Imagine upgrading your real estate portfolio without the immediate tax bill eating into your profits. That’s the real power of a 1031 exchange property strategy. It allows you to defer capital gains taxes on the sale of a business or investment property by reinvesting the proceeds into a new, like-kind asset. Think of it like trading up cars; you use the full value of your old vehicle to get a better one, pushing off the tax consequences until you finally decide to cash out for good.

Unleashing the Power of Your Real Estate Investments

Named after Section 1031 of the U.S. Internal Revenue Code, this exchange is one of the most powerful wealth-building tools a savvy real estate investor has. It lets you defer capital gains taxes when you sell an investment property, as long as you reinvest the proceeds into a new, "like-kind" property.

This isn't about tax evasion; it's about smart tax deferral. Instead of losing a huge chunk of your gains—often 15-20% or more—to the IRS, you get to put that entire amount to work again. This lets your capital grow, compound, and scale your assets way faster than if you were just selling and buying in separate, taxable transactions.

Why Every Investor Should Understand This Strategy

The main advantage is simple: maximum capital reinvestment. By putting off the tax bill, you keep the full purchasing power of your equity. This opens the door to acquiring higher-value assets, diversifying into different types of property, or moving your investments into more profitable markets. It's a move that can seriously accelerate your wealth-building journey.

For a deeper dive into how this powerful tool works, check out this comprehensive guide to the 1031 exchange.

A Tool with a Rich History

The 1031 exchange concept has been a cornerstone of American real estate investing since it was created way back in 1921. At first, these deals were clunky and required simultaneous swaps, which made them incredibly hard to pull off.

Everything changed with the landmark Starker v. United States case in 1979, which paved the way for the modern deferred exchanges we use today. Congress made it official in 1984, setting the 45-day identification and 180-day closing deadlines that now define the process.

The core idea is to transform what would be a taxable sale into a non-taxable event. The IRS views it as one continuous, ongoing investment, not a sale and a separate purchase. This shift in perspective is what unlocks its financial power.

By understanding the nuts and bolts of a 1031 exchange, you can make much smarter decisions about your real estate portfolio. While it's a key strategy for deferring taxes, it’s not the only one; you can explore other methods in our guide on how to offset capital gains. Throughout this guide, we’ll break down all the essential rules, timelines, and strategies you need to use this tool effectively.

Decoding the Critical Rules and Timelines

A successful 1031 exchange hinges on playing by a very specific, and very strict, set of IRS rules. Get them right, and the tax deferral is a powerful wealth-building tool. But get them wrong, and the whole thing can unravel, leaving you with the exact tax bill you were trying to avoid.

Let's start with the most fundamental concept: the "like-kind" requirement. This is probably the most misunderstood part of the entire process. It doesn't mean you have to trade a duplex for a duplex or a warehouse for a warehouse. The rule is actually much more investor-friendly than it sounds.

"Like-kind" simply refers to the nature of the property, not its specific type or condition. Essentially, any real estate held for investment or for productive use in a business can be exchanged for any other real estate that will be held for the same purpose. So yes, you can absolutely trade an apartment building for a portfolio of single-family rentals, or even swap a commercial office space for a piece of raw land.

The Unforgiving 1031 Exchange Clock

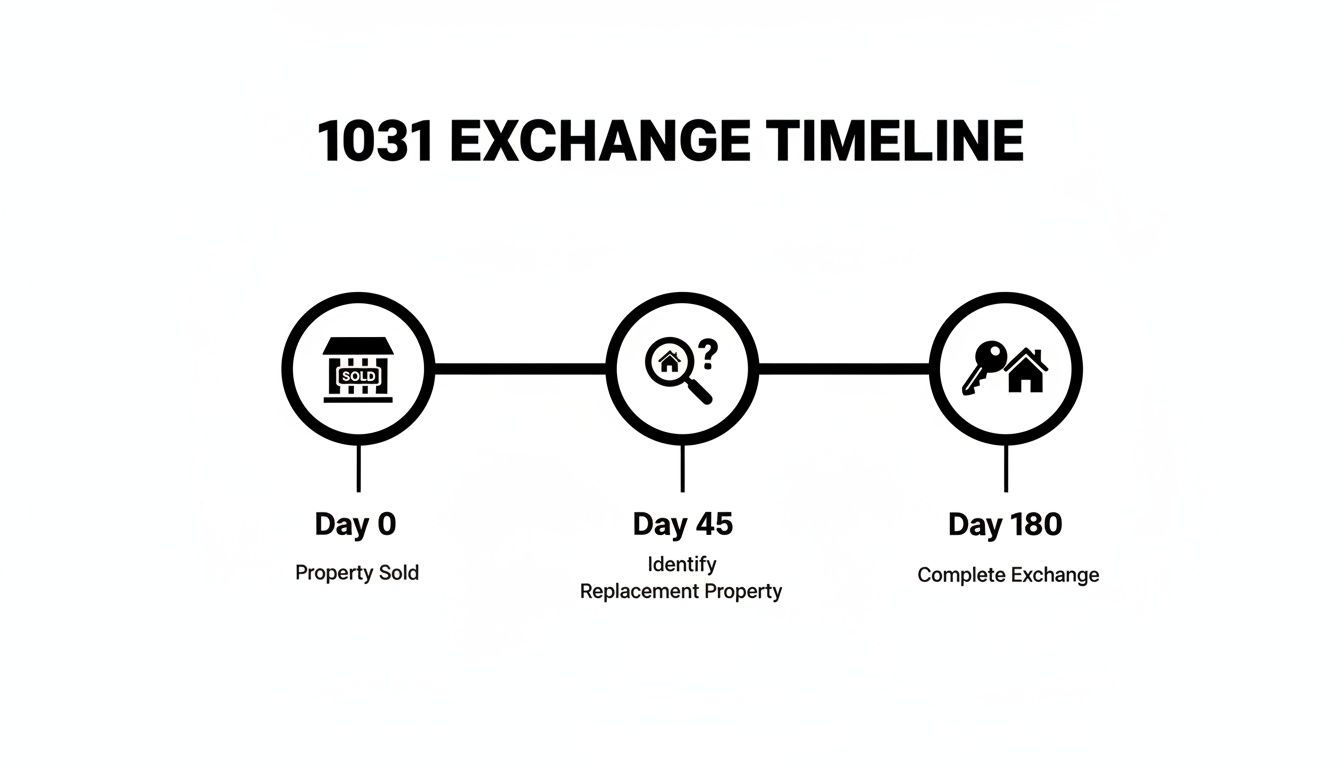

Where the process gets truly unforgiving is with the deadlines. The moment you close the sale on your original property (called the relinquished property), a clock starts ticking. Two critical deadlines are locked in, and the IRS offers no extensions or grace periods.

- The 45-Day Identification Period: You have precisely 45 calendar days to officially identify potential replacement properties. This isn't a casual list—it's a formal, signed, written declaration you deliver to your Qualified Intermediary.

- The 180-Day Closing Period: From the day you sell your original property, you have a total of 180 calendar days to close on one or more of the properties you identified. Remember, this 180-day window includes the 45-day period, so once you've identified your targets, you have 135 days left to get the deal done.

Missing either of these deadlines, even by a single day, is a deal-breaker. The exchange fails, and the tax deferral is lost. The IRS is notoriously rigid on this point, which is why planning ahead is everything.

To help you keep these critical deadlines straight, here is a simple breakdown of the core timeline and identification rules you must follow.

Key 1031 Exchange Timeline and Rules

Following this roadmap is non-negotiable for a valid exchange. The Qualified Intermediary is your partner in ensuring you stay on the right side of these rules.

The Role of the Qualified Intermediary

There's another ironclad rule: you can never, ever touch the money. If the proceeds from the sale of your relinquished property land in your personal or business bank account, even for a second, the exchange is busted. This is called "constructive receipt," and it's an instant disqualifier.

So how do you avoid this? The IRS requires you to use a Qualified Intermediary (QI), sometimes called an accommodator.

Think of a QI as a neutral, independent third party whose entire job is to facilitate your exchange correctly. They're not on your side or the other side; they're on the side of compliance. They handle a few crucial tasks:

- Holding the Funds: When your first property sells, the proceeds go directly to the QI, who holds them in a secure escrow account.

- Managing the Paperwork: The QI prepares the formal exchange agreements and receives your official 45-day identification notice.

- Funding the Purchase: When it's time to buy your new property, the QI wires the funds directly to the closing agent to finalize the transaction.

By stepping in as the middleman, the QI creates the necessary separation between you and the cash, keeping your exchange fully compliant. Choosing a reputable, experienced QI is one of the most important decisions you'll make. Their expertise is your primary defense against the simple but costly mistakes that could derail your entire tax strategy.

Navigating the Different Types of 1031 Exchanges

When it comes to a 1031 exchange property transaction, the core idea is always the same: deferring capital gains taxes. But that doesn't mean the strategy is one-size-fits-all. The best investors know how to adapt the structure of their exchange to fit their specific goals and, just as importantly, the reality of the market they're in.

Most people are familiar with the standard Delayed Exchange. This is the classic "sell first, buy later" model that works within the well-known 45/180 day timeline. It's the most common for a reason—it's straightforward. But in a fast-moving, competitive market, it's not always the smartest move.

Thankfully, there are other ways to structure an exchange. Knowing the difference between them can be what separates a successful, tax-deferred investment from a failed exchange and an unexpected tax bill.

The Most Common Path: The Delayed Exchange

The Delayed Exchange is the workhorse of the 1031 world. Just as the name implies, there's a delay between when you sell your old property (the "relinquished" property) and when you buy the new one (the "replacement" property). This structure gives you the full 45 days to identify potential replacements and a total of 180 days to close on one of them, offering a practical window to get a deal done.

- Best For: An investor who has a good idea of what they want to buy but needs some time on the ground to find the perfect asset after their sale closes.

- Example Scenario: You sell a rental condo. Your goal is to roll the proceeds into a small apartment building, but you need several weeks to scout different neighborhoods, run the numbers, perform due diligence, and negotiate the right price. The delayed structure is built for this kind of methodical approach.

Seizing Opportunity with a Reverse Exchange

What happens when you stumble upon the perfect replacement property before you've even listed your current one? In a hot market, waiting could mean losing the deal. This is precisely where a Reverse Exchange comes in, allowing you to lock down and acquire the new property first and then sell your old one.

Of course, the IRS won't let you own both properties at the same time within the exchange. To solve this, a specialized third party called an Exchange Accommodation Titleholder (EAT) steps in. The EAT, typically an entity set up by your Qualified Intermediary, temporarily "parks" the title to either your new property or your old one. It’s a clever but complex maneuver that keeps your exchange compliant.

This is essentially the standard timeline flipped on its head.

This visual shows the critical 45-day identification and 180-day closing deadlines that apply no matter which type of exchange you're pursuing.

The Rise of More Strategic Exchanges

We're seeing a clear trend toward these more complex exchange structures. Reverse exchanges are gaining serious traction, especially in tight markets where inventory is scarce, because they give buyers a massive competitive edge. At the same time, more investors are using their exchanges to fund new construction or major renovations, allowing them to use tax-deferred dollars to create their ideal property. You can find more data on these growing 1031 exchange trends on ipx1031.com.

Building Value with an Improvement Exchange

Sometimes the perfect property doesn't exist—you have to build it. An Improvement Exchange (also called a Construction or Build-to-Suit Exchange) lets you use 1031 funds to not only buy a property but also to pay for the improvements on it.

Much like a reverse exchange, the Exchange Accommodation Titleholder (EAT) is essential here. The EAT acquires and holds title to the new property while your exchange funds are used to pay for the construction. Once the work is done—or the 180-day exchange period is up—the improved property is transferred over to you.

This is a powerful tool for value-add investors looking to develop raw land or execute a major renovation on an existing building. It helps ensure the final value of the new property meets or exceeds the value of the one you sold, which is a fundamental requirement of any 1031 exchange. By understanding these different approaches, you can select the 1031 exchange property strategy that truly aligns with your financial vision.

Advanced Strategies for Portfolio Growth

For savvy investors, a 1031 exchange property isn't just a tax-deferral tactic—it's a powerful engine for strategic portfolio growth. Once you move past the basic property-for-property swap, you start to see the real potential: engineering growth, diversifying your assets, and even shifting from hands-on landlord to passive investor.

This is where the 1031 exchange stops being a one-off transaction and becomes the foundation of a real estate empire. It’s a shift in mindset, from simply replacing one property to using the exchange as a mechanism to solve bigger portfolio challenges or acquire a piece of institutional-grade real estate. This approach can completely change your investment trajectory, opening doors you might have thought were reserved for major real estate firms.

Unlocking Passive Income with Delaware Statutory Trusts

One of the most effective advanced strategies involves something called a Delaware Statutory Trust (DST). The easiest way to think of a DST is as a way to buy a small, completely passive slice of a very large, professionally managed property—think medical office complexes, massive apartment communities, or high-end shopping centers.

For an investor tired of the late-night calls and tenant headaches, a DST is a game-changer. The process is pretty simple: you sell your property and roll the 1031 exchange funds into beneficial interests in one or more DSTs. The IRS considers this a "like-kind" real estate investment, so you complete your exchange while hitting several key goals:

- Hands-Off Ownership: The DST sponsor takes care of everything, from asset management to property maintenance.

- Built-in Diversification: You can spread your capital across multiple DSTs, diversifying by property type and geographic location.

- Access to Premium Real Estate: DSTs give individual investors a ticket to the big leagues, allowing them to own a piece of properties that would otherwise be far out of reach.

A huge advantage of DSTs is how they simplify the exchange timeline. Sponsors usually have a ready inventory of pre-vetted properties, which can be a lifesaver when you're staring down that tight 45-day identification deadline.

Mastering the Art of Boot and Debt Management

A critical part of any serious 1031 exchange property strategy is skillfully managing "boot." Boot is just a term for any non-like-kind property you receive in an exchange, and it's taxable on the spot. It usually shows up in one of two ways: cash boot (any cash you walk away with) or mortgage boot (when your new property has less debt than your old one).

To defer all your capital gains taxes, the rule is simple: you have to buy a replacement property of equal or greater value and carry over an equal or greater amount of debt. Getting this math wrong can trigger a surprise tax bill, defeating the whole purpose of the exchange. For a deeper dive into getting your numbers right, our guide on how to value commercial real estate is an essential read.

Common Scenarios and Strategic Solutions

Let’s walk through a real-world example. An investor sells a building for $1 million. They had a $400,000 mortgage on it, so they have $600,000 in equity. To kick the tax can down the road completely, they must buy a new property worth at least $1 million and take on at least $400,000 in new debt.

Now, say they find a great property for $1.2 million but can only get a $300,000 mortgage. That leaves them with $100,000 of mortgage boot, which is now taxable income. The classic fix here is to bring an extra $100,000 in cash to closing to make up for the lower debt amount.

As you grow, another advanced strategy is simply running your portfolio more efficiently. Leveraging the right technology to streamline operations is key, and it's worth exploring some of the top property management apps to see how you can maximize returns. Understanding these nuances is what separates the novices from the pros, turning potential tax traps into opportunities for smart financial planning.

Common 1031 Exchange Pitfalls to Avoid

Executing a 1031 exchange is one of the most powerful wealth-building tools in real estate, but it’s a path littered with technical landmines. One wrong move can blow up the entire deal, instantly disqualifying your exchange and turning a tax-deferred dream into a taxable nightmare.

Let's be clear: the IRS doesn’t grade on a curve here. The rules are rigid, deadlines are absolute, and there's no room for "close enough." Success isn't just about picking the right property; it’s about flawlessly navigating a precise legal and financial process. Knowing where others have stumbled is the best way to protect your capital.

Failing the Clock and the Calendar

The most common and catastrophic mistake is botching the deadlines. Investors constantly underestimate how quickly the 45-day identification period and 180-day closing period vaporize.

- The 45-Day Identification Sprint: This isn't a suggestion; it's a hard stop. You have exactly 45 days from the day you sell your property to deliver a formal, written list of potential replacement properties. Waiting until your sale closes to start your search is a recipe for disaster.

- The 180-Day Closing Gauntlet: You must close on one of those identified properties within 180 days of your initial sale. Remember, that clock starts ticking on day one, so the 45-day window is part of the 180 days, leaving you just 135 days to negotiate, get financing, and wrap up due diligence.

The only way to win this race is to start before the gun goes off. Your search for a replacement property should be well underway before your current one is even on the market. Have a vetted list of primary targets and backups ready to go the moment the exchange officially kicks off.

The Dangers of "Touching the Money"

Another cardinal sin is what’s called "constructive receipt" of your sale proceeds. If the money from your relinquished property hits your personal or business bank account—even for a second—the exchange is dead on arrival.

This is precisely why a Qualified Intermediary (QI) isn't just a good idea; it's mandatory. The QI is a neutral third party who holds your funds in a secure account from the moment your first property sells until the replacement is purchased. Choosing a reputable, bonded, and insured QI is one of the most important decisions you'll make in this entire process.

Vague or Improper Identification

Just having a few properties in mind isn’t enough. Your 45-day identification notice must be formal, specific, and unambiguous. A vague description like "a three-bedroom rental in downtown Austin" won't cut it.

You also have to follow one of the strict identification rules, like the Three-Property Rule or the 200% Rule. Failing to do so will nullify your efforts. Each potential property has to be described with enough detail—like a legal description or street address—that it can't be confused with anything else.

The strategic importance of mastering these rules can't be overstated. During the mid-2010s, for example, 1031 exchanges for retail properties skyrocketed as savvy investors used the mechanism to swap out struggling assets for centers with better tenants and stronger cash flow. One brokerage reported that nearly 65% of its deals were 1031 trades, a testament to how investors use this tool to proactively upgrade their portfolios. You can read more about that trend in this 1031 exchange analysis on icsc.com. By avoiding these common traps, you can do the same.

Assembling Your Professional 1031 Exchange Team

Pulling off a 1031 exchange isn't a solo mission—it's absolutely a team sport. While knowing the rules yourself is a great start, the real secret to a smooth, successful exchange is surrounding yourself with a crew of seasoned professionals before you even begin.

Trying to go it alone is one of the fastest ways to put your entire investment at risk. Seriously, building out your team should be the very first thing you do, long before your relinquished property even hits the market. Getting these experts in your corner early is the single best move you can make to protect your capital and ensure everything goes off without a hitch.

Your Non-Negotiable Advisory Team

Think of these four professionals as your starting lineup. Missing even one of them leaves a huge gap in your defense, creating a vulnerability that could easily jeopardize the whole deal.

- Qualified Intermediary (QI): This is the one role the IRS absolutely requires you to have, and for good reason. A solid QI acts as the secure, independent third party who holds your sale proceeds so you don't accidentally take "constructive receipt" of the funds. They also draft the critical exchange documents and keep the transaction compliant with all the complex regulations.

- Experienced Real Estate Agent: Don't just hire any agent. You need someone who lives and breathes the fast-paced, high-pressure world of 1031 exchanges. A great 1031-savvy agent is worth their weight in gold when it comes to quickly finding qualified replacement properties and skillfully handling negotiations under a ticking clock.

- Strategic Tax Advisor (CPA): Your CPA is your financial quarterback for the entire process. They’ll run the numbers to show you exactly what your capital gains tax exposure would be without an exchange. They also help analyze the tax consequences of potential replacement properties to make sure the move aligns with your bigger financial picture.

- Detail-Oriented Real Estate Attorney: The attorney is your legal watchdog. Their job is to pore over every line of the contracts, title reports, and closing documents with a fine-toothed comb. They are there to shield you from legal landmines and ensure the property titles are transferred cleanly and correctly.

Getting this team together early creates a powerful, coordinated defense against the common mistakes that can derail an exchange. From identifying the right asset to securing financing, which you can learn about in our article on commercial loans for investment property, their collective expertise is your greatest asset. Don't wait until the 45-day clock is ticking to start making calls.

Frequently Asked Questions

When you're dealing with a 1031 exchange property, a lot of questions pop up. It's only natural. Getting the details right is the difference between a successful tax deferral and an unexpected bill from the IRS, so let's clear up some of the most common points of confusion.

Think of it this way: a small mistake can unravel the entire strategy. Getting these facts straight before you even list your property is crucial.

Can I Use a 1031 Exchange for My Primary Residence?

That's a definite no. A 1031 exchange is built specifically for investment or business properties. Your personal home falls under a different part of the tax code—Section 121—which is actually pretty generous on its own. It often lets you exclude a huge chunk of capital gains from taxes without jumping through any exchange hoops.

What about a vacation home? That’s where things get tricky. It might qualify, but you'll have to prove it was a legitimate investment property with very limited personal use. The IRS has some specific "safe harbor" guidelines you'd need to have followed to the letter.

What Happens If I Cannot Find a Property in 45 Days?

If you can't officially pinpoint a replacement property within that 45-day window, the exchange fails. Period. That deadline is set in stone, and there are absolutely no extensions, no matter the reason.

Once that 45th day passes, your Qualified Intermediary has to return the sale proceeds to you. The deal then becomes a regular, fully taxable sale. You’ll be on the hook for all the capital gains taxes in that tax year. This is exactly why savvy investors start hunting for their next property long before the first one even closes.

The 45-day identification rule is the single biggest reason that 1031 exchanges fail. Meticulous planning and having a list of backup properties are your best defenses against this unforgiving deadline.

Do I Have to Reinvest All of the Sale Proceeds?

If you want to defer 100% of your capital gains, you have to play by two key rules. First, the purchase price of your new property (or properties) must be equal to or greater than the net selling price of the one you just sold.

Second, you have to roll all of the net cash from the sale into the new deal. Any money that ends up in your pocket ("cash boot") or any reduction in your overall mortgage debt ("mortgage boot") is seen as profit by the IRS and gets taxed. For a full deferral, the goal is simple: trade up or equal in both equity and debt.

Can I Exchange One Property for Multiple Properties?

Yes, and this is one of the most powerful strategies out there. It's a fantastic way to diversify. You could sell one large 1031 exchange property—say, an apartment building—and use the money to buy several single-family rentals in different up-and-coming markets.

It works the other way, too. You can consolidate your portfolio by selling off a few smaller properties and rolling all that equity into one bigger, higher-quality asset. As long as the math works out—the total value you buy is equal to or greater than the total value you sold—the exchange is perfectly valid.

Navigating the complexities of a 1031 exchange and integrating it into your broader wealth strategy requires expert guidance. At Commons Capital, we specialize in helping high-net-worth individuals and families make informed financial decisions to achieve their long-term goals. To learn how we can assist with your investment portfolio, visit us at https://www.commonsllc.com.