When most people hear "wealth management," they think of investing. But for high-net-worth families, that's just one piece of a much larger, more intricate puzzle. True family wealth management is about creating a financial master plan strong enough to support not just you, but your children, grandchildren, and beyond.

It’s about architecting a structure that integrates everything—investment strategies, tax planning, estate documents, and even family values—into a single, cohesive blueprint. This comprehensive planning is especially critical for those with complex finances, like professional athletes or entertainers, where income streams can be unconventional and short-lived.

What Is Family Wealth Management and Why It Matters

So what's the real difference here? Think of it this way: a traditional financial advisor is like the skilled captain of a single ship, focused on navigating its journey.

A family wealth manager, on the other hand, is the admiral of an entire fleet. Their job is to make sure every vessel—your investment portfolio, your business interests, your real estate holdings, and your philanthropic goals—is sailing in perfect formation, headed in the same direction, and prepared for any storm on the horizon. This holistic approach is the essence of effective family wealth management.

It's About More Than Money

Here's a truth we’ve seen play out time and time again: without a clear plan, significant wealth often creates more conflict than opportunity. The real purpose of this process is to get ahead of the complex, and often emotional, family dynamics that come with financial success.

A well-crafted plan does more than just grow assets. It transforms wealth from a potential point of conflict into a powerful tool for unity, purpose, and a lasting family legacy.

It gives your family a framework to have those difficult but essential conversations about the future. From experience, we know that families who regularly talk about their values and the responsibilities that come with wealth feel far more confident that it will be passed on smoothly. You’re not just managing money; you’re building a story that will guide and inspire generations to come.

The Core Pillars of a Successful Strategy

A solid family wealth management strategy is built on a few essential pillars. Each one supports the others, creating a structure that can withstand market swings, tax law changes, and evolving family needs.

This table provides a snapshot of these core components and what they aim to achieve.

Let's quickly unpack these. Financial and Investment Management is the engine, ensuring there's enough fuel to power the family's long-term goals. Estate and Tax Planning is the navigation, charting the most efficient course to get assets where they need to go.

Meanwhile, Family Governance and Education acts as the crew's training manual, preparing everyone for their roles. And finally, Philanthropy and Legacy Planning is the ultimate destination—defining the family's lasting mark on the world. Without all four working together, the entire structure is at risk.

Building Your Family Governance Framework

Having a sharp financial plan is critical, but it’s only half the battle. The most durable family wealth strategies are always built on something more human: clear communication, shared values, and a set of agreed-upon rules. This is what we call family governance.

Think of it as the operating manual for your family's financial life. It’s designed to ensure decisions are made with care and to head off conflicts before they even have a chance to start.

Without this structure, even the most sophisticated investment portfolio can be torn apart by family disputes, simple misunderstandings, or just a lack of preparedness in the next generation. It’s the human element, not the spreadsheet, that usually determines whether wealth becomes a source of unity or division. Getting this right is the first real step in turning assets into a legacy that lasts.

The Family Constitution and Mission Statement

The centerpiece of good governance is a family constitution or mission statement. This isn't a legal document you file with a court; it’s a strategic and moral compass for everyone involved. It’s where you formally lay out the family’s core values, its vision for the future, and the principles that will guide every major decision about your collective wealth.

The process of creating one is often just as valuable as the final document. It gets family members talking openly about the big questions that often go unasked.

- What are our shared values? (e.g., hard work, education, community service, entrepreneurialism)

- What is the real purpose of our wealth? (e.g., to create opportunity, fund philanthropy, or just provide security)

- What kind of legacy do we want to build together?

Putting the answers down on paper creates a north star for future generations. It ensures that the original "why" behind the wealth is never forgotten and continues to guide every financial "what."

Establishing Clear Communication and Decision Making

A mission statement gives you a vision, but you need clear processes to make it a reality. A strong governance framework defines exactly how the family will talk to each other and make decisions, which replaces ambiguity with clarity and builds trust.

A common pitfall for families is assuming that everyone is on the same page. Formalizing communication and decision-making processes replaces assumption with clarity, which is the bedrock of trust.

This often means setting up regular family councils or meetings. These meetings become the dedicated time and place to discuss financial performance, review philanthropic efforts, and share business updates. They also double as a training ground for younger family members, slowly teaching them the responsibilities that come with stewardship.

A few key protocols you’ll want to define are:

- Roles and Responsibilities: Who does what? Getting specific about the roles of family members, board members, and outside advisors prevents confusion and turf wars.

- Voting and Resolution: How will you make the big calls? Decide whether it will be a majority vote, a consensus, or up to a specific committee.

- Conflict Resolution: What’s the plan when people disagree? Having a pre-approved method for handling disputes before they happen is absolutely crucial. You might be interested in learning about other structures that can help with this, like a Family Limited Liability Company, which you can read about in our comprehensive guide on the topic.

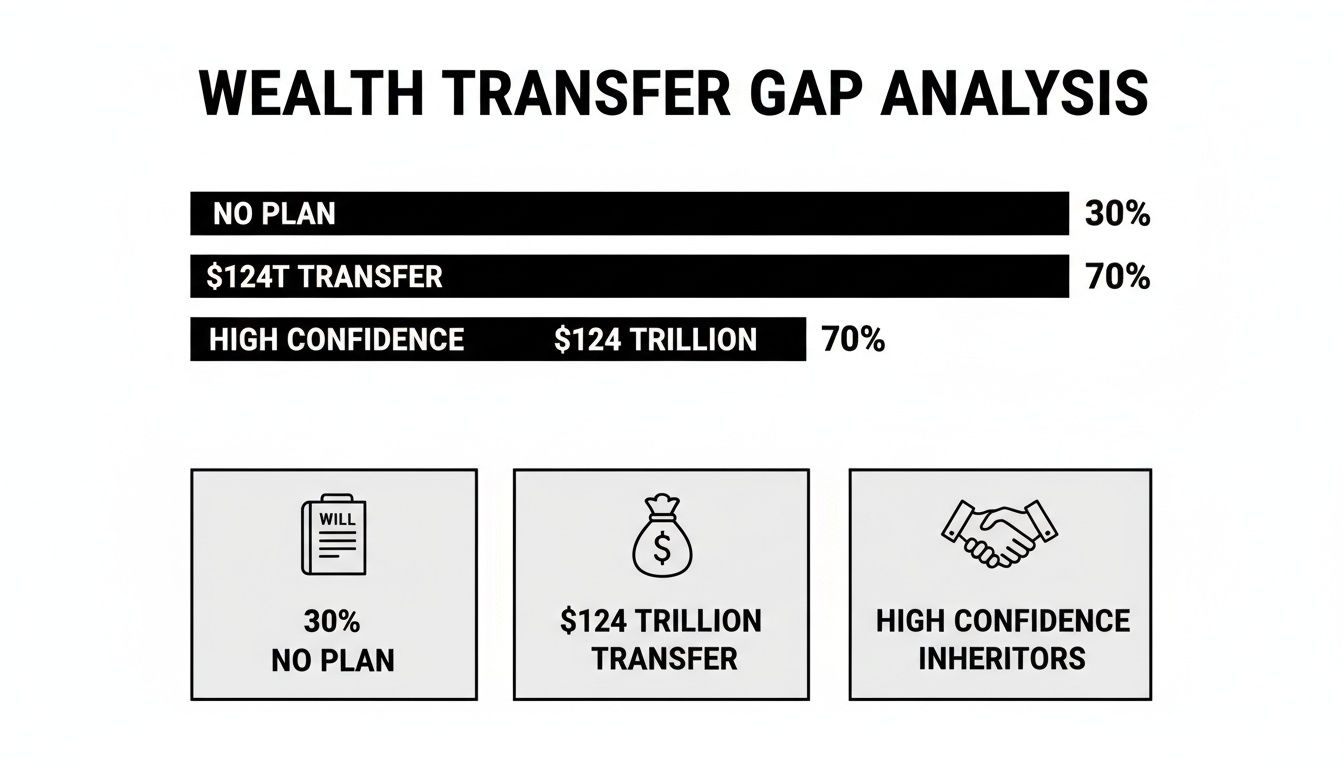

The need for these conversations is more urgent than ever. A staggering $124 trillion wealth transfer is expected to happen in the United States through 2048, yet huge communication gaps remain. Research shows that 30% of parents don't have a confident will and estate plan, and most simply avoid talking about inheritance with their children—creating the perfect environment for future conflict.

According to Fidelity's 2026 Family and Finance Study, families that have ongoing, open conversations about their values report feeling far more confident in their financial plans. This really highlights the need for proactive planning, especially for high-net-worth clients in complex fields like sports and entertainment where the stakes are even higher.

Crafting a Resilient Multi-Generational Investment Strategy

With your family's governance structure in place, it’s time to turn to the financial engine that will power your legacy: the investment portfolio. When we talk about family wealth management, we’re not talking about chasing market fads or gambling on explosive, short-term gains. It's about building a resilient, multi-generational strategy designed to weather market cycles and fund your family’s vision for decades.

Think of it like an all-weather vessel. It needs to be sturdy enough to navigate turbulent economic storms (that’s capital preservation) while still powerful enough to make steady progress in calm seas (that’s growth). This isn't a balance you stumble into. It's achieved through a deliberate investment philosophy that’s tied directly to your family’s specific risk tolerance, long-term goals, and cash flow needs.

Designing a Durable, All-Weather Portfolio

The bedrock of any durable portfolio is strategic asset allocation. At its core, this just means building a sophisticated mix of assets that react differently to various market conditions. Instead of putting all your eggs in one basket, you’re creating a diversified financial ecosystem where the weakness of one asset is often balanced by the strength of another.

A modern portfolio built for the long haul typically includes:

- Public Equities: This is your growth engine, providing the potential for long-term capital appreciation. A global mix of stocks across different sectors and market caps is crucial for spreading risk.

- Fixed Income: High-quality bonds are the stabilizer. They provide predictable income and act as a cushion during the stock market’s inevitable downturns.

- Alternative Investments: This is where many high-net-worth families create a real competitive edge. Alternatives can add powerful diversification and unlock return potential that isn't tied to the public markets.

A truly resilient portfolio is one that is built to achieve its objectives regardless of the economic forecast. It prizes durability over short-term performance, ensuring the family’s financial engine can run smoothly for generations.

The need for this kind of thoughtful strategy has never been greater. This chart shows the sheer scale of the wealth transfer we're facing—and how many families are still unprepared for this massive shift.

The numbers paint a clear picture: there is a major gap between the colossal amount of wealth changing hands and the lack of formal planning to guide it.

The Role of Alternatives in Modern Portfolios

For families with significant assets, alternative investments have moved from a niche play to a core component of a sophisticated strategy. The key is that these assets often have a low correlation to public markets, meaning they don't always move in lockstep with stocks and bonds. That can be invaluable during periods of volatility.

Key alternative categories include:

- Private Equity: Investing directly in private companies offers the potential for high growth long before they ever hit the public stock market.

- Private Credit: Lending money directly to businesses can generate attractive, steady income streams that are often less sensitive to the interest rate swings that affect traditional bonds.

- Real Assets: Tangible assets like commercial real estate, farmland, and infrastructure can provide both inflation protection and stable cash flow.

As families look to diversify, innovations like Real-World Asset Tokenization are also becoming critical tools for modernizing a portfolio, offering better liquidity and access to a wider range of assets.

A recent Goldman Sachs survey of family offices—where 67% manage over $1 billion—shows a deep commitment to this balanced approach. In 2026, alternatives made up a hefty 42% of the average portfolio, with public equities at 31% and fixed income at 11%. That kind of steady allocation highlights the long-term mindset that defines smart family wealth management.

Tailoring Strategies for Unique Income Streams

Of course, not all family wealth comes from a predictable salary or a traditional business. A truly robust investment plan has to account for the unique financial realities of clients in sports, entertainment, or even entrepreneurs who face highly irregular and concentrated income.

For these clients, the strategy is different. The primary goal is to take sporadic, high-income events—a major contract, a business sale, a massive royalty check—and convert them into a durable financial base that provides stable, long-term cash flow.

It’s all about front-loading investments, putting a premium on capital preservation, and building a portfolio that can support the family’s lifestyle long after the peak earning years are over. This approach ensures that a few great years can successfully fund a lifetime of financial security.

Choosing the Right Family Office Model

With your family’s governance and investment philosophy mapped out, the next question is a big one: who is going to run the show? This is where the "family office" comes in, serving as the dedicated engine for your entire financial world.

Getting this structure right is more than an administrative task. It’s a strategic decision that forces you to balance control, cost, and complexity, and the model you choose has to align with your family's wealth, the nature of your assets, and your vision for the future.

The Single-Family Office (SFO)

The Single-Family Office, or SFO, is the classic, bespoke approach. Think of it as building your own private wealth management firm, dedicated exclusively to the financial and personal affairs of your family. It offers the highest degree of control and privacy, with a hand-picked team that works only for you.

An SFO’s advantages are clear:

- Total Customization: Every single service, from investment management and tax planning to managing properties and travel, is tailored to your family's exact needs.

- Complete Control: You call all the shots. The family retains full authority over strategy, investments, and who gets hired.

- Unmatched Privacy: With an operation serving only one family, your financial information remains entirely in-house and confidential.

But this level of service doesn't come cheap. The operational costs are significant, which is why an SFO is typically only on the table for families with assets starting at $100 million or more.

The Multi-Family Office (MFO)

A Multi-Family Office, or MFO, offers the same comprehensive suite of services as an SFO but serves a select group of affluent families. By pooling resources, families gain access to top-tier institutional expertise and opportunities without taking on the entire financial weight of a dedicated SFO.

An MFO strikes a powerful balance, delivering sophisticated services and leveraging economies of scale. It’s a compelling option for families who want comprehensive management without the headaches of running their own private office.

You get the feel of a dedicated team and a broad service menu, but the costs are spread across multiple clients. This makes the MFO a much more accessible and efficient model for a wider range of high-net-worth families. You can discover more about how a Multi-Family Office works and if it's the right choice for you in our detailed guide.

The Modern Hybrid and Virtual Model

We're also seeing a powerful trend toward hybrid or "virtual" family offices. This isn't a formal structure but a flexible approach where families build a custom support system by blending a small internal team with outsourced specialists.

For instance, a family might handle day-to-day bill-pay and administrative tasks themselves but partner with an external firm like Commons for specialized functions—investment management, estate planning, or philanthropic strategy. This gives you the best of both worlds: you keep control over core functions while plugging into world-class expertise exactly where you need it.

Recent industry analysis backs this up. The Julius Baer Family Barometer 2026 notes that while roughly 40% of ultra-high-net-worth families are served by full family offices, many are hesitant to take on the cost and complexity. Instead, they’re looking to specialized wealth managers for more flexible, curated services. We see this demand every day with our own clients. Find out more in the 2026 family wealth management insights from Julius Baer. This modern approach empowers families to build a financial structure that's not just resilient but perfectly fitted to their unique journey.

Integrating Philanthropy and Impact into Your Legacy

True family wealth management goes far beyond just preserving assets and tracking returns. It recognizes that wealth is one of the most powerful tools you have to create positive change—building a legacy that genuinely reflects your family’s deepest values.

This means moving beyond just writing a check now and then. Strategic philanthropy lets your family direct its resources toward the causes that truly matter, forging a shared sense of purpose that can bring generations together. It’s a shift from passive giving to an active, hands-on expression of your family’s mission.

From Giving to Strategic Philanthropy

Making the leap to strategic philanthropy is really about a shift in mindset. Instead of making scattered, reactive donations, you develop a focused plan designed to make the biggest possible impact. The goal is to align every charitable dollar with the core values you’ve laid out in your family mission statement.

This intentional approach doesn't just make your giving more effective; it makes it more meaningful. It also creates a fantastic platform for bringing younger family members into the fold, teaching them about stewardship and instilling the principles you want to see passed down.

A well-defined philanthropic mission does more than just support worthy causes; it becomes a powerful narrative that connects family members, reinforces shared values, and gives purpose to the family's wealth for generations to come.

By formalizing your giving strategy, you're building a framework that ensures your family's positive impact will continue long into the future, guided by a clear and unified vision.

Key Vehicles for Charitable Giving

Several structures can help your family put its philanthropic mission into action. Each one offers a different mix of control, complexity, and tax benefits, so it’s critical to find the one that fits your specific goals.

- Donor-Advised Funds (DAFs): Think of a DAF as a charitable investment account. You make a contribution to the fund, get an immediate tax deduction, and then recommend grants to your favorite charities over time. It’s a simple, low-cost way to organize your giving.

- Private Foundations: This option gives your family the most control. You establish and manage your own charitable entity, making all the decisions about how funds are invested and granted. It's more complex and costly to run, but it creates a prominent and lasting platform for your family’s philanthropic identity.

- Impact Investing: This approach directly blends financial returns with measurable social or environmental impact. Instead of donating, you invest in companies, funds, and projects that are actively solving problems—from clean energy to affordable housing.

Choosing between these tools really comes down to what your family wants to achieve. To dig deeper, you can explore our guide comparing a donor-advised fund vs. a private foundation.

Philanthropy as a Unifying Force

Ultimately, weaving philanthropy into your wealth plan is about much more than tax strategies or public recognition. It’s a powerful way to build a stronger, more connected family.

When you work together on a shared philanthropic project—whether it’s volunteering, serving on a foundation board, or researching charities—you create a unique bond. It offers a neutral ground for communication and collaboration, fostering skills and relationships that are simply invaluable.

For the next generation, it’s a tangible way to connect with the family’s legacy and learn the responsibilities of stewardship firsthand. This ensures the wealth you’ve built continues to create value in the world for years to come.

Your Next Steps in Building a Lasting Financial Legacy

So, you’ve learned the theory. Now what? The real work of building a lasting financial legacy doesn’t happen on a whiteboard—it happens when you take concrete, intentional steps to turn those ideas into action.

It all boils down to bringing your family together around a shared purpose. This is about so much more than just numbers on a spreadsheet; it's about making sure your wealth actually serves the people and values you care about for decades to come.

It All Starts With a Conversation

The single most important—and often hardest—first step is just to start talking. It’s time for open, honest conversations with your family about money, your shared values, and what you all hope for the future. This isn't a one-and-done meeting, but the beginning of a real, ongoing dialogue.

The goal here is to take the mystery out of wealth and reframe it as a shared family tool. When everyone feels heard and respected, you build the kind of trust that’s absolutely essential for any long-term plan to succeed.

A Practical Checklist to Get Moving

Moving from talk to action is where the real momentum builds. Use this simple checklist to get the ball rolling and make sure you aren’t missing any foundational pieces.

- Schedule the First Family Talk: Put a dedicated time on the calendar to simply discuss your family’s core values and what you hope your wealth can achieve.

- Round Up Your Documents: Gather every financial and legal document you have—wills, trusts, investment statements, insurance policies. This will quickly show you where the gaps are.

- Map Out Your Advisors: Who do you currently work with? List out your accountant, lawyer, and insurance agent. Then, ask yourself honestly if their expertise matches your family's long-term vision.

- Draft a Simple Mission Statement: Don't overthink it. Even a one-page document outlining your family's core principles and financial purpose can provide incredible clarity and direction.

Think of these as the foundational steps. They set the stage for the deeper, more detailed work that lies ahead.

The Power of a Coordinated Team

A truly successful family wealth plan is almost never the work of one person. It’s the result of a team of specialists all working together, like a championship sports team where every player knows their role and executes it flawlessly.

The real magic happens when your wealth manager, estate attorney, and tax professional stop working in silos and start acting as a single, unified team—all driving toward the goals your family has defined.

This integrated approach is what closes the gaps that can cost families dearly. A great investment idea might look brilliant on its own, but it could trigger unintended tax consequences if it isn't viewed through the lens of your estate plan. When everyone is at the same table, those blind spots disappear.

At Commons Capital, we see our role as the quarterback for your entire financial team. We either coordinate with the professionals you already trust or help you assemble a new team of experts. Our focus is making sure every piece of your financial life is working in perfect harmony. We specialize in walking high-net-worth families, including those in unique fields like sports and entertainment, through this very process. By taking these concrete steps, you can start the journey of securing your family’s legacy with genuine confidence.

Frequently Asked Questions About Family Wealth Management

As families build and protect their wealth, certain questions come up time and time again. Below, we tackle some of the most common ones we hear from our clients, offering straightforward answers to help you map out your family's future.

At What Level of Wealth Should a Family Consider Formal Wealth Management?

It’s less about hitting a magic number and more about when your financial life starts getting complicated. While there’s no single threshold, a coordinated strategy often becomes essential for families with investable assets starting around $500,000.

The real triggers, though, are life events and complexity. Are you running a business? Managing multiple properties? Thinking seriously about how to pass wealth to your kids and grandkids? If so, it’s probably time to move from piecemeal advice to a holistic plan.

How Can We Prepare the Next Generation to Manage Inherited Wealth?

Getting the next generation ready isn't a one-time conversation; it's a long-term commitment built on education, open communication, and trust. You can start by bringing younger family members into financial discussions that are right for their age, perhaps by involving them in philanthropic decisions.

The real aim is to shift their mindset from being passive beneficiaries to becoming responsible stewards of the family’s legacy. This journey has to start years, even decades, before any wealth actually changes hands.

A solid family governance plan, complete with a shared mission statement, is a powerful tool for instilling these values. It’s also smart to be pragmatic and understand what a prenup can protect, including inheritances and business assets, as these agreements are often vital for smooth, multi-generational wealth transfers and preventing future disputes.

What Is the Difference Between a Wealth Manager and a Family Office?

A wealth manager’s world primarily revolves around investment management and financial planning. A family office, on the other hand, takes a much wider view. It's an integrated command center for a family's entire financial universe—handling everything from tax and legal matters to philanthropy and even lifestyle management.

Here’s a quick look at the different models:

- Single-Family Office (SFO): A dedicated, private company set up to serve just one ultra-high-net-worth family. It’s the ultimate bespoke solution.

- Multi-Family Office (MFO): An independent firm that provides the full suite of family office services to a select group of affluent families, allowing them to share resources and expertise.

- Hybrid or Virtual Family Office: This modern approach involves a lead advisory firm that acts as a central quarterback, coordinating a network of best-in-class external specialists for the family.

Firms like Commons Capital excel in this hybrid model. We deliver the comprehensive, coordinated service of a traditional family office but without the massive overhead of a standalone SFO. It’s a flexible and powerful way for families to get top-tier, professional guidance.

Ready to secure your family's financial future for generations to come? The team at Commons Capital has the expertise to guide you through every step of the family wealth management process. Visit us today to learn how we can help you build a lasting legacy.