Figuring out what a commercial property is really worth comes down to three classic methods: analyzing the income it can produce, comparing it to what similar properties have recently sold for, and calculating its replacement cost. A smart valuation doesn't just pick one; it blends the insights from all three to get to the true market value.

Why Accurate Commercial Property Valuation Matters

Understanding how to value commercial real estate isn’t just an academic exercise—it’s the most fundamental skill for any serious investor. Think of an accurate valuation as your primary defense against overpaying. It’s also your sharpest tool for spotting those undervalued gems with serious upside potential.

Getting this number right drives every decision you'll make, from the initial offer and financing structure all the way to your eventual exit strategy.

A precise valuation gives you a clear picture of potential returns, helps you lock in better terms with lenders, and makes sure the deal actually lines up with your long-term financial goals. For instance, many investors are getting creative with how they fund their deals. Our guide on buying real estate in an IRA shows just how critical a rock-solid valuation is, especially when you're using non-traditional financing.

The Three Pillars of Valuation

At the core of any professional appraisal are three distinct, yet complementary, approaches. Each one gives you a different lens through which to view the property's value. When you put them together, you get a complete financial picture.

- The Income Approach: This is all about the property's ability to generate cash flow. For assets like office buildings, apartment complexes, or retail centers, this is often the most important piece of the puzzle.

- The Sales Comparison Approach: This method keeps you grounded in reality. It looks at what comparable properties in the area have actually sold for recently.

- The Cost Approach: This one asks a simple question: What would it cost to build a similar property from the ground up today, factoring in depreciation for the existing building?

A robust valuation doesn't just average these three numbers. Instead, it involves a weighted analysis, where the relevance of each approach shifts based on the property type, its age, and the quality of available data.

To really dig into the details, exploring broader concepts like Property Valuation Analytics can give you a more comprehensive framework. This guide will walk you through each of these core methods, step-by-step, with practical examples to help you move forward on your next investment with confidence.

Mastering the Income Approach for Property Valuation

When you're dealing with income-producing assets—think office buildings, retail centers, or apartment complexes—cash flow is king. It's the ultimate measure of an asset's worth, which is exactly why the Income Capitalization Approach is so powerful.

This is the method most seasoned investors rely on. It cuts through the noise and creates a direct, tangible link between a property's earning potential and its price tag. The logic is simple: a property is worth what it can earn.

Getting to Your Net Operating Income

The entire Income Approach is built on one critical number: the Net Operating Income (NOI). This is your property's pure profit engine—its total income after all operating expenses are paid, but before you factor in things like mortgage payments or income taxes.

Getting this number right is absolutely non-negotiable. It means diving deep into the property's financial records. A solid grasp of understanding financial statements isn't just helpful; it's essential for pulling the right data.

You begin with the Potential Gross Income (PGI), which is what the property would generate with 100% occupancy. From there, you subtract an allowance for expected vacancy and credit losses to land on the Effective Gross Income (EGI).

Then, you deduct all the operating expenses:

- Property taxes

- Insurance

- Management fees

- Repairs and maintenance

- Utilities

- Any administrative costs

What's left is your NOI. This single figure is the heartbeat of your valuation.

To give you a clearer picture, here’s a simplified breakdown for a hypothetical commercial property.

Sample NOI Calculation for a 10-Unit Commercial Building

This NOI of $158,880 is the number we'll use to determine the property's value.

The Art and Science of the Cap Rate

With your NOI in hand, the next piece of the puzzle is the capitalization rate (cap rate). Think of the cap rate as a market-driven snapshot of the expected return for a property like yours, in its specific location, at this moment in time.

Valuation Formula: Property Value = Net Operating Income (NOI) / Capitalization Rate (Cap Rate)

Choosing the right cap rate is where experience really comes into play. It's a reflection of risk. A lower cap rate means lower perceived risk and, consequently, a higher valuation. A higher cap rate signals more risk and a lower price tag.

Several factors influence this number:

- Property Location: A building in a prime downtown corridor will always have a lower cap rate than one in a struggling suburb.

- Asset Class: A logistics warehouse leased to a Fortune 500 company is a safer bet than a small retail strip with local tenants. The warehouse gets the lower cap rate.

- Tenant Quality: Properties with long-term leases to creditworthy tenants (like a national pharmacy) are highly desirable and valued accordingly.

- Market Conditions: The broader economy, current interest rates, and local supply and demand all push cap rates up or down.

Putting It All Together: A Real-World Example

Let's see this in action. Suppose you're analyzing a multi-tenant office building with a calculated annual NOI of $500,000. After researching comparable sales in the area, you find that similar buildings are trading at a 5.0% cap rate.

Here’s the math:

- NOI: $500,000

- Cap Rate: 5.0% (or 0.05)

- Calculation: $500,000 / 0.05 = $10,000,000

Just like that, the Income Approach gives us an estimated value of $10 million. This straightforward calculation is the bedrock of professional commercial real estate valuation, turning a simple income stream into a solid, defensible number.

Using the Sales Comparison Approach Like a Pro

While the Income Approach looks at a property's potential, the Sales Comparison Approach grounds your valuation in cold, hard reality. It answers a simple but powerful question: what have similar properties nearby actually sold for?

This method is all about reflecting what real buyers are willing to pay, which makes it a critical sanity check when you’re learning how to value commercial real estate. At its core, it's about finding truly comparable properties—often called "comps"—that have sold recently.

Sourcing and Selecting Quality Comps

Finding the right comps is where the rubber meets the road. You can't just pick any property that sold in the same zip code last year. The details matter, and even small differences can throw your valuation way off.

You've got to look for similarities across a few key features:

- Location and Proximity: Is the comp in a similar neighborhood? Does it have comparable traffic, visibility, and zoning?

- Property Size: This means both the building's square footage and the overall lot size.

- Building Age and Condition: A brand-new build-to-suit isn't a fair comparison to a 30-year-old property that needs a new roof.

- Tenancy and Lease Terms: Are the comps occupied by similar tenants on comparable leases? A building with a long-term national tenant is a different animal than one with a dozen small, local tenants on short-term leases.

I always tell clients to focus on sales from the last six to twelve months. Anything older than that, especially in a fast-moving market, might as well be from another era.

The Art of Making Adjustments

Here's the thing: no two properties are ever identical. The real skill in this approach lies in making logical, defensible adjustments to the comps' sale prices to account for these differences.

If a comp is superior to your property—say, it has better road frontage or a newer HVAC system—you subtract value from its sale price. If it's inferior—maybe it's smaller or has higher vacancy—you add value. This process essentially neutralizes the differences, giving you a clearer picture of what that comp would have sold for if it were identical to your property.

Think of it like this: you are not changing the value of your property. You are adjusting the comparable property's sale price to make it a more accurate benchmark. It's a critical distinction that keeps the process objective.

A Practical Example in Action

Let’s walk through a real-world scenario. Say you're valuing a 10,000 sq ft retail building. After some digging, you find three recent comps.

- Comp A: Sold for $2.1M. It's identical in size but sits on a much busier intersection. You and your broker determine that superior location is worth about $100,000. Your adjusted price for Comp A becomes $2.0M.

- Comp B: Sold for $1.9M. It's very similar, but you know it has significant deferred maintenance, including an ancient HVAC system you estimate costs $75,000 to replace. Your adjusted price for Comp B is now $1.975M.

- Comp C: Sold for $2.2M. This one is a bit larger at 11,000 sq ft. Based on a price-per-square-foot analysis of similar properties, you subtract $200,000 for that extra space. The adjusted price for Comp C is $2.0M.

After your adjustments, all three comps are pointing to a value right around $2.0 million. This tight grouping gives you a ton of confidence in your estimate. You've gone from raw sales data to a nuanced and supportable valuation—exactly what a savvy investor needs.

When to Use the Cost Approach for Valuation

While the Income and Sales Comparison approaches get most of the attention, the Cost Approach offers a totally different—and sometimes critical—angle. It tackles one simple question: what would it cost to build this exact property again, right now, from scratch?

This method becomes your MVP when you’re dealing with unique or special-purpose properties. Think about valuing a school, a newly built church, or a government building. These assets don't hit the open market often, and they certainly don't generate income like an office building. In these cases, the Cost Approach is often the most logical and defensible way to pin down a value.

The Core Formula for the Cost Approach

The logic here is pretty straightforward. No savvy buyer is going to pay more for an existing property than it would cost to build a brand-new, identical one. It just doesn't make sense.

The calculation itself follows a clear path:

Replacement Cost - Accrued Depreciation + Land Value = Property Value

First, you figure out the replacement cost—the all-in price for materials, labor, and everything else to construct a similar building at today’s prices. Next, you subtract accrued depreciation, which is the value lost due to the property's age and condition. Finally, you add in the current market value of the land itself.

Understanding the Three Faces of Depreciation

Depreciation is where the real nuance comes in. It’s not just about how old a building is. It actually breaks down into three distinct types that every investor learning how to value commercial real estate needs to get familiar with.

- Physical Deterioration: This is the one everyone thinks of first—basic wear and tear. A leaky roof, cracked pavement in the parking lot, or an HVAC system on its last legs all fall under this category.

- Functional Obsolescence: This is about design or features that are just plain outdated. Imagine an office building with ceilings so low they feel claustrophobic, or a warehouse with support columns spaced so awkwardly that modern forklifts can't maneuver. The building works, but not well.

- External Obsolescence: This one is completely out of your control. It’s when something outside the property lines hurts its value. A new industrial park gets zoned right next to your retail center, or a major highway gets rerouted, killing your foot traffic.

The Cost Approach really sets a "floor" for a property's value. It’s incredibly useful for new construction where depreciation is almost zero, and it’s a go-to for figuring out insurance replacement values.

A Practical Walkthrough with a New Warehouse

Let's put this into action with a brand-new 50,000-square-foot warehouse.

Your first step is to nail down the land value. After looking at recent sales, you find that comparable parcels in the area are trading for around $500,000.

Next up is the replacement cost. You talk to a few builders and cost estimators and determine that building a similar warehouse today would run about $150 per square foot. That gives you a total replacement cost of $7.5 million (50,000 sq ft x $150/sq ft).

Since the warehouse is new, physical and functional depreciation are basically non-existent. We’ll also assume there are no new highways or industrial parks popping up next door. So, accrued depreciation is $0.

Now, the math is easy:

$7,500,000 (Replacement Cost) - $0 (Depreciation) + $500,000 (Land Value) = $8,000,000

This approach gives you a distinct perspective by focusing on what it would take to replicate the asset today. It's the perfect tool for special-use buildings where market data is thin. To see how this fits in with other valuation methods, check out our guide on common commercial real estate valuation models. Once you understand its components, you can apply the Cost Approach with confidence when the situation calls for it.

How to Reconcile the Three Valuation Methods

After running the numbers for the Income, Sales Comparison, and Cost approaches, you’ll have three distinct valuations. So, what's next? The final step in learning how to value commercial real estate isn't to simply average them out—it's to perform a thoughtful reconciliation.

This process is more art than science. It's about weighing each method based on its relevance to the specific property and, just as importantly, the quality of the data you were able to gather. Think of it as synthesizing three different expert opinions into one final, defensible conclusion.

Assigning Weight to Each Approach

The key is to assign a percentage weight to each valuation method, making sure the total adds up to 100%. This weighting is a direct reflection of your confidence in each approach for the property you're analyzing.

For a stable, fully-leased office building with a long history of predictable cash flow, the Income Approach is king. It will likely get the heaviest weighting, perhaps 60-70%. But for a unique property like a school or a brand-new industrial facility with no rental history, the Cost Approach suddenly gains a ton of significance and might be weighted much more heavily.

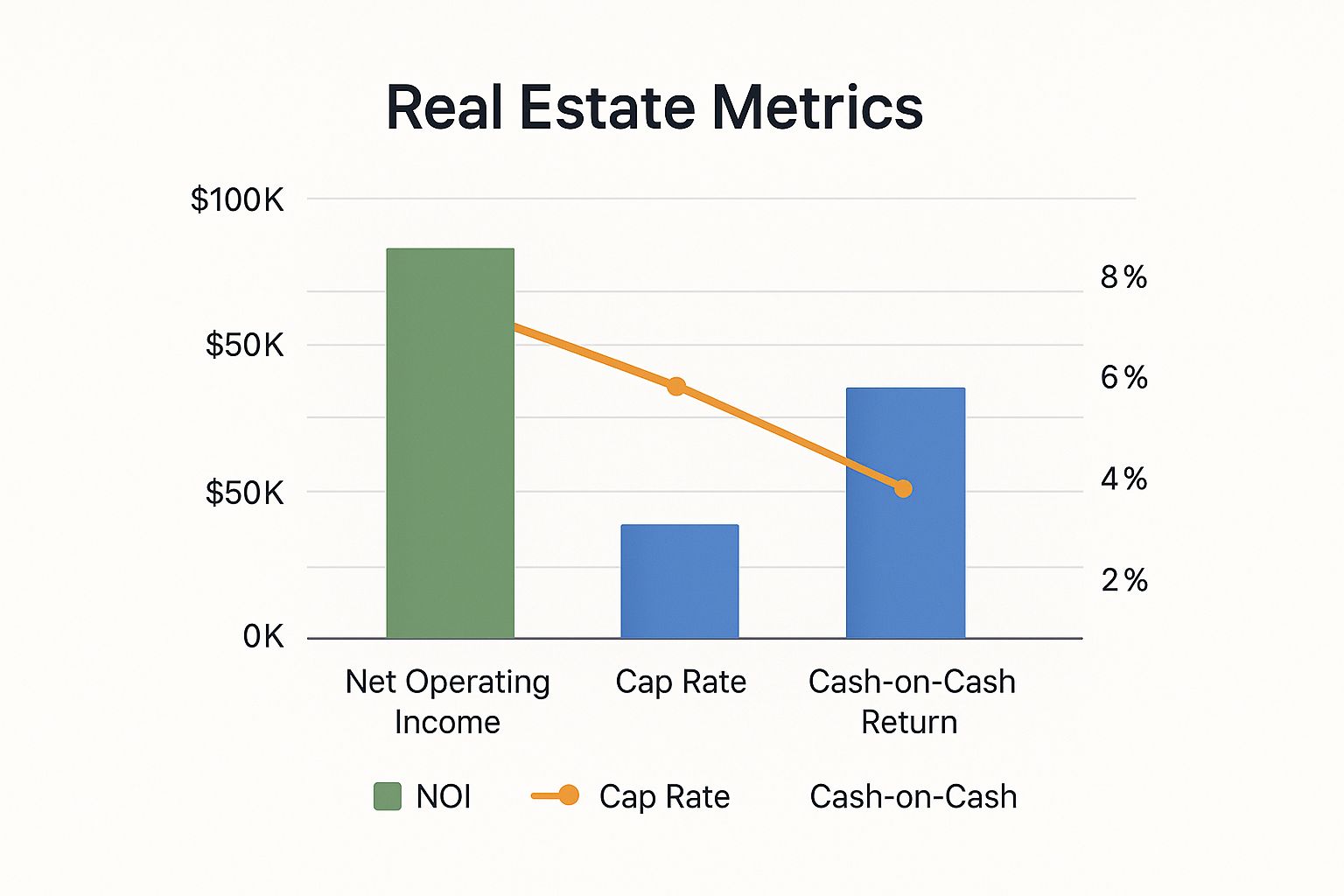

The infographic below breaks down some of the key financial metrics that drive the Income Approach, showing how Net Operating Income, Cap Rate, and Cash-on-Cash Return all fit together.

As you can see, a higher NOI directly boosts a property's value, while the cap rate acts as a market-driven lever on that income stream.

The goal of reconciliation is to arrive at a final value that reflects the most reliable indicators for that specific asset. It’s about building a logical argument for your final number, not just doing math.

Scenario-Based Weighting Examples

The right mix depends entirely on the asset in front of you. If you are preparing to sell a property, this final number becomes the foundation of your entire strategy. For more on this, our guide detailing how to sell a business provides great context on how valuation impacts exit strategies.

The weighting isn't random; it's a strategic decision based on the property's unique characteristics. The table below shows how you might adjust the weights for different types of commercial real estate.

As you can see, a property with reliable income streams will lean heavily on the Income Approach, while a brand-new or unique building will give more credence to the Cost Approach. Here’s a more detailed look at how you might assign weights in a couple of real-world scenarios:

- 15-Year-Old Multi-Tenant Retail Center:

- Income Approach: 60% (This is your strongest indicator, thanks to stable, diverse tenant income.)

- Sales Comparison: 30% (Good comps are likely available, providing essential market context.)

- Cost Approach: 10% (Less relevant here because of the property's age and depreciation.)

- Cost Approach: 50% (Highly relevant since depreciation is minimal and construction costs are current.)

- Sales Comparison: 30% (Recent sales of other new warehouses are solid comps.)

- Income Approach: 20% (Less reliable until the property is fully leased and stabilized.)

This weighted analysis moves you from raw calculations to a sophisticated and confident final valuation. It gives you a number you can stand behind in any negotiation.

Common Questions About Commercial Real Estate Valuation

Even when you have a solid handle on the three core valuation methods, you'll find that real-world scenarios always throw a few curveballs. Answering these practical questions is what separates a decent valuation from a truly insightful one. Let's dig into some of the most common questions investors grapple with.

How Does Tenant Credit Quality Affect a Property's Value?

The financial strength of your tenants is a massive lever on a property's value. Think about it: a building leased long-term to a national corporation with a stellar credit rating is about as close to a sure thing as you can get in real estate. That lower risk profile allows investors to accept a lower capitalization rate, which directly translates to a significantly higher property valuation.

On the flip side, a property filled with tenants on short-term leases or those with weaker financials introduces a lot more uncertainty. To stomach that higher risk, investors will demand a higher cap rate as compensation, which pushes the property's valuation down. It always comes back to the perceived stability of that income stream.

What Is the Difference Between As-Is and As-Stabilized Value?

These two terms are snapshots of a property at very different points in its life, and they're crucial for different reasons.

- 'As-Is' Value: This is exactly what it sounds like—the property's value in its current condition. It reflects today's occupancy, today's rental income, and its present physical state.

- 'As-Stabilized' Value: This is a forward-looking projection. It’s what the property could be worth once you’ve completed planned renovations or leased it up to its target occupancy. This number is the lifeblood of any value-add investor looking to buy, improve, and then refinance or sell for a profit.

Understanding both is non-negotiable. The 'As-Is' value grounds you in reality and helps you determine a fair offer, while the 'As-Stabilized' value validates the upside you're chasing.

Can Market Trends Heavily Influence a Valuation?

Absolutely. No property exists in a bubble. Valuations are deeply tied to the broader economic climate, and outside forces can swing your final number in a big way.

For instance, when the Fed raises interest rates, cap rates tend to rise across the market. This can lower property values even if your building's income hasn't changed a bit. Conversely, strong local job growth can create a surge in demand for space, allowing you to push rents and boost the property’s value. A sharp analysis always has one eye on the building and the other on the market's economic trajectory.

How Often Should a Commercial Property Be Revalued?

For anyone actively managing their assets, it’s a smart habit to revisit valuations at least once a year. This keeps you honest about your performance, helps you stay in sync with market changes, and flags opportunities to make strategic moves.

Of course, you'll need a formal, third-party appraisal during major events like a sale, a refinance, or for financial reporting requirements. But doing those regular, informal check-ins ensures you're never caught off guard and always have a clear-eyed view of what your assets are worth.

Navigating the complexities of commercial real estate valuation is a critical step in building a successful investment portfolio. At Commons Capital, we specialize in providing the expert guidance high-net-worth individuals need to make confident and informed financial decisions.

Discover how our private wealth management services can help you achieve your financial goals.