plans are rarely a good fit for anyone looking to protect their savings from a major health event. Ultimately, a smart medicare supplement plan comparison is about finding that sweet spot between premium cost and airtight protection — a balance that Plans G and N strike best for most people turning 65 today.

Financial Breakdown: Plan G vs. Plan N

When it comes to a Medicare supplement plan comparison, the conversation for most new enrollees quickly narrows to just two contenders: Plan G and Plan N. These are the most practical and popular choices on the market today, and figuring out which one fits your finances is about more than just the monthly premium.

This decision is a strategic one, a balance of your health, your lifestyle, and how much financial risk you’re willing to shoulder. Plan G is all about predictability; Plan N opens the door to lower upfront costs if you’re okay with some small, defined out-of-pocket expenses along the way.

Calculating Your Total Cost of Ownership

To really get this right, you have to look at the whole picture. It’s not about the premium; it’s about modeling your potential yearly costs for both plans to see where you’ll actually come out ahead. The "best" plan is simply the one that leaves more money in your pocket over time.

With Plan G, the math is easy. Your total annual cost is just your monthly premium times twelve, plus the yearly Medicare Part B deductible. Once you hit that deductible, you’re 100% covered for all Medicare-approved medical costs. No surprises.

Plan N throws a few more variables into the mix. Its premiums are almost always lower than Plan G's, but you have to be ready for some potential copayments.

- Office Visits: Up to a $20 copay each time you go.

- ER Visits: A $50 copay, but this gets waived if you’re admitted to the hospital.

These copays are predictable, but they are the key to figuring out your true break-even point.

The Break-Even Point Analysis

The heart of the Plan G vs. Plan N debate is this break-even analysis. At what point do the copayments on Plan N wipe out the savings you get from its lower premium? If your total copays for the year are less than what you saved on premiums, Plan N was the cheaper choice.

Let's walk through a real-world example:

- Plan G Premium: $170/month ($2,040 annually)

- Plan N Premium: $130/month ($1,560 annually)

- Annual Premium Savings with Plan N: $480

In this case, you'd have to visit the doctor more than 24 times in one year (24 visits x $20 copay = $480) for Plan G to start making more financial sense. For a healthy, active retiree who only sees a doctor a few times a year, Plan N can mean real savings that add up year after year.

For anyone who puts a high value on predictable cash flow, the lower monthly payment of Plan N is incredibly appealing. The trick is to be honest with yourself about how much you expect to use your healthcare benefits.

Premium Stability and Long-Term Value

While the starting premium gets all the attention, what really matters for long-term financial planning is how stable that premium will be. Historically, Plan N has tended to see smaller annual rate increases than Plan G. This makes sense — because Plan N policyholders share a small piece of the cost, it often leads to a more stable claims history for the insurance company.

A plan that starts out cheaper and also has smaller rate hikes can create a huge gap in savings over a 20- or 30-year retirement. For a high-net-worth client, those savings can be redirected into investments or legacy planning, making their entire financial strategy more efficient.

Ultimately, this medicare supplement plan comparison is a critical piece of wealth management, not just a healthcare decision. Whether you go with the ironclad security of Plan G or the cost-efficient design of Plan N comes down entirely to your personal finances and your outlook on your health.

When to Enroll and What Drives Your Premiums

Timing is absolutely everything when it comes to getting a Medigap plan. There's a specific window where you can buy any plan you want, regardless of your health, and missing it can have serious consequences. For high-net-worth families, getting locked out of the right coverage isn't just an inconvenience — it's a direct threat to a carefully built financial future.

The most critical period you need to know about is your Medigap Open Enrollment Period. This is a one-time, six-month window that kicks off the month you turn 65 and are signed up for Medicare Part B. During these six months, insurance companies are legally required to sell you any Medigap plan they offer at their best rate. They can't ask you health questions, charge you more for a pre-existing condition, or flat-out deny you.

Let that window close, and you lose those powerful guaranteed-issue rights. If you try to apply later, you'll almost certainly have to go through medical underwriting. An insurer can then use your health history to deny your application, leaving a major gap in your retirement strategy. That's why we consider enrolling on time a non-negotiable step.

How Insurance Companies Price Their Plans

Once you're in, the long-term cost of your Medigap plan comes down to how the insurer prices its premiums. You have to look past the initial price tag to see how that number will change over a 20- or 30-year retirement. Insurers generally use one of three methods.

- Community-Rated: Everyone in a given area pays the same premium, no matter their age. Your rate can still go up with inflation, but it won't increase just because you have a birthday. This offers the most predictable costs over the long haul.

- Issue-Age-Rated: Your premium is locked in based on your age when you first buy the policy. While the rate won't climb simply because you get older, it can still rise for other reasons. These plans often look more affordable upfront than community-rated ones.

- Attained-Age-Rated: This is the most common model. The premium is based on your current age, so it goes up every year. These plans usually start with the lowest premiums but can become the most expensive over time.

For affluent retirees who need to forecast expenses for decades, a community-rated or issue-age-rated policy is almost always the smarter play for cost control. This decision is tightly woven into your broader financial picture, right alongside choices like your Social Security claiming strategies.

Other Factors That Move the Needle on Your Premium

Beyond the pricing model, two other big variables will determine your monthly bill: where you live and which insurance company you pick. Because Medigap plans are standardized by the government, a Plan G from one company provides the exact same benefits as a Plan G from another. The only things that change are the price and the company's service reputation.

This is where you have to do your homework. Premiums for the identical plan can swing by hundreds of dollars a year based on nothing more than the insurer and your zip code.

Key Insight: Shopping around isn't just a good idea; it's essential. Since the coverage is identical letter for letter, your job is to find the most stable carrier offering the lowest price for your chosen plan.

The good news is that recent market trends have been favorable for consumers. Based on an analysis of insurer rate filings, average premiums for the popular Plan G actually dipped by 0.4%, while Plan N saw an even larger 4.1% drop. The median rate changes were even better, with a 1% decrease for Plan G and a 4.9% decrease for Plan N. As competition heats up, it’s helping keep these comprehensive plans more affordable. This data shows that Plans G and N aren't just great coverage; they continue to be a source of stable, predictable value.

Medigap vs. Medicare Advantage for High-Net-Worth Retirees

When you finally enroll in Original Medicare, you face one of the most critical healthcare decisions of your retirement. It’s a fork in the road, leading down two very different paths: stick with Original Medicare and add a Medigap plan, or switch to an all-in-one Medicare Advantage (Part C) plan.

For anyone with significant assets, this choice is less about healthcare and more about risk management. It’s about protecting the financial independence you spent a lifetime building. While both routes have their merits, a close medicare supplement plan comparison shows Medigap often proves to be the smarter play for a wealth preservation strategy.

The Core Difference: Freedom vs. Structure

Medigap plans are designed to supplement Original Medicare, not replace it. This preserves Medicare’s biggest selling point: the freedom to see any doctor or visit any hospital in the United States that accepts Medicare. There are no networks to navigate, and you almost never need a referral to see a top specialist.

Medicare Advantage plans, on the other hand, are run by private insurance companies and completely take the place of Original Medicare. They operate a lot like the HMO or PPO plans most people have during their careers, meaning you have to stay within a specific network of doctors and hospitals to keep costs down.

For a retiree who splits their time between two homes or travels the country, the nationwide access of a Medigap plan is invaluable. It completely removes the financial risk of having a medical emergency while out of your plan’s network.

Cost Predictability and Financial Certainty

From a financial planning standpoint, the two systems couldn't be more different. With a comprehensive Medigap plan like Plan G, your healthcare spending for the year becomes almost entirely predictable. You pay your monthly premium and the annual Part B deductible. For Medicare-approved services, that’s it.

Medicare Advantage plans often look appealing with their low or even $0 monthly premiums, but they introduce a different kind of financial exposure through out-of-pocket costs. These plans come with their own system of deductibles, copayments, and coinsurance that you pay as you need care.

While every Advantage plan has a cap on what you can spend, this maximum out-of-pocket limit can reach as high as $9,100 for in-network care. This creates a wide and unpredictable spending range, which can be a real problem for a carefully constructed retirement budget.

A Tale of Two Retirees: A Scenario Comparison

To see how this plays out in the real world, let’s imagine two retirees who both need to see a cardiologist for a new heart condition.

- Retiree A (with Medigap Plan G): She researches the best cardiologists in her state and calls her top choice directly to make an appointment. No referral is needed. She knows that once her small Part B deductible is met, all her costs for visits, tests, and any procedures will be covered at 100%. She has total control and, more importantly, total financial peace of mind.

- Retiree B (with a Medicare Advantage HMO): He first has to book an appointment with his primary care physician to ask for a referral to a cardiologist. His choice of specialist is restricted to doctors who are in his plan’s network. When the cardiologist orders a series of advanced diagnostic tests, each one has to be submitted for prior authorization from the insurance company, creating delays and the risk of a denial. Every visit and test also carries a copay, so his total costs are a moving target.

The difference is stark. Medigap provides autonomy and predictable costs. Medicare Advantage introduces network limitations, administrative hurdles, and variable expenses.

For retirees who value immediate access to premier specialists and want to eliminate financial shocks, the Medigap framework is the clear winner. It turns healthcare from a potential financial liability into a fixed, manageable line item — a vital piece of any serious retirement plan.

Making Your Final Medigap Plan Decision

After comparing all the details, the final choice comes down to you. It’s a personal call based on your finances, your health, and frankly, your own tolerance for risk. There is no single "best" plan for everyone; the real goal is to find the one that fits neatly into your retirement strategy and protects your long-term financial security.

To get there, you have to be honest with yourself about what truly matters. Answering these questions will point you in the right direction.

A Decision-Making Checklist

- How critical is it for me to see any doctor, anywhere in the country, without worrying about networks or referrals?

- Do I prefer a predictable, fixed monthly premium, or am I okay with some variable costs like copayments to save money upfront?

- Am I willing to risk paying for potential Part B excess charges myself in exchange for a lower monthly bill?

- Do I expect to see doctors frequently, or am I in good health and only need occasional medical care?

Your answers will likely steer you toward one of two front-runners: Plan G or Plan N.

Think of Plan G as the go-to for anyone who wants absolute predictability. You pay a higher premium, but in return, you get unrestricted access to care and virtually eliminate any surprise out-of-pocket costs. It’s an investment in pure peace of mind.

Plan N, on the other hand, is built for the cost-conscious retiree who is comfortable with a little more risk. The lower premiums can mean significant savings, especially if you’re healthy. It’s a great way to lower your fixed expenses while still having solid, reliable coverage for the big things.

Final Takeaway: Your Medigap decision is a core part of your wealth management. It's meant to shield your assets from the volatility of healthcare expenses, ensuring the financial plan you've built stays on track for the long haul.

Part of this process is also about the advice you get. To make a smart choice, it helps to understand how different advisors work. Some provide insurance advice with or without commissions, and knowing the difference helps ensure the guidance you receive is truly in your best interest.

Tying your Medigap choice into your big-picture financial goals is essential. For more on how these pieces fit together, take a look at our guide on choosing a retirement financial advisor. This helps make sure both your health and wealth are secured for the years ahead.

Your Top Medigap Questions, Answered

As you dive into the details of a medicare supplement plan comparison, a few key questions almost always come up. Let's get them answered so you can feel confident in your decision.

Can I Switch My Medigap Plan Later?

Yes, you can apply to switch your Medigap plan at any time. The catch? Unless you have a "guaranteed issue right," insurance companies can use medical underwriting to evaluate your application.

This means they have the right to deny you coverage or charge you much higher premiums based on your health history. It’s exactly why your choice during the initial Open Enrollment Period is so critical.

Do Medigap Plans Cover Prescription Drugs?

No. Medigap plans sold to anyone new to Medicare after 2006 do not include prescription drug benefits.

To get that coverage, you’ll need to enroll in a separate Medicare Part D Prescription Drug Plan. Pairing your Medigap policy with the right Part D plan is a crucial piece of the puzzle for complete healthcare coverage in retirement.

A standardized Medigap plan, like Plan G, offers the exact same benefits no matter which insurance company you buy it from. The monthly premiums, however, can vary dramatically. Your comparison should really zero in on the premium cost, the insurer’s financial stability, and its reputation for customer service.

What Is a Part B Excess Charge?

A Part B excess charge is an extra amount — up to 15% over what Medicare agrees to pay — that some doctors can add to their bill. For retirees who want complete freedom to see any specialist without worrying about a surprise bill, this is a make-or-break detail.

- Who Covers It? Only Medigap Plans G and F cover these excess charges.

- Why It Matters: This single benefit is a key reason many high-net-worth individuals land on Plan G. It guarantees there are no unexpected out-of-pocket costs when seeing doctors who don't accept Medicare's approved amount as full payment.

For those who prioritize total protection and unrestricted access to providers, this feature often makes the decision for them.

At Commons Capital, we help our clients fit these important healthcare decisions into their complete wealth management strategy. To see how we can help you build a secure financial future, you can learn more about our approach.