Think of a wealth planner as the master architect of your financial life. They go far beyond just managing investments, designing a comprehensive blueprint for your entire financial world to ensure every piece works together to support your most important life goals. A skilled wealth planner offers strategic guidance that is essential for navigating financial complexity and building lasting prosperity.

What Does a Wealth Planner Actually Do?

Imagine you’re building a high-end custom home. You wouldn't ask the plumber to frame the house or have the electrician pour the foundation. You’d hire a general contractor or an architect—someone who sees the entire project and coordinates all the specialists to make sure the final structure is sound, functional, and exactly what you envisioned.

A wealth planner is that architect for your finances.

They serve as the financial quarterback for high-net-worth individuals and families. Their role is to coordinate a team of experts—like CPAs, estate attorneys, and insurance specialists—to ensure every decision fits into one cohesive strategy. This holistic approach is a world away from a typical stockbroker who is focused primarily on market returns.

A Holistic Financial Blueprint

The real value of a wealth planner is their 30,000-foot view. They aren't just managing one piece of the puzzle; they're putting the entire thing together. For anyone with significant assets, this integrated approach isn't a luxury—it's a necessity.

Their work typically revolves around a few core areas:

- Advanced Investment Strategy: This goes far beyond just public stocks and bonds. They often provide access to private equity, real estate, and other alternative investments, all while managing risk.

- Estate & Legacy Planning: They work with attorneys to structure your affairs so that your wealth transfers smoothly and tax-efficiently, whether it’s to the next generation or to charitable causes you care about.

- Proactive Tax Planning: A good wealth planner is always looking for ways to be more tax-efficient. They coordinate with your CPA to structure investments, time transactions, and make decisions that minimize your tax bill year after year.

- Comprehensive Risk Management: This is about protecting what you've built. They analyze your exposure to everything from lawsuits and business risks to personal health crises, ensuring you have the right protections in place.

This kind of oversight is becoming more crucial than ever. Global assets under management (AUM) are expected to climb from US$139 trillion in 2024 to a staggering US$200 trillion by 2030, according to PwC's Global Asset and Wealth Management Report. Much of that growth is coming from individuals with investable assets over $500,000, which shows just how many people are reaching a level of complexity where a financial architect becomes essential.

A wealth planner's goal isn't just to make you more money. It's to protect what you have, preserve it for the future, and make sure it's all working to support the life you truly want to live.

This is exactly why successful professionals, families, and even dedicated family offices lean on a wealth planner. They bring strategic direction to the table, turning financial complexity into clarity and making sure every component of your wealth is pulling in the same direction.

The Core Services of a Modern Wealth Planner

To really understand what a wealth planner brings to the table, you have to look past the job title and at the actual, high-impact services they deliver. This isn’t a checklist of disconnected tasks; it's a completely integrated system designed to build, protect, and eventually pass on your wealth in the most effective way possible.

Think of it like this: their services are the five foundational pillars holding up the entire structure of your financial life.

These pillars are designed to work together, making sure a move in one area—like your investments—also supports your goals in another, like your estate plan. It’s this constant coordination that truly sets a wealth planner apart from other financial professionals. Let's break down each of these critical functions.

Advanced Investment Management

A modern wealth planner’s work goes far beyond a simple mix of stocks and bonds. They build portfolios using sophisticated risk modeling that is tied directly to your personal tolerance for volatility and what you want to achieve in the long run, whether that’s launching a new business or guaranteeing a stress-free retirement.

The real game-changer is their ability to get you into private market investments. These are opportunities that are typically off-limits to the average investor, and can include:

- Private Equity: Investing in promising private companies before they ever hit the stock market.

- Venture Capital: Backing early-stage startups that have explosive growth potential.

- Private Credit: Lending money directly to companies, which can offer better yields than public bonds.

- Real Estate Funds: Getting a piece of large-scale commercial property deals.

These alternative assets are absolutely critical for true diversification and can produce returns that have nothing to do with the swings of the public markets. The complexity here is no joke—a single operations person at a typical firm might only be able to handle 200-250 manual alternative investment positions. A wealth planner doesn't just open the door; they perform the intense due diligence required to make sure these opportunities are sound. To get a better handle on this specialized field, our guide on private wealth management offers a much deeper look.

Holistic Financial and Retirement Planning

This is the master blueprint for your entire financial life. Your wealth planner creates a detailed map that models your cash flow, measures your progress toward major life goals, and stress-tests the whole plan against different economic shocks.

This isn't just about saving for retirement; it's about defining what retirement looks like for you and building a precise, data-driven path to get there.

For a business owner, this could mean mapping out an exit strategy that gets the best possible sale price while minimizing the tax hit. For a professional athlete, it might involve structuring their income to last for decades after their peak earning years are over. This plan isn't static; it's a living document that gets updated as your life, career, and goals change.

Estate and Legacy Strategy

What happens to your wealth after you’re gone? A wealth planner works hand-in-hand with top estate attorneys to answer that question with precision and care. They are absolutely essential in designing a strategy that ensures your assets are transferred smoothly, privately, and with as little tax friction as possible to your family or favorite charities.

Their work here includes:

- Setting up trusts that shield assets from creditors and make sure they're managed exactly how you intended.

- Running family meetings to walk everyone through the plan and get the next generation ready for their role.

- Using smart strategies to reduce estate taxes, which can take a massive bite out of an inheritance if you don't plan ahead.

Proactive Tax Optimization

Taxes can be the single biggest drag on growing your wealth over time. A wealth planner doesn't replace your CPA; they act as a strategic quarterback, making sure every investment and financial decision is made with taxes in mind.

This forward-thinking coordination can save a fortune over a lifetime. For instance, they might suggest harvesting tax losses to cancel out gains, strategically placing certain assets in tax-friendly accounts, or timing a big property sale to land in a more favorable tax year. This constant, proactive approach is a signature of high-level wealth planning.

Comprehensive Risk Management

Finally, a wealth planner is your financial guardian, spotting and neutralizing risks that could blow your entire plan off course. This goes way beyond just market risk. They'll dig into your personal and professional life to make sure you have the right life and disability insurance, use strategies to protect your assets from potential lawsuits, and ensure your business has a solid succession plan. It’s the ultimate safety net, giving you the confidence to go after your biggest goals.

Navigating the Great Wealth Transfer

We are on the verge of the largest hand-off of wealth in history. It presents a massive opportunity for high-net-worth families, but also carries significant risk. A wealth planner is the expert families turn to when navigating this shift.

The numbers are almost hard to comprehend. A recent analysis from UBS projects that a staggering USD 83 trillion will move from one generation to the next over the coming two decades. This gives families a once-in-a-lifetime chance to cement their legacy, but only if they manage the process with expert care.

Without a smart plan in place, that transfer can quickly become a source of family conflict and, ultimately, wealth destruction. This is where a wealth planner’s job becomes much more than just financial advice; they become a critical facilitator for the family itself.

The Planner as Family Guide

There's an old saying: "shirtsleeves to shirtsleeves in three generations." It’s a classic warning that family fortunes are often gone by the time the grandchildren are in charge. A wealth planner’s main job during a wealth transfer is to help break that cycle. They do it with more than just financial models—they use communication and education.

A huge part of their work is guiding families through difficult, but necessary, conversations between generations. They create a neutral, structured space where everyone can talk openly about goals, values, and expectations for the family’s wealth.

A wealth planner's true value is measured not just in portfolio returns, but in their ability to turn a potential family crisis into a foundation for multi-generational success.

They also serve as a mentor for heirs, getting them ready for the responsibilities that come with significant assets. This process often includes:

- Financial Stewardship Education: Teaching the next generation the fundamentals of budgeting, smart investing, and sound financial management.

- Defining a Family Mission: Helping the family articulate what the wealth is for—whether it's growing a business, funding philanthropic work, or providing for generations to come.

- Structuring for Success: Collaborating with legal experts to set up trusts and other structures that protect the assets and align with the family’s long-term vision.

Structuring a Lasting Legacy

A good planner goes beyond simple inheritance and dives into sophisticated legacy planning. This involves building a durable framework that can adapt as the family and the economy change over the decades.

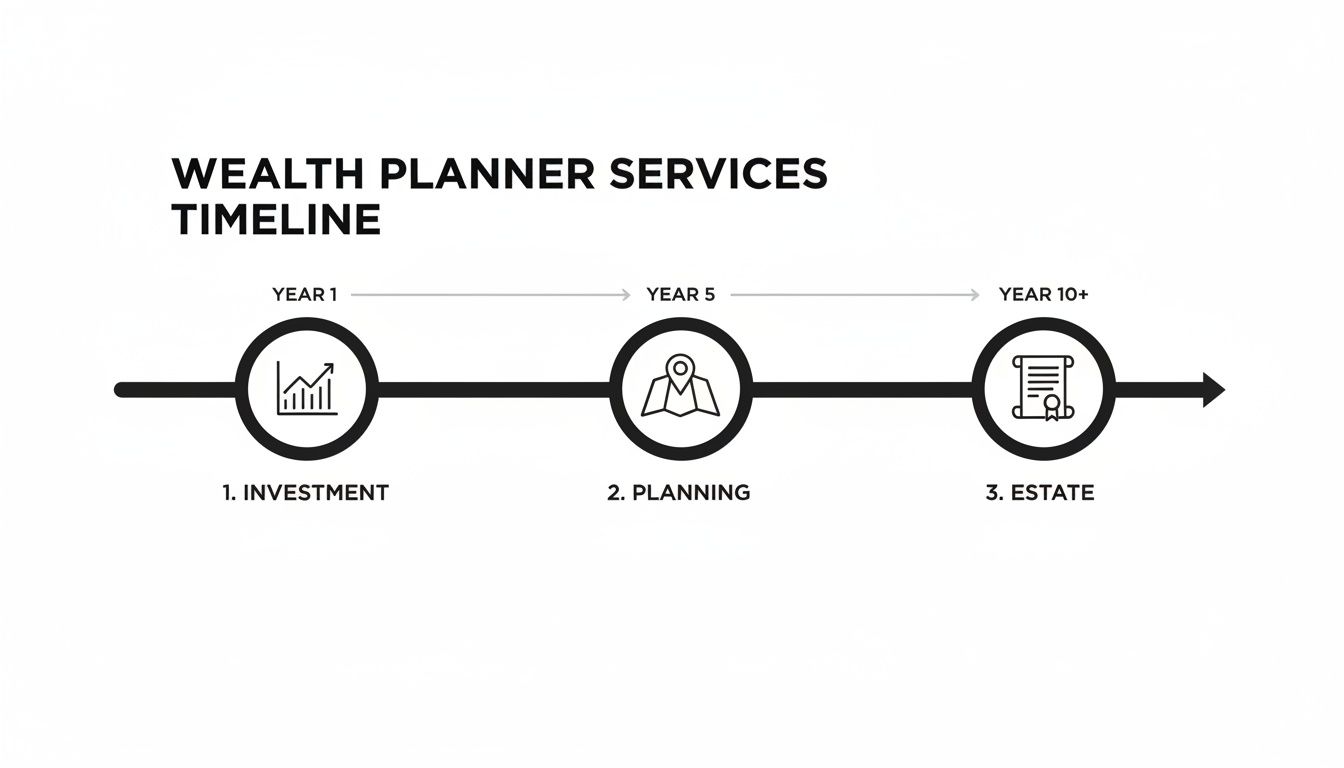

This timeline shows how a planner's focus evolves, starting with building the initial investment base and progressing toward preserving it for future generations.

As you can see, true legacy work is a long game. It culminates in complex estate strategies that are built on years of careful planning and investment management. If you're interested in taking this long-term approach, you can learn more about building generational wealth in our guide.

This is especially true for family offices, where managing shared assets across multiple branches of a family requires an expert, objective hand. By orchestrating the entire process, a wealth planner helps turn a simple inheritance into a lasting legacy.

Crafting Your Personalized Investment Strategy

Forget everything you think you know about cookie-cutter portfolios. A top-tier wealth planner starts from a completely different place, recognizing that your investment strategy should be as unique as you are. Their real job is to build a plan that’s deeply woven into the fabric of your life, not just to pick a few stocks and bonds.

This all kicks off with a serious deep dive into your world. A planner will want to understand your true tolerance for risk, the timeline for your biggest life goals, and even what you value most. The end result should feel like a direct reflection of who you are and where you want to go.

Building Beyond Public Markets

While stocks and bonds are the bedrock of most portfolios, a truly skilled wealth planner opens the door to a much wider universe of opportunities. They specialize in weaving alternative investments into a cohesive strategy, giving you a powerful advantage that’s impossible to get if you’re only playing in the public markets.

These alternatives are critical for real diversification. They can deliver returns that don't just follow the stock market's daily mood swings. Some of the most common avenues include:

- Private Equity: Taking direct ownership stakes in private companies, which offers the chance for huge growth before those companies ever hit the stock market.

- Hedge Funds: These are actively managed funds that use a whole playbook of strategies to chase returns, whether the market is going up or down.

- Private Credit: This is essentially becoming the bank and lending directly to businesses. It can provide higher, more stable income streams than you’ll find in the traditional bond market.

A great planner doesn't just hand you a menu of options. They meticulously vet these private deals, doing the exhaustive due diligence needed to protect your capital. This gives clients—from retirees and seasoned stock investors to professional entertainers—an edge they simply can't get on their own.

The Rise of Personalization and Alternatives

The entire industry is shifting to meet this demand. In the past, this degree of personalization and access to alternatives was a perk reserved only for the ultra-wealthy. Today, it’s becoming a core part of modern wealth planning. According to a 2026 report from MSCI on wealth trends, factors like unique investment preferences and complex tax optimization are driving this change. Research from Mercer's 2026 report shows the momentum, noting that an incredible 92% of financial advisors now use alternatives, with 91% planning to increase their allocations. You can dig deeper into how these trends are shaping the future by exploring the 2026 wealth trends research.

This confirms what we’ve seen for years: a sophisticated wealth planner must be fluent in both public and private markets to build a portfolio that can actually last.

The goal is to construct a portfolio that is not just built for growth, but is also fortified to withstand economic turbulence, aligning perfectly with your long-term objectives.

This integrated approach provides a level of financial security and opportunity that's tough to replicate with a conventional, public-market-only strategy. The careful blending of these diverse asset classes is what separates a premier wealth planner from the rest.

Expanding the Definition of Assets

A truly comprehensive investment strategy looks at every possible path for growth and protection. Beyond stocks, bonds, and even private equity, a forward-thinking planner will explore other asset classes that hold and grow value.

This might include tangible assets like fine art, collectibles, or even luxury timepieces. For anyone curious about these unique opportunities, an expert guide on how to start investing in luxury watches can be an excellent resource.

Ultimately, your wealth planner acts as your guide through this complex world, helping you understand the real risks and rewards of every piece of your portfolio. By combining traditional investments, exclusive private market deals, and even non-traditional assets, they build a robust and highly personal strategy designed to grow and protect your wealth for generations. This is what modern wealth management is all about.

How to Find and Vet the Right Wealth Planner

Choosing a wealth planner is one of the most critical financial decisions you’ll ever make. This isn't just about hiring an advisor; it's about forming a partnership built on a foundation of trust, shared vision, and a deep understanding of your life's goals.

Finding the right person requires a deliberate, almost investigative approach. You need to look past the polished website and the firm handshake to really get at the core of their philosophy and how they operate. Think of it as hiring the master architect for your family's financial future—you wouldn't rush that decision.

Start with the Non-Negotiables

Before you even start scheduling meetings, there are two foundational standards that are completely non-negotiable. Don't even consider a planner who doesn't meet both.

Fiduciary Duty: This is the absolute bedrock of a trustworthy relationship. A planner who is a fiduciary is legally and ethically required to act in your best interest, always. It means your financial well-being comes before their own compensation or their firm's bottom line. It's a simple, powerful promise.

Fee-Only Compensation: You want a planner who is paid directly by you, with zero ambiguity. This usually takes the form of a percentage of assets under management (AUM) or a straightforward flat fee. This structure guts the conflicts of interest that plague "fee-based" or commission models, where an advisor might be tempted to recommend a product because it pays them a higher kickback, not because it's the best fit for you.

Demand both. A true wealth planner will proudly operate as a fee-only fiduciary. It’s the only structure that ensures their advice is completely aligned with your success.

Verify Credentials and Experience

Once you've established that a potential planner is a fee-only fiduciary, it's time to scrutinize their qualifications. You're looking for respected professional designations that signal a serious commitment to expertise and ethics.

The two most recognized and rigorous designations in the industry are:

CFP® (Certified Financial Planner™): This is the gold standard for comprehensive financial planning. Holders have gone through extensive training, passed a notoriously difficult exam, and must adhere to a strict ethical code.

CFA® (Chartered Financial Analyst): The CFA charter is globally recognized as the pinnacle of achievement in investment analysis and portfolio management. It signifies a deep, technical mastery of investment strategy.

Don't just take their word for it. You can and should verify any planner's credentials and check for disciplinary history on the websites of the certifying bodies, like the CFP Board and the CFA Institute. It’s a simple step that provides immense peace of mind.

Conduct a Thorough Interview

This is where you move from checking boxes to finding the right personal fit. You need to prepare for this conversation with a list of pointed questions. Our guide on questions to ask a wealth manager is a great place to start building your list.

Make sure your interview digs into these key areas:

Investment Philosophy: Ask them to describe their approach in their own words, not just reciting a brochure. Are they believers in active management, passive indexing, or some combination? Where and how do they use alternative investments? Their answer should be clear and make sense to you.

Client Experience and Communication: Get specific. How often will you meet? What does a typical review meeting actually cover? Most importantly, how will they communicate with you when the markets inevitably get choppy?

Specialization: Do they have a track record of working with people in your exact situation? Whether you're a business owner navigating a complex exit, a retiree focused on capital preservation, or a professional athlete with unique income streams, their expertise must align with your specific needs.

Finding the right wealth planner is a journey, and the interview is perhaps the most crucial stop. It's your opportunity to vet not just their expertise, but their character. To help you prepare for this critical step, we've compiled a list of essential questions to ask.

Key Questions to Ask a Potential Wealth Planner

This table provides a checklist of key questions to help you evaluate and select a wealth planner who truly aligns with your financial goals and values.

| Category | Question to Ask | Why It Matters |

|---|---|---|

| Philosophy & Ethics | Are you a fiduciary at all times, and will you put that in writing? | This is the most important question. You need unwavering confirmation that they are legally obligated to act in your best interest. |

| Compensation | How are you compensated? Are you fee-only, or do you earn commissions? | This uncovers potential conflicts of interest. Fee-only is the cleanest model, ensuring advice is unbiased. |

| Investment Strategy | What is your investment philosophy, and why do you believe it's effective? | You're looking for an approach that is disciplined, well-researched, and aligns with your own risk tolerance and long-term goals. |

| Client Profile | What does your typical client's financial situation look like? | This helps determine if they have experience with situations like yours (e.g., business owners, retirees, family offices). |

| Service & Communication | What does your client service model look like? How often will we communicate? | Establishes expectations for ongoing support, meeting frequency, and how they handle client relationships. |

| Team & Firm | Who will be on my team? What is the background of the people I will be working with? | You're not just hiring one person. You're hiring a firm and a team. Understand the depth of the resources you're getting. |

| Performance Reporting | How do you measure and report on portfolio performance? | You need clear, transparent reporting that shows how your investments are performing against relevant benchmarks, net of all fees. |

These questions are your toolkit for a productive interview. Don't be afraid to ask follow-up questions and press for clarity. A great planner will welcome the detailed inquiry and have thoughtful, transparent answers. It's a sign they take their role as seriously as you do.

The Commons Capital Partnership: A Bespoke Approach

Knowing what a wealth planner does is one thing. Finding one who has the technical chops and genuinely understands the messy, wonderful complexities of your life is another thing entirely. We built Commons Capital on that very idea: that true financial strategy requires deep personalization and the experience to guide you through major life and financial events.

Our work goes far beyond standard financial advice. Think of us as the architect for your financial legacy—someone who designs the blueprint, but also sticks around to make sure it’s built with precision and care. For us, a win is seeing every component of your financial world, from sprawling investments to delicate family dynamics, work together to bring your vision to life.

Expertise Tailored to Your World

We've intentionally focused our practice on clients whose financial lives simply demand a higher degree of coordination and insight. This focus allows us to provide real value where it counts the most.

High-Net-Worth Individuals & Families: Once your investable assets cross the $500,000 mark, complexity becomes the norm. We step in as the central hub, working with your other professional advisors to make sure your investment, tax, and estate plans are all pulling in the same direction.

Family Offices: We operate as a natural extension of your team. We can provide the specialized investment analysis and strategic oversight needed to manage wealth across generations and keep your family’s mission on track.

Sports & Entertainment Professionals: Careers in sports and entertainment follow a unique financial curve—think high peak earnings and very specific planning challenges. We build durable financial plans designed to protect that wealth, ensuring it supports you for a lifetime, long after the final curtain call.

We believe exceptional wealth planning isn’t about selling products. It’s about building a relationship founded on trust, transparency, and a shared commitment to your long-term prosperity.

Begin Architecting Your Financial Future

Choosing a wealth planner is a huge decision. The right partnership can set the financial course for your family for generations to come. If our way of thinking resonates with you, we should talk.

Let's explore what a truly customized financial plan could do for you and your family. We offer a confidential, no-obligation consultation to hear about your goals and see if we're the right fit to help you get there. It’s a chance for you to ask the tough questions and for us to show you the clarity and direction we can bring to your financial life.

This is about more than just managing money; it's about building the framework for your future. To take the next step and see how the right wealth planner can make all the difference, schedule your confidential consultation with Commons Capital today. Let's build your legacy, together.

Frequently Asked Questions About Wealth Planners

Even after you’ve decided you need help, hiring a wealth planner is a big step. It's only natural to have a few more questions before you commit.

Clarity is everything when it comes to your money. Here are some of the most common questions we get—and the straight answers you deserve.

What Is the Minimum Net Worth to Need a Wealth Planner?

There isn’t a single magic number, but these comprehensive services really start to make a difference once your financial life gets complicated.

Generally, you’ll feel the full impact once you have at least $500,000 in investable assets. This is the point where challenges like sophisticated tax planning, access to private investments, and complex estate questions usually pop up.

Below that level, the cost might outweigh the benefits. But as your wealth grows, the need for a financial quarterback becomes undeniable.

How Are Wealth Planners Compensated?

You have to know how your planner gets paid. It's the only way to be sure your interests are truly aligned.

The most transparent and client-first model is "fee-only" compensation. Here, the planner is paid directly by you—either as a small percentage of the assets they manage (AUM) or through a simple flat retainer.

Always confirm that a prospective planner is a fiduciary and operates on a fee-only basis. This structure removes the conflicts of interest found in "fee-based" models, where advisors might earn hidden commissions for selling certain financial products.

This clean arrangement ensures their advice is driven by what's best for you, not by a potential commission check.

How Often Will I Communicate With My Wealth Planner?

The right communication rhythm is the one that works for you, and you should iron this out from the start. A solid relationship usually involves in-depth review meetings at least once or twice a year to track your progress and make any needed adjustments.

But it goes beyond scheduled check-ins. A great planner is proactive. You should expect to hear from them during major market shifts, when tax laws change, or after a big life event like a business sale or inheritance.

They should be on call when you need them, making sure you feel supported every step of the way.

What Is the Difference Between a Wealth Planner and a Financial Advisor?

This is a critical distinction, even though people often use the terms interchangeably. Think of it like the difference between a general practitioner and a top surgeon who also coordinates your entire team of specialists.

A Financial Advisor typically focuses on one thing: investment management. Their main job is to build and manage a portfolio of stocks, bonds, and funds to help you hit your targets.

A Wealth Planner takes a 360-degree view of your entire financial world. They’re your financial quarterback, weaving investment strategy together with advanced tax planning, estate design, risk management, and even your family's philanthropic goals.

A financial advisor manages one piece of the puzzle. A wealth planner makes sure every single piece fits together perfectly.

At Commons Capital, we believe true wealth management is a partnership. If you’re ready to move from simply managing assets to architecting a comprehensive financial future, we invite you to learn more. Start your journey by visiting us at https://www.commonsllc.com.