Learning how to avoid probate court is a crucial step for protecting your legacy. The simplest answer is through smart, strategic estate planning using powerful tools like living trusts and beneficiary designations. This guide provides a clear roadmap, walking you through exactly how these strategies work and how to implement them effectively.

First, let's explore why avoiding probate is such a critical goal for anyone with significant assets to protect.

Understanding The High Cost Of Probate Court

Probate is the formal legal process that validates a will and supervises the distribution of assets after someone passes away. While it serves a purpose, for high-net-worth families, it often becomes a major headache—one that's expensive, painfully slow, and surprisingly public.

Understanding these drawbacks is the first step toward building a plan to sidestep the entire ordeal. The primary motivation for most people to learn how to avoid probate court is the sheer expense involved. These costs, paid directly from the estate before your heirs get anything, can seriously diminish the legacy you intend to leave.

The Financial Drain of Probate

Make no mistake, probate isn't just a legal formality; it's a financial event. The costs can be staggering, often calculated as a percentage of your estate's total value. This includes court filing fees, executor compensation, attorney fees, and appraisal costs. For larger, more complex estates, these expenses can easily run into the tens of thousands of dollars.

Beyond the direct costs, the process itself is notorious for delays. In the United States, around 2.6 million probate cases are filed every year, and these proceedings are frequently bogged down. The problem became especially severe after the COVID-19 pandemic, which created a massive backlog that courts are still struggling to clear. You can get a better sense of the scale from recent probate statistics in the United States.

Probate reframes your private family matters into a public record. Every asset, debt, and beneficiary named in your will becomes accessible to anyone who requests the court file, creating a significant loss of privacy for your loved ones.

The Public Nature of Court Proceedings

Another critical factor is the complete lack of privacy. When an estate goes through probate, the will and all related documents—including a detailed inventory of your assets—become public records. This means anyone can walk into the courthouse and see sensitive financial details, such as:

- The total value of your estate.

- A list of specific assets, from real estate to investment accounts.

- The names and addresses of your beneficiaries.

- Any debts or claims made against the estate.

This public exposure can make your heirs targets for financial predators or simply create unwanted attention during an already difficult time.

This toxic combination of high costs, long delays, and public scrutiny is precisely why avoiding probate is a central goal of effective estate planning. Fortunately, with the right strategies, you can ensure your assets are transferred efficiently, privately, and exactly as you wish—bypassing the courtroom altogether.

The table below offers a quick comparison of how assets are handled inside and outside the probate system.

Probate vs. Non-Probate Asset Transfer at a Glance

As you can see, the advantages of keeping your assets out of probate are clear and substantial. The following sections will detail the specific tools and techniques to help you achieve this.

Using a Living Trust to Bypass Probate

When you start digging into how to avoid probate court, one strategy consistently rises to the top as the most powerful and flexible tool in the playbook: the revocable living trust. It’s best to think of it not as some intimidating legal document, but as a private container you create to hold and protect your most valuable assets.

A will is essentially a set of instructions for the probate court to follow. A living trust, on the other hand, operates completely outside the court's reach. By setting one up, you transfer ownership of your assets into the trust while you’re alive, but you keep total control as the trustee.

When you pass away, the assets inside the trust are passed directly to the people you’ve chosen, precisely according to the rules you laid out. The entire process happens privately and efficiently, steering clear of the delays, costs, and public record that come with probate.

How a Living Trust Works in Practice

Creating a living trust is like writing a private rulebook for your estate. You, as the grantor (the creator), establish the trust. Then comes the critical part: you retitle your assets—like your home, brokerage accounts, or business interests—into the name of the trust.

While you're alive and well, you typically act as the trustee, managing everything just as you always have. You can buy, sell, or refinance assets held in the trust without any extra hassle. And because it's "revocable," you have the freedom to change the terms or even dissolve the entire trust whenever you want.

The real magic happens when you can no longer manage your affairs or after you pass away. At that moment, your designated successor trustee seamlessly steps in. Their job is to manage or distribute the trust's assets exactly as you instructed, bypassing the entire probate process.

The Critical Role of a Successor Trustee

Choosing your successor trustee is one of the most important decisions you'll make. This person or institution is responsible for carrying out your wishes, which can involve managing complex assets and navigating family dynamics.

Here are the key qualities I tell my clients to look for:

- Trustworthiness and Integrity: This is non-negotiable. You must have complete faith that they will act in the best interests of your beneficiaries.

- Financial Acumen: They should be capable of handling the specific assets in your trust, whether that's investments, real estate, or a family business.

- Impartiality: The ability to be objective is crucial, especially when you have multiple beneficiaries with different needs or personalities.

- Longevity and Availability: Think about the age and health of an individual. For trusts designed to last a long time, a corporate trustee (like a bank’s trust department) is often a more reliable choice.

For example, appointing your most financially savvy child might seem like the obvious move, but it can easily lead to family conflict. Sometimes, bringing in a neutral professional is the best way to ensure your plan is executed smoothly and without emotional friction.

A living trust is only as effective as the assets it contains. An "unfunded" or partially funded trust is one of the most common and costly mistakes in estate planning, often forcing valuable assets back into the probate system you intended to avoid.

Funding Your Trust: The Make-or-Break Step

The trust document itself is just paper. To turn it into a powerful probate-avoidance tool, you must actively transfer your assets into it. This step is called funding the trust, and it's where many people unfortunately drop the ball.

Funding means formally changing the title of your assets from your individual name to the name of the trust. For example, the deed to your home would be updated from "John and Jane Doe" to "John and Jane Doe, Trustees of the Doe Family Revocable Trust."

Here’s a quick look at what that process typically involves:

This requires meticulous attention to detail. Forgetting to fund a single major asset, like a vacation home or a significant brokerage account, means that specific asset will almost certainly have to go through probate—defeating the whole purpose of your careful planning.

While a living trust and a will are both critical parts of a solid estate plan, they play very different roles. We break down these differences in our detailed comparison of a living trust vs. a will. By properly creating and, most importantly, funding a revocable living trust, you create a seamless, private, and efficient pathway for your legacy.

The Power of Smart Asset Titling

While living trusts are a fantastic tool, sometimes the simplest ways to learn how to avoid probate court are built right into how you own your assets. Smart asset titling is one of the most direct techniques for ensuring certain properties transfer automatically to a co-owner or beneficiary when you pass away, completely sidestepping any need for court intervention.

One of the most common ways to do this is through Joint Tenancy with Rights of Survivorship (JTWROS). When you title an asset—whether it’s a house, a car, or a brokerage account—this way, you and the co-owner share equal ownership. When one owner dies, their share automatically and immediately passes to the surviving owner.

The transfer is instantaneous. All it usually takes is a death certificate and some straightforward paperwork. No probate, no delays.

Joint Ownership in Action

Let's look at a real-world scenario. A couple buys a vacation home together and titles the property as "Jane Smith and John Smith, as Joint Tenants with Rights of Survivorship." If Jane passes away, John instantly becomes the sole owner. He doesn't need a will or a court order to make it happen; the deed itself dictates the transfer of ownership.

The same principle works for financial accounts. If you have a joint brokerage account with your spouse under JTWROS, the surviving spouse gets full control of the assets without any interruption from the probate court. This seamless transition can be a financial lifeline, ensuring immediate access to funds during an incredibly difficult time.

Understanding the Risks and Drawbacks

As simple as it sounds, joint ownership isn't a silver bullet for everyone. It comes with some significant trade-offs that you absolutely have to consider. The moment you add someone as a joint owner to your asset, you are giving them immediate ownership rights.

This means you can no longer make decisions about that asset on your own. For instance, if you add your adult child to the deed of your home, you can’t sell or refinance the property without their explicit consent. You’ve effectively given away a portion of your control.

While JTWROS is an effective probate avoidance tool, it introduces immediate risks. The asset becomes vulnerable to the co-owner's creditors, lawsuits, and potential marital disputes, which could jeopardize your financial security.

Another huge risk is exposure to your co-owner’s financial troubles. If your joint owner gets sued, goes through a divorce, or files for bankruptcy, your shared asset could be targeted by their creditors to satisfy their debts. This could potentially force the sale of your home or the liquidation of an investment account, even if you had nothing to do with their financial problems.

When Smart Titling Makes Sense

So, when is JTWROS a good move? It's most commonly and effectively used between spouses, since their financial lives are typically already intertwined. For other relationships, it demands a massive degree of trust and a very clear understanding of the potential downsides.

- For Spouses: Titling a primary residence, bank accounts, and investment accounts as JTWROS is often a practical and efficient choice.

- For Unmarried Partners: This can work, but it requires a frank discussion about financial stability and potential liabilities.

- With Children: Adding a child as a joint owner is generally much riskier and should be approached with extreme caution due to the loss of control and creditor exposure.

Proper estate planning is crucial because probate expenses can eat up as much as 10% of an estate's value. And with roughly 60% of American adults still lacking a will as of 2025, many estates are left vulnerable to these high costs. Another powerful strategy involves strategically moving assets out of your name during your lifetime. Understanding the process of drafting gift deeds can help you effectively shrink your probate estate. Much like JTWROS, this approach can simplify the transfer of your legacy, but it has its own set of rules and potential tax implications that must be carefully weighed.

Maximizing Beneficiary Designations

Beyond the high-level architecture of trusts and property titles, one of the most direct and powerful tools for keeping your assets out of court is probably already in your financial toolkit. Many financial accounts let you name a beneficiary—a simple action that completely changes how that asset is handled when you pass away. It's one of the most effective, yet surprisingly overlooked, strategies for anyone figuring out how to avoid probate court.

These designations function as a legal shortcut. When you die, the asset transfers directly to the person you named, entirely bypassing your will and the probate process. It’s a private, fast, and cost-effective way to pass on wealth.

You'll find this feature on many accounts you likely already have:

- Retirement Accounts: This includes 401(k)s, 403(b)s, and Individual Retirement Accounts (IRAs).

- Life Insurance Policies: The death benefit is paid straight to your named beneficiary.

- Annuities: Similar to life insurance, the proceeds go directly to the designated person.

Using POD and TOD Designations

Even your everyday bank and brokerage accounts can be set up to avoid probate. These are usually called Payable-on-Death (POD) for bank accounts and Transfer-on-Death (TOD) for investment or brokerage accounts.

Getting them in place is often as simple as filling out a one-page form from your financial institution. You name your primary beneficiary and, in most cases, a contingent (or backup) beneficiary. While you’re alive, the beneficiary has zero access or control over the funds; the designation only kicks in after your death.

A Cautionary Tale: The Peril of Outdated Forms

The simplicity of beneficiary designations is also their greatest weakness. Because they are so easy to set and then forget, they often become dangerously out of date.

Consider this all-too-common scenario: A man names his wife as the beneficiary of his substantial 401(k). Years later, they go through a bitter divorce, and he remarries. He meticulously updates his will to leave everything to his new wife and children but completely forgets to change that old 401(k) beneficiary form.

When he passes away, the 401(k) provider is legally required to pay the entire account balance to the person named on the form—his ex-wife. The beneficiary designation legally trumps the instructions in his will. This single oversight can unintentionally disinherit his current family and send a major asset to the wrong person. It's an irreversible mistake.

A beneficiary designation is a powerful legal contract that supersedes a will. Failing to review and update these forms after major life events like marriage, divorce, or the birth of a child is one of the most devastatingly simple mistakes in estate planning.

The Annual Beneficiary Audit: A Critical Checklist

To prevent a disaster like that, you have to be proactive. I recommend conducting a "beneficiary audit" at least once a year, or immediately after any major life event. This review ensures every single asset is pointed in the right direction and aligns with your current wishes.

Here’s an actionable checklist to guide your audit:

- Inventory All Accounts: Make a complete list of every account with a beneficiary designation. This means retirement plans, life insurance policies, annuities, and any bank or brokerage accounts with POD/TOD forms.

- Verify Current Designations: Contact each financial institution or log into your online portal to confirm who is currently listed as the primary and contingent beneficiary for each account. Don't rely on memory.

- Align with Your Estate Plan: Does each designation match what you’ve laid out in your will or living trust? For example, if your trust is designed to manage assets for a minor child, you might name the trust itself as the beneficiary.

- Update as Needed: If you find any discrepancies, request the proper forms right away and submit the updates. Always follow up to confirm the institution has processed the changes correctly.

This proactive audit is a vital part of a smooth estate administration process. In fact, the global market for these services is booming, expected to be worth around $50 billion in 2025 and growing at 7% annually. This growth reflects a rising awareness of just how important precise estate planning is. To dig deeper into these trends, you can explore the full market research on estate administration services.

For retirement accounts, the tax implications for beneficiaries can get complicated. Understanding these rules is critical, which is why we've put together a guide on the tax implications of an inherited 401(k) that can help inform your decisions. A regular review of your designations is the best way to ensure your financial legacy is secure.

Building Your Comprehensive Estate Plan

The real secret to figuring out how to avoid probate court isn't about finding one magic tool. It's about making all the different strategies—living trusts, joint ownership, beneficiary forms—work together as a single, coordinated plan. A living trust is powerful, but only if you actually fund it. Beneficiary designations are simple, but only if they're kept up to date.

The goal here is to move from theory to action. It’s about building a cohesive system where every single asset has a clear, non-probate path to the right person, at the right time. When all these pieces are aligned, they form a protective barrier around your legacy, making sure it’s handled exactly as you intended, without the courts getting involved.

From Individual Tools to a Cohesive Strategy

Think of your estate plan as a finely tuned machine. The living trust is the engine, but the beneficiary designations on your retirement accounts and the joint title on your home are the essential gears. If one part is misaligned, the whole machine can grind to a halt.

For example, your living trust might be perfectly drafted to manage your children's inheritance in a protected, structured way. But if your largest brokerage account still lists your kids directly as "Transfer on Death" (TOD) beneficiaries, that money bypasses the trust entirely. This could dump a huge windfall on a young adult you never intended to manage that much money alone. A comprehensive plan ensures every piece works toward the same objective.

A successful estate plan is not a collection of separate documents; it is a single, integrated strategy. The true power lies in ensuring your trust, asset titles, and beneficiary forms all tell the same story and work together to bypass probate.

The key is a holistic review. You have to look at your entire financial picture and make sure the instructions on your deeds, account forms, and trust document are in perfect harmony. This simple step prevents conflicts and closes the gaps that could accidentally force an asset back into the probate system.

Your Action Plan: A Practical Checklist

Feeling empowered to protect your assets starts with a clear roadmap. This isn't complicated, but it does require attention to detail. This practical checklist gives you the actionable steps needed to build a robust plan that keeps your estate out of court.

- Inventory Every Asset: First things first, you need to know what you own. Create a detailed list of everything: real estate, bank accounts, investment portfolios, retirement plans, life insurance policies, business interests, and valuable personal property. You can't protect what you haven't accounted for.

- Review All Titles and Deeds: Next, examine how each asset is legally owned. Is your home titled as Joint Tenants with Rights of Survivorship? Are your brokerage accounts held individually or jointly? This step quickly reveals which assets will automatically bypass probate and which ones are currently vulnerable.

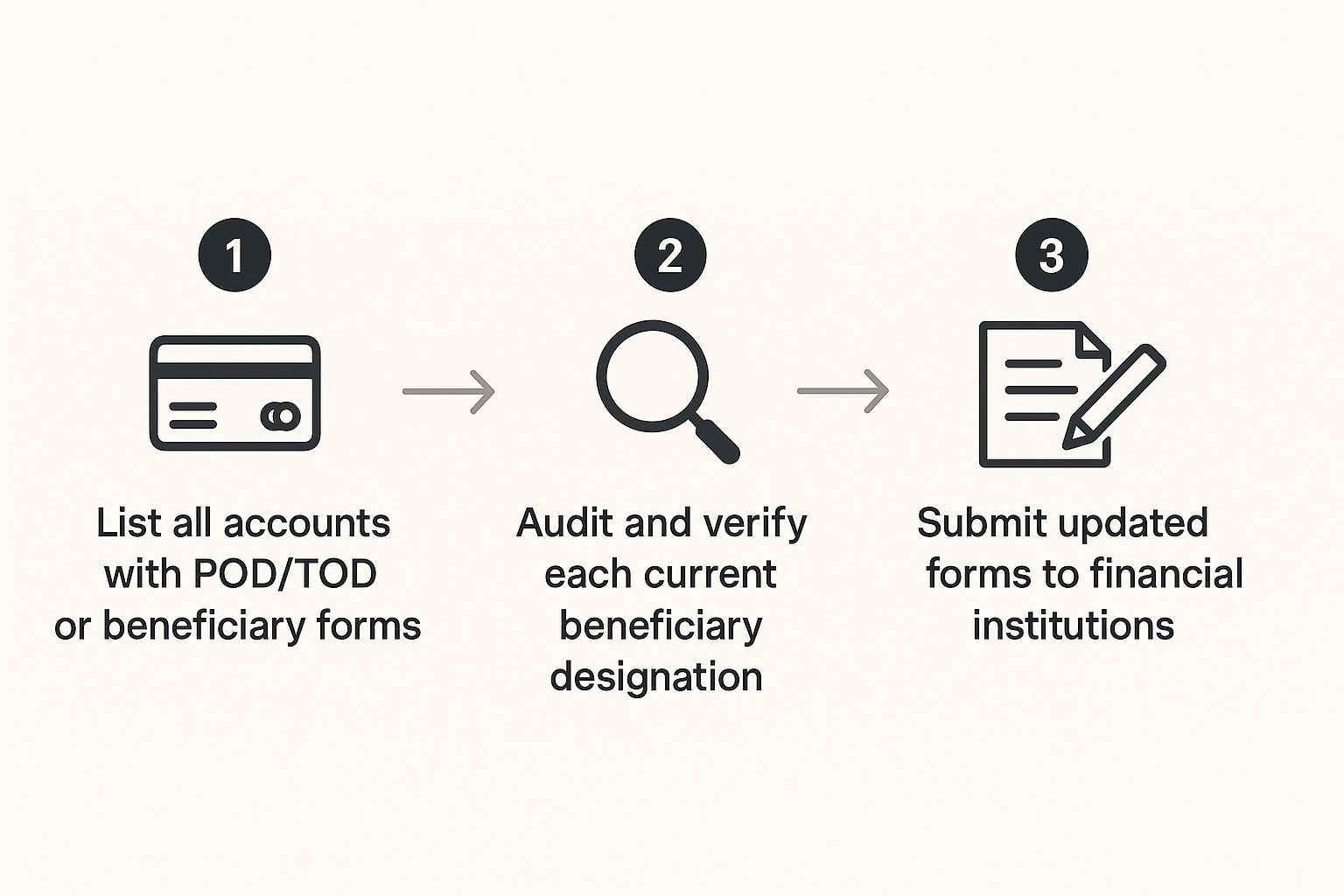

- Conduct a Full Beneficiary Audit: This is non-negotiable. Get on the phone or go online and request the current beneficiary designation forms for every single retirement account, life insurance policy, and annuity. Verify that the primary and contingent beneficiaries are correct and align with your overall estate goals.

This infographic breaks down the simple but critical process for auditing and updating your beneficiary forms.

This process really underscores how a simple administrative review is one of the most effective things you can do to keep major assets from getting tangled up in probate court.

Preparing to Work with a Professional

While you can do much of this prep work yourself, finalizing your plan requires professional guidance. An experienced estate planning attorney is essential for drafting the legal documents, like a living trust and a pour-over will, and making sure they comply with state law. For a deeper look at the broader legal landscape, you might find a comprehensive guide to Ontario wills and estate law helpful context.

To make your meeting with an advisor as productive as possible, bring your completed asset inventory and copies of deeds and beneficiary forms. This preparation allows them to focus on strategy rather than fact-finding, which saves you both time and money.

By taking these proactive steps, you can create a clear and effective plan. You can learn more about how we approach this by exploring our trust and estate planning services.

Common Questions About Avoiding Probate

Navigating the world of probate avoidance strategies always brings up a few key questions. Even with a solid plan, it's completely normal to have lingering concerns about the details. Let's walk through some of the most common ones we hear.

If I Have a Will, Do My Assets Still Go Through Probate?

Yes, almost always. This is one of the most persistent and costly misconceptions in estate planning.

Think of a will as your personal instruction manual for the probate court, not a hall pass to skip it entirely. The court’s first job is to legally validate your will to confirm it’s authentic. Only after that does it supervise your executor as they gather assets, pay off debts, and finally distribute what’s left according to your wishes.

To actually keep your assets out of the courtroom, you need to use tools specifically designed for that purpose—living trusts, joint ownership, and beneficiary designations are the big three.

Is Setting Up a Living Trust Too Expensive?

While a revocable living trust definitely has a higher upfront cost than a simple will, it is almost always far cheaper than the probate fees your estate could face down the line. For high-net-worth individuals, it’s more accurate to see the cost of a trust as an investment, not an expense.

You're essentially investing in several critical benefits:

- Privacy: All your asset transfers happen completely outside of the public record.

- Efficiency: Your handpicked successor trustee can manage and distribute assets immediately, without waiting months or even years for court approval.

- Cost Savings: You are potentially saving your heirs from paying attorney, executor, and court fees that can easily eat up 3-8% or more of your estate's total value.

For a substantial estate, that initial investment can save your beneficiaries tens of thousands of dollars and an immeasurable amount of stress.

An asset not formally transferred into your trust is not governed by it and will almost certainly have to go through probate. This is why a "pour-over will" is a crucial safety net for any trust-based estate plan.

What Happens If I Forget to Put an Asset into My Trust?

This is a very common and understandable mistake. An asset that hasn't been formally retitled into the name of your trust is considered "unfunded." This just means it remains in your individual name and isn't controlled by the trust's terms when you pass away.

As a result, that forgotten asset will likely have to go through the probate process. To guard against this exact scenario, a well-drafted estate plan always includes a "pour-over will."

This special type of will acts as a safety net. Its only job is to "catch" any unfunded assets and instruct the probate court to move—or "pour"—them into your living trust. While this still requires a probate proceeding for those specific assets, it makes sure they ultimately end up under the management of your trust and are distributed according to your wishes, not state intestacy laws.

At Commons Capital, we specialize in creating integrated financial strategies that protect your legacy. If you're ready to build a comprehensive plan that ensures your assets are transferred privately and efficiently, we can help.

Learn more about our private wealth management services at Commons Capital.