Securing a commercial loan for an investment property is fundamentally different from obtaining a residential mortgage for a personal home. This type of financing is a strategic business tool, designed specifically to purchase or refinance real estate intended to generate income.

Unlike a residential loan where a lender scrutinizes your personal salary, commercial loans focus primarily on the property's potential to produce consistent cash flow. This makes them the ideal financing option for acquiring assets like apartment buildings, office spaces, retail centers, and industrial warehouses. Understanding this distinction is the first step toward successfully scaling your real estate portfolio.

What Are Commercial Loans For Investment Property

At its core, a commercial loan for an investment property is a business-to-business transaction. It requires a shift in mindset—from thinking like a homeowner to thinking like a CEO securing capital for a profitable venture.

The property itself is the centerpiece of the deal. Whether it's a multi-unit apartment complex, a warehouse, or a local shopping center, its ability to generate reliable rental income is the lender's primary concern.

This financing is specifically for non-owner-occupied properties, including:

- Apartment buildings with five or more units

- Office buildings and professional suites

- Retail stores and shopping centers

- Industrial warehouses and distribution centers

- Mixed-use properties (e.g., retail on the ground floor, apartments above)

The Business-First Approach To Lending

The fundamental difference lies in the underwriting process. A residential loan application places your personal income and credit score under a microscope. A commercial loan application, however, shifts the focus directly onto the property's financial performance and viability as a standalone business.

Lenders are laser-focused on the property's Net Operating Income (NOI) and its capacity to cover mortgage payments with a healthy margin.

They assess this using a key metric called the Debt Service Coverage Ratio (DSCR). This powerful calculation compares the property's annual net operating income to its annual mortgage debt service. For a deeper dive into this crucial tool, check out what a DSCR loan is and how it works for rental property investors.

Key Takeaway: With commercial loans, the property must be financially self-sufficient. The lender's central question is, "Does this asset generate enough cash to comfortably cover its debt and still produce a profit?"

To provide a clearer picture, let's break down the key differences between commercial investment loans and the residential loans you might be more familiar with.

Commercial vs Residential Investment Loans at a Glance

This table offers a quick comparison to highlight how these two financing paths diverge, even when both are used for investment purposes.

As you can see, the structure, focus, and terms are fundamentally different. Choosing the right loan depends entirely on the scale and type of property you're targeting.

Market Trends And Investor Activity

The demand for commercial investment properties—and the loans that fund them—ebbs and flows with economic conditions. Recently, momentum in commercial real estate lending has been building.

For example, in the first quarter of the year, the CBRE Lending Momentum Index, which tracks commercial loan closings, increased by 13% from the previous quarter and an impressive 90% year-over-year. This surge in activity indicates renewed confidence among banks and private lenders, who are actively deploying capital for quality assets. You can find more on the latest commercial real estate lending trends on cbre.com.

Finding the Right Commercial Loan for Your Strategy

Choosing the right commercial loan for an investment property is not a one-size-fits-all decision. The optimal financing option is intrinsically linked to your specific investment strategy, the nature of the property, and your long-term goals. Think of it like a toolbox: you wouldn't use a sledgehammer when a precision tool is required.

Your strategy is the blueprint that dictates the loan structure. Are you planning a quick renovation and flip, or are you settling in for a decade of stable cash flow? Different objectives demand different financial instruments. For instance, investment strategies like short-term leasing for apartments carry a different risk and income profile than a long-term lease with a corporate tenant, and lenders evaluate them accordingly. Aligning your financing with your strategy is the key to maximizing returns.

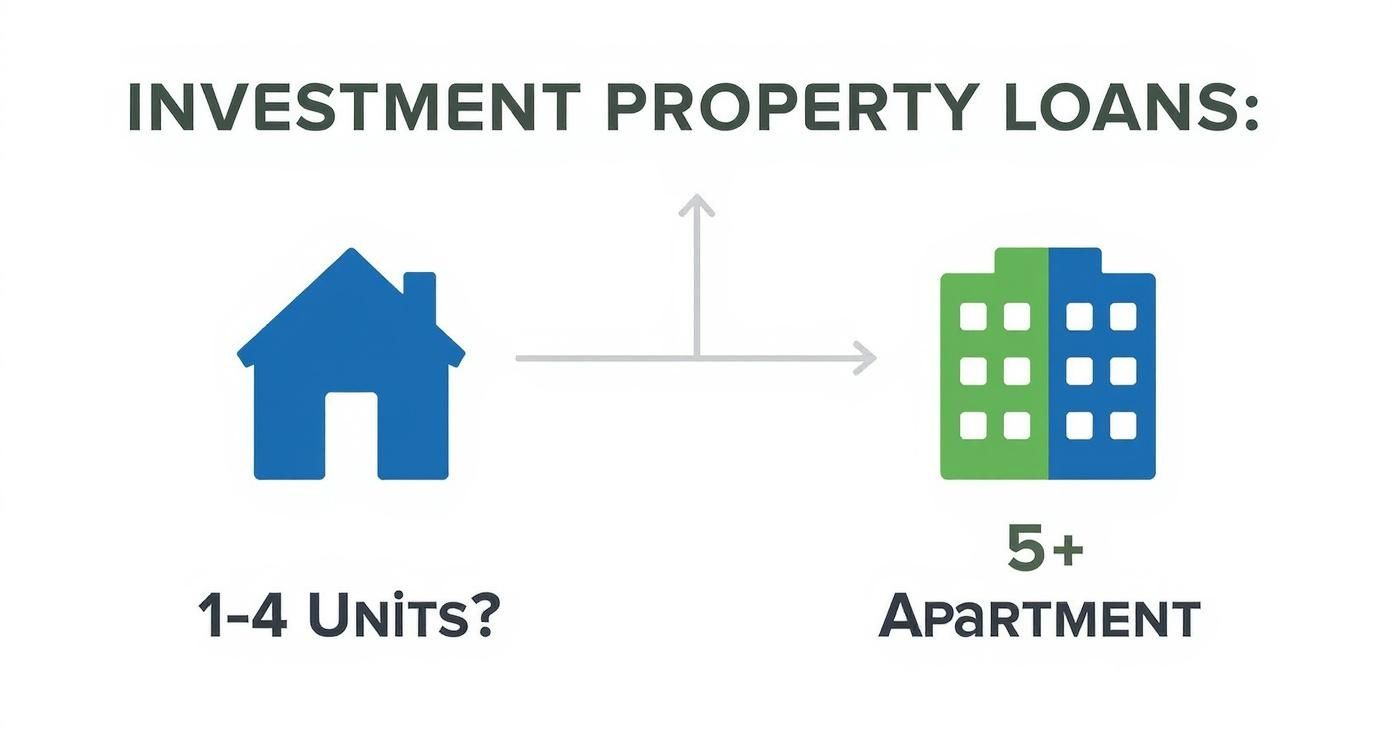

This decision tree provides a quick visual for the initial fork in the road, which often depends on the number of units.

As the infographic illustrates, there is a fundamental split. Properties with one to four units typically fall under residential lending rules. Once you reach five or more units, you enter the commercial financing arena, where the lender's focus shifts from your personal income to the property’s ability to generate cash flow.

Matching Loan Products to Investment Goals

Understanding the primary types of commercial loans is the first step. Each is designed for a specific purpose, offering unique advantages depending on your business plan.

- Traditional Commercial Mortgages: These are the workhorses of commercial real estate finance. They are ideal for stabilized, cash-flowing properties you intend to hold for the long term (typically 5+ years). Lenders favor these for assets with a proven track record of high occupancy and consistent income.

- Bridge Loans: As the name suggests, these are short-term loans designed to "bridge" a financial gap. They are perfect for "value-add" projects, such as renovating an outdated apartment building to increase rents or acquiring a property that needs significant improvements before it can qualify for permanent financing.

- Hard Money Loans: When speed is the priority, hard money loans are the solution. Funded by private investors rather than traditional banks, these loans can close much faster but come with higher interest rates and fees. They are best suited for short-term holds, fix-and-flips, or any situation where you need to secure a deal quickly.

- SBA 504 and 7(a) Loans: While commonly associated with owner-occupied businesses, these government-backed loans can sometimes be used for investment properties, particularly if your business will occupy a significant portion of the space. They often feature favorable terms, such as lower down payments and longer repayment periods.

Practical Scenarios in Action

Let’s translate theory into practice. Seeing how these loans are applied in real-world situations clarifies which tool is appropriate for which job.

Scenario 1: The Stabilized Office Building

An investor wishes to purchase a fully leased, Class A office building with strong, long-term tenants. The goal is straightforward: collect steady, predictable cash flow over the next decade.

- Best Fit: A traditional commercial mortgage. The property’s stable income stream makes it a low-risk investment for a conventional lender. The investor can secure a 10-year fixed-rate loan, ensuring predictable payments and a solid return. The lender's confidence is built on the property's health, documented in its rent roll. To see why this document is so vital, you can learn more about what a rent roll is and why it's crucial for underwriting.

Scenario 2: The Value-Add Multifamily Complex

A real estate group identifies an older 50-unit apartment building in a gentrifying neighborhood. The property is dated, and rents are significantly below market rate. Their plan is to renovate each unit, upgrade common areas, and increase rents by 30% over the next 18 months.

- Best Fit: A bridge loan. In its current state, the property does not generate enough income to qualify for a traditional mortgage. A bridge loan provides the necessary capital for both the acquisition and the renovation. Once the improvements are complete and the building is stabilized with higher rental income, the group can refinance into a long-term, traditional commercial mortgage.

Choosing the right commercial financing is less about finding the lowest rate and more about finding the most strategic partner. The loan's structure—its term, flexibility, and covenants—must align perfectly with your business plan for the asset. A mismatch can create significant financial friction and hinder your investment's success.

How Lenders Evaluate Your Commercial Loan Application

Obtaining a commercial loan for an investment property is not about pitching a great idea; it's about presenting a meticulously documented business case. Lenders are essentially becoming your financial partners. They are putting their capital at risk and need to scrutinize every detail to ensure the deal is sound.

The key to approval is understanding their perspective. Lenders evaluate your application through a specific lens, focusing on five core pillars of underwriting. This process is a comprehensive health check for both you and the property. They must be confident that the asset can cover its own debt and that you, the investor, have the expertise to manage it effectively.

The Five Pillars of Commercial Underwriting

Lenders do not make decisions based on intuition. They follow a structured, time-tested process that balances financial metrics, your experience, and the quality of the asset itself. Each pillar provides a crucial piece of the puzzle, creating a complete picture of the investment’s viability.

Here are the critical components they analyze:

- Debt Service Coverage Ratio (DSCR): This is arguably the most important metric. It measures the property's ability to cover its mortgage payments using its Net Operating Income (NOI). A DSCR of 1.0x means the property is breaking even, which is insufficient. Lenders require a buffer, typically looking for a DSCR of 1.25x or higher.

- The Borrower's Financial Strength: Lenders will conduct a thorough review of your personal financial health. This includes your credit score, personal financial statements, and available liquid assets. They need assurance that you are a responsible operator who can handle unexpected vacancies or major repairs without defaulting.

- Real Estate Experience: Your track record matters significantly. Lenders want to see a history of successfully owning and managing similar properties. A well-documented portfolio of profitable real estate investments instantly enhances your credibility and makes them more comfortable with the deal.

- Loan-to-Value (LTV): This ratio compares the loan amount to the property's appraised value. For commercial real estate, lenders are more conservative and require more "skin in the game" from the borrower. This translates to a larger down payment, typically in the 25% to 35% range.

- Property Condition and Appraisal: An independent appraiser will evaluate the building's physical condition, location, and market value. A well-maintained property in a prime location with a strong tenant history will always receive a more favorable assessment. If you want to dive deeper into this, our guide on how to value commercial real estate breaks it all down.

Crafting a Winning Loan Package

Your loan application is your formal pitch. A disorganized or incomplete package raises immediate red flags, leading to delays or an outright rejection. A professional presentation signals that you are a serious, organized investor they can trust.

A strong loan package is more than just a collection of forms; it’s a compelling narrative that tells the story of the investment. It should clearly and concisely present the opportunity, supported by robust financial data.

The current lending environment is quite active. Commercial and multifamily mortgage originations saw a 66% surge in the second quarter compared to the previous year, demonstrating a renewed appetite from lenders. This trend was fueled by growth across various property types, including office, health care, and industrial sectors.

Key Documents Lenders Need to See

To streamline the process, begin gathering these essential documents well in advance. Having everything organized demonstrates professionalism and helps the underwriters move your file forward much faster.

- Executive Summary: A concise, one-page overview of the deal, including the property details, your business plan, and the loan you are requesting.

- Property Financials: At least three years of historical operating statements (profit and loss) and a current rent roll.

- Personal Financial Statement: A detailed breakdown of your personal assets and liabilities.

- Real Estate Portfolio Summary: A schedule of all real estate you currently own, showing the purchase price, current value, debt, and cash flow.

- Purchase and Sale Agreement: The fully executed contract for the property you are acquiring.

By viewing your application through the lender's eyes, you can anticipate their questions and proactively provide the necessary documentation. A well-prepared package doesn't just meet the requirements—it builds confidence and sets the stage for a smooth and successful closing.

Decoding Commercial Loan Rates and Terms

To succeed in commercial real estate, you must become fluent in the financial architecture of the deal. Commercial loans are not like the straightforward 30-year fixed mortgages on residential homes. They feature more complex structures and clauses that can dramatically impact your cash flow and overall profitability. Understanding these financial levers allows you to negotiate from a position of strength and secure terms that align with your investment goals.

The interest rate is often the main focus, but it's merely the starting point. When it comes to commercial loans, you'll generally encounter two main types: fixed-rate and variable-rate. Each serves a different strategic purpose, depending on your holding period and risk tolerance.

Fixed-Rate vs. Variable-Rate Loans

A fixed-rate loan locks in your interest rate for a predetermined period, typically 5, 7, or 10 years. This provides predictability, making it much easier to forecast expenses and cash flow. For investors with a long-term buy-and-hold strategy, this stability is invaluable as it insulates them from market fluctuations.

In contrast, a variable-rate loan (also known as an adjustable-rate mortgage or ARM) has an interest rate that changes over time. It is usually tied to a benchmark index, such as the prime rate. These loans may offer a lower initial rate, but they introduce significant risk—if the index rises, so will your monthly payment.

A core concept in commercial lending is the difference between the loan's term and its amortization period. Your loan might have a 10-year term, but the payments are calculated as if it's being paid off over 25 or 30 years. This mismatch is what creates a balloon payment down the road.

Understanding Key Loan Terminology

To fully comprehend the loan you're signing, you must look beyond the interest rate. Several other components are equally important, as they define the loan's true cost and flexibility. For any serious investor, mastering these terms is non-negotiable.

- Amortization Period: This is the total time over which your loan payments are calculated. A longer amortization period—for example, 30 years—results in lower monthly payments, but you will pay more in total interest over the life of the loan.

- Loan Term: This is the actual lifespan of the loan, or the period until the full balance is due. Commercial loan terms are much shorter than their amortization schedules, often lasting just 5 to 10 years.

- Balloon Payment: Because the term is shorter than the amortization, a large final payment—the "balloon"—is due when the term expires. At that point, you must either sell the property, pay off the balance with cash, or refinance into a new loan.

Critical Clauses Hiding in the Fine Print

Often, the most impactful provisions of a commercial loan agreement are buried in the details. Two clauses in particular can have massive financial consequences if you are not prepared for them: prepayment penalties and recourse provisions.

A prepayment penalty is a fee the lender charges if you decide to pay off your loan early. Lenders use these to guarantee a certain amount of interest income from the deal. This can be a significant obstacle if you plan to sell or refinance the property before the penalty period ends.

Another critical element is whether the loan is recourse or non-recourse. The difference is substantial.

- Recourse Loan: If you default on this type of loan, the lender can seize the property and pursue your personal assets to cover any remaining debt. This puts your entire personal net worth at risk.

- Non-Recourse Loan: With a non-recourse loan, the lender's only remedy in a default is to take possession of the property itself. Your personal assets are protected, providing a crucial layer of security.

Knowing the difference is vital for asset protection. By carefully decoding these rates and terms, you can structure a commercial loan for your investment property that not only gets the deal done but also supports your financial strategy for years to come.

Weighing the Pros and Cons of Commercial Financing

Using a commercial loan for an investment property can be an incredibly powerful strategy for building wealth. It allows you to acquire larger, more profitable assets than you could with cash alone—a method known as leverage. This is how sophisticated investors amplify their potential returns.

However, this strategy is a double-edged sword that introduces significant risks.

Understanding both sides of this coin—the strategic advantages and the potential pitfalls—is absolutely essential before committing. This isn't just about securing capital; it’s about ensuring the loan structure aligns with your long-term financial health and protects the portfolio you’ve worked hard to build. A prudent decision requires a balanced, clear-eyed view.

The Strategic Advantages of Commercial Loans

The primary benefit of using a commercial loan is the ability to scale your real estate portfolio faster and more substantially. With leverage, you can control a million-dollar asset with only a fraction of that in your own cash, freeing up capital for other investments or opportunities.

Beyond pure growth, many savvy investors also find that leverage can be an effective asset protection strategy. By financing properties through a legal entity like an LLC, you can create a clear separation between your business and personal assets, shielding your personal wealth from liabilities tied to a specific property. If you're considering this approach, you might find our guide on buying real estate in an IRA helpful for more advanced strategies.

Key upsides include:

- Amplified Returns: Leverage can significantly boost your return on investment (ROI). If a property's value increases, the gains are calculated on its total value, not just your initial down payment.

- Portfolio Diversification: Financing allows you to spread your capital across multiple properties or asset types instead of concentrating it all in a single, large cash purchase.

- Access to Larger Assets: Commercial loans open the door to acquiring high-value properties like apartment complexes or office buildings that offer greater income potential.

Potential Pitfalls and Market Risks

While the benefits are compelling, the risks associated with commercial financing are equally real. These are business debts, and lenders are far less forgiving than in the residential market. Defaulting can have severe consequences, especially if your loan includes a personal guarantee.

The structure of commercial loans also introduces unique challenges. They often have shorter terms, typically 5-10 years, which conclude with a large balloon payment. This requires you to either sell the property or refinance—a task that can be incredibly difficult in a tight credit market or an economic downturn.

The current lending environment presents a notable challenge for commercial real estate. With nearly $957 billion in loans maturing, the pressure to refinance is immense, representing almost triple the 20-year average. This "refinancing wall" is a major risk, especially as delinquency rates for commercial mortgage-backed securities (CMBS) have climbed to 7.29%. Discover more insights about the challenges in commercial real estate on kaplancollectionagency.com.

Key downsides to keep in mind:

- Higher Costs and Fees: Commercial loans almost always come with higher interest rates, origination fees, and appraisal costs compared to residential mortgages.

- Interest Rate Volatility: If you have a variable-rate loan, a sudden spike in interest rates can dramatically increase your monthly payments, quickly eroding your property's cash flow.

- Personal Liability: Many commercial loans require a personal guarantee, which puts your personal assets on the line if the property fails to perform and you default on the loan.

To help you weigh your options, we've compiled a table summarizing the key advantages and disadvantages of using a commercial loan for your next investment.

Weighing Your Options The Pros and Cons of Commercial Loans

Ultimately, a commercial loan is a tool. In the right hands and with a sound strategy, it can accelerate wealth creation like nothing else. But without a full understanding of the risks, it can just as easily become a liability. The key is to approach it with a clear strategy and a healthy respect for both sides of the equation.

Common Questions About Investment Property Loans

Navigating the world of commercial real estate financing can feel like learning a new language. However, you’ll find that most investors, whether they are on their first deal or their fiftieth, encounter the same fundamental questions. Obtaining clear answers is the key to moving forward with confidence.

Consider this section your essential FAQ. We will address the most common questions about commercial loans for investment property, providing the practical insights you need before you begin speaking with lenders. Having this information helps you set realistic expectations and build a smarter financing strategy from the outset.

What Is a Typical Down Payment for a Commercial Property Loan?

This is one of the most significant adjustments for investors transitioning from the residential market. Lenders view commercial properties as business assets, so they require you to have more "skin in the game." A larger down payment demonstrates your commitment and provides the bank with a greater equity cushion from day one.

While the exact amount can vary based on the property type, the lender, and your financial standing, the standard range is typically 25% to 35% of the purchase price. For riskier property types or for borrowers with less experience, this figure can be higher.

How Long Does the Commercial Loan Closing Process Take?

Prepare for a much longer and more involved timeline compared to a residential mortgage. The additional time is due to the lender's in-depth underwriting process. They will scrutinize everything from a detailed property appraisal and environmental assessments to the property's historical financial performance.

On average, you can expect the entire process to take anywhere from 45 to 90 days, from submitting a complete loan package to closing. Several factors can influence this timeline:

- Lender Efficiency: Some lenders are simply more organized and efficient than others.

- Application Completeness: A well-prepared loan package with all necessary documents will move through underwriting smoothly. An incomplete one will get bogged down in requests for more information.

- Third-Party Reports: Delays with the appraiser or environmental consultant can easily add weeks to your closing date.

What Is the Difference Between Recourse and Non-Recourse Loans?

This is one of the most critical distinctions in commercial lending, as it directly impacts your personal financial risk. The difference boils down to a single question: if you default, what assets can the lender pursue?

A recourse loan grants the lender the right to seize the investment property and pursue your other personal assets to satisfy the debt. This means your home, savings, and other investments could all be at risk.

A non-recourse loan, on the other hand, limits the lender's claim to the collateral itself—the investment property. If you default, they can take the property, but their claim ends there. They cannot touch your personal assets. This provides a vital layer of protection for you as an investor, creating a firewall between the property's risk and your personal wealth.

Naturally, non-recourse loans are highly sought after. Because they present less risk for the borrower, they are typically harder to qualify for and may come with slightly higher interest rates, but for many investors, the peace of mind is well worth the trade-off.

At Commons Capital, we specialize in helping high-net-worth investors navigate the complexities of real estate financing and wealth management. If you're looking to build a robust real estate portfolio, our team can provide the expert guidance needed to structure deals that align with your long-term financial objectives.

Explore how our advisory services can support your investment journey at https://www.commonsllc.com.