When planning your legacy, the choice between a living trust and a will is one of the most critical decisions you'll make. The core difference boils down to a fundamental trade-off: control versus complexity, and privacy versus public process. A will eventually becomes a public document, guided through the court system in a process called probate. A living trust will strategy, on the other hand, operates primarily in private, keeping your affairs out of the courts and away from public view.

Getting this single distinction right is the first, most crucial step toward protecting your assets and ensuring your family's future is secure.

Decoding Your Estate Planning Choices

Let's be honest—thinking about estate planning can feel overwhelming, and it’s a task that’s incredibly easy to push to the back burner. This is a common hurdle, but once you get clear on your options, the path forward becomes much more manageable. You're not just signing legal documents; you're deciding how you want your legacy handled—with privacy, efficiency, and your direct control.

Think of this guide as your roadmap. We’ll cut through the legal jargon and focus on the two main vehicles for securing your assets for the next generation:

- The Will: A foundational legal document that lays out your final wishes. It’s straightforward but must go through a public, court-supervised process to be executed.

- The Living Trust: A private arrangement that lets you manage your assets seamlessly during your lifetime and ensures they pass to your heirs without court intervention.

Before we dive into the details, let's take a quick look at the core differences.

Living Trust vs Will at a Glance

This table offers a high-level summary of the fundamental differences between a living trust and a will, helping you quickly grasp the key distinctions before we dive into the details.

As you can see, the right choice really depends on what you value most—simplicity and lower upfront cost, or privacy, control, and probate avoidance.

Why Planning Ahead Is Crucial

It's surprisingly common to put off estate planning. A recent study showed that a staggering 55% of Americans don't have any estate planning documents in place. Just 31% have a will, and a mere 11% have set up a living trust. The top reason? People simply haven't gotten around to it, even if they know it's important.

The real cost of doing nothing isn't just financial—it's the complete loss of control. If you don't have a plan, state laws will decide who gets your assets and, more importantly, who cares for your dependents. That’s a scenario no one wants.

A well-crafted plan guarantees your wishes are followed to the letter. As you start thinking about this, a great first step is to understand if you need an estate plan and what it should accomplish for you. That foundational knowledge is what empowers you to choose confidently between a will and a living trust. This guide will give you that clarity, helping you move from hesitation to action.

Understanding a Will: The Foundation of Estate Planning

Before we dive into the complexities of living trusts, we have to start with the cornerstone of every estate plan: the will. Think of a will, formally known as a last will and testament, as the essential instruction manual for what happens after you’re gone. It’s a legally binding document that spells out your final wishes, making sure your assets end up exactly where you want them.

A will is a pretty straightforward document. It doesn't do anything while you're alive. It just sits quietly, waiting. Only after you pass away does it spring into action, kicking off a court-supervised process called probate. This is where a judge authenticates the will and oversees the distribution of your assets according to your instructions.

The Core Functions of a Will

A will does more than just hand out your property. It has a few critical jobs that no other document can handle, which is precisely why you still need one even if you have a living trust.

Here's what it's responsible for:

- Naming an Executor: This is the person or institution you trust to carry out your will’s instructions. They are your chosen manager for settling your final affairs.

- Designating Beneficiaries: This is where you get specific about who gets what—from your house and investment accounts to sentimental family heirlooms.

- Appointing Guardians for Minor Children: This might be the single most important function of a will. It is the only place you can legally name guardians to raise your children if the unthinkable happens.

If you don't have a will, you're leaving these massive decisions up to the state. A judge who has never met you will appoint someone to manage your estate and, more importantly, decide who will raise your kids. That's a scenario most parents would do anything to avoid.

Who Is the Executor and What Do They Do?

Your executor is the quarterback of your estate settlement. You need to pick someone who is trustworthy, organized, and responsible because they have some serious legal and financial duties ahead of them. This person effectively steps into your shoes to manage your estate through the probate process.

Here’s a look at their key responsibilities:

- Filing the Will with the Probate Court: They kick off the legal process by submitting your will to the court.

- Locating and Managing Assets: The executor has to find everything you own—bank accounts, real estate, personal belongings—and secure it.

- Paying Debts and Taxes: Before your heirs get anything, the executor must use estate funds to pay off any outstanding debts, final bills, and taxes.

- Distributing Property to Heirs: Once all the bills are paid, the executor follows your will’s instructions to distribute the remaining assets to your beneficiaries.

An executor has a fiduciary duty, which is the highest legal standard of care. This means they are legally obligated to act solely in the best interests of the estate and its beneficiaries, without any personal gain or conflict of interest.

The Limitations of a Will

For all its importance, a will isn't perfect. It has some significant limitations, which is why so many people look to living trusts as a better alternative. The biggest drawback? A will guarantees your estate will go through probate. This court process can be incredibly slow, often dragging on for months or even years.

On top of that, probate is a public affair. Your will becomes a public record, along with a complete inventory of your assets and debts. Anyone can walk into the courthouse and see exactly what you owned and who you owed. For families who value their privacy, especially high-net-worth individuals, this is a major concern.

Understanding these shortcomings is the first step in appreciating why a living trust is such a powerful tool in modern estate planning.

Exploring a Living Trust: The Private Alternative

While a will is a cornerstone of any good estate plan, a living trust offers a more powerful and private way to manage your legacy. Don't think of it as just a set of instructions for after you're gone. A living trust is a dynamic legal entity you create to hold and manage your assets—one that works for you during your lifetime and continues to operate seamlessly when you're no longer here.

The process is pretty straightforward. You, as the Grantor, create the trust and then transfer your assets into it. This key step is called funding the trust. Once that's done, the assets are technically owned by the trust itself, not you personally. But don't worry—you still have complete control.

The Key Players in Your Trust

To really get a handle on living trusts, you need to know the three essential roles involved. These might sound like complex legal terms, but the concepts are simple. In the beginning, you'll almost certainly wear all three hats yourself.

- The Grantor (or Settlor): This is you—the person creating the trust. You set the rules, define the terms, and decide which of your assets go inside.

- The Trustee: This is the manager. The trustee is responsible for handling the trust's assets according to the rulebook you created. You’ll serve as your own trustee at first, which means nothing changes in how you control your money.

- The Beneficiary: This is whoever benefits from the trust's assets. During your lifetime, you are the primary beneficiary. You can use your money and property just as you always have.

This setup ensures that even though your assets are technically titled in the trust's name, your day-to-day financial life feels exactly the same. You can still buy, sell, invest, and spend your money however you see fit.

How a Trust Handles Incapacity and Death

This is where the real power of a living trust shines. In the trust document, you'll name a successor trustee—the person or institution you've chosen to take over management of the trust if you become incapacitated or pass away.

The handoff is seamless and automatic, with no court intervention required. If you become unable to manage your own affairs, your successor trustee steps in immediately to pay bills, oversee investments, and handle your finances according to your wishes.

By planning for incapacity, a living trust provides a powerful layer of protection that a will simply cannot offer. It avoids the need for a costly and public court process known as guardianship or conservatorship, keeping your family's private matters out of the courthouse.

When you pass away, your successor trustee acts much like a will's executor. They are responsible for gathering the trust's assets, paying final debts and taxes, and distributing what's left to your named beneficiaries. The crucial difference? This entire process happens privately and completely outside of probate court.

This privacy and efficiency are why so many people, especially those with significant assets, choose a living trust. While there are different kinds of trusts, you can learn more about the distinction between a trust and a living trust to see how they function differently.

Bypassing probate doesn't just save your family an enormous amount of time and money; it also shields your financial affairs from public record. Your legacy is distributed as a private family matter—exactly as you intended.

Key Differences Where a Living Trust Shines

When you start comparing a living trust vs. a will, the real distinctions pop up in a few critical areas. Think of them both as essential tools in your estate planning toolkit, but a living trust has some serious advantages when efficiency, privacy, and control are at the top of your list. Nailing down these differences is the key to figuring out which one truly protects your assets and serves your family best.

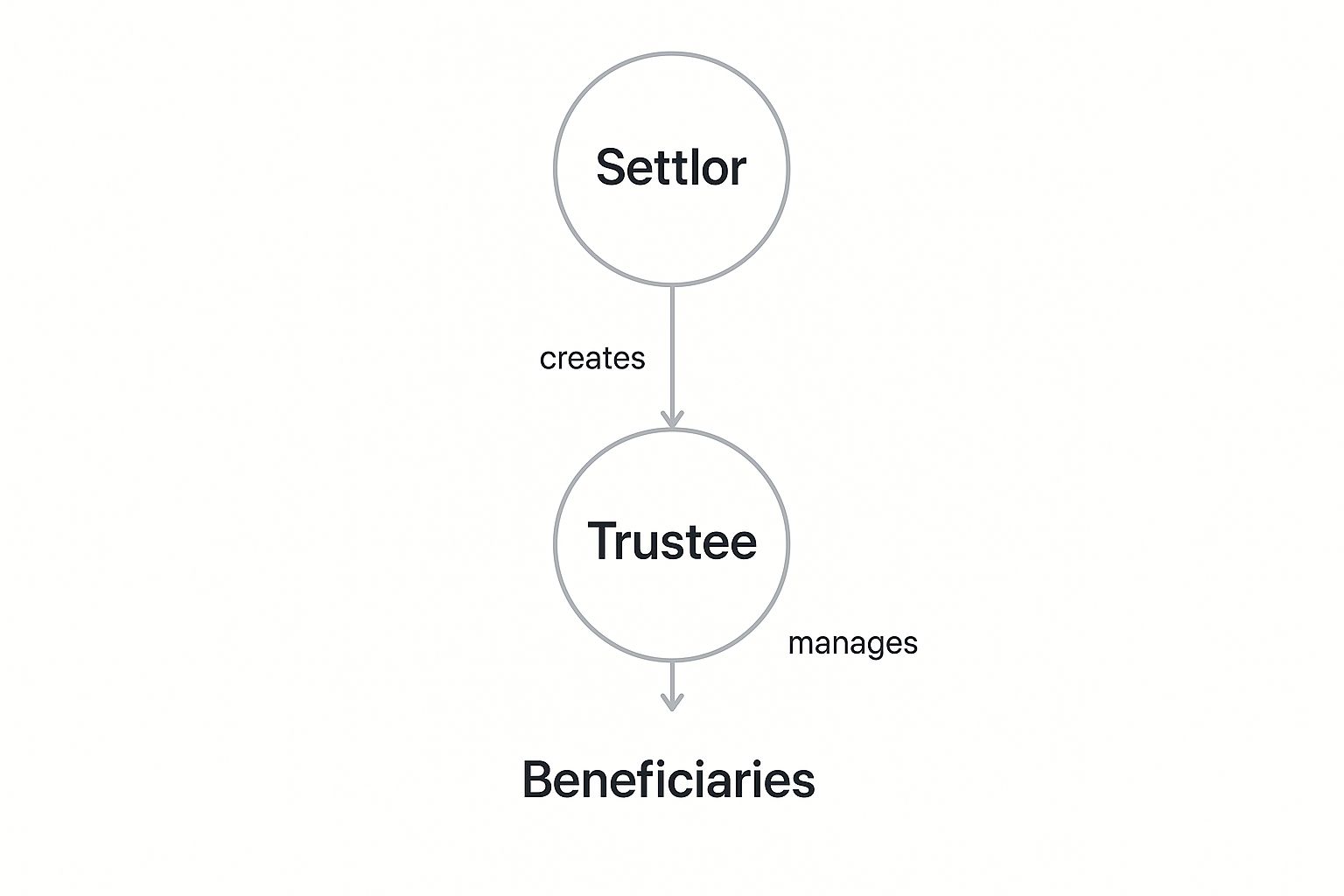

The image below breaks down the three main players in a living trust: the Settlor (that’s you, the creator), the Trustee (the manager), and the Beneficiaries (the folks who receive the assets).

As you can see, the Settlor keeps the reins, often by serving as the first Trustee. This setup lets you direct how everything flows to your beneficiaries, all while keeping the process private and completely out of a courtroom.

The Probate Process

The single biggest difference between a will and a trust? Probate. A will all but guarantees your estate will land in this public, court-supervised process. Probate is the court's way of validating your will, paying off creditors, and legally transferring assets to your heirs. It’s methodical, but it can be a painfully slow and expensive ordeal.

A living trust, on the other hand, is specifically engineered to avoid probate entirely. Because the trust technically owns the assets—not you personally—there’s nothing for the court to administer when you pass away. Your chosen successor trustee simply steps in and distributes the assets according to your private instructions. The courthouse doors never open.

This is a huge deal. Skipping probate saves your family a tremendous amount of time—often months, sometimes years—and helps them sidestep legal and administrative fees that can eat away at the value of an estate.

Privacy Concerns

Here’s something many people don’t realize: because a will is filed with the court, it becomes a public record. That means anyone—a nosy neighbor, a distant cousin, or even a predatory business—can look up a detailed inventory of your assets, see who you owed money to, and find out exactly who got what. For anyone who values discretion, especially high-net-worth individuals, this level of public exposure is a massive drawback.

A living trust operates in a completely different world. It’s a private document, period. Its terms, the assets it holds, and the identities of your beneficiaries are never filed with a court or made public. The entire distribution process is handled confidentially between your trustee and your loved ones.

This level of privacy is a cornerstone of modern estate planning. It protects your family from unwanted solicitations and prevents public scrutiny of your financial affairs, allowing your legacy to be managed as a private family matter.

This privacy isn't just about the numbers. It keeps sensitive family dynamics—like unequal distributions to children or gifts to non-relatives—out of the public eye, which can go a long way in preventing potential disputes.

Managing Incapacity

Life is unpredictable. A solid estate plan has to account for the possibility that you might become incapacitated—alive, but unable to manage your own financial affairs due to an illness or injury. This is another area where a living trust truly shines.

If all you have is a will, it offers zero protection while you're alive. In a case of incapacity, your family would have to go to court and petition to have a conservator or guardian appointed to manage your finances. It's a public, expensive, and often emotionally draining process.

A living trust, however, comes with incapacity planning built right in. You name a successor trustee from the start, clearly designating who will take over your financial affairs if you can't. The transition is seamless and immediate, with no court intervention required. Your successor trustee can step in to pay your bills and manage your investments without missing a beat, ensuring your financial life continues smoothly.

For a great, straightforward breakdown of these key differences, you can find more on wills vs. trusts explained in plain English.

How a Will and Living Trust Work Together

Lots of people think they have to choose between a will or a living trust, seeing it as an "either-or" decision. But in reality, the strongest estate plans don’t pick one over the other—they use both. They aren't rivals; they're partners that work in concert to create a comprehensive safety net for your family.

This powerful combination covers all the bases. The living trust does the heavy lifting, like managing your assets and keeping them out of probate court. Meanwhile, the will steps in to handle a few critical jobs that a trust legally can't touch.

The Pour-Over Will: A Critical Backup Plan

When you set up a living trust, you'll also create a special type of will called a pour-over will. Think of it as your estate’s ultimate fail-safe. Its primary job is simple: to "catch" any assets you forgot to put in your trust and "pour" them into it after you pass away.

Life gets busy, and it’s surprisingly easy to overlook an asset. You might buy a new car, inherit a small piece of property, or open a new investment account and just not get around to formally transferring it. Without a pour-over will, those forgotten assets would be stuck in limbo, forcing your family to deal with the public probate process just to have them distributed according to state law.

The pour-over will prevents this mess. It directs all those leftover assets straight into your trust, ensuring everything is ultimately handled according to your private wishes.

Guardianship: An Essential Role Only a Will Can Fill

This is one of the most important points for parents with young kids: a living trust cannot name guardians for your minor children. This is a job that only a will can legally perform.

If you have minor children, a will isn't optional—it's an absolute necessity. It is the sole legal document where you can nominate the person or people you trust to raise your children if you're no longer there to do it yourself.

Without a will, that deeply personal decision falls to a judge who doesn't know you, your family, or your values. This fact alone makes the pour-over will an indispensable part of any family’s living trust will strategy. It makes sure that while your trust is busy managing your financial legacy, your will is protecting your most precious one. For a deeper dive into crafting a complete strategy, explore our resources on comprehensive trust and estate planning.

While it's true that assets caught by a pour-over will still have to go through probate, the process is dramatically simplified. The will has just one beneficiary: the trust. As soon as the assets are officially transferred, the private terms of your trust take over, shielding the final distribution from public view and making the whole settlement process smoother for your loved ones.

Making the Right Choice for Your Family

So, how do you navigate the choice between a will and a living trust? It all comes down to one goal: creating a secure future for the people you love. By now, you’ve seen the unique roles these two documents play. The real question isn’t which one is “better,” but which is the right fit for your financial picture, your family, and what you want to accomplish.

The answer lies in a few key questions about your life and assets. For some, especially those just starting out with a straightforward financial life, a simple will gets the job done. For others, the robust protection and privacy offered by a living trust are absolutely essential.

When a Simple Will Might Suffice

If you’re young, single, or a couple with few assets and no real estate, a standalone will is often a perfectly reasonable starting point. Its biggest advantages are its simplicity and lower upfront cost.

A will is often enough if you:

- Are early in your career with limited savings.

- Don’t own any real estate.

- Primarily want to name guardians for minor children—a critical task that only a will can perform.

In these cases, the effort and expense of setting up and funding a trust might be overkill for now. The main goal is simply to have a legal document in place that outlines your basic wishes and, most importantly, protects your kids.

Scenarios Where a Living Trust Is Strongly Recommended

As your life gets more complex and your assets grow, the benefits of a living trust really start to shine. It offers a level of control, privacy, and efficiency that a will just can’t provide on its own.

A plan that combines a living trust and a will is almost always the best strategy for anyone who:

- Owns real estate: Putting your property into a trust is the single most effective way to make sure it passes to your heirs without the frustrating delays and high costs of probate.

- Has significant assets: If you have a substantial investment portfolio, business interests, or savings, a trust ensures that everything is managed and distributed privately.

- Prioritizes privacy: A will becomes a public record. If keeping your financial affairs out of the public eye is important to you, a trust is the only tool that guarantees it.

- Wants to plan for incapacity: A trust allows your chosen successor trustee to step in and manage your finances seamlessly if you become unable to, avoiding a public, expensive, and stressful court proceeding.

It’s interesting to see how demographics and even where you live can play a role. For instance, recent data shows that residents in the Western U.S. are most likely to have a trust, at 17%. This is likely driven by high-value real estate markets where avoiding probate can save a family a small fortune. On the flip side, only 8% of people in rural areas have a trust. You can discover more insights about these estate planning trends and see how they vary across the country.

Your estate plan isn't just a stack of legal documents; it’s a reflection of your priorities. The choice between a will and a trust often comes down to how much control and privacy you want for your family’s future.

To help you find your path forward, ask yourself the following questions. Your answers will give you a solid framework for a productive conversation with an estate planning attorney, empowering you to make a decision you can feel confident about.

- Do I own a home or any other real estate?

- Do I own property in more than one state?

- Are my total assets large enough that avoiding probate is a major financial benefit?

- Is keeping my family’s financial affairs private a top priority for me?

- Do I have a blended family or other complex family dynamics?

- Do I want to spare my loved ones from a public and lengthy court process?

If you answered "yes" to even one of these questions, it’s a strong indicator that a living trust is the right choice for your family’s security and your own peace of mind.

Common Questions About Living Trusts and Wills

Even after you get the hang of the basics, a few specific questions always seem to pop up when it's time to choose between a living trust and a will. Getting these last few details ironed out is often the final step needed to feel truly confident in your decision.

Let's tackle some of the most common questions we hear to clear up any lingering confusion.

Is a Living Trust Really That Much More Expensive Than a Will?

This is a classic "pay now or pay later" situation. A will is almost always cheaper to create upfront. No doubt about it. But the total cost of a will isn't realized until after you're gone, when your estate enters probate. That process brings court costs, attorney fees, and executor compensation that can take a significant bite out of the inheritance you intended for your family.

A living trust, on the other hand, requires a bigger investment to set up and fund correctly. Yet, that upfront cost is often just a fraction of what a family might end up spending on probate down the road. By sidestepping probate entirely, a living trust can save your estate a substantial amount of money in the long run. For homeowners or anyone with considerable assets, it often proves to be the more cost-effective choice.

How Often Should I Update My Estate Plan?

Think of your estate plan as a living document, not something you set in stone and forget. It needs to evolve as your life does. A good rule of thumb is to pull out your living trust and will for a review every three to five years.

However, some life events are so significant they should trigger an immediate check-in to make sure your documents still reflect your wishes.

You’ll want to schedule a review after any of these milestones:

- Marriage, divorce, or remarriage: These events have a direct and immediate impact on who your beneficiaries are and how assets should be split.

- Birth or adoption of a child: New family members need to be included, and if you have a will, this is when you’ll name guardians.

- A big change in your financial picture: Coming into a large inheritance, selling a business, or making a major investment can change the entire landscape of your estate.

- Moving to a new state: Estate planning laws are not universal; they vary by state. Your documents might need a tune-up to stay valid and effective.

Does a Living Trust Protect My Assets from Creditors?

This is a critical and very common misconception. A standard revocable living trust does not shield your assets from your own creditors. Because you keep full control over the assets and have the power to revoke the trust at any time, the law essentially sees those assets as your personal property. Creditors can absolutely come after them to satisfy your debts.

For true creditor protection, you'd need to explore more complex tools like irrevocable trusts. But those come with a major trade-off: you have to give up control over the assets you place inside them. The real power of a revocable living trust lies in probate avoidance, planning for incapacity, and maintaining your privacy—not in shielding assets from creditors.

Beyond these questions, people often want to know about the practical side of things, like how long probate takes, a timeline that is massively influenced by the estate planning choices you make today.

At Commons Capital, we understand that navigating the complexities of estate planning is a critical part of wealth management. Our team is dedicated to helping high-net-worth individuals and families craft strategies that preserve their legacy and provide peace of mind. To learn how we can help you achieve your financial goals, visit us at https://www.commonsllc.com.