Effectively protecting assets from nursing home costs begins with a candid look at the immense financial challenge your family could face. It’s not just about paying for care; it's about using proactive strategies, like trusts and Medicaid planning, to shield a lifetime of savings from being wiped out by long-term care expenses.

The Reality of Nursing Home Costs Today

The thought of a loved one needing long-term care is emotional enough without the crushing weight of the financial burden. For too many families, the reality of these expenses only hits when a crisis occurs, which is often too late to put the best asset protection strategies in place.

Imagine working for decades to build a comfortable nest egg, only to watch it vanish in a matter of months. That’s not an exaggeration; it’s a painfully common story for families who underestimate the relentless expense of skilled nursing care.

The Staggering Financial Impact

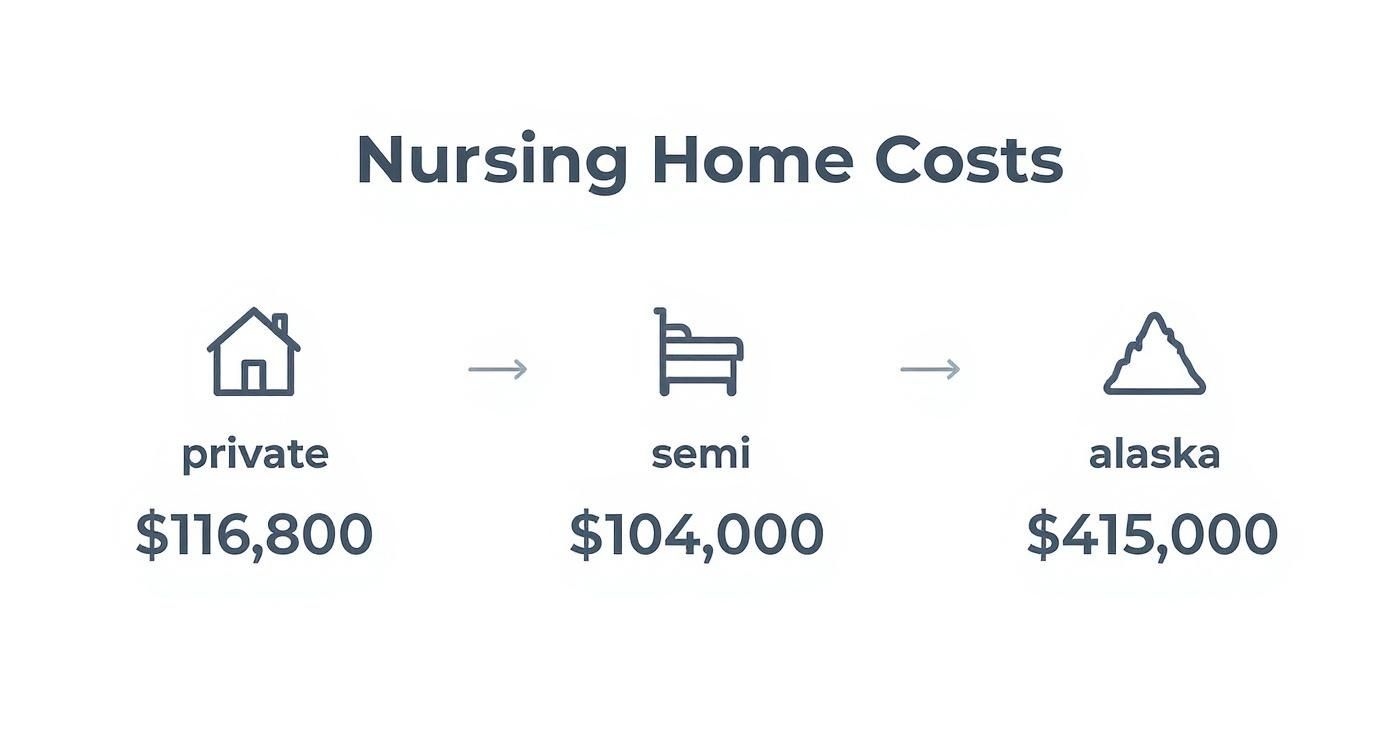

The cost of nursing home care in the United States has continued its sharp upward climb, putting seniors and their families at significant financial risk. Recent data shows the median annual cost for a private room in a nursing home is now around $116,800, with semi-private rooms not far behind at just over $104,000 per year.

These figures can swing wildly depending on where you live. For instance, care in Alaska can soar to a breathtaking $415,005 annually, while a state like Missouri is closer to $78,000. These statistics highlight the varied financial landscape of long-term care.

This kind of financial pressure makes it painfully clear why a simple savings plan often isn't enough. Without a dedicated asset protection strategy, a multi-year stay can easily consume an entire retirement portfolio, leaving nothing for a surviving spouse or the next generation.

Why You Cannot Afford to Wait

When it comes to long-term care planning, procrastination is the single biggest threat to your financial legacy. Many of the most powerful legal tools require years to become fully effective, which makes taking action early absolutely critical.

The goal isn't just to pay for care; it's to preserve the financial security and dignity you've worked your entire life to achieve. Understanding the scale of the problem is the first step toward proactive, empowered planning.

While financial planning is essential, it’s also valuable to know that alternatives can sometimes reduce the need for these facilities. For families looking at different options, exploring how care at home can positively replace traditional care homes provides a broader perspective on managing care needs.

Ultimately, facing these daunting figures isn’t about creating fear—it’s about building a foundation for a secure future. By acknowledging the reality of these costs, you can shift from a position of worry to one of informed action, ready to explore the proven strategies that can protect your family’s legacy.

Understanding Your Medicaid Planning Options

For many families, Medicaid is the last line of defense against the staggering costs of long-term care. But qualifying for it isn't automatic—it demands careful, proactive planning. Medicaid is a joint federal and state program, which means the rules can vary, but its core purpose is to help people with limited income and resources cover their medical bills.

Successfully protecting your assets from nursing home costs almost always involves navigating Medicaid's very strict financial eligibility rules.

This can feel incredibly complicated, but it really boils down to two things: your income and your "countable" assets. While the exact numbers change from state to state, an individual can typically only have a few thousand dollars in countable assets to qualify for nursing home benefits.

This financial reality is a huge deal, especially when you look at the numbers. There are roughly 1.16 million seniors in U.S. nursing homes, and anyone turning 65 today has a 70% chance of needing some form of long-term care in their lifetime. With Medicaid footing the bill for about 62% of this care, its tight asset limits create a major hurdle for countless families.

This infographic gives you a quick snapshot of just how much nursing home costs can vary, hammering home the need to plan ahead.

As you can see, where you live makes a huge difference, with places like Alaska having astronomical expenses. This just reinforces why you can't afford to ignore this, no matter where you are.

The Critical Medicaid Look-Back Period

If there’s one concept you absolutely must understand in Medicaid planning, it’s the look-back period. This is a five-year window (in most states) where Medicaid scrutinizes every single financial transaction you’ve made. They are looking for one thing: assets that you gave away, transferred, or sold for less than what they were worth.

If they find any improper transfers, they will hit you with a penalty period. This is a stretch of time where you will be flat-out ineligible for benefits, even if your assets are now low enough to qualify.

The math is simple and brutal. They calculate the penalty by dividing the total value of the gifts by the average monthly cost of a nursing home in your area. For instance, if you gave your kids $150,000 and the average local care cost is $10,000 a month, you’re facing a 15-month penalty period. That’s over a year you’ll have to pay for care completely out of pocket.

Strategically Spending Down Your Assets

When your assets are over the limit, you have to "spend down" the excess before Medicaid will step in. This doesn't mean you have to burn through your life savings on useless things. A smart spend-down is about using your money on permissible expenses that benefit you or your spouse, all while legally reducing your countable assets.

The goal isn't to just get rid of your money. It's about converting countable assets into non-countable ones or paying for legitimate needs, preserving your quality of life while moving you closer to eligibility.

Think of it as smart reallocation, not senseless spending. By focusing on allowed purchases and payments, you can meet Medicaid’s rules without destroying the nest egg you worked so hard to build.

To get a clearer picture of what's at stake, it helps to understand what Medicaid considers "countable." The table below breaks down the typical categories.

Exempt vs Countable Assets for Medicaid Eligibility

As you can see, the distinctions are crucial. A strategic spend-down focuses on moving funds from the "Countable" column to the "Exempt" one.

Allowable Expenses for a Medicaid Spend-Down

So, what are some smart, effective ways to spend down assets without getting penalized? Here are some of the most common strategies I’ve seen work for clients:

- Wipe out your debts. Paying off your mortgage, credit cards, or a car loan is one of the cleanest ways to reduce cash on hand.

- Make your home safer. Spending on home modifications like wheelchair ramps, walk-in showers, or stairlifts is a permissible expense that helps you stay at home longer.

- Buy a reliable vehicle. If your current car is on its last legs, purchasing a new one is an allowable way to spend down.

- Pre-pay for final expenses. You can set up an irrevocable funeral trust or purchase a burial plot for yourself and your immediate family. This is an exempt expense.

- Catch up on personal care. Need dental work, new glasses, or better hearing aids? These are often permissible expenses that directly improve your quality of life.

- Handle certain retirement accounts. The rules around retirement accounts like a 401(k) or IRA can be a minefield, as some are countable. You can learn more by checking out our guide on whether IRAs are protected from creditors.

Each of these moves allows you to legally lower your countable assets while getting something of real value in return. It's all about careful planning to get the help you need while protecting what you can.

Using Trusts to Safeguard Your Legacy

When it comes to protecting assets from nursing home costs, few tools are as powerful—or as misunderstood—as a trust. For many, the word itself brings to mind sprawling estates and old money. In reality, a specific type of trust is the cornerstone of modern Medicaid planning for everyday families.

This legal instrument allows you to transfer ownership of your assets into a separate entity, effectively taking them out of your name. By doing this, you can legally shield those assets from being counted by Medicaid, preserving your life's savings for your loved ones.

Irrevocable Trusts: The Gold Standard for Asset Protection

The key to this entire strategy is the Irrevocable Trust, often called a Medicaid Asset Protection Trust (MAPT). Once you place assets like your home or investments into this trust, you legally give up direct control and ownership. This is the critical step that protects them.

This stands in stark contrast to a Revocable Living Trust. While a living trust is an excellent tool for avoiding probate and managing your affairs if you become incapacitated, it offers zero protection from nursing home costs. Because you can change or dissolve a revocable trust at any time, Medicaid considers its assets to still be yours. For a deeper dive into the differences, our article comparing a living trust vs. a will can provide more clarity.

The distinction is simple, but it has massive financial implications. Only an irrevocable trust creates the legal separation needed to shield your life's savings from being depleted by long-term care expenses.

Addressing the Biggest Fear: Losing Control

The word "irrevocable" can be intimidating. It sounds permanent and final, leading many people to fear they'll lose all access to the assets they've worked so hard for. However, a properly drafted trust is designed to address this very concern.

While you give up direct ownership, you can still keep certain rights and control. For instance:

- You can choose the trustee. This person, often a trusted adult child or a professional, manages the trust according to the rules you set. You can also keep the power to change the trustee if you're unhappy.

- You can receive income. The trust can be structured to pay any income it generates—like stock dividends or rent from a property—directly to you.

- You can live in your home. If you place your primary residence in the trust, you can include provisions that give you the absolute right to live there for the rest of your life.

The goal of an Irrevocable Trust isn't to lock you out of your own life. It's to build a protective wall around your assets that Medicaid cannot breach, while ensuring you can still enjoy the benefits of what you've built.

This approach requires navigating a complex interplay of public funding programs and private financial tools, with Medicaid being a crucial factor. The high cost of formal care often pushes families to use strategies like trusts to qualify for public programs. You can discover more insights about long-term care planning around the world on nber.org.

A Real-World Scenario: Protecting a Family's Future

Let's look at how this works in practice. Meet David and Sarah, both 65. They own their home outright (valued at $450,000) and have a non-retirement investment portfolio worth $300,000. They're in good health but are worried about the future cost of long-term care.

Following the advice of an elder law attorney, they decide to create a Medicaid Asset Protection Trust.

- Asset Transfer: They transfer the deed of their home and their $300,000 investment portfolio into the newly created trust. Their daughter, Emily, is named the trustee.

- Retaining Benefits: The trust document specifies that David and Sarah have the legal right to live in the home for life. It also directs that all dividend income from the investments be paid to them annually.

- Starting the Clock: The day the assets are transferred into the trust, the crucial five-year look-back period clock begins to tick.

Fast forward six years. David's health declines, and he now requires skilled nursing care. Because their home and investments have been in the Irrevocable Trust for more than five years, they are completely protected. Medicaid does not consider them countable assets.

This single strategic move allows Sarah to continue living in her home without fear of a Medicaid lien. The investment portfolio remains untouched, preserved as an inheritance for Emily. Most importantly, David is able to qualify for Medicaid to cover the high cost of his care without the family first going bankrupt. This scenario shows just how critical proactive planning can be.

Exploring Advanced Protection Strategies

While an Irrevocable Trust is a powerful tool for planning far in advance, what happens when you’re facing a more immediate crisis? The good news is, you still have options. Several advanced strategies can be used for protecting assets from nursing home costs, even when you don't have the luxury of a five-year runway.

These methods are designed for specific, often urgent, situations—from last-minute planning to handling unique assets like your family home. Each approach comes with its own set of rules and benefits, so it’s essential to understand which one might align with your family’s needs. These are definitely not DIY solutions; they require precise execution with the help of a qualified elder law attorney.

Long-Term Care Insurance

For those who plan well ahead, Long-Term Care (LTC) insurance is often the first line of defense. It’s a private policy designed specifically to cover the costs of skilled nursing, assisted living, or in-home care. The benefit is straightforward: the insurance pays for care without forcing you to burn through your life savings first.

But LTC insurance isn't for everyone. The premiums can be expensive, and you generally have to be in decent health to qualify. For many, the high cost is a deal-breaker, but for those with substantial assets to protect, it can be a worthwhile investment to preserve their legacy for the next generation.

Medicaid Compliant Annuities

When a crisis hits and one spouse needs nursing home care right away, a Medicaid Compliant Annuity (MCA) can be an absolute lifesaver. This is a highly specialized financial product designed for a very specific scenario: a married couple where one spouse (the "institutionalized spouse") is entering a nursing home, and the other (the "community spouse") is still living at home.

Here’s how it works: the couple spends down their excess countable assets by purchasing an MCA in the name of the community spouse.

- Instant Conversion: The MCA immediately converts a lump sum of countable cash into a non-countable income stream for the healthy spouse.

- Immediate Eligibility: This single move can make the institutionalized spouse instantly eligible for Medicaid benefits.

- Income Preservation: The annuity payments provide a steady, predictable income to the community spouse, helping them maintain their lifestyle without financial hardship.

This strategy is one of the most powerful tools in crisis planning. It allows a family to protect a huge portion of their savings from being spent down on care, ensuring the financial security of the spouse who remains at home.

Life Estate Deeds for Real Estate

Your home is often your most valuable asset, and protecting it is usually priority number one. A Life Estate Deed is a legal tool that lets you transfer ownership of your property to a beneficiary (like your children) while you keep the absolute right to live in it for the rest of your life. The person living in the property is the "life tenant," and the future owner is the "remainderman."

This strategy effectively removes the home from your probate estate and, crucially, starts the five-year look-back clock for Medicaid. After five years, the home's value is generally protected. But you need to understand the trade-offs. Once the deed is created, you can’t just sell or mortgage the property without the consent of the remainderman. There can also be tax implications that need careful consideration with your attorney.

A primary goal of asset protection is often to enable individuals to remain at home. Learn more about effective in-home support to avoid nursing home care and preserve your legacy.

Using a Family Limited Liability Company

For families with more complex assets—think business interests or multiple real estate properties—other legal structures might make more sense. A Family Limited Liability Company (FLLC) can offer another layer of protection and control over these assets.

While it's not a direct Medicaid planning tool on its own, an FLLC can be a key part of a larger, more sophisticated strategy. If you're looking to understand how these entities work, you can explore the details of a Family Limited Liability Company in our comprehensive guide. These advanced strategies show that even in urgent situations, there are powerful options available for protecting what you've worked so hard to build.

Costly Planning Mistakes and How to Avoid Them

Knowing what not to do when protecting assets from nursing home costs is every bit as important as knowing which strategies to use. I’ve seen countless families make well-intentioned moves, often based on advice from friends or neighbors, that backfire spectacularly.

These simple missteps can lead to devastating financial penalties and, worst of all, disqualification from Medicaid right when you need it most. A single error can easily trigger a penalty period, leaving you to pay for incredibly expensive care out-of-pocket for months or even years.

The Danger of Gifting Money to Family

One of the most frequent mistakes I see is people simply giving away money or property to their children. It seems like a perfectly logical way to reduce your net worth on paper, but to Medicaid, it’s a giant red flag.

Any gift made within the five-year look-back period is flagged as an improper transfer. For example, let's say you give your son $120,000 to help with a down payment on a house. If the average nursing home in your state costs $10,000 per month, that generous gift just created a 12-month period of Medicaid ineligibility. You’ll be on the hook for the full cost of care during that time.

Instead of making outright gifts, a much safer approach is to transfer assets into a properly structured Irrevocable Trust. This starts the five-year clock on your terms and provides a legal shield that simple gifting does not.

Putting a Child's Name on Your Deed or Bank Account

Another common trap is adding an adult child's name to your house deed or bank accounts. While this might seem like a simple shortcut to pass on assets and avoid probate, it creates enormous risks you probably haven't considered.

The moment you make your child a co-owner, you expose your assets to their entire financial life. If they go through a messy divorce, get sued after a car accident, or have to declare bankruptcy, your home and your savings could be seized by their creditors. It's no longer just your asset; legally, it becomes theirs as well.

It's a tough but essential lesson: understanding the most common errors is the first step toward building a plan that actually works.

To make it easier, I've put together a quick summary of the most frequent missteps I see in my practice and the correct strategies you should be using instead.

Common Planning Mistakes and Better Alternatives

Looking at this, you can see how easy it is to make a move that feels right but has serious unintended consequences.

The Pitfall of Waiting Too Long

If there's one mistake that does more damage than any other, it's procrastination. Many of the most powerful strategies for protecting your assets, like using an Irrevocable Trust, are completely dependent on clearing that five-year look-back period.

If you wait until a health crisis strikes, your options shrink dramatically. Starting the planning process in your early to mid-60s gives you the best chance to put a rock-solid plan in place and let the five-year clock run out. While crisis planning is sometimes possible, the strategies are far more restrictive and may not protect as much of your legacy.

Your future self will thank you for taking action today.

Answering Your Key Planning Questions

Navigating the world of long-term care planning often feels like learning a new language. It naturally brings up some critical, and sometimes stressful, questions. Getting clear, straightforward answers is the only way to move forward with confidence and protect your assets from nursing home costs.

Let's cut through the noise. Below, we're tackling the most common concerns we hear from families just like yours. Think of this as a practical FAQ designed to give you the clarity you need to take the next step.

How Early Should I Start Planning?

If there's one piece of advice I can give, it's this: start early. The ideal time for most people is in their early to mid-60s. This isn't just an arbitrary number; it's strategically tied to Medicaid's five-year "look-back" period.

By getting your planning in place at least five years before you might need care, you give yourself access to the most powerful asset protection tools, like an Irrevocable Trust. Once that five-year clock has run out on a transfer, the assets you've properly shielded are generally safe from being counted by Medicaid.

But let me be clear: while starting early is ideal, it is never too late to explore your options. Even in a crisis situation, there are still specific strategies, like a Medicaid Compliant Annuity, that can help protect a significant portion of your assets.

Don't let the feeling that you've "waited too long" stop you from seeking advice. There are always steps you can take.

Can the Nursing Home Take My House?

This is one of the biggest and most persistent myths in long-term care planning. The short answer is no, a nursing home cannot simply "take" your house. They are healthcare providers, not debt collectors who can seize your property.

However, the real threat to your home comes from Medicaid itself. If Medicaid pays for your long-term care, the state has the right to try and recover those costs from your estate after you pass away. This process is called Medicaid Estate Recovery, and your home is often the most valuable asset available to them.

So, while they won't seize the deed while you're alive, they can place a lien on the property. That lien must be paid off before the home can be passed on to your heirs. Fortunately, you have several powerful strategies to prevent this from happening:

- Spousal Protections: Your home is generally protected as long as a spouse, a minor child, or a disabled child lives there.

- Irrevocable Trusts: Placing your home in a specially designed trust more than five years before needing care removes it from your countable estate entirely.

- Life Estate Deeds: This tool can transfer ownership to your heirs while letting you live in the house for the rest of your life, which also starts the five-year clock.

Do I Really Need an Elder Law Attorney?

I know it’s tempting to try and handle this process on your own to save a few dollars. But in my experience, it's one of the most financially dangerous mistakes a family can make. Medicaid's rules are incredibly complex, constantly changing, and vary significantly from state to state. This is not a DIY project.

An experienced elder law attorney does far more than just fill out paperwork. They are strategists who live and breathe this intricate legal landscape. Their job is to:

- Analyze your unique family and financial situation.

- Create a personalized, legally sound plan to protect your specific assets.

- Help you avoid the devastating penalties that come from simple, unintentional mistakes.

- Guide you through a crisis with proven, lawful strategies when time is short.

Hiring a specialist isn't an expense; it's an investment in protecting your entire life's savings from being needlessly spent down to zero.

At Commons Capital, we understand that protecting your legacy is paramount. Our team is dedicated to helping you manage your wealth and achieve your long-term financial goals with confidence. If you're ready to build a robust financial plan, contact us today.