Smart social security claiming strategies are about much more than just picking an age. They’re about treating your benefit like the valuable financial asset it is. The right approach weaves your Social Security decision into your total wealth picture, factoring in taxes, longevity, and spousal benefits to get the most out of your lifetime income. Optimizing your retirement income involves knowing the best time to claim Social Security, and this guide will help you understand the core factors at play.

Rethinking Social Security as a Strategic Asset

For many affluent families, Social Security can seem like an afterthought—a minor check compared to a large investment portfolio. This perspective is a massive missed opportunity.

Your Social Security benefit is a unique asset: it's backed by the government, adjusts for inflation, and can easily be worth hundreds of thousands of dollars over your lifetime. The real question isn't if you should care about it, but how to get the most value from it within your comprehensive financial plan.

This means looking past generic advice. The common wisdom to delay until age 70 often boils down to a simple breakeven calculation that doesn't capture the complex reality high-net-worth investors face.

More Than a Simple Breakeven Number

A truly effective strategy looks at the whole board. It’s a sophisticated analysis that balances several moving parts, especially with policy risk on the horizon. The Social Security Administration's own projections suggest its main trust fund could face depletion between 2033 and 2035, adding another layer to the decision.

For those with $1,000,000 or more in wealth, advanced models from firms like NewRetirement often show the optimal claiming age might be younger than 70. This kind of research accounts for the fact that retirement spending isn’t a straight line—it often follows "go-go," "slow-go," and "no-go" phases. You can find more details on how wealth influences the best claiming age.

For affluent investors, the decision is less about hitting a single breakeven age and more about unlocking value. The right social security claiming strategies can provide early-retirement liquidity, create tax-planning opportunities, and secure a stronger financial foundation for a surviving spouse.

Key Factors in Your Claiming Decision

To build a retirement strategy that fits your life, you must see how all the pieces of your financial puzzle interact. The goal is to make a deliberate choice that supports your long-term vision, not just fall back on default advice.

The decision really comes down to these core areas:

- Longevity and Health: Your health and family history are huge factors. A long life expectancy can make delaying more attractive, but you must weigh that against funding an active lifestyle in your early retirement years.

- Spousal and Survivor Needs: For married couples, coordinating benefits is crucial. A smart strategy can significantly boost your combined lifetime income and, critically, leave a much larger survivor benefit for the spouse who lives longer.

- Tax Implications: Your claiming decision directly impacts your tax bill. It can open the door for strategic Roth conversions or, if not carefully managed, push you into a higher tax bracket and increase your Medicare premiums (IRMAA).

- Overall Wealth and Income Sources: Your Social Security timing should harmonize with other income, like pensions and portfolio withdrawals. For instance, claiming early could provide the cash flow to avoid selling investments when the market is down.

Key Social Security Claiming Ages and Their Impact

To see how this plays out in practice, it helps to have a quick reference for the major claiming milestones. The table below breaks down the key ages and what they mean for your benefit amount.

Ultimately, this table illustrates the trade-offs: liquidity now versus larger checks later. Your personal circumstances will determine which path makes the most sense for you and your family.

Understanding Your Core Social Security Choices

Picking when to start your Social Security benefits is one of the most important financial decisions you'll make for retirement. It's not a one-size-fits-all answer; it’s about finding the move that best fits your personal financial picture. At its heart, every Social Security strategy comes down to three main choices: claiming early, waiting until your Full Retirement Age, or holding out for the biggest possible check.

Each option presents a classic trade-off: Do you want cash in hand sooner, or a larger, guaranteed income stream for the rest of your life? Let's walk through these fundamental choices to see how they stack up.

Claiming Early at Age 62

You can start taking benefits as soon as you turn 62. This is the earliest you can claim, and it's the go-to option if you need an immediate income stream. For many, it's the key that unlocks an early retirement, helps bridge an income gap, or simply provides cash for the active "go-go" years.

But this early access comes with a permanent catch. Your monthly check will be cut by as much as 30% compared to what you'd get at your Full Retirement Age. That's a permanent reduction, locked in for life.

This path often makes sense for individuals who:

- Have to retire and simply need the income.

- Face health issues or have a family history that suggests a shorter life expectancy.

- Prioritize funding travel and experiences right now, rather than later.

For high-net-worth investors, there's another perspective. Some analyses, like this one from the CFA Institute's blog, suggest that claiming at 62 and investing the money can create a significant pool of capital upfront. When factoring in realistic life expectancies, claiming early can sometimes lead to greater overall wealth than delaying.

Claiming at Full Retirement Age (FRA)

Waiting until your Full Retirement Age (FRA) is the baseline strategy. For anyone born in 1960 or later, your FRA is 67. If you claim then, you receive 100% of your primary insurance amount (PIA)—the full benefit you've earned over your working years.

Think of FRA as the neutral ground. You avoid the permanent haircut you get for claiming early, but you don't get the bonus credits that come from waiting longer.

This is a solid, middle-of-the-road choice for millions of retirees. It's especially smart if you're still working. If you claim before FRA while earning an income, the "earnings test" can temporarily reduce your benefits. Once you hit your FRA, that test goes away completely.

Delaying for Maximum Benefits at Age 70

The third option is a game of patience: waiting all the way until age 70 to claim. For every single year you delay past your Full Retirement Age, the Social Security Administration gives you Delayed Retirement Credits. These credits boost your future benefit by 8% a year.

By waiting from an FRA of 67 to age 70, you'll get a monthly check that's 24% bigger—for life. This is the largest benefit you can possibly get, and like all Social Security income, it's indexed to inflation. You can model this difference yourself using a Social Security benefits calculator to see the numbers in black and white.

Holding out until 70 is often the best move for those who:

- Are healthy and expect to live well into their 80s or 90s.

- Have enough other income or savings to comfortably bridge the years from FRA to 70.

- Are the higher earner in a marriage and want to lock in the largest possible survivor benefit for their spouse.

Coordinating Spousal Benefits for Maximum Advantage

For married couples, viewing Social Security as two separate checks is a missed opportunity. The real power comes from treating your benefits as a single, coordinated asset. It's a team sport, and running the right play can add tens, or even hundreds, of thousands of dollars to your lifetime retirement income.

This coordinated approach is absolutely essential for couples with different lifetime earning histories. A smart strategy provides income when you need it while also maximizing your long-term payout. But most importantly, it protects the surviving spouse.

The Power of the Split Strategy

One of the most effective social security claiming strategies for couples is often called a "Split Strategy." The idea is simple but powerful: one spouse—typically the lower earner—claims benefits early to get cash flowing, while the higher-earning spouse delays as long as possible.

By waiting, the higher earner’s benefit grows by a guaranteed 8% for each year they delay past their Full Retirement Age (FRA), all the way up to age 70. This delay doesn’t just boost their future monthly check; it fundamentally increases the financial safety net for both of you.

The crucial part of this play is what happens down the road. When one spouse passes away, the survivor gets to keep the larger of the two Social Security benefits. So, by having the higher earner delay, you are directly increasing the value of that survivor benefit, which will last for the rest of the surviving spouse's life.

This coordinated play isn't just about maximizing numbers on a spreadsheet. It's about legacy planning and ensuring the spouse who lives longer maintains their financial stability and quality of life without compromise.

This is a cornerstone of sound retirement planning, especially where one partner was the primary breadwinner. A recent analysis from Nasdaq confirms the power of this dual-benefit approach. For married couples with a notable income gap, having the lower-earning spouse claim early while the higher-earning spouse waits until 70 is the optimal move. This structure maximizes the survivor benefit, potentially adding up to hundreds of thousands in additional lifetime income. You can read more on this strategy from Nasdaq.

Case Study: The Andersons' Coordinated Claim

Let's put this into practice with an example. Meet David and Susan. David was the higher earner, while Susan worked part-time and was the primary caregiver for their children.

- David's Situation: At his FRA of 67, his benefit is $3,000 a month. If he delays to age 70, that grows to $3,720 per month—a 24% raise.

- Susan's Situation: Her FRA benefit at 67 is $1,400 per month. If she claims at the earliest age, 62, it’s reduced to $980 a month.

A common, but far from optimal, move would be for both to claim at 67. They would get a combined $4,400 per month. But a split strategy delivers a much better long-term result.

The Split Strategy in Action

- Susan Claims Early: At age 62, Susan files for her benefit. She starts receiving $980 per month, giving the couple an immediate income stream to help fund their early retirement adventures.

- David Delays: David holds off, waiting until age 70 to claim his benefit. By doing so, he locks in his maximum possible monthly payment of $3,720.

- The Long-Term Impact: Years later, when David passes away, Susan's smaller $980 benefit stops. But she then "steps up" to his much larger survivor benefit, receiving $3,720 per month for the rest of her life.

If they had both claimed at their FRA, her survivor benefit would have been just $3,000 per month. The split strategy permanently increased her financial security by $720 every single month, for life, all adjusted for inflation. It's a perfect example of how thoughtful social security claiming strategies can transform two individual benefits into one powerful financial plan.

Integrating Social Security into Your Total Wealth Picture

Your Social Security claiming decision isn't something to figure out in a vacuum. It’s a strategic choice that ripples across your entire financial life, and for affluent investors, treating it as an afterthought is a serious mistake.

Think of it as a central gear in your financial engine. The timing of your claim directly affects your taxes, your investment withdrawals, and even your healthcare costs. The right social security claiming strategies don't just determine when you get a check—they synchronize this income stream with your bigger financial goals. Get it right, and you can unlock some powerful opportunities. Get it wrong, and you could be dealing with the fallout for decades.

The Tax Implications of Your Claiming Decision

As soon as you start receiving Social Security, your tax picture changes. Your benefits get added to what the IRS calls "provisional income," a formula that includes your adjusted gross income, tax-free interest, and half of your Social Security benefits.

Based on that number, up to 85% of your benefits can suddenly become taxable. This new income can easily be enough to bump you into a higher tax bracket, a phenomenon sometimes called the "tax torpedo."

But this interaction also opens a window for smart planning. By delaying Social Security, you can keep your provisional income low during your 60s. This creates a valuable opportunity for some tax-savvy moves.

A lower-income period before claiming can be the perfect time to execute Roth conversions. By moving money from a traditional IRA to a Roth IRA, you pay taxes on it now, at what might be a lower rate. This builds a pool of tax-free money you can tap into later, after your Social Security benefits might have pushed your income—and your tax bracket—higher.

Seeing how Social Security fits with your broader retirement plan is a cornerstone of smart wealth management. You can explore more comprehensive financial planning resources to make sure all the pieces are working together.

Protecting Your Portfolio During Market Volatility

There’s another powerful connection here: the one between your claiming age and your investment withdrawal plan. Taking benefits earlier can create a stable, predictable cash flow that has nothing to do with the stock market's daily gyrations.

Having that reliable Social Security check every month means you might not have to sell investments when they're down just to cover your living expenses. It’s a simple but effective way to avoid locking in losses and gives your portfolio the breathing room it needs to recover—a critical part of preserving your capital for the long haul. We go into much more detail on this in our guide to retirement withdrawal strategies.

This tactic is especially useful for managing sequence of returns risk, which is the danger that a bear market early in retirement can do permanent damage to your portfolio's staying power.

Understanding the Earnings Test and IRMAA

If you plan to keep working past age 62, your claiming decision bumps up against two important rules: the Social Security earnings test and the Income-Related Monthly Adjustment Amount (IRMAA) for Medicare.

- The Social Security Earnings Test: If you claim benefits before your Full Retirement Age (FRA) and still have earned income over a certain limit, your benefits get temporarily reduced. For 2024, that limit is $22,320. For every $2 you earn above that threshold, your benefit is cut by $1. The good news is this test vanishes completely once you reach your FRA.

- Medicare IRMAA Surcharges: Your income, which includes your now-taxable Social Security, can also trigger higher premiums for Medicare Part B and Part D. These surcharges, known as IRMAA, are based on your income from two years prior. Claiming Social Security can easily push you over the income thresholds, leading to surprisingly higher healthcare costs in retirement.

At the end of the day, your claiming strategy is a powerful lever. Pulling it at the right time can lower your lifetime tax bill, shield your investment portfolio, and help keep your healthcare costs from spiraling. The key is to stop seeing it as a standalone choice and start treating it as the linchpin of your total wealth picture.

Moving Beyond Breakeven with Longevity Planning

Most people start their Social Security analysis with a simple breakeven chart. It’s a common first step, but it often stops short of telling the whole story. These charts simply show you the single age where delaying your benefits "pays off," a calculation that falls flat when planning for the complex realities of retirement, especially for those with significant assets.

To get a complete picture, we need to shift our thinking beyond a single crossover point and fully embrace longevity planning.

This isn’t about trying to guess the exact year you’ll pass away. Instead, it's about making a strategic decision based on probabilities—your health, your family history, your lifestyle, and what you truly want out of retirement. The question evolves from "When do I break even?" to "Which strategy best funds the life I want to live, given a realistic range of outcomes?"

From Crossover Age to Lifestyle Funding

A breakeven chart is a simple plot of cumulative benefits over time. It’s a handy visual, but it makes a critical error: it treats a dollar you receive at age 65 the same as a dollar you receive at age 85. Anyone planning an active, vibrant retirement knows that's not how life actually works. The real-world value of that money—what it can do for you—changes dramatically as you age.

This is where we talk about the "go-go," "slow-go," and "no-go" years of retirement. Your 'go-go' years, usually your 60s and early 70s, are when you have the health and energy for big trips, new hobbies, and adventure. Delaying Social Security might maximize your check later, but it could mean you miss the window to fund those experiences.

Instead of focusing only on maximizing lifetime dollars, consider how you want to fund your health span—the years you are healthy enough to truly enjoy your wealth. This reframes the claiming decision around optimizing your quality of life, not just your balance sheet.

Cumulative Benefit Comparison: Early vs. Delayed Claiming

To see how this plays out financially, let's look at the numbers. The table below compares the total benefits received by someone who claims at the earliest possible age (62) versus someone who delays until the maximum age (70). Notice how the early claimer builds a significant lead, but the delayed claimer's higher monthly benefit eventually catches up and surpasses the early total.

Note: Assumes a Primary Insurance Amount (PIA) of $2,500 at a Full Retirement Age of 67. Claiming at 62 results in a $1,750 monthly benefit; delaying to 70 results in a $3,360 monthly benefit. Figures are illustrative and do not include cost-of-living adjustments.

The "breakeven" point here happens around age 82. But as the following examples show, that single number is only one piece of a much larger, and more personal, puzzle.

Case Study: The Active Retiree

Let's consider Mark and Lisa, both 62. They're in good health and have a clear vision for their first decade of retirement: traveling the world while they're still active and able. Their financial plan shows they can retire comfortably, but funding their ambitious travel goals would mean drawing down their investment portfolio at a faster rate than they'd prefer, especially if the market takes a dive.

The Dilemma: Delaying Social Security to age 70 would give them larger checks later, but it would put a lot of pressure on their portfolio during their prime 'go-go' years.

The Strategy: They decide to claim their benefits right away at 62. This gives them an immediate and reliable stream of cash flow. It allows them to fund their travels without having to aggressively sell off investments, significantly reducing their exposure to sequence of returns risk. You can see just how much this risk can impact a portfolio in our guide on sequence of returns risk in retirement planning.

The Outcome: For Mark and Lisa, accepting a smaller future benefit is a smart trade-off. They get the certainty and liquidity they need to live out their dreams now.

Case Study: The Longevity Planner

Now, let's look at a different situation. Sarah is a 64-year-old business owner who comes from a family where living well into your 90s is the norm. She's in excellent health and enjoys her work, planning to continue part-time for several more years.

The Dilemma: Sarah doesn't need Social Security income to fund her current lifestyle. Her main goal is to lock in the highest possible financial security for her later years and maximize what she can leave behind.

The Strategy: Sarah makes the call to delay her benefits all the way to age 70. This simple decision boosts her eventual monthly check by 24% over what she'd get at her full retirement age, giving her a larger, inflation-adjusted income that acts as powerful longevity insurance.

The Outcome: By waiting, Sarah maximizes her guaranteed income for life, creating a powerful defense against the risk of outliving her other assets. This move perfectly aligns with her risk tolerance and long-term goals.

As these two stories show, the "best" Social Security strategy isn't found on a simple chart. It’s deeply personal and depends entirely on how you weigh the desire for immediate lifestyle funding against the need for long-term financial security.

Building Your Personal Decision Framework

After digging into the mechanics of Social Security, spousal benefits, and tax implications, we’ve arrived at the most critical piece of the puzzle: you. Generic online calculators can spit out a number, but they can't account for your life, your family, or your vision for retirement. The best Social Security claiming strategies are deeply personal.

Think of what follows as a pre-flight checklist before you make one of the most significant financial decisions of your retirement. The goal isn’t to pinpoint a single “correct” answer right now. Instead, it’s to illuminate the best path for your unique circumstances and prepare you for a productive conversation with your financial advisor.

Key Questions to Guide Your Social Security Decision

Let's start by working through the big questions. Your answers will begin to paint a clear picture of which strategy makes the most sense for your financial and personal goals.

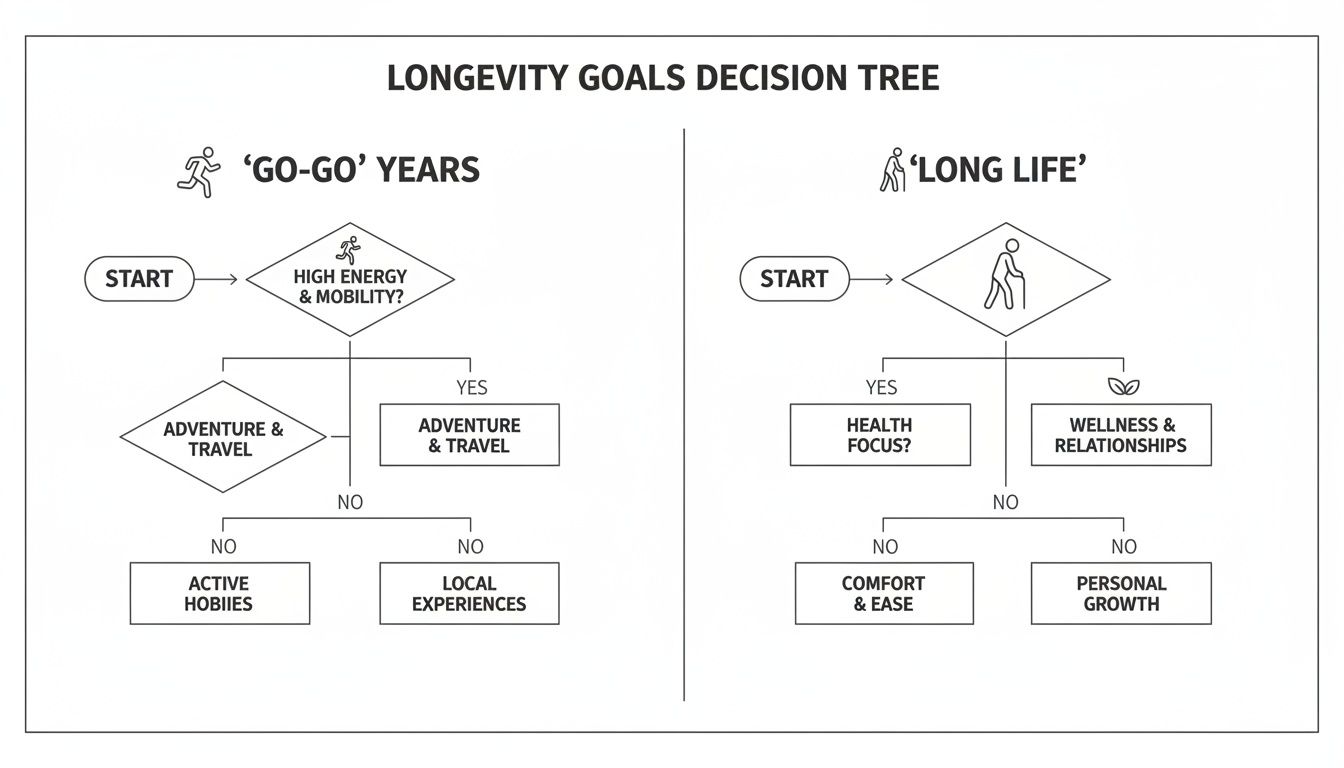

- Health and Longevity: What’s your family health history look like? Do you have good reason to believe you’ll live well into your 80s or 90s? If so, maximizing your monthly benefit by delaying acts like powerful longevity insurance. Or, is your priority to have more cash on hand to fund your active "go-go" years?

- Income Needs and Cash Flow: Do you plan to keep working? Do you need Social Security to fill an income gap and retire early, or do you have enough from your portfolio and other sources to live on comfortably without it for a few years?

- Spousal and Survivor Needs: If you're married, what's the income gap between you and your spouse? For many couples, especially those with a significant earnings difference, using the higher earner's record to maximize the survivor benefit is one of the most powerful legacy planning tools available.

- Tax Planning Opportunities: Are you heading into a few lower-income years before you plan to claim? Delaying Social Security can open up a valuable window for strategic Roth conversions at a lower tax rate, a move that could save you a fortune in future taxes.

- Portfolio and Risk Management: How would claiming early affect your investment portfolio? For many retirees, a guaranteed income stream from Social Security reduces the pressure to sell assets during a market downturn—a vital tool for managing sequence of returns risk.

This decision tree helps visualize the trade-off between fueling your active 'go-go' years and planning for a long, financially secure life.

As the chart shows, your personal goals are the primary driver. They determine whether it makes more sense to claim sooner for immediate liquidity or to delay for a much larger, inflation-protected benefit down the road.

From Answers to Action Plan

With your answers in hand, a strategy is likely starting to take shape. You can see how the different pieces—your health, your spouse, your portfolio, your tax plan—all fit together. The final step is to translate these ideas into a concrete plan.

Your Social Security claiming strategy isn't just a financial decision; it’s a life decision. It needs to support the retirement you've actually envisioned, whether that means traveling the world in your 60s or having maximum financial security in your 90s.

Ultimately, getting this right requires a personalized approach. By systematically thinking through your health, finances, and family situation, you give yourself the power to make a confident, informed choice—one that will serve you and your loved ones for decades.

Common Questions & Last-Minute Considerations

Even with a solid plan, a few specific questions always seem to pop up as you get closer to claiming. Let's walk through some of the most common ones we hear from clients.

Can I Change My Mind After I Claim?

What if you start taking benefits and then realize you made a mistake? The Social Security Administration (SSA) gives you a couple of ways to handle "claimer's remorse," but your options are limited.

You have a one-time-only window to completely withdraw your application. This must be done within 12 months of when you first started getting paid. If you go this route, you must repay every dollar you and any family members received based on your application. It essentially resets the clock, letting you file again later for a higher monthly check.

The other option is suspension. If you started your benefits at or after your Full Retirement Age (FRA), you can tell the SSA to pause your payments anytime up until you turn 70. While your benefits are suspended, you'll earn delayed retirement credits at a rate of 8% per year. Your payments will restart automatically at age 70 if you haven't already turned them back on yourself.

What Are the Rules for a Divorced Spouse?

If you were married for at least 10 years and are currently single, you might be eligible to claim a benefit based on your ex-spouse's work history. This can be a huge help if your own benefit is significantly lower.

The basic requirements are:

- You must be at least 62.

- Your ex-spouse needs to be eligible for their own retirement or disability benefits.

- The spousal benefit you'd receive has to be more than you'd get from your own work record.

One of the most important things to know is that your decision to claim is completely independent. It has absolutely no impact on your ex-spouse's benefit amount or what their current spouse can receive.

When Does a Lawyer Need to Get Involved?

For most people, filing for standard retirement benefits is a straightforward process you can handle on your own. But that's not always the case.

The situation changes dramatically if you're applying for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI). The disability application process is notoriously complex, and initial denials are unfortunately quite common.

For complex situations or denials, you might ask, "Do I Need A Social Security Disability Lawyer?" to help boost your SSDI/SSI odds. Legal experts can help gather medical evidence and navigate the appeals process, which can be critical for a successful claim.

At Commons Capital, we specialize in integrating complex decisions like these into a cohesive wealth plan. If you're ready to create a personalized strategy that aligns with your long-term goals, we invite you to connect with us. Learn more about how we help our clients at https://www.commonsllc.com.