Effective cash flow management for small business isn't just about tracking money; it's the lifeline that determines your company's stability and growth potential. It’s not about the profit you see on a spreadsheet. It’s about having the actual cash in the bank to pay your bills, make payroll, and seize growth opportunities. Mastering this is the key to making confident financial decisions and achieving genuine stability.

Why Cash Flow Is Your Most Important Metric

Profit is a great number to look at, but it won't pay your rent. A positive cash flow is the ultimate measure of your business's health.

Picture this: You just had a record sales month. Your income statement looks fantastic. But when payroll is due, you're scrambling to cover it. It's a nightmare scenario that many business owners face, learning the hard way that being profitable and being cash-positive are two different things.

The culprit? Your clients haven't paid their invoices yet. So while you're technically successful, your bank account is empty.

That's the essence of cash flow management. It's the daily discipline of ensuring your cash inflows arrive before your outflow deadlines. When you get this right, you stop reacting to financial fires and start proactively building a stronger business. You can finally:

- Reduce Financial Stress. Knowing you can cover rent, supplier invoices, and other operating expenses on time, every single time, is a huge weight off your shoulders.

- Seize Opportunities. A great deal on new equipment? The perfect person to hire? A solid cash position means you can say "yes" without hesitation.

- Plan Strategically. A clear view of your cash flow lets you think strategically about the future, whether that means expanding your operations or building a rock-solid business exit strategy.

This isn't an abstract concept; it's a real, persistent challenge. According to recent research from OnDeck, 29% of small businesses rank cash flow management as their second-biggest challenge, right behind inflation at 31%. This statistic highlights just how common this pain point is for entrepreneurs.

The goal is to shift from just surviving to truly thriving. When you control your cash, you control your company's destiny. You turn financial anxiety into a genuine competitive edge.

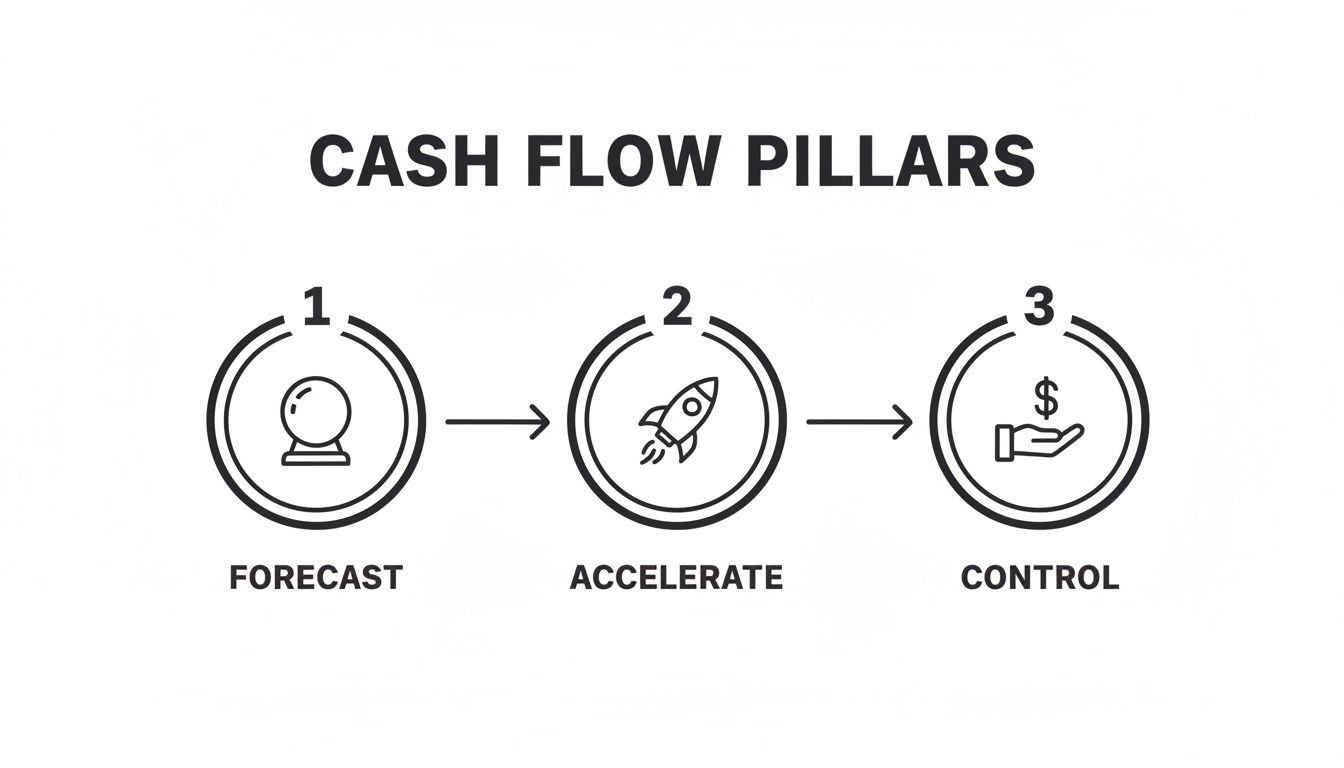

This guide is your complete playbook for achieving that control. We'll explore the three pillars of effective cash management: forecasting your needs, accelerating payments, and controlling your spending. Master these, and you'll build a financial foundation that supports real, sustainable growth.

Creating a Cash Flow Forecast You Can Actually Use

A cash flow forecast shouldn't be a complex spreadsheet you create once and forget. Think of it as your business's financial GPS—a living tool that shows where you are, where you're headed, and what financial potholes lie ahead. This is where truly effective cash flow management for small business begins.

Operating without a forecast is like flying blind. A rolling 13-week cash flow forecast is one of the most powerful tools in your arsenal, providing a clear, forward-looking map of your cash position for the next quarter. This allows you to make decisions proactively instead of constantly reacting to financial emergencies.

The process boils down to three core pillars: forecasting what you'll need, accelerating the cash coming in, and controlling the cash going out.

This simple flow emphasizes a critical point: forecasting is the foundational step that informs every other action you take to maintain financial stability.

The Direct Method: A Practical Example

For most small businesses, the direct method is the most straightforward and intuitive approach. It’s simple: you list all your anticipated cash inflows (money coming in) and all your expected cash outflows (money going out) over a set period.

Let's walk through an example. Imagine a small consulting firm building its first 13-week forecast.

First, they'd map out every single source of expected cash. This isn't your sales pipeline; it’s about when the actual dollars will hit your bank account.

- Invoice Payments: They’d list every outstanding invoice, noting the client and the most realistic date they expect to be paid. If you know Client A always pays 15 days late, that's what you put in the forecast.

- New Sales: For new projects, they’d estimate the closing date and when the initial deposit will land.

- Other Income: This is a catch-all for things like a tax refund, a loan disbursement, or maybe the sale of an old piece of equipment.

Brutal honesty is your best friend here. It's tempting to be optimistic about sales projections, but a useful forecast is built on realistic data, not wishful thinking. Your own past performance is the best guide.

Next, they’d plot out every single dollar they expect to spend. Precision is key, as small "cash leaks" can add up quickly and drain your resources.

- Fixed Expenses: These are the predictable costs—rent, software subscriptions, insurance premiums, and loan payments.

- Variable Expenses: This bucket includes payroll (which might change with commissions or hours), supplier invoices, marketing spend, and travel costs.

- One-Time Costs: Planning to buy new laptops in week eight? That goes into the forecast.

For your forecast to be effective, learning how to improve forecast accuracy is non-negotiable. This involves refining your predictions over time by comparing them to actual results.

Choosing Your Forecasting Method

Deciding between the direct and indirect methods often comes down to your business's complexity and your goals. Here’s a quick breakdown to help you choose the right fit.

For the vast majority of small business owners, the direct method is the clear winner for practical, operational planning. It's actionable and directly tied to the real-world flow of money in your business.

Make Your Forecast a Living Document

The biggest mistake business owners make is treating their forecast like a static report. The market shifts, clients pay late, and unexpected expenses always pop up. Your forecast is only valuable if it reflects today's reality.

This means you must dedicate time each week—perhaps every Monday morning—to update it. Sit down and compare the previous week's projections to what actually happened.

- Did a client pay earlier than you thought? Update the inflow.

- Did that supplier bill come in higher than expected? Adjust the outflow.

- Did you close a new deal? Add that projected deposit to the right week.

This weekly discipline transforms your forecast from a historical document into a powerful decision-making tool. If you see a potential cash shortfall coming in week five, you now have four weeks to do something about it. You can push harder on collections, delay a non-essential purchase, or look into short-term financing. That proactive stance is the very heart of great cash flow management.

Actionable Strategies to Get Paid Faster

Waiting on invoices is one of the biggest cash flow killers for any business owner. Improving your accounts receivable (AR) process is a direct lever you can pull to dramatically shorten your cash conversion cycle. It’s about rethinking the entire payment experience to make it fast, easy, and beneficial for your clients to pay you on time.

Persistent cash flow pains often stem from these operational gaps. Research shows that small business owners frequently grapple with managing unexpected expenses (42%), dealing with late customer payments (35%), and navigating seasonal business swings (29%). Proactive AR management is your first line of defense against these common risks.

Rethink Your Invoicing and Payment Terms

The best time to ensure prompt payment is before you even start the work. Your contracts and invoicing process are powerful tools for setting cash flow expectations from the beginning.

Structure your agreements to get cash in the door upfront. Instead of waiting until a project is 100% finished to send a single invoice, try these approaches:

- Require Upfront Deposits: For any new client or significant project, it’s smart to require a deposit of 30-50% before work begins. This immediately gives you working capital and confirms the client is serious.

- Implement Milestone Payments: Break down larger, long-term projects into distinct phases. As each milestone is completed, you send an invoice. This creates a steady, predictable stream of cash throughout the project.

Next, you can actively incentivize the behavior you want to see. One of the most effective tactics is offering a small discount for paying early.

The classic "2/10, net 30" model is a perfect example. You give your client a 2% discount if they pay within 10 days; otherwise, the full amount is due in 30 days. This small incentive can work wonders for accelerating your cash inflows, especially on larger invoices where the savings are meaningful for your client.

Make Paying You Effortless

Every bit of friction in your payment process is another reason for a client to delay. If a client has to find a checkbook, an envelope, and a stamp to pay you, you’ve already lost. Your goal is to make paying an invoice as easy as a one-click purchase on Amazon.

This means offering a variety of modern payment options. Modern accounting software and payment processors make it incredibly simple to accept:

- ACH Bank Transfers: These are often low-cost or even free, providing a convenient way for businesses to pay directly from their bank accounts.

- Credit Cards: Sure, there’s a processing fee (typically 2.9% + $0.30), but the convenience is often worth it. Many clients prefer using credit cards to earn rewards points and manage their own cash flow.

When you provide multiple, easy-to-use options right on the digital invoice, you remove common roadblocks and shrink the time it takes for money to land in your account.

A Real-World Example in Action

Let’s look at a marketing agency that was constantly fighting a slow collections cycle. Their average collection period was 45 days, which put a constant strain on their ability to pay their own vendors and freelancers on time.

They decided to completely overhaul their process. Here’s what they did:

- Contract Changes: They updated their standard agreement to require a 50% deposit on all new projects.

- Payment Options: They integrated their accounting software with a payment processor, letting clients pay invoices directly via ACH or credit card with a single click.

- Incentives: They rolled out a “2/10, net 30” discount for paying early.

- Automated Follow-ups: They configured automated reminders to go out a few days before an invoice was due, on the due date, and then at regular intervals if it became overdue.

The results were stunning. Within just six months, their average collection period plummeted from 45 days to just 18 days. This massive improvement in their cash conversion cycle gave them the stability to hire new talent and expand their services.

Implementing systems that encourage timely payments can be a game-changer. You might even consider leveraging tools like automated payment reminders to improve cash flow to make the process even smoother.

Smart Ways to Manage Expenses and Working Capital

Bringing cash in the door is only half the battle. Controlling what goes out—and when—is just as crucial for a healthy business. This is the defensive side of cash flow management, and it’s all about making sure every dollar you have is working for you.

The goal isn’t to slash costs indiscriminately. It's about being strategic. It’s about making deliberate choices with your money, starting with the day-to-day fuel your business runs on: working capital. Think of it as the cash you have on hand to cover all your short-term operational needs.

Conduct a Simple Expense Audit

You can't fix what you can't see. The first move is to find the "cash leaks"—those sneaky, recurring costs that silently drain your bank account month after month.

Pull up your last three to six months of bank and credit card statements and start categorizing everything. You’re looking for patterns, specifically:

- Subscription Creep: Are you still paying for software you haven’t logged into for months? Those $20/month subscriptions add up to real money.

- Redundant Services: It's surprisingly common to find businesses paying for multiple tools that do the exact same thing.

- "Miscellaneous" Spending: This category is often a black hole for impulse buys and unclassified waste. Dig into it.

Once you have a clear picture, start asking hard questions. Is this expense absolutely essential to generating revenue? Is there a more cost-effective alternative?

This is about being intentional, not cheap. I worked with a small agency that found they were spending over $800 a month on three different project management tools. They consolidated to a single platform, saving nearly $10,000 a year without missing a beat.

Strategic Accounts Payable Management

How you handle your accounts payable (AP) can be a powerful lever for your cash position. Yes, paying your bills on time is non-negotiable for maintaining good vendor relationships. But paying them too early can put an unnecessary strain on your cash reserves.

Instead of paying invoices the second they arrive, get more strategic.

- Negotiate Longer Payment Terms: Don't just accept the standard "net 30" terms from a new supplier. Ask for "net 45" or even "net 60." Many vendors are surprisingly flexible, especially if you can offer them consistent business.

- Align Payments with Cash Inflows: Look at your cash flow forecast. When do your biggest client payments typically hit your account? Schedule your major bill payments to go out right after those deposits land, so you're never paying bills when your account is at its lowest.

This isn’t about being a late payer. It’s about using the agreed-upon payment window to your full advantage to maintain maximum liquidity. For a deeper dive, check out our guide to professional cash management services.

Keep Your Inventory Lean

For any business that sells a physical product, inventory is one of the biggest cash traps. Every unsold item sitting on a shelf is cash you can't use for payroll, marketing, or rent.

Adopting a just-in-time (JIT) inventory strategy—where you order products as close as possible to when you need them—can be a game-changer. While not suitable for every business, the core principle of keeping inventory lean is universal.

Dive into your sales data regularly to spot your slow-moving products. Don't be afraid to run a sale or a promotion to liquidate that dead stock and turn it back into cash. You can then reinvest that money into products that sell quickly, creating a much more efficient and profitable cycle.

How to Build a Financial Safety Net for Your Business

A healthy cash reserve is your business’s ultimate insurance policy. It's the financial cushion that provides peace of mind, knowing you can handle a sudden emergency, a slow season, or even a golden opportunity without panicking. Building this safety net is a core discipline of smart cash flow management for small business.

This isn't just a "nice-to-have." The reality for many small businesses is stark. One study found that a staggering 39% of them have less than a month of cash on hand to cover their expenses. It’s even more precarious for new companies—20.7% of businesses under two years old reported having less than seven days of cash in their accounts. These numbers make a dedicated reserve strategy non-negotiable. You can read more about these trends over on Bluevine.com.

Set a Clear Savings Goal

So, where do you start? The industry standard is a powerful benchmark: aim to have three to six months of essential operating expenses saved.

To be clear—this isn't your total revenue. This is the bare-bones, keep-the-lights-on number. We're talking about the essentials:

- Rent or mortgage

- Payroll

- Key software subscriptions

- Utilities

- Any other bill you absolutely have to pay to stay in business

Calculating your target is straightforward. Add up all those essential monthly costs to get your one-month survival number. Then, multiply that total by three for your minimum goal and by six for your ideal safety net. This turns a vague idea like "save more money" into a concrete, measurable objective.

Automate Your Savings Habit

The single most effective way to build your cash reserve is to make it automatic. If you rely on willpower to move whatever is "left over" at the end of the month, it won't happen consistently.

Instead, treat your savings contribution like any other non-negotiable operating expense.

Set up an automated weekly or bi-weekly transfer from your main business checking account into a separate, dedicated high-yield savings account. It doesn't have to be a huge amount. Even a small, consistent transfer of 1-2% of your revenue adds up significantly over time.

By automating the process, you take emotion and effort out of the equation. Your buffer builds itself in the background. This is a foundational piece of any solid financial plan. For a deeper dive into how this fits with your personal wealth strategy, check out our guide on business owner financial planning.

Turn Your Safety Net into a Competitive Advantage

While we usually think of a cash reserve as a defensive tool, a strong cash position can quickly become a powerful offensive weapon.

When the economy gets shaky or the market takes a downturn, many of your competitors will be forced to pull back. They'll be cutting costs, laying people off, and operating from a place of fear.

With a solid cash buffer, you have options they don't. This financial stability allows you to:

- Negotiate better deals with suppliers who might need quick cash payments.

- Invest in marketing when ad costs are lower and your competitors go silent.

- Hire top talent as other companies are forced into layoffs.

- Purchase assets or inventory at a serious discount from distressed sellers.

When you methodically build your financial safety net, you're doing more than just protecting your business from the downside. You're strategically positioning it to turn market volatility into your greatest opportunity.

A Few Final Questions on Cash Flow

Even with the best playbook, questions are natural. Here are a few of the most common ones I get from business owners, along with straightforward answers to help you stay on track.

What Is The Difference Between Profit And Cash Flow?

This is the most critical concept to master in business finance. Profit is what's left after you subtract all business expenses from your total revenue. It’s found on your income statement and is a great barometer for your business model's long-term health.

Cash flow, on the other hand, is the actual money moving into and out of your bank accounts. You can be wildly profitable on paper but still face a massive cash crunch if your clients are slow to pay.

Think of it this way: profit is how you keep score, but cash flow is the fuel that keeps your business running day-to-day. Without it, the engine seizes up.

How Often Should I Be Checking My Cash Flow?

The key here is building a rhythm. For most small businesses, a quick check-in once a week is perfect. This isn't about deep analysis; it's about taking a quick pulse to spot small problems—like a late client payment—before they become emergencies.

Then, you need to go deeper at least once a month. This is where you pull up your cash flow forecast and compare it to what actually happened.

This monthly review is vital for two reasons:

- It sharpens your aim. The more you compare your projections to reality, the better you get at making realistic forecasts.

- It informs your next move. This is the hard data you need to make smarter decisions on big-ticket items like hiring, expanding, or making a significant equipment purchase.

What Should I Do First In A Cash Flow Emergency?

If you find yourself staring at a cash shortfall, the first few hours are crucial. You need to act fast and with a clear head.

First, pick up the phone. Start calling every single client with an outstanding invoice. A real conversation is almost always more effective than another automated email.

Next, get proactive with your own payables. Call your key suppliers—before a payment is late—and ask for a short extension. You’d be surprised how understanding most vendors are when you communicate openly and honestly.

At the same time, hit the pause button on all non-essential spending. Delay any purchase that isn't absolutely critical to keeping the lights on. As a final step, look into short-term financing like a business line of credit or invoice financing to bridge the gap.

Is Accounting Software Worth It For Cash Flow Management?

One hundred percent, yes. It's one of the best investments you can make. Modern accounting platforms like QuickBooks or Xero do more than just bookkeeping; they give you a real-time dashboard of your company's financial health.

These tools offer significant benefits:

- Live Data: They sync directly with your bank accounts, so you always have an up-to-the-minute view of your cash position.

- Smarter Invoicing: You can send professional invoices in minutes and set up automated reminders to chase late payments.

- Effortless Reporting: Need a cash flow statement or a P&L? It’s usually just a couple of clicks away.

This isn't just about saving time. It's about shifting from reacting to old numbers to proactively managing your money based on what's happening right now. That clarity is the foundation of solid cash flow management for small business.

Mastering your cash flow is the key to unlocking sustainable growth and financial peace of mind. At Commons Capital, we specialize in helping successful business owners navigate complex financial situations, aligning their business success with their personal wealth goals.

If you’re ready to build a comprehensive financial strategy that goes beyond the day-to-day, let's talk. Learn more about our private wealth management services.