When you've built significant wealth, estate planning for wealthy individuals goes far beyond drafting a simple will. It becomes a strategic process designed to protect your assets, minimize tax liabilities, and ensure the legacy you envision is realized. Unlike a standard plan focused on basic distribution, a high-net-worth strategy must manage complex financial structures, anticipate legal challenges, and navigate delicate family dynamics.

Why Standard Estate Plans Fall Short for High-Net-Worth Families

For high-net-worth families, relying on a generic will is like trying to navigate a bustling city with a crumpled paper map. While it might show the main streets, it misses the critical, real-time data needed to avoid tax gridlock, legal disputes, or the faster routes offered by strategic trusts. A sophisticated plan is your GPS, constantly updating to find the most efficient path for your wealth.

The goals themselves are worlds apart. A standard plan might focus on distributing personal property and a family home. In contrast, estate planning for wealthy individuals involves orchestrating business successions, managing massive investment portfolios, handling diverse real estate holdings, and fulfilling philanthropic ambitions—all while navigating a dense web of tax laws.

A Tale of Two Plans

The difference in complexity is stark. A typical plan might involve a simple will and naming beneficiaries on a 401(k). For a high-net-worth individual, the toolkit is far more extensive and must be custom-fitted to their unique circumstances.

This usually brings a whole different set of tools into play:

- Advanced Trusts: Think Irrevocable Life Insurance Trusts (ILITs), Grantor Retained Annuity Trusts (GRATs), or even Dynasty Trusts. These are powerful vehicles designed to shield assets from estate taxes and creditors.

- Business Succession Plans: You need a seamless transition plan for the family business, whether that means passing it to the next generation or preparing for a sale without tanking its value or disrupting operations.

- Philanthropic Vehicles: Structuring your charitable giving is key. Using Donor-Advised Funds (DAFs) or private foundations allows you to maximize your impact while also realizing significant tax benefits.

- Asset Protection Strategies: It's about legally structuring your assets today to insulate them from potential lawsuits or unforeseen liabilities down the road.

This level of detail is non-negotiable given the scale of wealth involved. The global wealth management industry is booming to meet these exact needs. By 2025, global Assets under Management (AuM) are projected to hit $145.4 trillion, a massive jump from $84.9 trillion in 2016. This growth highlights just how complex and important specialized wealth preservation has become. You can dive deeper into these global wealth trends and their impact on financial planning.

Using a basic will for a multi-million-dollar estate is like bringing a rowboat to cross an ocean. It might work for a small pond, but it's completely inadequate for the journey ahead. The right tools are essential for navigating the turbulent waters of tax law and wealth preservation.

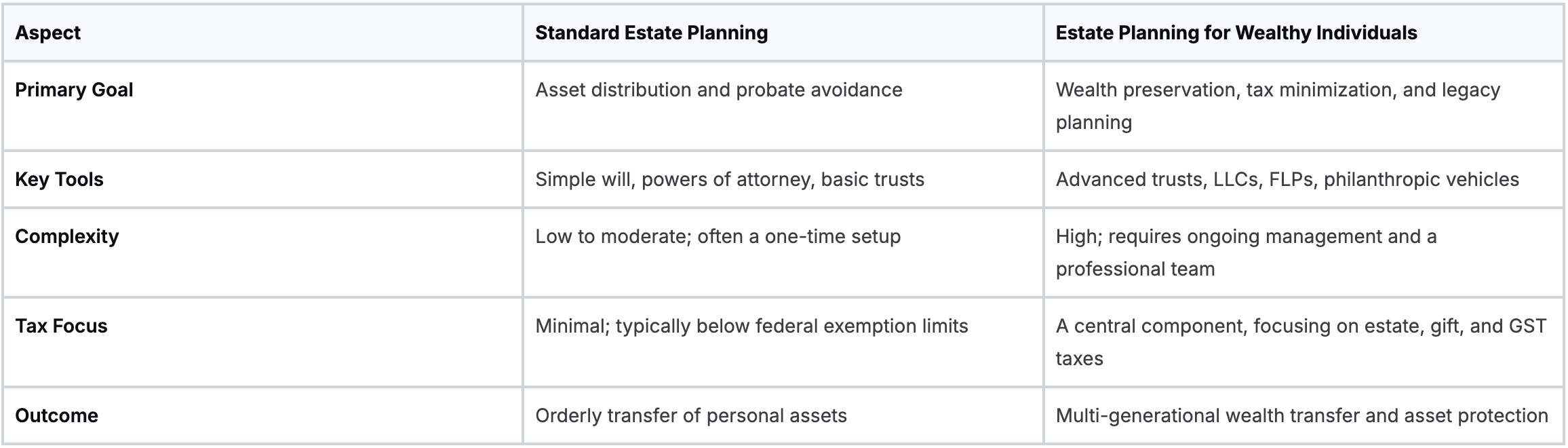

To really bring these differences into focus, let’s lay it out side-by-side.

Standard vs High-Net-Worth Estate Planning at a Glance

A quick comparison shows just how different the approach needs to be when significant wealth is on the line. The goals, tools, and overall complexity are simply in different leagues.

Ultimately, a standard plan fails because it’s reactive, not proactive. It addresses what happens after death but does little to preserve the wealth itself. For affluent families, the mindset must shift from simple distribution to strategic, long-term stewardship.

Core Pillars of Advanced Estate Planning

When you're building a truly effective estate plan, especially with significant wealth on the line, it all comes down to a few foundational pillars. Trusts are, without a doubt, the most critical.

Think of your estate like a valuable collection you’ve spent a lifetime building. A simple will is like leaving a note with instructions—helpful, but basic. Trusts, on the other hand, are like secure, specialized containers designed to protect and manage specific assets according to a very precise set of rules you create. Getting to know these core tools is the first step toward building a plan that actually holds up.

At the heart of it all are two main types of trusts: Revocable and Irrevocable. Each serves a completely different purpose, and they are the essential building blocks for hitting key goals like avoiding probate, maximizing tax efficiency, and ensuring your assets are distributed exactly as you intend for generations to come.

The Revocable Living Trust: A Personal Vault

A Revocable Living Trust is easiest to picture as a personal vault that you own and control completely. You can put assets into it, take them out, and change the rules whenever you want during your lifetime. Its main job is to hold the title to your assets, which allows them to pass directly to your heirs without getting bogged down in the public, expensive, and often lengthy probate process.

But here’s the catch: because you keep full control, the IRS and the courts still see those assets as yours. This means a revocable trust offers no protection from estate taxes or creditors. It’s a fantastic tool for privacy and efficiency, but it’s not designed for advanced tax planning or asset protection.

A Revocable Trust simplifies passing assets to your beneficiaries, making the whole process smoother and more private. For high-net-worth families, it's a foundational piece, but it's almost always just the starting point of a much bigger strategy.

The Irrevocable Trust: A Fortified Strongbox

An Irrevocable Trust, as the name implies, is a different beast entirely. Think of it as a fortified strongbox that, once locked, generally stays locked. When you transfer assets into it, you can’t simply take them back or change the terms on a whim.

By giving up that control, you legally remove those assets from your personal estate. This is a powerful move, and it comes with some major benefits for wealthy families.

This legal separation is precisely what makes irrevocable trusts the cornerstone of advanced estate planning. They are built to do the heavy lifting that a revocable trust simply can't.

Here are the key advantages:

- Estate Tax Reduction: Because the assets are no longer legally yours, they can grow and pass to your heirs without being hit by federal estate taxes, which can be as high as 40% on amounts over the exemption limit.

- Asset Protection: Assets held inside a properly structured irrevocable trust are generally shielded from future creditors, lawsuits, and other financial claims made against you personally.

- Legacy Control: You can set very specific rules for how and when beneficiaries get their distributions. This ensures the wealth is used for what matters to you—like education, healthcare, or other specific goals—across multiple generations.

For a deeper look at how these different trust structures work in practice, you can learn more about comprehensive trust and estate planning services.

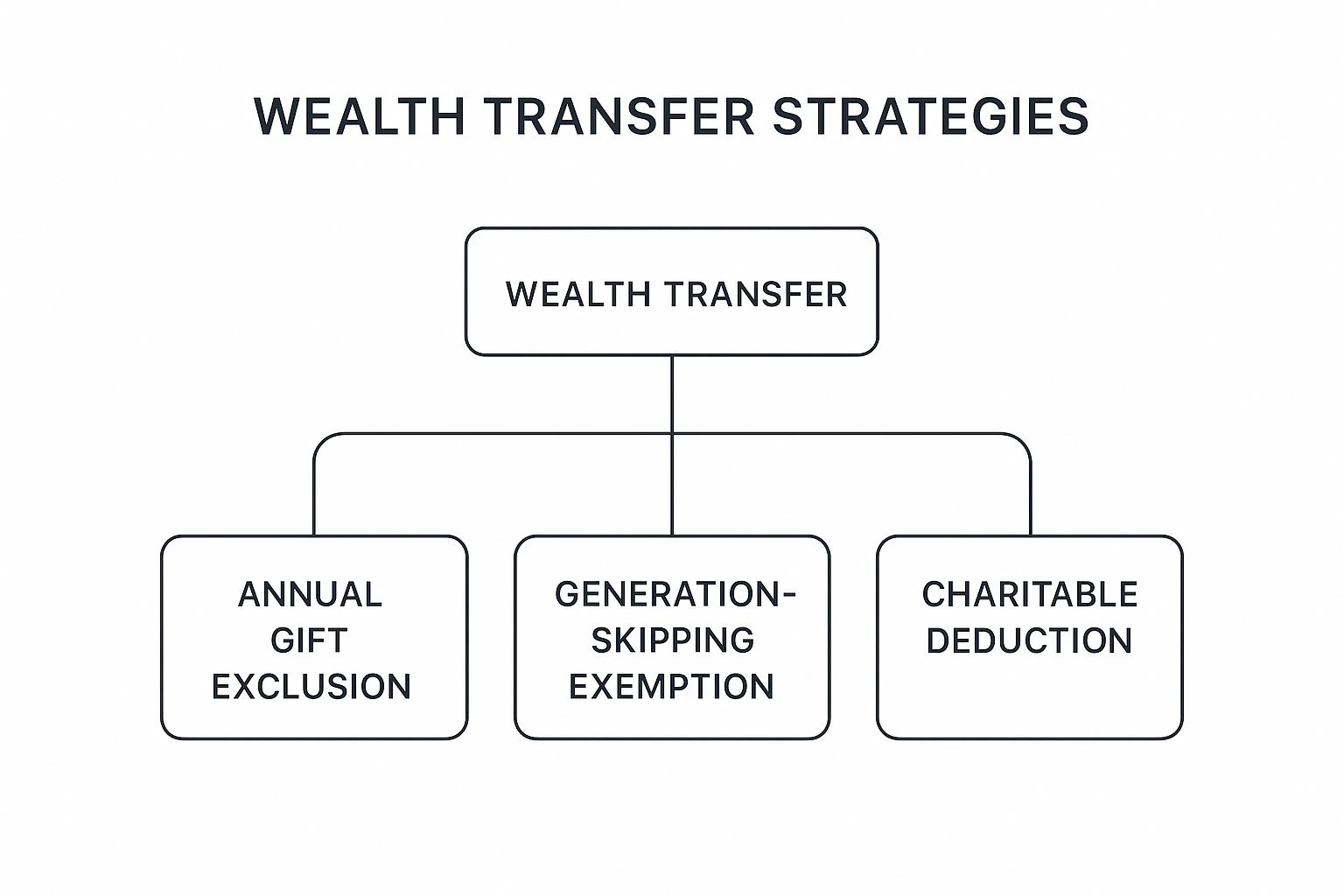

The diagram below shows a few of the key strategies high-net-worth individuals use to transfer wealth as efficiently as possible.

As you can see, things like annual gifting, generation-skipping planning, and charitable deductions aren't isolated tactics. They are distinct but complementary pathways that work together to minimize your overall tax exposure.

Interlocking the Pillars for a Cohesive Strategy

The real power of estate planning for wealthy individuals isn't just using one of these tools; it's about weaving them together into a single, cohesive strategy.

For instance, a business owner might put their primary home and personal investments into a Revocable Living Trust for simple day-to-day management and to keep them out of probate court.

At the same time, they could set up an Irrevocable Life Insurance Trust (ILIT) to hold a large life insurance policy, which keeps the massive payout from becoming part of their taxable estate. They might also use a Grantor Retained Annuity Trust (GRAT) to pass appreciating business stock to their children while using up very little of their gift tax exemption.

Each pillar supports the others, creating a multi-layered defense that preserves wealth, slashes taxes, and secures a legacy that lasts.

Mastering Tax Minimization Strategies

When it comes to estate planning for wealthy individuals, the name of the game is wealth preservation. And nothing eats away at wealth faster than taxes. For any sizable estate, the federal government is waiting to take a significant cut through estate, gift, and generation-skipping transfer (GST) taxes. Getting a handle on these is the first step toward keeping more of your assets where you want them.

Think about it: the federal estate tax alone can claim up to 40% of an estate’s value above the exemption limit. That limit is generous right now—$13.61 million per person in 2024—but it’s set to be slashed in half at the end of 2025. That ticking clock makes smart, proactive tax planning non-negotiable.

This isn't about finding shady loopholes. It's about using well-established, legal tools to transfer your wealth as efficiently as possible, ensuring more of it ends up with your family and the causes you believe in.

Proactive Gifting and Advanced Trusts

One of the most straightforward ways to shrink your future estate tax bill is to give assets away during your lifetime. As of 2024, you can give up to $18,000 to as many people as you want each year without touching your lifetime gift tax exemption. A married couple with three kids and their spouses could transfer $216,000 annually, tax-free. Over a decade, that’s over $2 million moved out of their taxable estate.

But when you're dealing with larger assets, especially ones you expect to grow in value, you need more sophisticated tools. That's where irrevocable trusts really shine.

- Grantor Retained Annuity Trust (GRAT): This is a fantastic tool for transferring appreciating assets like company stock. You put the assets into the trust and, in return, receive a fixed annuity payment for a set number of years. Any growth that occurs above a specific IRS interest rate passes to your beneficiaries completely tax-free.

- Family Limited Partnership (FLP): An FLP lets you pool family assets—like a business or real estate portfolio—into one entity. You can then gift minority shares to family members. Because these shares lack control and are not easily sold, they can often be valued at a discount, letting you transfer significant wealth out of your estate while you maintain management control.

These strategies aren't set-it-and-forget-it; they demand precise timing and expert execution. You can learn more by exploring our guide on 3 ways to minimize your tax liability.

Leveraging Spousal Benefits

For married couples, another powerful tool is spousal portability. This provision lets a surviving spouse use any of their deceased spouse's unused federal estate tax exemption. If one spouse passes away without using their full $13.61 million exemption, the leftover amount can be added to the surviving spouse’s exemption. This effectively doubles their potential exemption to a massive $27.22 million.

But relying on portability alone can be a mistake. It doesn't apply to the GST tax and offers none of the asset protection or control that a well-designed trust does. Think of it as a valuable safety net, not a substitute for a comprehensive plan.

Timing is everything in tax-efficient estate planning. The strategies that are most effective, like GRATs and lifetime gifting, deliver the greatest benefits when implemented years before they are needed, allowing assets to grow outside of your taxable estate.

Ultimately, mastering tax minimization is about getting ahead of the curve. By combining annual gifting, advanced trusts, and the smart use of spousal provisions, you can build a powerful defense against taxes. This is how you ensure the wealth you’ve built is preserved for generations, securing a legacy for the people and causes that matter most.

Protecting Assets from Creditors and Litigants

Think of your wealth as a fortress. While a simple will might act as the front gate, real security in estate planning for wealthy individuals demands a much more sophisticated defense system—complete with moats, high walls, and even a few secret passages. Building these protections isn't about waiting for a threat to appear on the horizon. It's about proactively constructing a legal stronghold that can stand up to future claims from creditors, litigants, and other unexpected challenges.

The most effective strategies are always put in place long before a storm gathers. If you wait until a lawsuit is filed to start moving assets, it’s usually too late. Courts can easily view those last-minute transfers as fraudulent. The real goal is to legally and ethically separate your personal wealth from potential risks, creating barriers that make your assets an unattractive, costly, and difficult target for anyone to pursue.

Building Your Financial Fortress

The whole strategy boils down to using specific legal entities to hold title to your assets. Instead of owning everything in your personal name—which is like leaving the castle gates wide open—you place assets into structures specifically designed to shield them. This creates a clean, clear separation between you, the individual, and your wealth.

Some of the key defensive layers you might build into your fortress include:

- Limited Liability Companies (LLCs): Often the vehicle of choice for real estate or business interests. An LLC creates a corporate veil, meaning if a lawsuit targets the LLC, the claim is typically confined to the assets within that specific company, protecting the rest of your personal wealth.

- Family Limited Partnerships (FLPs): Working much like LLCs, FLPs are fantastic for consolidating and managing family assets. You can gift limited partnership interests to family members to transfer wealth over time, while you maintain control as the general partner—all while adding a powerful layer of creditor protection.

- Irrevocable Trusts: As we covered earlier, these are the high stone walls of your fortress. When you transfer assets into a properly structured irrevocable trust, you legally give up ownership. From that point on, those assets are generally shielded from your personal creditors and any legal judgments against you.

This kind of proactive structuring is more critical than ever. Global wealth recently hit an unprecedented $471 trillion at the end of 2024, with huge growth coming from markets like the U.S. and China. While strong equity markets are driving this expansion, they also bring new complexities and potential liabilities, making robust asset protection an absolute must. You can learn more about these trends from BCG's 2025 Global Wealth Report.

Asset protection is not about hiding wealth; it's about intelligently structuring it. The strongest plans make it so difficult and costly for a potential litigant to pursue your assets that they often decide it's not worth the effort.

Domestic vs. Offshore Trusts

For the highest level of security, some clients look beyond domestic options to offshore asset protection trusts. These are set up in jurisdictions with ironclad privacy laws and legal systems that are incredibly favorable to debtors—places like the Cook Islands or Nevis are common choices.

If a domestic trust is a strong wall around your castle, an offshore trust is like moving your most valuable treasures to a separate, heavily guarded fortress on a remote island. It introduces significant legal and geographical hurdles that a creditor has to overcome. While they are certainly more complex and costly to establish, they offer a level of protection that’s nearly impossible to replicate within the U.S. legal system. Deciding between a domestic and an offshore strategy really comes down to your specific risk profile, the types of assets you hold, and your ultimate long-term goals.

Structuring Your Philanthropic Legacy

For many families, estate planning goes beyond simply passing wealth to the next generation. It’s about leaving a mark—a desire to create a lasting, positive impact on the world. This is where strategic philanthropy becomes a core component of estate planning for wealthy individuals, offering both a deep sense of purpose and some pretty significant tax advantages.

But integrating charitable giving into your plan isn't as simple as writing a check. It’s about choosing the right vehicle to maximize your impact, get your family involved, and build a legacy that truly reflects your values. The right structure is what makes your contributions both meaningful and incredibly efficient.

Choosing Your Charitable Vehicle

When you're looking at substantial philanthropic goals, three main options tend to rise to the top: Donor-Advised Funds (DAFs), private foundations, and Charitable Remainder Trusts (CRTs). Each works differently, and the best fit really hinges on your personal goals for control, family involvement, and timing.

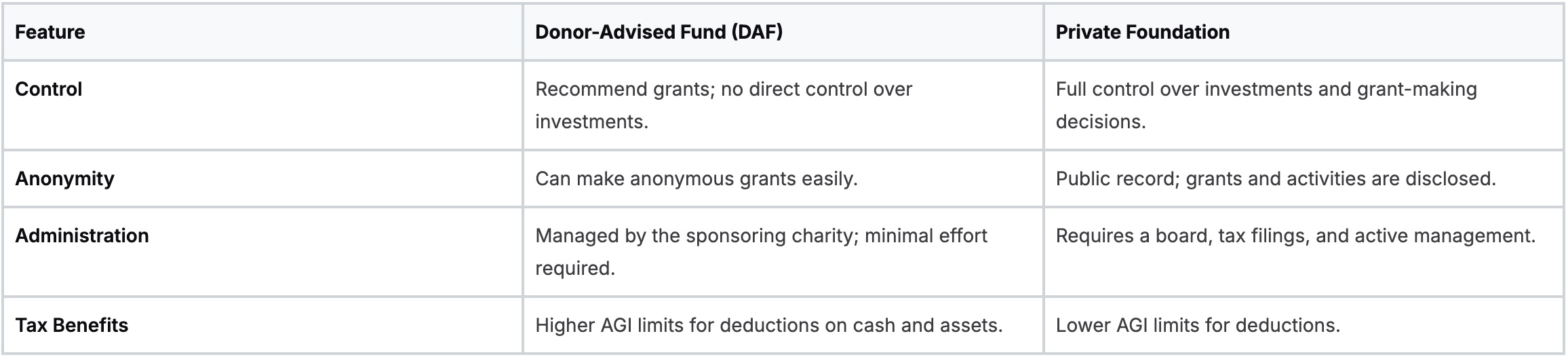

Think of a Donor-Advised Fund (DAF) as your own personal charitable investment account. You make a contribution to a public charity that sponsors the DAF, get an immediate tax deduction, and then you can recommend grants to your favorite causes whenever you like. It's straightforward, private, and takes very little administrative effort on your part.

A private foundation, on the other hand, is like launching your own family-run charitable enterprise. It gives you the ultimate control, letting your family manage the investments, set up formal grant-making processes, and even build a public presence around your mission. That control, however, comes with higher setup costs, more stringent regulations, and a good deal of ongoing administrative work. For families ready to take this hands-on approach, our guidance on family office services can be invaluable in navigating the complexities.

Choosing a philanthropic vehicle is about aligning the structure with your vision. Do you want the simplicity of an investment account or the hands-on engagement of running a family enterprise? The answer determines your path.

Comparing Your Philanthropic Options

Before you commit, it’s crucial to understand the key differences in how these vehicles are governed, set up, and treated from a tax perspective. A quick side-by-side comparison can make it much clearer which one aligns with your family’s style.

Then there's the Charitable Remainder Trust (CRT), which offers a unique hybrid approach. You transfer assets into the trust, and in return, it pays you (or other beneficiaries) an income stream for a set period. Once that term is up, whatever is left in the trust goes to the charity you designated.

This is a powerful tool, especially for generating income from appreciated assets like real estate or stock without having to pay immediate capital gains tax. For instance, a family could place highly appreciated stock into a CRT, receive a steady income for 20 years to support their lifestyle, and then have the remainder establish a university scholarship in their name. It’s a brilliant way to achieve multiple financial and philanthropic goals all at once.

Building Your A-Team and Implementing the Plan

Even the most brilliant estate plan is just a blueprint. Without a skilled team to build it and keep it standing, it’s not much more than an expensive piece of paper. Assembling the right group of professionals is the step that turns your strategy from an idea into a living, breathing structure that works for you and your family.

This isn't a one-person job. Proper estate planning for wealthy individuals absolutely requires a team of specialists working in sync. Think of it as assembling a personal board of directors for your legacy, where each member brings a critical perspective to the table.

Your Core Advisory Team

Your A-team will typically have a few key players, each working together to protect and grow your wealth exactly how you’ve envisioned.

- The Estate Planning Attorney: This is your plan’s architect. They’re the ones who draft the foundational legal documents—like wills and trusts—and make sure every part of the structure is legally sound and perfectly aligned with your goals.

- The Certified Public Accountant (CPA): Your CPA is the tax strategist. Their entire focus is on minimizing income, gift, and estate taxes, ensuring every financial move is as tax-efficient as possible.

- The Financial Advisor: This is the professional managing your investment portfolio. They work to align your assets with the long-term goals of your estate plan, making sure the engine of your wealth continues to run smoothly.

- The Insurance Specialist: They analyze your risk exposure and find the right solutions. A common strategy is using life insurance, often held within an ILIT, to provide ready cash for taxes and other estate expenses without having to sell off other assets.

This kind of collaboration is non-negotiable in a world where managing wealth has become incredibly complex. Today’s wealth managers must be fluent in handling diverse asset classes and using technology to navigate what many are calling the 'great wealth transfer.' You can find more insights on evolving wealth trends on msci.com.

A Step-by-Step Implementation Checklist

Once your team is in place, it’s time to get to work. Implementation is all about organization and clear communication. Following a simple checklist ensures nothing gets missed.

- Gather All Essential Documents: Start by collecting everything—financial statements, property deeds, insurance policies, business agreements, the works.

- Define Your Objectives: Get crystal clear on what matters most to you. Is it minimizing taxes? Protecting assets from creditors? Ensuring a smooth business succession? Or is philanthropy your top priority?

- Draft and Review Legal Documents: Your attorney will create the first drafts of your will, trusts, and powers of attorney. Then, the entire team should review them to make sure every angle is covered.

- Fund Your Trusts: This step is absolutely critical and often overlooked. You have to formally transfer your assets by retitling them into the name of your trusts. If you skip this, the trust is just an empty shell.

- Schedule Regular Reviews: An estate plan isn't static. Commit to reviewing it with your team at least once a year, and immediately after any major life event (like a birth, death, or divorce) or significant change in tax law.

A sophisticated estate plan is a living document, not a one-time event. Continual vigilance and regular updates are essential to ensure it remains aligned with your life, your goals, and the ever-changing legal and economic landscape.

Frequently Asked Questions

When it comes to something as important as your legacy, it’s only natural to have a few questions. Below, we’ve tackled some of the most common ones we hear from clients, offering straightforward answers to help you navigate the process.

How Often Should I Review My Estate Plan?

Think of your estate plan as a living document, not something you set in stone and forget. As a rule of thumb, it’s wise to sit down with your advisory team for a thorough review at least every three to five years.

Of course, life doesn’t always stick to a neat schedule. Certain events should trigger an immediate check-in to make sure your plan still reflects your reality. These moments include:

- A marriage, divorce, or the beginning of a new partnership.

- The arrival of a new child or grandchild, whether by birth or adoption.

- A major shift in your financial picture, like selling a business or a significant inheritance.

- Changes in the tax code, such as the upcoming adjustments to the estate tax exemption.

Keeping your plan current ensures it always works for you, no matter what changes come your way.

Revocable vs. Irrevocable Trusts Explained

At their core, the difference between these two trusts comes down to one thing: control. A revocable trust is flexible. You’re in the driver’s seat, free to change the terms or even dissolve it completely whenever you want. Its main job is to hold your assets to sidestep the probate process—a great tool for privacy and efficiency, but it won’t offer any tax advantages or protection from creditors.

An irrevocable trust, on the other hand, is built for permanence. Once you transfer assets into it, you’re handing over the keys for good. You generally can’t change the terms or take the assets back. It’s precisely this trade-off—giving up control—that allows the assets to be removed from your taxable estate, offering powerful protection against both estate taxes and lawsuits.

You can think of a revocable trust like a personal safe you hold the key to. An irrevocable trust is more like a bank’s vault—you’ve handed over control for maximum, long-term security.

Does a Living Trust Protect Assets from Lawsuits?

This is a very common misconception. A standard revocable living trust does not shield your assets from personal creditors or legal claims. Why? Because you still have full control and can access the assets at any time, the law views them as your personal property.

For real asset protection, you need to create a barrier between you and your wealth. This is where tools like an irrevocable trust or other structures like an LLC or Family Limited Partnership (FLP) come in. By legally giving up ownership and direct control, you make it far more difficult for anyone to reach those assets in a lawsuit.

At Commons Capital, we specialize in creating sophisticated estate plans that preserve your wealth and secure your legacy. Contact us today to build a strategy that protects what you've worked so hard to achieve.