A dedicated wealth manager for entertainers and celebrities builds a system that transforms volatile, project-based income into a stable financial foundation for life. Proper financial planning for this industry demands a playbook completely different from traditional financial plans, one that zeroes in on smoothing out irregular income, managing complex revenue streams, and protecting assets during those critical peak earning years.

The Unpredictability of Entertainment Income

For anyone in the entertainment world, income is almost never a steady paycheck. It's more like a series of tidal waves followed by long, quiet spells. A blockbuster film, a sold-out world tour, or a chart-topping album can generate an incredible amount of wealth in a very short time.

But those highs are often followed by lean periods between projects. This boom-and-bust cycle makes long-term financial stability a serious challenge and renders traditional budgeting almost useless. This is where irregular income financial planning HNW (high-net-worth) strategies become critical.

The Power of Financial Smoothing

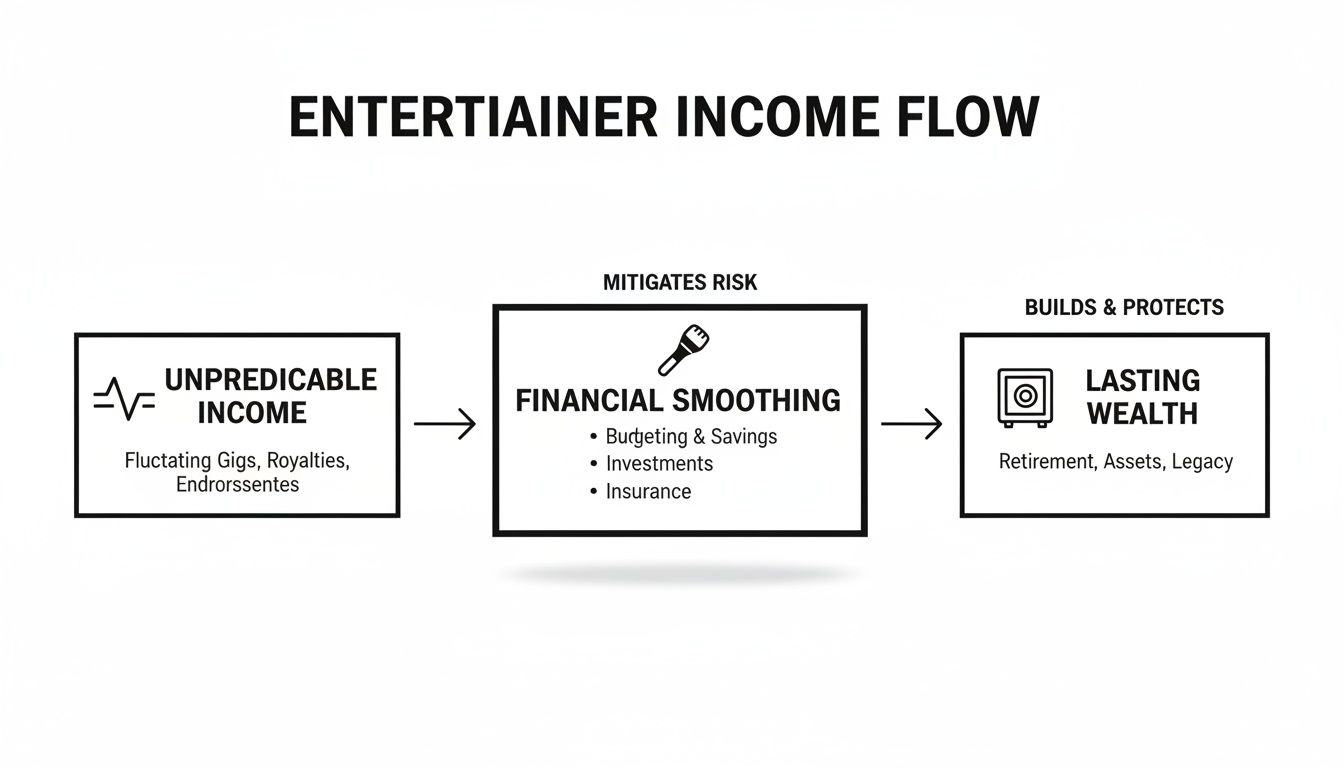

The core strategy for managing this kind of volatility is called financial smoothing. This isn't about pinching pennies or limiting your lifestyle. It's about creating a system that makes your personal income predictable, even when your professional earnings are anything but. The goal is to turn those unpredictable windfalls into a reliable, consistent salary.

An experienced wealth manager helps get this done by:

- Building a "War Chest": A significant portion of any large payout is immediately set aside into a liquid reserve account. This fund is what covers your fixed costs—mortgage, insurance, staff salaries—during the slower months.

- Paying You a "Salary": You receive a fixed, regular payment from your central business account. This mimics the stability of a traditional job, making it far easier to manage a personal budget and resist the urge to overspend after a big payday.

- Forecasting Cash Flow: Your team should be constantly analyzing contracts, royalty statements, and tour schedules to project future income and spot potential shortfalls months or even years in advance.

This kind of proactive management is the bedrock of sports and entertainment wealth management. It shifts the entire dynamic from reacting to income swings to controlling them.

This diagram shows how this process works, turning chaotic earnings into a dependable financial engine.

Without a deliberate smoothing strategy, even massive, unpredictable income rarely translates into lasting financial security.

Entertainer vs. Traditional High-Earner Financial Profile

This volatility is what makes an entertainer's financial life so different from other high-income professions. The reality is stark: research shows 73% of top-earning entertainers will see their income drop by more than 50% in at least one year within five years of their peak. You can read the full research about these creative industry financial trends to truly grasp the risks.

This fact alone proves why a generic financial plan from a conventional advisor just won’t cut it.

The differences become even clearer when you compare the financial profiles side-by-side. A doctor or lawyer builds wealth on a predictable, upward-sloping line. An entertainer's journey looks more like a mountain range, with towering peaks and deep valleys.

| Financial Aspect | Entertainer or Celebrity | Traditional High-Earner (e.g., Doctor, Lawyer) |

|---|---|---|

| Income Stream | Highly volatile, project-based, lump-sum payments | Stable, predictable, and incremental salary increases |

| Earning Window | Often short and concentrated into a few peak years | Long, steady career path spanning 30-40 years |

| Tax Complexity | Multi-state/international filings, varied income types | Primarily W-2 income with simpler state tax obligations |

| Key Risk | Lifestyle inflation during peaks, unsustainability in troughs | Career burnout or market downturn affecting a single firm |

Understanding these distinctions is the first step toward building a financial plan that actually works for a creative career. An expert in irregular income financial planning for HNW (high-net-worth) individuals recognizes that the goal isn't just to earn the money, but to structure it so it can support you for a lifetime.

Royalties, Residuals, and Licensing: How to Manage Them

While big paydays from a tour or a film shoot feel like the main event, they’re often just the beginning. The real, long-term wealth in this business comes from your intellectual property (IP). Think of it as a financial orchard that can bear fruit for decades through royalties, residuals, and licensing deals.

These are the cornerstones of generational wealth, but they’re also a minefield of complexity and frequent miscalculations.

Simply waiting for the checks to show up isn't a strategy—it's a gamble. A wealth manager for entertainers and celebrities helps you cultivate this income, not just collect it. They see these payments for what they are: deferred compensation you’ve already earned. Managing them right is the difference between temporary success and true financial freedom.

Auditing and Forecasting Your IP Income

First thing's first: you need to know exactly what you're owed. Royalty and residual statements are notoriously confusing and, frankly, often wrong. A single film can spit out hundreds of statements from different countries and platforms, making it nearly impossible for an artist to track it all.

Your financial team’s job is to go forensic on these statements, digging into the details to find what’s missing.

- Royalty Audits: Your team should be running regular audits on distributors, publishers, and record labels. It's not uncommon to find discrepancies of 5-15%. Over a career, that can easily add up to millions in lost income.

- Forecasting Future Earnings: By looking at historical data and what’s happening in the industry, a specialist can create a solid projection of what your back catalog will generate. This forecast is the key to smoothing out your cash flow, letting you plan your life and budget for years based on predictable IP earnings.

For creators, really getting a handle on your music publishing rights is non-negotiable. If you don't know what you own, you're just leaving money on the table. This kind of detailed tracking and forecasting is what turns a stream of unpredictable checks into a reliable financial asset.

Structuring Your Business for Optimal Growth

Getting paid is one thing; how you get paid is another. Funneling all that royalty and licensing income straight into your personal bank account is one of the biggest tax and liability mistakes you can make.

A dedicated business entity, like an LLC or S-Corp, is not just a suggestion; it's a necessity for any serious entertainer. It creates a firewall between your personal assets and business liabilities while unlocking powerful tax optimization strategies unavailable to individuals.

A financial advisor for entertainers will coordinate with your attorney and CPA to nail down the right structure for you. The goal is to build a central hub for all your professional income, which opens up some major advantages.

This setup makes tax planning more efficient and financial reporting crystal clear. It professionalizes your career, turning it from a hustle into a well-oiled business.

Key Benefits of a Business Entity

Setting up a formal business entity is a fundamental move in sports and entertainment wealth management. It’s the engine that lets your team execute a real long-term financial plan.

Tax Optimization:

An S-Corp, for example, can create huge savings on self-employment taxes. It lets you pay yourself a "reasonable salary" (which is subject to payroll taxes), but any profits beyond that can be taken as distributions, which aren't hit with the same tax burden.

Asset Protection:

By drawing a clean line between your business and personal finances, an LLC shields your personal assets—your home, your savings—from lawsuits or other liabilities that might come up in your professional life.

Legacy and Estate Planning:

A business entity makes it infinitely easier to manage and eventually pass your IP assets down to your heirs. Your catalog can keep providing for your family for generations, but only if it's held and managed properly within a trust or business structure. This is how you turn a successful career into a lasting legacy.

Brand Deal and Endorsement Income Planning

In the entertainment world, brand deals and endorsements can be game-changers. A single partnership might bring in more money than years on the road or in the studio. But seeing that check as just a pile of cash is a huge mistake—it’s an opportunity you can’t afford to fumble.

The key is shifting your mindset from "how much?" to "how well?" The best deals aren't just about the upfront payment; they're about aligning with the right brand and building your own personal equity for the long haul. A bad deal can tarnish your brand, and that financial damage can stick around long after the money is gone.

This is where a wealth manager for entertainers and celebrities becomes essential. They work right alongside your agent and lawyer, but with a different focus: making sure the financial guts of the contract are built to create lasting wealth, not just a temporary bump in your bank account.

Deconstructing the Deal Structure

The negotiation table is where long-term value is either built or destroyed. A sharp financial team won't get star-struck by the headline number. They’ll dig into the mechanics of the deal and how every clause impacts your bigger financial picture.

From a wealth management perspective, here are the points that really matter:

- Payment Structures: Does a lump sum make the most sense, or could a performance-based deal with bonus escalators earn you more over time? A lump sum gives you capital to work with immediately, but a performance deal can create a steady income stream tied to the campaign's success.

- Usage Rights and Term: How long can the brand use your image, and where? Keeping these terms tight can leave the door open for other deals in different product categories or countries down the line.

- Exit Clauses and Morality Clauses: What’s the escape plan if the brand’s reputation takes a hit, or if your public image shifts? A well-written exit clause protects you from being tethered to a sinking ship.

Of course, to get to the negotiation, you need a killer pitch. Looking at successful influencer media kit examples can give you a real edge in crafting your presentation and starting the conversation from a position of strength.

The Power of Income Tranching

Once that big check from a brand deal actually lands in your account, the real work starts. The smartest way to handle this kind of irregular income financial planning for HNW clients is a strategy called "income tranching." It’s a simple but disciplined system for carving up a large payment into specific buckets before you spend a single dollar.

Income tranching prevents a large, one-time payment from simply funding a short-term lifestyle upgrade. Instead, it forces a strategic allocation that prioritizes tax obligations, savings, and long-term investment goals, ensuring the deal accelerates your journey to financial independence.

This method brings clarity and control to what can otherwise feel like a chaotic cash infusion, turning it into a structured, wealth-building event.

A typical income tranching plan breaks down like this:

- Tax Bucket (35-50%): The very first move. A huge slice of the gross payment goes directly into a separate, high-yield savings account just for taxes. This move alone prevents a nightmare tax bill from wrecking your plans next April.

- Lifestyle & "War Chest" Bucket (10-20%): This is for refilling your cash reserves. It covers your personal "salary" for the next 6-12 months, making sure your living expenses are handled without depending on future gigs. It’s your financial foundation.

- Long-Term Investment Bucket (40-55%): This is the engine for building real wealth. The rest of the money—often the largest portion—is put to work immediately in your long-term investment portfolio, whether that's in growth stocks, real estate, or other assets outlined in your financial plan.

Following this disciplined model with a financial advisor for entertainers ensures that a massive brand deal doesn't just fund a few good years—it becomes a powerful accelerator for your entire financial future.

Protecting Wealth During Peak Earning Years

The money you make at the height of your career is incredible. It's also temporary. That window for maximum income can slam shut faster than anyone expects, which is why you have to build a financial plan that's designed to last a lifetime, not just until the next album drops or the series wraps.

This isn't about tucking away whatever's left over at the end of the month. It's about having a disciplined game plan for every dollar that comes in—a system that top wealth managers use to turn today's high earnings into durable, long-term wealth that works for you long after the final curtain call.

Building Your Financial Fortress

The foundation of protecting your wealth is a clear, repeatable system for where your money goes. This means aggressive saving, smart debt management, and building a truly diversified investment portfolio. For entertainers, who often operate as a business of one, tools like a SEP-IRA or a Solo 401(k) are absolute must-haves.

These aren't your standard retirement accounts. They allow you to contribute far more than a typical IRA, letting you shield a huge chunk of your income from taxes right now, during your highest-earning years. A good financial advisor will make sure you’re maxing these out every single year. It’s one of the most powerful moves you can make to build a massive nest egg while cutting your current tax bill.

The Three-Bucket Investment Strategy

Saving money is one thing; turning it into real wealth is another. To do that, the money needs to be invested wisely. One of the most effective frameworks in sports and entertainment wealth management is the "three-bucket" strategy. It’s a simple way to organize your investments based on what you need them to do for you.

The Liquidity Bucket (Safety): Think of this as your financial bedrock. It’s 12-24 months of living expenses parked in safe, easy-to-access accounts like a high-yield savings or money market fund. This cash ensures you can ride out long gaps between projects without financial stress or being forced to sell your long-term investments at the worst possible time.

The Growth Bucket (Long-Term): This is your wealth-building engine. This money is invested for the long haul in a diversified mix of global stocks, index funds, and ETFs. The goal here is to crush inflation and compound over decades. This is the capital you won’t touch for at least 5-10 years.

The Alternative Bucket (Opportunity): For high-net-worth entertainers, this bucket adds another layer of diversification beyond the public markets. It might hold investments in real estate, private equity, venture capital, or even direct investments into projects that align with your brand. These assets are usually harder to sell quickly but can offer higher returns that don't always move in lockstep with the stock market.

A disciplined three-bucket strategy gives your money a purpose. It perfectly balances the need for immediate security with the critical goal of long-term growth, making sure your wealth is working for you across different timelines.

Insuring Your Most Valuable Asset

Finally, a core piece of any solid financial plan is managing risk. Your single most valuable financial asset isn't your house or your car—it’s your ability to earn. A career-ending injury, a sudden illness, or a public liability issue can threaten everything you've built.

This is why specialized insurance isn’t a "nice-to-have." It's essential.

- Disability Insurance: This pays you an income if you can't work due to an injury or illness. For a musician whose hands are their livelihood or a performer who depends on their physical health, a high-limit, "own-occupation" policy is non-negotiable.

- Liability (Umbrella) Insurance: As a public figure, you're a bigger target for lawsuits. A good umbrella policy adds an extra layer of protection on top of your home and auto insurance, shielding your assets from legal claims. You can learn more about methods for protecting assets from lawsuits in our detailed guide.

A seasoned wealth manager makes sure these policies are in place and scaled correctly to your net worth. It’s the final piece of the puzzle in fortifying your wealth—protecting not just what you have now, but your power to earn in the future.

Philanthropy and Legacy for Public Figures

For many successful entertainers, wealth isn't just about the number in your bank account. It's a powerful tool—one that can build a legacy and create an impact that echoes long after the final curtain call.

The final act of a truly solid financial plan shifts from just growing and protecting your money. It’s about channeling your success into causes you’re passionate about and making sure your assets are passed down smoothly, privately, and on your terms.

This is where philanthropy and estate planning come together. It’s not just about giving back; it's about designing a strategy that reflects your values and, frankly, comes with significant tax benefits that can amplify your generosity. A wealth manager for entertainers and celebrities is indispensable here, helping you cut through the noise and turn your vision into a reality.

Strategic Philanthropy for Public Figures

As an entertainer, giving back presents a unique chance to sync your personal brand with what you truly care about. When you get it right, it creates a powerful, positive legacy that can even outshine your professional work. This is about more than just writing a check—it's about building a structured, impactful giving program.

To move past simple donations, you need to use more formal vehicles to direct your giving.

- Donor-Advised Funds (DAFs): Think of a DAF as your own personal charitable savings account. You make a sizable, tax-deductible contribution now, let the funds grow tax-free, and then recommend grants to your favorite charities whenever you choose. They’re simple and offer immediate tax perks.

- Private Foundations: If you’re looking to make a major, long-term commitment, a private foundation gives you the ultimate control. You can get your family involved, build a public platform for your cause, and create an institution that will last for generations. Be warned, though—they come with much heavier administrative and regulatory burdens.

- Charitable Trusts: These are legal setups that let you support a charity while also creating financial benefits for yourself or your heirs. A Charitable Remainder Trust, for instance, can pay you an income stream for life, with whatever is left going to a charity you designate after you pass away.

The real key is picking the right tool for your specific goals, financial picture, and how hands-on you want to be.

Aligning Your Giving with Your Brand

Strategic philanthropy is also about being intentional. Many public figures discover their impact is magnified when their giving is tied to their personal story. A musician might back music education in underserved schools. An actor could champion a cause connected to a role that profoundly changed them.

Aligning your philanthropic efforts with your public persona creates an authentic narrative that resonates with your audience and amplifies your message. It transforms your giving from a financial transaction into a powerful statement of your values.

This approach doesn't just maximize your social impact. It can also strengthen your brand and deepen the connection you have with your fans.

Privacy and Protection in Estate Planning

While your public giving shapes your legacy, private estate planning is what ensures it’s protected and passed on securely. For celebrities, privacy is everything. A standard will is a public document once it hits probate court, throwing the doors wide open on your finances, your assets, and your heirs for anyone to see.

This exposes your family to a level of public scrutiny and unwanted attention they just don’t need.

Effective financial planning for entertainers and celebrities absolutely must prioritize protecting your family from this kind of exposure. The best tool for the job is almost always a revocable living trust.

By retitling your major assets—your home, investment accounts, intellectual property—into the name of the trust, you can completely sidestep the public probate process.

What does that mean in plain English? The details of your estate, including who gets what and how much, stay completely private. It’s a critical step to shield your heirs from the media, financial predators, and frivolous lawsuits. A trust ensures the wealth you’ve worked so hard to build is transferred smoothly, efficiently, and exactly as you wished—far from the public eye.

Ready to build a financial plan that can withstand the demands of an entertainment career? Speak with our entertainment wealth specialists. Schedule your consultation today.