Think of your real estate portfolio as having a hidden reservoir of cash. A cost segregation study is the key to unlocking it. The biggest wins here are accelerated depreciation deductions and a massive boost to your immediate cash flow. It’s a powerful, IRS-approved tax strategy that acts as a financial accelerator for any serious real estate investor.

Unlock Immediate Tax Savings with a Cost Segregation Study

While standard depreciation offers a slow, steady trickle of tax benefits over decades, a cost segregation study opens the floodgates. By meticulously identifying and reclassifying parts of your property, you can drastically shorten their depreciation timelines. The trick is to stop thinking of your building as a single asset and start seeing it as a collection of hundreds of individual parts.

Instead of lumping everything into a 27.5-year (residential) or 39-year (commercial) depreciation schedule, this engineering-based analysis pulls out all the shorter-lived assets.

This can include items like:

- Carpeting and specialty flooring

- Decorative lighting and custom cabinetry

- Dedicated electrical systems for specific equipment

- Landscaping, paving, and other exterior improvements

When you reclassify these items from long-term real property to short-term personal property—with lifespans of 5, 7, or 15 years—you get to front-load your depreciation deductions into the very first years you own the property.

This strategic reclassification creates significant paper losses, which directly slash your current taxable income and free up a substantial amount of cash. You’re essentially transforming a future tax benefit into immediate liquidity, giving you capital to reinvest and build real wealth.

The Financial Impact of a Study

The return on investment can be both substantial and immediate. For a $1 million commercial property, for instance, a cost segregation study can often generate $40,000 to $60,000 in tax savings in year one alone.

Considering a typical study might cost around $10,000, that translates to an immediate 4x to 6x return on your investment. That impact becomes especially potent when paired with bonus depreciation. This isn’t just a minor accounting tweak; it’s a fundamental shift in how you manage your property’s tax basis.

The table below gives you a clearer picture of how these returns scale with property value.

Estimated Year-One ROI from Cost Segregation

This table illustrates the potential first-year tax savings and return on investment (ROI) from a cost segregation study across different property values, highlighting the scalability of this strategy.

| Property Value | Typical Study Cost | Estimated Year-One Tax Savings | Projected ROI |

|---|---|---|---|

| $1,000,000 | $10,000 | $40,000 - $60,000 | 400% - 600% |

| $5,000,000 | $20,000 | $200,000 - $300,000 | 1,000% - 1,500% |

| $10,000,000 | $35,000 | $400,000 - $600,000 | 1,140% - 1,715% |

| $25,000,000 | $60,000 | $1,000,000 - $1,500,000 | 1,660% - 2,500% |

As you can see, the ROI becomes incredibly compelling as the value of the asset increases, making it a cornerstone strategy for larger portfolios.

Ultimately, this approach gives you what is essentially an interest-free loan from the government. It provides capital that can be put back to work in your portfolio right away. Instead of waiting decades for small deductions, you get a large chunk of tax savings now, when that money has the greatest potential to grow.

By exploring a range of tax reduction strategies, you can see how cost segregation fits into a larger financial plan. Understanding the core benefits empowers you to make smarter financial decisions, turning your properties into highly efficient cash-flow engines from day one.

How a Cost Segregation Study Actually Works

So, what really happens during a cost segregation study? Forget a standard property appraisal. Think of it more like a forensic audit of your building, performed by a specialized team of engineers and tax experts.

Instead of seeing one single asset, they see a collection of hundreds of individual components. Each one has its own specific lifespan and, crucially, its own depreciation schedule. This detailed engineering analysis is designed to legally maximize your tax deductions by separating these assets into their proper IRS-approved categories.

It’s a well-established, defensible tax strategy, grounded in decades of IRS rules and court cases.

The Step-by-Step Study Process

A cost segregation study is an engineering-driven process that meticulously dissects a property to unlock its hidden tax value. It follows a clear, methodical path from start to finish.

The main goal is to shift assets from the default 27.5-year or 39-year depreciation schedules into much faster 5-year, 7-year, or 15-year categories.

Here’s how a typical study unfolds:

- Initial Property Analysis: The process kicks off with a thorough review of all available documents. This means digging into blueprints, cost records, purchase agreements, and architectural drawings to get a baseline understanding of the property's construction and cost basis.

- On-Site Inspection: This is the most critical phase. Engineers physically walk the property to identify, photograph, and document every single component. They’re looking at everything from specialized plumbing and decorative lighting to the parking lot paving and surrounding landscaping.

- Cost Estimation and Allocation: Next, the team assigns a cost to each component they identified. If the original invoices aren't available, they use established construction cost-estimating guides to determine the value of each piece.

- Final Report Generation: All these findings are compiled into a comprehensive report. This document provides the detailed engineering and legal justification for reclassifying the assets, serving as your primary support in the event of an IRS review.

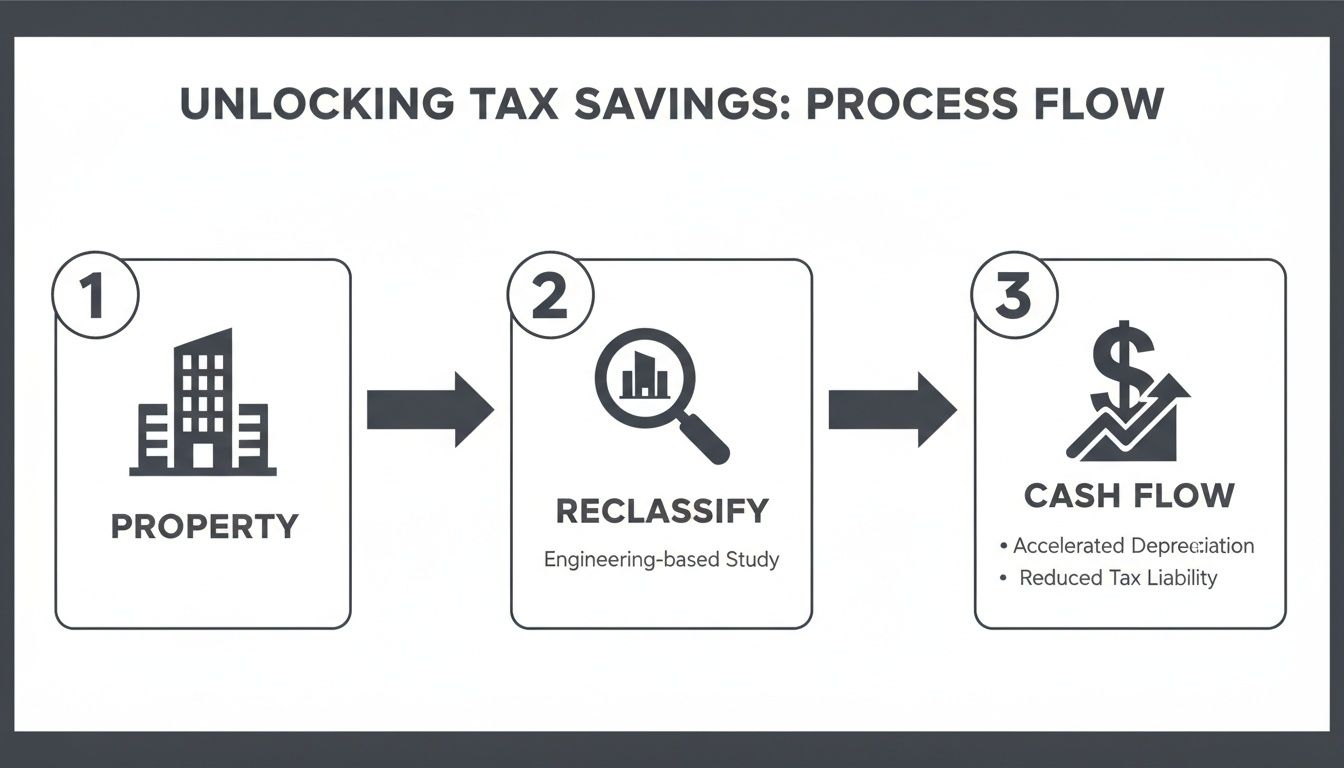

This simple flow from property to cash flow is powerful in practice.

As you can see, the study directly connects the physical components of your building to reclassification, which in turn improves your cash position.

Identifying Assets That Qualify for Faster Depreciation

The real power of a cost segregation study is its ability to separate personal property from real property. The IRS has very specific definitions for this, which is precisely why an engineering-based approach is essential.

Think of it like taking apart a brand-new car. The frame and chassis are the long-life structural elements—the real property. But the engine, tires, seats, and custom sound system are all individual components with much shorter lifespans. They are the personal property.

A cost segregation study does exactly that for your building.

An expert team isn't just looking for what's easily removable. They analyze whether an asset is related to the operation of the building itself or to the specific activities of the business within it. This distinction is a key part of maximizing the cost segregation study benefits.

Some of the most common assets reclassified for accelerated depreciation include:

- Interior Finishes: Things like carpeting, vinyl flooring, and decorative millwork.

- Specialty Systems: Dedicated electrical wiring for equipment, specific plumbing for commercial kitchens, or reinforced flooring for heavy machinery.

- Exterior Improvements: Landscaping, sidewalks, fencing, and parking lots.

- Decorative Elements: Custom lighting fixtures and other ornamental features that aren't essential to the building’s basic function.

This entire strategy is built on a solid legal foundation of IRS guidance and court rulings. A reputable firm relies on this precedent to build a robust and defensible analysis, ensuring your accelerated deductions are fully compliant. It’s how you turn a standard building into a finely tuned instrument for tax efficiency.

Unlocking Your Property's Hidden Value with Depreciation

At its heart, a cost segregation study is all about timing. It’s a powerful tax strategy that lets you pull future deductions into the present day, creating significant, immediate savings. This is driven by a concept called accelerated depreciation, which gets a massive boost from current tax laws like bonus depreciation.

Think of it this way: without a study, the IRS sees your commercial building as one giant block depreciating slowly over 39 years. It's a predictable, but frustratingly slow, drip of tax benefits. A cost segregation study, on the other hand, meticulously breaks that block apart, identifying components that can be written off much faster—over 5, 7, or 15 years. You're essentially shifting your deductions from the slow lane to the fast lane.

A Tale of Two Timelines: Standard vs. Accelerated Depreciation

Let's put some real numbers on this. Imagine you've just acquired a commercial property for $1.2 million. After backing out the land value, the building itself is worth $1 million.

Before the Study (Straight-Line): The standard approach gives you an annual depreciation deduction of just $25,641 ($1,000,000 divided by 39 years). It’s something, but it’s not going to make a huge dent in your tax bill.

After the Study (Accelerated): A detailed study might find that 25% of the building’s cost ($250,000) is actually personal property (carpeting, specialty lighting, etc.) with a 5 or 7-year life. The other 75% ($750,000) remains on the 39-year track. This one simple reclassification completely changes your tax picture.

This is the core of the strategy—claiming much larger deductions right away when they’re most valuable. To really get a feel for how this works, it’s worth reviewing the fundamentals of rental property depreciation. That groundwork makes the power of an engineered study crystal clear.

Supercharging Deductions with Bonus Depreciation

This is where things get really interesting. The tax code includes a provision called bonus depreciation, which allows investors to immediately write off a huge chunk of the cost for assets with a life of 20 years or less.

Bonus depreciation acts as a powerful multiplier for cost segregation. By reclassifying assets into 5, 7, and 15-year categories, you make them eligible for this immediate, first-year write-off.

While the 100% bonus depreciation from a few years ago is phasing down, it’s still an incredibly potent tool in 2026. You can still expense a significant percentage of all those short-life assets in year one, front-loading your tax savings and putting cash back in your pocket.

This combination is where you see the most dramatic results. For instance, on a property with a $500,000 depreciable basis, a study that reallocates just 20% ($100,000) to short-life assets can have a massive impact. One analysis by the tax experts at HCVT showed how a similar scenario could increase first-year deductions from a paltry $17,425 to over $113,940—a nearly 6.5x increase.

The end result is a monumental first-year deduction that can create a substantial "paper loss." This loss can then be used to shield other passive income from taxes, dramatically reducing your liability and freeing up cash flow. This is the engine room of the cost segregation strategy, turning a standard tax practice into a dynamic wealth-building opportunity for savvy investors.

Turning Tax Savings into Real-World Cash Flow

Tax deductions are nice on paper, but cash in the bank is what really matters. This is where a cost segregation study truly shines—it turns a theoretical tax benefit into actual cash you can use, fundamentally changing how you can operate your real estate portfolio.

Think of it like this: by speeding up your depreciation deductions, you're essentially getting an interest-free loan from the government. Instead of that capital being tied up for decades, it flows back to you in the first few years you own the property. This isn't just an accounting trick; it's a powerful tool for growth.

Putting Your Newfound Capital to Work

Once that cash is unlocked, your strategic options open up significantly. This isn't just about padding your reserves; it’s about having proactive capital ready to deploy for serious portfolio growth and greater financial stability.

Smart investors put this money to work in a few high-impact ways:

- Acquire More Properties: That cash can serve as the down payment on your next income-producing asset, letting you scale your portfolio far faster than you could otherwise.

- Pay Down High-Interest Debt: You can attack expensive debt on other properties or business ventures, which immediately improves profitability and lowers your financial risk.

- Fund Capital Improvements: Reinvesting in the property can boost its value, help you attract better tenants, and justify higher rents.

- Increase Investor Distributions: For family offices or partnerships, this often means rewarding stakeholders with larger, more frequent distributions.

When you strategically redeploy this capital, a tax tactic becomes a core engine for business growth. It's a key principle of effective cash flow management for real estate investors.

Case Study: Unlocking Over $1 Million in Liquidity

The scale of this cash flow benefit can be staggering. It’s not unusual for a single study on a mid-sized commercial property to free up a seven-figure sum in the first year alone.

In one real-world example, a cost segregation study on a $13.5 million retail shopping center resulted in an immediate, first-year tax savings of $1,168,876.

The return on investment for the study itself was an incredible 95.5 to 1. This isn't a minor tax tweak; it's a massive injection of liquidity that can fuel acquisitions, renovations, or major debt reduction.

The accelerated depreciation from a cost segregation study can dramatically improve your cash flow and returns. It highlights just how important it is to be accurately calculating your rental property's ROI to see the full financial picture. The numbers simply don't lie.

Ultimately, this immediate boost to your financial flexibility is the most powerful of the cost segregation study benefits. It’s about taking control of your capital and putting it to work today, not decades from now. That proactive approach is what separates savvy investors from the rest of the pack.

Advanced Strategies for Wealth and Estate Planning

Sure, the immediate cash flow from a cost segregation study is a nice perk. But its real power, especially for high-net-worth investors and family offices, goes much deeper. This isn't just a simple trick for your annual tax return; it's a sophisticated tool for long-term wealth management, smarter transactions, and multi-generational estate preservation.

When you start looking at cost segregation through this wider lens, you can find value at every stage of a property's life—from the day you buy it to the day you sell or pass it on. These advanced techniques can turn a one-off tax tactic into a cornerstone of a truly robust financial plan. It’s all about knowing when and how to pull the right levers.

The Power of the Look-Back Study

Did you miss the window to run a cost segregation study when you first bought a property? The good news is, you haven't lost out. The IRS allows for a "look-back" study, which is a powerful way to retroactively apply cost segregation to properties you've owned for years.

This isn't about the headache of amending old tax returns. Far from it. Instead, you get to capture all the missed depreciation from prior years and claim it all in a single year.

You do this by filing an IRS Form 3115, Application for Change in Accounting Method. The result is a massive, one-time "catch-up" deduction that can create a significant tax shield right now. This is a fantastic move for investors who've had a sudden spike in income and are looking for a way to offset a big tax bill.

Optimizing Transactions and Capital Gains

A cost segregation study also proves its worth when it's time to sell. When you sell a property, the depreciation you've claimed over the years is "recaptured" by the IRS and taxed. However, the upfront tax savings and the ability to reinvest that cash often far outweigh this future tax bill, thanks to the time value of money.

But here’s where it gets really strategic. You can use those large depreciation deductions to offset capital gains from selling other assets, making your entire portfolio more tax-efficient.

For example, say you sell a stock portfolio for a significant gain. A cost segregation study on a real estate asset in the same year could generate a paper loss big enough to absorb much of that gain, dramatically cutting your overall tax burden.

This approach is also incredibly effective when you're planning for a 1031 exchange. By getting a precise breakdown of the personal property components in your building, you can better structure the exchange. This helps ensure you're replacing "like-kind" real property while potentially managing the tax hit from any non-like-kind personal property assets separately.

Integrating with Estate Planning for Permanent Savings

Perhaps the most compelling advanced benefit is how cost segregation plays into estate planning. When an investor passes away, their heirs receive a "step-up" in basis on inherited assets, meaning the asset's cost basis is reset to its fair market value at the time of death. For a property that has already undergone cost segregation, this is a game-changer.

This step-up in basis effectively wipes out the future depreciation recapture tax liability. All the accelerated depreciation taken during the original owner's lifetime becomes a permanent tax savings for the estate. That deferred tax bill simply vanishes. You can learn more about how this fits into a broader strategy by exploring our guide to estate planning for wealthy individuals.

This move transforms the tax deferral from cost segregation into a permanent tax reduction. For high-net-worth families, it's an essential piece of the puzzle for multi-generational wealth preservation, ensuring the full financial advantage passes to the next generation.

Is a Cost Segregation Study Right for You?

The theory behind cost segregation is powerful, but how does it actually play out in a real-world portfolio? While the tax savings can be massive, it’s not a magic bullet for every property or every investor.

Deciding if a study makes sense comes down to a practical look at the numbers. For the right asset, it's a huge financial accelerator. For the wrong one, the costs can simply chip away at any potential gains. Let’s break down where it works best.

Who Are the Ideal Candidates?

A cost segregation study delivers the most bang for your buck when a large chunk of a property’s cost can be shifted from long-life real property to short-life personal property.

You’re likely a perfect candidate if you own:

- Newly constructed or acquired properties: Doing a study right out of the gate, in the year of purchase or construction, maximizes the time value of money. You get those accelerated deductions immediately.

- Properties with significant renovations: A major facelift or expansion is an ideal trigger. It gives you a clean opportunity to segregate all the new components you just paid for.

- Commercial or residential rentals valued over $750,000: While smaller properties can benefit, the ROI really starts to pop on higher-value assets. At this level, the tax savings can easily dwarf the study's fee.

- Specialized facilities: Think manufacturing plants, medical centers, or even data centers. These buildings are packed with process-related infrastructure—specialized electrical, plumbing, HVAC—making them prime targets for reclassification.

Understanding the Costs and Risks

Before you jump in, it's crucial to weigh the upfront investment against the return. The fee for a cost segregation study isn't one-size-fits-all. It’s going to depend on the property's size, complexity, and location. A straightforward warehouse will naturally cost less to analyze than a multi-story medical office filled with specialized equipment.

The main risk to have on your radar is depreciation recapture.

When you eventually sell a property that has benefited from cost segregation, the IRS "recaptures" the accelerated depreciation you claimed. The portion that was classified as personal property is usually taxed at ordinary income rates, which can be higher than long-term capital gains rates.

But this future tax bill is often a small price for the significant cash flow you unlocked years earlier. That immediate capital, if reinvested smartly, can generate returns that far outstrip the eventual tax cost. And, as we covered in the context of estate planning, this recapture can be wiped out entirely through a step-up in basis at death.

Ultimately, figuring out if a study is right for you boils down to a simple cost-benefit analysis. A qualified firm can run a preliminary analysis for you, projecting your potential first-year tax savings against the cost of the study itself. This gives you a clear, data-driven look at your projected ROI, ensuring the cost segregation study benefits align perfectly with your financial strategy.

Common Questions We Hear About Cost Segregation

Even after seeing the numbers, it's natural to have a few questions. We get them all the time from investors who are new to this strategy. Let's walk through some of the most frequent ones to clear up any confusion.

Can I Do This for a Property I Bought Years Ago?

Yes, and you absolutely should. This is one of the most powerful and common applications of cost segregation, often called a “look-back” study.

The IRS allows you to go back and capture all the depreciation you should have been taking since you bought the building. You don't have to amend old tax returns. Instead, you file a Form 3115, "Application for Change in Accounting Method," and take all those missed deductions in a single, massive "catch-up" deduction on this year's return. This can create a huge, immediate tax savings.

What Happens When I Go to Sell the Property?

This is a critical question. When you sell, the accelerated depreciation you took is subject to "recapture" by the IRS. The portion of your gains attributed to the reclassified personal property will likely be taxed at higher ordinary income rates, not the more favorable long-term capital gains rates.

But here's the trade-off you need to weigh: The significant tax deferral gave you cash in hand years earlier. That's money you could have reinvested, used to acquire other properties, or put to work generating its own returns. More often than not, the financial benefit of having that cash upfront far outweighs the tax bill down the road. It's all about the time value of money.

Will a Cost Segregation Study Trigger an IRS Audit?

A properly done study will not put a target on your back. Cost segregation is a well-established, IRS-accepted tax planning strategy that has been validated in court for decades. It’s not some gray-area loophole.

The key is who does the study. When you work with a reputable engineering firm that follows the IRS's own detailed guidelines, the report is your defense. A high-quality, engineering-based study provides all the necessary documentation to justify the asset reclassifications, making your tax position solid and defensible. Avoid cheap, "estimated" reports at all costs—that's where the risk lies.

Navigating the complexities of tax strategies like cost segregation is a critical component of sophisticated wealth management. At Commons Capital, we help high-net-worth individuals and families integrate these powerful tools into a cohesive financial plan. To explore how we can optimize your portfolio's tax efficiency, visit us at Commons Capital.