When someone names you the executor of their will, they are placing an enormous amount of trust in your hands. It is a profound gesture, but it also comes with significant legal weight. Fulfilling the executor of a will responsibilities means you are legally in charge of wrapping up their entire life — securing assets, paying off debts, and ensuring the remaining inheritance gets to the correct people.

It’s a role that demands a sharp eye for administrative, financial, and legal details, often while navigating personal grief.

Understanding the Executor Role Beyond the Title

Think of an executor as the project manager for a person's final affairs. It's far more than an honorary title; your job is to see the entire process through with integrity and diligence, from start to finish. This can be a challenging responsibility, especially when you're also grieving.

Many new executors are caught off guard by the scope of the duties involved. Research shows a significant number of people are unaware of their legal and financial obligations. For example, 44% of people don't know an executor must secure the deceased's property, and 47% are unaware they are responsible for calculating and paying taxes. These knowledge gaps can lead to serious complications.

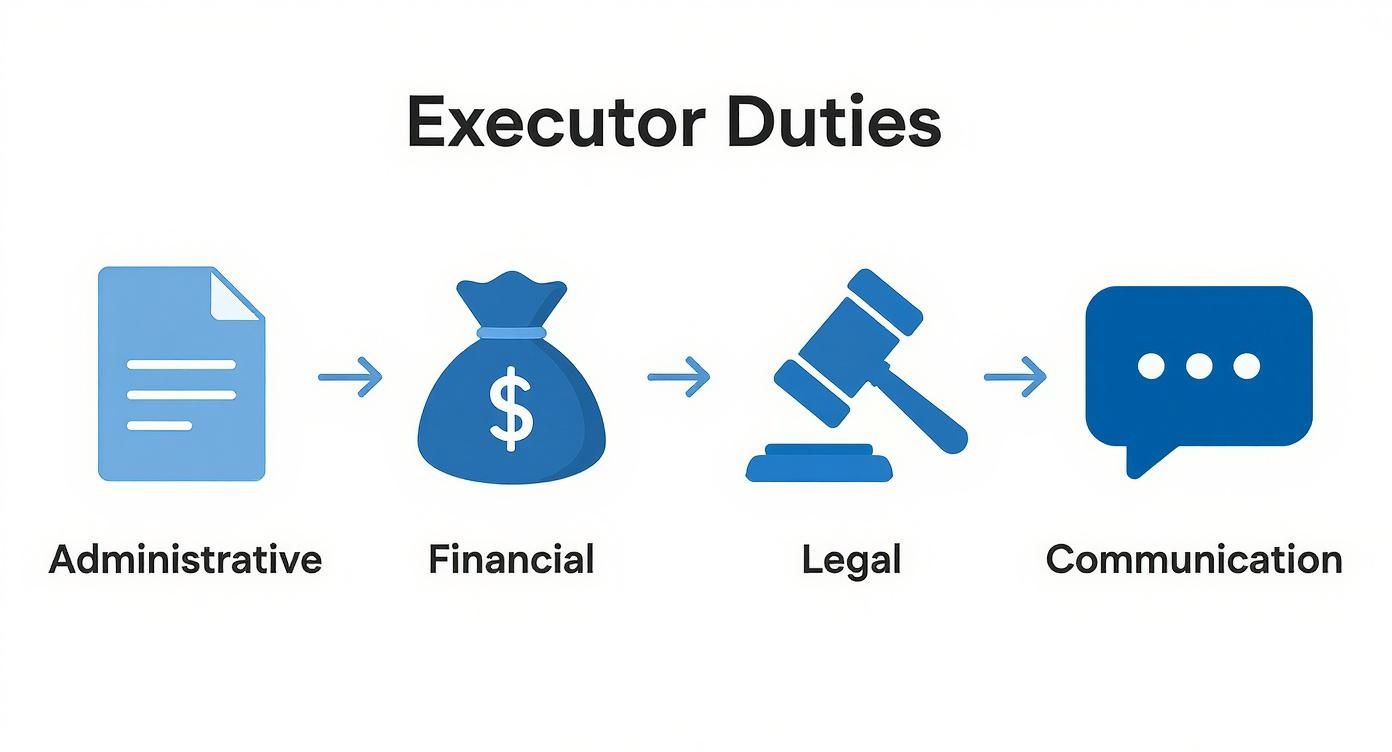

The Four Pillars of Executor Duties

To manage the role effectively, it helps to break down the responsibilities into four core areas. This framework can make the journey ahead feel much more manageable.

- Administrative Duties: This involves all the foundational paperwork. You will need to locate the original will, obtain multiple copies of the death certificate, and begin notifying various entities, from government agencies to banks.

- Financial Management: This is where much of the detailed work lies. Your job is to find, secure, and create a detailed inventory of every asset — bank accounts, investments, real estate, and personal belongings. You will also need to open a dedicated estate bank account to keep all funds separate and transparent.

- Legal Obligations: As an executor, you have a fiduciary duty, which legally requires you to act in the absolute best interests of the estate and its beneficiaries. This often means initiating the probate process with the court, which validates the will and officially grants you the authority to act. A solid understanding of the legal landscape, such as local Ontario wills and estate law, is crucial.

- Communication: Keeping the beneficiaries informed is non-negotiable. You must be proactive in sharing updates on progress, timelines, and any challenges that arise. Transparent communication is the best way to prevent misunderstandings and family disputes.

It's also important to understand how your duties might change based on the estate planning documents. Knowing the difference between a living trust vs. a will provides critical context, as the administration process can differ significantly.

To give you a clearer picture, here’s a quick summary of what the job entails.

Executor Responsibilities at a Glance

These categories provide a roadmap for navigating your responsibilities, ensuring no critical step is overlooked.

Your Step-by-Step Estate Administration Roadmap

Taking on the executor role can feel like being handed a map to a labyrinth. It’s a lot to process. This guide is your chronological walkthrough, breaking down the entire journey of administering an estate into a clear, phase-by-phase plan. We'll turn that intimidating list of executor of a will responsibilities into a series of manageable steps.

Phase 1: Initial Actions After a Death

The first few days and weeks are absolutely critical. What you do now sets the tone for the entire process. Your immediate job is to find the essential documents and make sure the deceased's assets are safe.

First, locate the original, signed will. This document is the foundation of everything you will do, as it outlines the deceased's final wishes. Once you have it, you’ll also need to obtain several official copies of the death certificate. You will need them for nearly every administrative task, from closing bank accounts to dealing with government agencies.

Next, you must secure all physical and digital property quickly. This means changing the locks on the house, gathering valuable items like jewelry or art for safekeeping, and taking possession of any vehicles. Part of this initial sweep involves managing all the physical items left behind; using an ultimate estate cleanout checklist can be a lifesaver to ensure nothing is missed.

Phase 2: Initiating the Legal Process

With the initial groundwork laid, your focus now shifts to the legal side of things. This phase is all about getting the court’s official stamp of approval, giving you the authority to act for the estate.

This is where you’ll dive into the probate process. As executor, you must file a petition for probate with the court. This is a formal request for the court to validate the will and officially appoint you. It’s the key that unlocks your ability to legally manage assets, pay off debts, and handle taxes.

Keep in mind that while probate is common, not all assets have to go through it. Figuring out which ones can bypass the court can save a ton of time and hassle. If you want to get a better handle on this, check out our guide on how to avoid probate court for certain types of assets.

This chart breaks down the core duties of an executor into four main buckets: administrative, financial, legal, and communication.

As you can see, being an executor is a multi-faceted job. You’re essentially a project manager, and success depends on juggling tasks across all these different areas.

Phase 3: Asset and Liability Management

Once the court gives you the green light with the grant of probate, the real detailed work begins: marshalling the estate's finances. This is one of the most time-consuming parts of the job.

You need to create a thorough and meticulous inventory of everything the deceased owned. It’s more than just the obvious things like a house or a bank account. You need to track down:

- Financial Accounts: Checking, savings, investment portfolios, and retirement accounts.

- Real Estate: The primary residence, any vacation homes, or investment properties.

- Personal Property: Cars, collectibles, art, furniture, and anything else of value.

- Digital Assets: Online accounts, cryptocurrency, or digital intellectual property.

At the same time, you have to hunt down all outstanding debts and liabilities. This means sifting through mail and financial statements to find any loans, credit card balances, mortgages, or other financial obligations.

To maintain financial clarity and fulfill your fiduciary duty, it is absolutely critical to open a separate bank account just for the estate. All estate income goes in, and all debts and expenses are paid out from this single account. This creates a clean, transparent record that’s easy to audit.

Phase 4: Finalizing the Estate

Once you have a complete picture of the assets and liabilities, you're in the home stretch. This final phase is all about settling the estate’s financial affairs before you can distribute what’s left to the heirs.

Your responsibility is to pay all legitimate debts, final expenses, and taxes. This includes everything from credit card bills and final medical expenses to funeral costs and filing the deceased's final income tax return. You have to make sure every creditor is paid before a single beneficiary gets their inheritance.

Only after every last debt and tax bill is settled can you move on to the final — and most rewarding — step: distributing the remaining assets. You must follow the will to the letter, giving each beneficiary exactly what they were left. It's a smart move to have beneficiaries sign a release form acknowledging they've received their inheritance. This gives you a final layer of legal protection and officially wraps up your primary duties, bringing the estate administration process to a close.

Navigating Complex Financial and Legal Duties

Once you've handled the first wave of administrative tasks, your focus has to shift to the more complex financial and legal side of the equation. This is where the core executor of a will responsibilities really come into play, demanding a sharp eye for detail and a steady hand. Managing the estate’s money isn't just about balancing a checkbook; it’s about protecting its value and acting with complete integrity.

Your first major task is to determine the value of all estate assets. While a savings account is straightforward, unique assets require professional valuation. A family business, a collection of fine art, or a vintage car all need professional appraisers to determine their fair market value. Getting these valuations right is absolutely critical for tax filings and ensuring each beneficiary receives their fair share.

From day one, impeccable accounting is your best friend and your strongest legal shield. You need to track every single dollar that comes into or goes out of the estate. That means keeping meticulous records of all income, expenses, and transactions through that dedicated estate bank account you set up. This financial ledger is the ultimate proof of your careful management.

Demystifying Estate Taxes and Debts

Tackling taxes is often the most daunting part of the job. You’re responsible for filing the deceased’s final personal income tax return, which covers all income they earned up until their death. On top of that, if the estate itself earns any income while you're managing it — say, from investments or rent — you'll need to file an estate income tax return (in Canada, this is often a T3 Trust Return).

Executor's Fiduciary Duty: This is a crucial legal concept. It is your legal obligation to act only in the best interests of the estate and its beneficiaries. That means being prudent, totally transparent, and steering clear of any conflicts of interest. Failure to do so could result in personal liability for any losses.

Dealing with debts requires a formal, methodical process. You have to make a real effort to find and notify anyone the deceased might have owed money to. The standard way to do this is by publishing a notice in a local newspaper, which gives creditors a deadline to come forward with their claims.

Paying those claims follows a strict order. All legitimate debts, funeral bills, and administrative costs must be paid out of the estate’s funds before a single dollar goes to the beneficiaries. If you distribute assets too early and the estate can't cover its debts, you could be on the hook for the difference. It's always a good idea to look into strategies for how to minimize estate taxes to preserve as much of the estate’s value as possible for the heirs.

Handling Tricky Financial Scenarios

Of course, real-world estates are rarely so neat and tidy. You'll likely run into complicated situations that require sound judgment and, more often than not, some professional advice. These are the moments that truly test an executor's ability to make smart, defensible decisions.

Here are a few common challenges you might face:

- Volatile Investment Portfolios: If the estate holds a lot of stocks or other investments, you have to manage them wisely. In a shaky market, you’ll have to decide whether to sell assets to stop the bleeding or hold on and hope for a rebound, all while balancing the estate's cash needs and the beneficiaries' interests.

- Insolvent Estates: Sometimes, an estate’s debts are greater than its assets. When this happens, you have to follow a strict legal pecking order for paying creditors. This is a high-stakes scenario where getting legal advice isn't just a good idea — it's essential to protect yourself from personal liability.

- Business Operations: If the estate includes an active business, you might have to step in and oversee its operations for a while. This could mean everything from making payroll to managing inventory, just to keep things running until the business can be sold or passed on to an heir.

Each of these situations highlights just how heavy the financial and legal responsibilities can be. The key to getting through it successfully is to have a clear plan, keep flawless records, and know when to call in the experts.

Managing Timelines and Sidestepping Common Pitfalls

If there are two things every executor needs, it's patience and a sharp eye for detail. Settling an estate isn’t a weekend project; it’s a marathon that often takes one to two years to complete, sometimes even longer if the assets are complex or family disputes crop up.

That timeline often comes as a shock. The sheer volume of administrative work is significant and requires your steady attention for months on end. According to data from EstateExec.com, a leading tool for executors, the average executor puts in around 570 hours to close out an estate. Even though most estates fall under 800 hours of work, executors consistently rate the job as moderately difficult.

Knowing this upfront helps you set realistic expectations, both for yourself and for the beneficiaries. Trying to rush things is one of the worst mistakes you can make, as it almost always leads to costly errors and legal headaches down the line.

A Realistic Timeline for Estate Settlement

While no two estates are exactly alike, the process follows a fairly standard path. Having a rough roadmap can help you stay organized and keep everyone in the loop.

- First 1-3 Months: This is all about gathering intel and securing the estate. Your job is to find the will, order copies of the death certificate, notify banks and other institutions, and start building a comprehensive list of assets.

- Months 3-9: Now the real administrative work begins. You’ll be applying to the court to open probate, sending formal notices to creditors, hiring appraisers for assets like real estate or art, and filing the deceased’s final tax returns.

- Months 9-18+: Once you get the green light from the court (the grant of probate) and the tax authorities, you can start clearing the estate's debts. This means paying off every legitimate creditor claim, along with all the administrative bills you've accumulated.

- Final Stage: With all obligations handled, you'll draw up a final accounting for the beneficiaries to review. Once they approve it, you can finally distribute the remaining assets as directed by the will.

The Most Common Executor Pitfalls to Avoid

Successfully navigating this role means knowing where the landmines are buried. A few common missteps can easily derail the entire process, sparking conflict and even putting you on the hook for financial losses.

As an executor, you have a fiduciary duty — a legal obligation to act with the highest degree of good faith and loyalty. Even simple, preventable mistakes can be viewed as a breach of that duty, creating major legal and financial risks for you personally.

One of the most classic blunders is sloppy record-keeping. You have to document every single dollar that comes in and goes out, every decision you make, and every conversation you have. Without a clean paper trail, you’re left exposed to challenges from beneficiaries or tough questions from the court.

Poor communication is another frequent mistake. Keeping beneficiaries in the dark is a recipe for suspicion and resentment. Sending regular, clear updates — even if it's just to say there's no news — can head off most disputes before they even start.

Finally, the most dangerous pitfall of all is paying out inheritances too soon. You absolutely must pay all the estate's debts, taxes, and administrative expenses before a single beneficiary gets a dime. If you distribute the assets and a surprise tax bill or creditor claim pops up, you could be held personally responsible for paying it out of your own pocket.

Common Executor Mistakes and How to Prevent Them

Thinking ahead can help you steer clear of the most frequent traps executors fall into. Here’s a quick guide to the biggest mistakes and, more importantly, how to avoid them.

By keeping these points in mind, you can navigate your duties with confidence and bring the estate to a successful and drama-free conclusion.

Handling High-Value and Complex Estate Assets

When an estate involves more than just a house and a checking account, the executor's job gets exponentially more complicated. High-net-worth estates are often a tangled web of sophisticated assets, and managing them demands specialized knowledge and a serious level of diligence. For an executor in this position, the role shifts from simple administrator to financial strategist.

Your legal duty to act in the estate’s best interest — your fiduciary duty — is under a microscope when dealing with active businesses, large investment portfolios, or properties in multiple states or countries. A simple oversight can trigger major financial losses, so it's critical to have a clear game plan for each type of asset. The mission is to protect and grow the estate's value while navigating a much tougher legal and financial maze.

Overseeing Business Interests and Investments

If the deceased owned a business, you have a new set of responsibilities. You are now responsible for ensuring the business maintains its value until it can be sold or passed on to the heirs. This doesn’t mean you have to start running the company day-to-day, but you do have to oversee its management.

This might involve:

- Ensuring Operational Continuity: You need to make sure the business continues to operate. This means ensuring payroll is met, vendors are paid, and daily operations continue smoothly.

- Valuing the Business: You will need to hire a professional business appraiser to get a firm valuation of the company. This is a non-negotiable step for both tax filings and ensuring fair distribution to heirs.

- Executing a Succession Plan: If the owner had a succession plan, your job is to help implement it. If not, you may need to prepare the business for sale, as directed by the will.

The same applies to a substantial investment portfolio. You cannot simply let it sit, especially in a volatile market. You have a duty to manage those investments prudently. More often than not, this means bringing in a financial advisor to help rebalance the portfolio or strategically sell assets to cover estate taxes and other expenses.

Managing Cross-Jurisdictional and Unique Assets

Wealthy individuals often own assets scattered across various locations. Real estate in different provinces, or even different countries, adds a thick layer of complexity. Every jurisdiction has its own probate laws, tax rules, and legal procedures.

An executor must navigate the legal requirements in every jurisdiction where property is located. This almost always means hiring local lawyers to handle what's called "ancillary probate" — a separate probate process required to transfer out-of-province or out-of-country assets.

And it’s not just real estate. You could be dealing with fine art collections, intellectual property rights, or even valuable digital assets. Each requires a specialized approach to valuation and management.

Coordinating with Trusts and Tax Planning

It is very common for high-net-worth individuals to use trusts to manage their wealth. If the deceased had a trust, your job as executor is to work closely with the trustee. The trustee manages everything inside the trust, while you handle everything outside of it. Clear communication and coordination between you and the trustee are vital to settling the entire estate smoothly.

Finally, strategic tax planning becomes a major part of the job. With larger estates, the tax bill can be staggering. Your duty is to legally minimize what the estate owes to preserve as much wealth as possible for the beneficiaries. This usually means working closely with a tax lawyer or accountant to identify all available tax-saving strategies, ensuring the deceased's financial legacy is passed on efficiently.

When and How to Assemble Your Team of Experts

Stepping into the role of executor isn't a solo mission. In fact, one of the smartest things you can do is recognize when you need to call in the professionals. Trying to navigate complex legal, financial, and tax issues on your own is a huge risk — not just for the estate, but for you personally. Bringing in a team of experts isn't an admission of weakness; it’s the hallmark of a diligent and responsible executor.

Your first, and arguably most important, call should be to an estate lawyer. Think of them as your guide through the legal labyrinth of probate. They’ll make sure all court filings are handled correctly and, crucially, protect you from liability. A seasoned lawyer can decipher complicated language in the will, manage claims from creditors, and offer invaluable advice if any disputes pop up between beneficiaries.

Identifying Your Core Professional Team

Beyond the legal side, your team will likely need some financial firepower to address the specific needs of the estate. These experts bring the clarity and precision you need to make sound financial decisions.

Your core team will typically include:

- An Accountant: This person is absolutely essential for navigating the world of taxes. They’ll handle the deceased's final personal tax return and prepare any necessary estate income tax returns, ensuring you’re fully compliant while minimizing the tax bite.

- A Financial Advisor: If the estate has a sizable investment portfolio, a financial advisor can help you manage these assets prudently. Their guidance is key when deciding whether to hold or sell securities based on market conditions and the estate's need for cash.

- Appraisers and Specialists: For unique or high-value assets — think real estate, fine art, collectibles, or a family business — you'll need certified appraisers. Their valuations are critical for filing accurate tax returns and ensuring every beneficiary gets their fair share.

Here's a crucial point to remember: these professionals get paid from the estate itself. Their fees are considered administrative expenses and come directly out of the estate’s funds — not from your own pocket.

So, where do you find these people? Referrals from your estate lawyer are often the best place to start. You can also look for individuals with specific designations, like a Chartered Professional Accountant (CPA) for tax matters.

When you're vetting potential team members, ask about their direct experience with estate administration. You'll also want to get their fee structure upfront to ensure total transparency and avoid any surprises down the road. By building this skilled team, you're making sure every aspect of your duty is handled with the highest level of expertise.

A Few Common Questions About Being an Executor

Stepping into the executor role naturally comes with a lot of questions. Let's tackle some of the most common ones that come up as people navigate their executor of a will responsibilities.

Am I Personally on the Hook for the Estate's Debts?

In most cases, no. An estate's debts get paid from the estate's assets. However, you can expose yourself to personal liability if you're not careful. This can happen if you mismanage the funds, start paying heirs before all the creditors and taxes have been settled, or simply fail to pay taxes due. The best way to protect yourself is to act prudently and get professional advice when you need it.

How Do Executors Actually Get Paid for This Work?

Executor compensation, often called an executor fee, is usually dictated by the will itself or by state law. If the will doesn't name a specific amount, the court will typically approve a "reasonable" fee, which is often a percentage of the estate's total value. It's absolutely critical to keep detailed records of your time and every task you complete to justify whatever compensation you take.

Don't forget: executor compensation is considered taxable income. You'll need to report these earnings on your personal income tax return in the year you receive the payment.

What if a Beneficiary Challenges My Decisions?

Beneficiaries have a right to ask questions and see a formal accounting of everything you've done with the estate's assets. If they suspect you're acting improperly, they can take it to court and ask a judge to step in or even have you removed. Your best defense is always clear, consistent communication and keeping meticulous records of every single decision and transaction.

Can I Just Say No to Being an Executor?

Yes, you can absolutely decline the role. It's a process called "renunciation," and you have to do it formally, in writing, before you take any action to manage the estate. The minute you start performing executor duties, you've legally accepted the job. If you do renounce, the alternate executor named in the will is next in line to step up.

Managing an estate is a major undertaking, and it demands serious financial oversight. For high-net-worth estates with complex assets, getting professional guidance isn’t just a good idea — it's essential. Commons Capital specializes in private wealth management, providing the expert financial advisory needed to navigate these responsibilities with confidence. To see how we can help preserve and manage estate assets, visit us at https://www.commonsllc.com.