As a business owner, your focus is on growth and innovation, but overlooking your tax obligations can significantly erode your bottom line. Effective tax planning is not merely about compliance; it is a powerful financial tool for maximizing profitability and enhancing cash flow. This guide explores essential tax strategies for business owners, designed to move you from a reactive to a proactive mindset. By understanding and implementing these sophisticated yet actionable approaches, you can transform your tax burden into a strategic advantage, freeing up capital to reinvest in your business, your team, and your long-term financial goals.

We will delve into 10 specific strategies, from optimizing your business structure to leveraging advanced retirement and depreciation tactics. These insights provide a clear roadmap to a more tax-efficient future. For entrepreneurs operating on a global scale, grasping diverse tax frameworks is crucial. For example, understanding the process for UAE corporate tax registration can offer valuable insights for international business planning and compliance. This article will equip you with the knowledge to make informed decisions, minimize your liabilities, and keep more of your hard-earned revenue working for you.

1. Business Entity Structure Optimization

One of the most foundational tax strategies for business owners is rooted in the legal structure of the company itself. Your choice of entity, whether an LLC, S-Corporation, C-Corporation, or Partnership, directly dictates how profits are taxed, your personal liability, and your ability to attract investment. This is not a one-time decision but a strategic choice that should be re-evaluated as your business grows and evolves.

How Entity Choice Impacts Your Tax Bill

Different structures carry vastly different tax implications. A sole proprietorship offers simplicity but exposes you to high self-employment taxes on all net income. An S-Corp, however, allows you to pay yourself a "reasonable salary" subject to self-employment taxes, while remaining profits can be distributed as dividends, which are not. This single change can result in substantial savings. For instance, a consultant earning $150,000 in net income could save over $8,000 annually in self-employment taxes by converting from a sole proprietorship to an S-Corp and establishing a reasonable salary.

Key to optimizing your tax position from the outset is careful consideration of your business entity. For further guidance, explore resources on choosing the right business structure to understand the nuances that may apply to your specific situation.

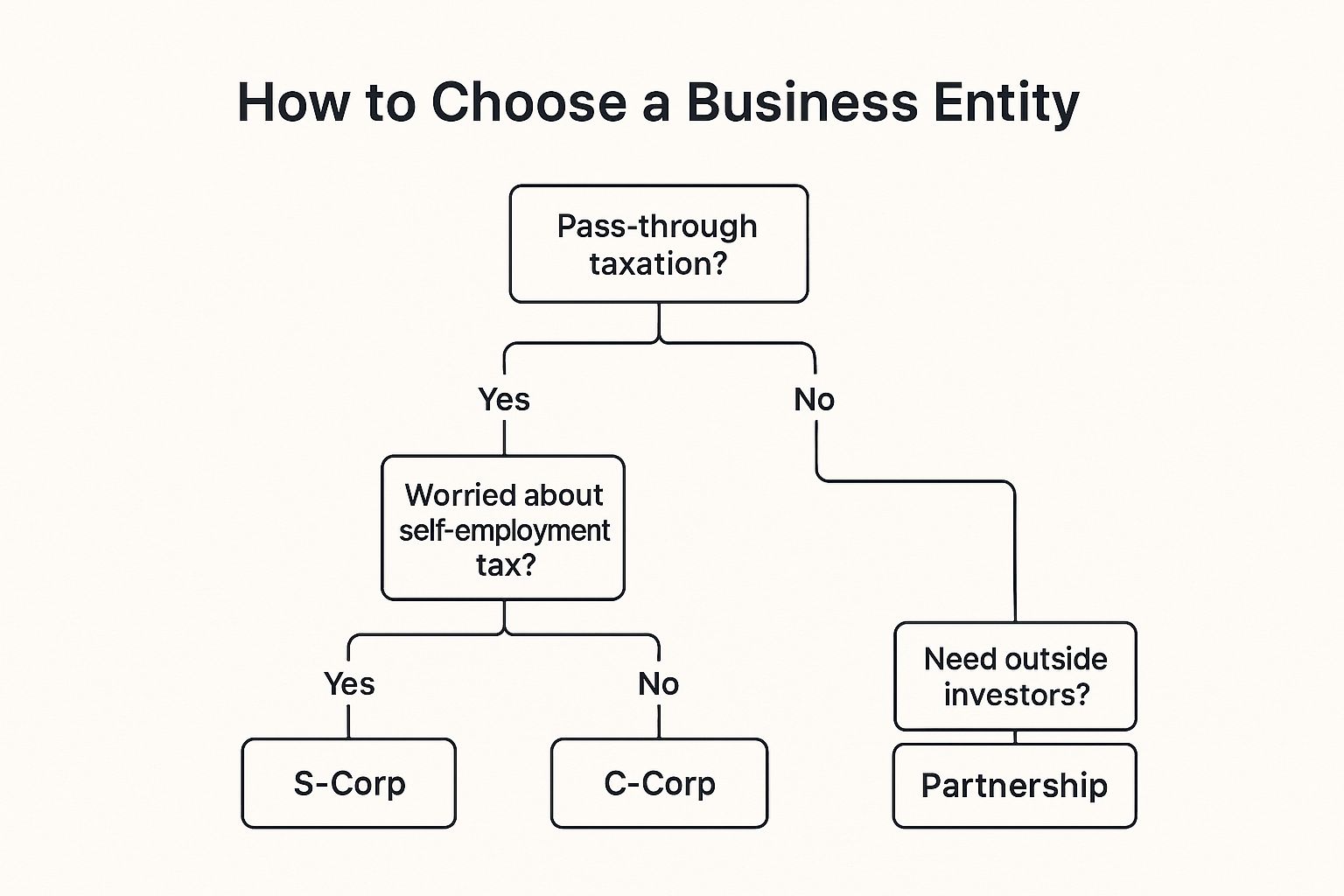

The decision tree below simplifies the initial thought process based on key priorities like taxation and investor needs.

This visual guide highlights that your approach to taxation (pass-through vs. corporate) and your need for external capital are primary drivers in selecting the most advantageous entity.

Actionable Tips for Optimization:

- Evaluate Self-Employment Taxes: If your business generates significant profit, compare the tax burden of a pass-through entity like an LLC with the potential savings of an S-Corp election.

- Plan for Growth: If you anticipate seeking venture capital, a C-Corporation is often the preferred structure for investors due to its favorable stock options and straightforward ownership model.

- Consult Professionals: This decision has significant legal and financial consequences. Always consult with both a tax advisor and a corporate attorney to align your structure with your long-term goals.

- Annual Review: Treat your entity choice as a dynamic part of your business plan. A structure that works today may not be optimal in three years.

2. Section 199A Qualified Business Income (QBI) Deduction

One of the most impactful tax strategies for business owners is leveraging the Section 199A Qualified Business Income (QBI) deduction. Introduced by the Tax Cuts and Jobs Act, this provision allows eligible owners of pass-through entities like LLCs, S-Corporations, and partnerships to deduct up to 20% of their qualified business income. This directly reduces your taxable income, lowering your effective tax rate without complex restructuring.

How the QBI Deduction Impacts Your Tax Bill

The QBI deduction can create significant tax savings by shielding a portion of your business profits from taxation. For a manufacturing business owner with $150,000 in qualified income, this could mean a $30,000 deduction, saving them over $7,000 in federal income tax, depending on their tax bracket. However, the rules can be complex. The deduction may be limited based on your taxable income, the W-2 wages paid by your business, and the cost of qualified property it holds.

It is particularly important for owners of a Specified Service Trade or Business (SSTB), such as consultants or doctors, to monitor their income levels. As their income surpasses certain thresholds, their ability to take the deduction is phased out. Understanding these limitations is a critical component of maximizing this powerful tax strategy. For a deeper dive into the specifics, the IRS provides detailed guidance on the QBI deduction.

Actionable Tips for Optimization:

- Segregate Income Streams: Meticulously track your qualified business income separately from investment income or wages to ensure an accurate calculation.

- Manage Income Thresholds: If you operate an SSTB, consider strategies like deferring income or accelerating expenses to stay below the income phase-out thresholds.

- Maximize W-2 Wages: For businesses subject to wage limitations, strategically increasing W-2 wages paid to employees (or yourself, in an S-Corp) can increase your potential QBI deduction.

- Acquire Qualified Property: If your deduction is limited, acquiring new business property can increase the unadjusted basis immediately after acquisition (UBIA) of qualified property, potentially boosting your deduction amount.

3. Strategic Business Expense Deductions

One of the most direct tax strategies for business owners involves maximizing legitimate business deductions. The IRS allows you to deduct expenses that are both "ordinary and necessary" for your trade or business. Diligent tracking and categorization of these costs, from vehicle mileage to professional development, can significantly reduce your taxable income, directly lowering your final tax liability.

How Deductions Impact Your Tax Bill

Every dollar you deduct as a business expense is a dollar removed from your taxable income. This strategy is not about finding loopholes but about ensuring you claim every legitimate deduction you are entitled to. For example, a sales professional who meticulously logs their vehicle use for client visits could deduct over $15,000 annually. Similarly, a consultant who dedicates a specific area of their home exclusively for business can claim a home office deduction, potentially saving thousands each year on mortgage interest, utilities, and insurance.

The key to successful deduction is meticulous record-keeping. Proper documentation substantiates your claims in the event of an audit and ensures you don't miss out on valuable savings. This proactive approach turns everyday operational costs into powerful tools for tax reduction.

Actionable Tips for Optimization:

- Leverage Technology: Use dedicated expense tracking apps or accounting software to capture receipts and categorize expenses in real-time, ensuring nothing is overlooked.

- Separate Business and Personal: Maintain separate bank accounts and credit cards for business activities. For mixed-use assets like a vehicle or phone, keep detailed logs to clearly distinguish business from personal use.

- Time Large Purchases: Consider making significant equipment or software purchases before the end of the year to accelerate deductions and lower the current year's tax bill.

- Conduct Monthly Reviews: Don't wait until tax season. Review your expenses monthly to ensure accurate categorization and identify potential new deductions, such as professional subscriptions or industry-specific software.

4. Retirement Plan Maximization

One of the most potent tax strategies for business owners involves leveraging company-sponsored retirement plans. Unlike standard employee plans, options available to entrepreneurs like a SEP-IRA, Solo 401(k), or a defined benefit plan offer significantly higher contribution limits. This allows you to aggressively save for the future while substantially reducing your current taxable income, creating a powerful dual benefit.

This approach is not just about saving; it's a direct and immediate way to lower your tax liability. These contributions are made pre-tax, meaning every dollar you put into the plan is a dollar removed from your business's taxable profit for the year.

How Retirement Plans Lower Your Tax Bill

The primary advantage for business owners is the scale of the tax deduction. While an employee might be limited to a standard 401(k) contribution, a business owner can often contribute much more. For example, a freelance consultant operating as a sole proprietor could contribute up to $69,000 to a Solo 401(k) in 2024. If they are in the 24% tax bracket, this single action could generate an immediate federal tax saving of $16,560.

To truly maximize your retirement plan, consider exploring advanced strategies like understanding how maximizing your retirement income with 72t SEPP can help, especially if you plan for early access. These strategies are particularly impactful for high-income earners looking to optimize their long-term financial health. Learn more about the best tax strategies for high-income earners on commonsllc.com to further enhance your financial plan.

Actionable Tips for Optimization:

- Choose the Right Plan: Evaluate a Solo 401(k) for its high contribution limits and loan options if you have no employees. A SEP-IRA is simpler to administer and is great for businesses with variable income.

- Meet Key Deadlines: You must establish most plans by December 31st of the tax year, but you often have until your tax filing deadline (including extensions) to make contributions.

- Consider Roth Options: If your plan allows it, making Roth contributions means you pay taxes now but get tax-free withdrawals in retirement, providing valuable tax diversification.

- Review Annually: As your business income and goals change, the best retirement plan for you may also change. Reassess your strategy each year to ensure it remains optimal.

5. Equipment and Asset Depreciation Strategies

One of the most impactful tax strategies for business owners involves how you handle the cost of equipment and other business assets. Instead of slowly deducting the cost over several years, depreciation strategies allow you to accelerate these deductions, significantly reducing your taxable income in the year of purchase. Methods like Section 179 expensing and bonus depreciation are powerful tools for managing cash flow and lowering your tax liability.

How Depreciation Choices Impact Your Tax Bill

Strategic depreciation allows you to time your largest deductions to offset high-income years. For example, a restaurant purchasing $80,000 in new kitchen equipment could potentially use Section 179 to deduct the entire amount in the first year, rather than a small fraction. Similarly, a construction company buying a $200,000 excavator could use 80% bonus depreciation (for 2023) to immediately write off $160,000. This immediate deduction provides a substantial tax savings that directly improves the company's cash position, freeing up capital for other investments.

These methods essentially pull future tax deductions into the present, providing an immediate financial benefit. For more details on the specific rules, the IRS offers comprehensive guidance on depreciation methods.

Actionable Tips for Optimization:

- Plan Major Purchases: Align significant capital expenditures with years you anticipate higher-than-average income to maximize the tax-shielding effect of accelerated depreciation.

- Coordinate Elections: Work with a tax professional to decide between Section 179, bonus depreciation, or traditional depreciation, as each has different limitations and long-term implications for your tax strategy.

- Maintain Meticulous Records: Document the purchase date, cost, and percentage of business use for every asset. This is crucial for substantiating your deductions in the event of an audit.

- Time Asset Sales: Be mindful of depreciation recapture rules. Selling a depreciated asset can trigger a taxable gain, so timing the disposition strategically is key to managing your overall tax liability.

6. Income Timing and Recognition Strategies

A powerful yet often overlooked strategy involves controlling when your business recognizes income and deducts expenses. This tactic, known as income timing, allows you to shift financial events between tax years to your advantage. By understanding the difference between cash and accrual accounting methods, you can legally manage your tax liability, smoothing out income fluctuations and deferring taxes to years when your rates may be lower.

How Timing Impacts Your Tax Bill

The core principle is simple: accelerate deductions into the current, higher-income year and defer income into a future, potentially lower-income year. For a service-based business using cash-basis accounting, this could mean delaying a December invoice until January, pushing that revenue into the next tax year. Similarly, a retailer could prepay January rent or purchase office supplies in December to accelerate those deductions, reducing the current year's taxable income. An installment sale on a large asset can also spread the tax gain over several years instead of taking the hit all at once.

This level of control is crucial for managing cash flow and minimizing your overall tax burden across multiple years, making it one of the most flexible tax strategies for business owners.

Actionable Tips for Optimization:

- Monitor Year-End Projections: As the year closes, analyze your projected income and tax bracket. This data will inform whether it’s better to accelerate or defer income and expenses.

- Prepay Deductible Expenses: Identify recurring expenses for the upcoming year, such as insurance premiums, rent, or professional subscriptions, and consider paying them before year-end to claim the deduction now.

- Manage Accounts Receivable: If you use cash-basis accounting, strategically manage your invoicing and collections at the end of the year to control when revenue is officially received.

- Coordinate with Personal Finances: Align your business income timing with other household income sources to get a complete picture of your tax situation and avoid accidentally pushing yourself into a higher bracket.

7. Family Employment and Income Splitting

One of the most effective yet personal tax strategies for business owners involves employing family members. This approach allows you to legitimately shift business income to family members, often children or a spouse, who are in a lower personal tax bracket. The wages paid are a deductible business expense for you, while the family member pays tax at their lower rate, reducing the overall tax liability for the entire family unit.

How Family Employment Impacts Your Tax Bill

This strategy creates a powerful win-win scenario. It provides a genuine business deduction, funds college savings or retirement accounts for your loved ones, and offers them valuable work experience. For example, a photographer in the 35% tax bracket could hire their teenage child to manage social media for $12,000 a year. The business gets a $12,000 deduction, saving $4,200 in taxes. The child, likely in a 10-12% bracket, pays far less tax on that income, resulting in significant net savings for the family.

This method transforms a personal family expense, like an allowance or college savings contribution, into a tax-deductible business expense. It's a strategic way to keep wealth within the family while meeting legitimate business needs.

Actionable Tips for Optimization:

- Ensure Legitimacy: The work performed must be ordinary and necessary for the business. Document everything with a clear job description, signed employment agreement, and detailed time records.

- Pay a Reasonable Wage: The compensation must be comparable to what you would pay a non-family member for the same role and skills. Overpaying can trigger an IRS audit.

- Follow Payroll Rules: Treat your family member like any other employee. Use a payroll service to handle withholdings, file the necessary forms (like W-2s), and maintain compliance.

- Fund Retirement Accounts: This is an excellent opportunity to start a Roth IRA for a child. Their earned income makes them eligible, allowing them to begin tax-free growth for retirement decades in advance.

8. Health Insurance and Medical Expense Optimization

Beyond standard business deductions, optimizing how you handle health-related expenses offers a significant opportunity for tax savings. For self-employed individuals and small business owners, structuring health insurance premiums and medical costs correctly can convert personal expenses into powerful business deductions. This strategy involves leveraging specific accounts and deductions designed to lower your taxable income while providing essential health coverage.

How Health Expense Strategies Impact Your Tax Bill

The right approach can generate substantial tax benefits. The self-employed health insurance deduction, for instance, allows sole proprietors and partners to deduct 100% of their health insurance premiums. Another powerful tool is the Health Savings Account (HSA), which provides a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For a business owner in a high tax bracket, maximizing a family HSA contribution of $8,300 (2024 limit) could translate into over $3,000 in combined federal and state tax savings, while also building a tax-free investment account for future medical needs.

These tax strategies for business owners turn a necessary cost into a valuable financial tool, reducing both income and self-employment tax liabilities.

Actionable Tips for Optimization:

- Combine an HDHP with an HSA: Pair a high-deductible health plan (HDHP) with a Health Savings Account. This allows you to pay for current medical expenses with pre-tax dollars and invest the remaining funds for tax-free growth.

- Maximize HSA Contributions: Contribute the maximum allowed amount to your HSA annually. Consider paying for smaller medical expenses out-of-pocket to allow your HSA funds to grow as a long-term, tax-free retirement vehicle for healthcare.

- Deduct Premiums Correctly: If you are self-employed, ensure you are taking the self-employed health insurance deduction. This is an "above-the-line" deduction, meaning it reduces your adjusted gross income (AGI) directly.

- Explore Health Reimbursement Arrangements (HRAs): Small businesses can implement HRAs like the Qualified Small Employer HRA (QSEHRA) to reimburse employees tax-free for their medical expenses, creating a valuable employee benefit and a business deduction.

9. Business Loss Utilization and Carryforward Strategies

A business loss is never the goal, but when it occurs, it can become a powerful financial tool. One of the most critical tax strategies for business owners involves strategically managing these losses to offset other income and optimize tax benefits across multiple years. Understanding how to utilize net operating losses (NOLs) can turn a difficult year into a significant tax-saving opportunity for future periods.

How Loss Utilization Impacts Your Tax Bill

Properly managed, a business loss isn't just a number on a P&L statement; it's a valuable asset that can reduce your tax liability. For instance, a new restaurant might incur a $50,000 loss in its first year. This loss could potentially offset a spouse's W-2 income on a joint return, generating a substantial immediate tax refund. The key is navigating complex regulations like passive activity loss rules and at-risk limitations, which determine how and when you can claim these deductions.

The rules governing loss carryforwards are also crucial. For most businesses, NOLs generated can be carried forward indefinitely to offset up to 80% of taxable income in future years, providing a long-term benefit. For more details on this topic, you can read about various tax loss harvesting strategies to better understand how these rules apply.

Actionable Tips for Optimization:

- Understand Material Participation: Determine if your involvement in the business qualifies as "material participation." This dictates whether a loss is active, and thus deductible against other income, or passive, which has stricter limitations.

- Track Your At-Risk Basis: You can only deduct losses up to the amount you have "at risk" in the business, which includes your cash contributions and certain loans. Meticulous tracking is essential.

- Time Loss Recognition: When possible, time the recognition of certain expenses or asset sales to align losses with high-income years, thereby maximizing their tax-saving impact.

- Coordinate with Other Strategies: Ensure your loss utilization plan works in concert with other tax strategies, such as retirement contributions and capital gains planning, for a cohesive and effective financial approach.

10. Estate and Succession Tax Planning

Effective tax strategies for business owners must extend beyond annual income tax to encompass long-term wealth preservation. Estate and succession planning is a critical component that ensures the value you build is transferred efficiently to the next generation or successor, minimizing potential tax burdens that could jeopardize the company's future. This long-term approach protects business assets from significant erosion by estate taxes while providing a smooth transition.

How Succession Planning Impacts Your Tax Bill

Without a plan, a business owner's death can trigger substantial estate taxes, forcing heirs to sell company assets or even the entire business just to pay the bill. Strategic planning utilizes tools like gifting, valuation discounts, and trusts to transfer ownership gradually and tax-efficiently. For example, a family business owner can gift minority interests annually to their children. These interests often qualify for valuation discounts for lack of control and marketability, allowing more value to be transferred tax-free. A tech entrepreneur could use a Grantor Retained Annuity Trust (GRAT) to pass on high-growth shares to heirs while minimizing gift tax exposure.

Careful planning is essential for preserving your legacy. For a deeper understanding of the techniques involved, you can learn more about estate planning for high-net-worth individuals on commonsllc.com to explore advanced strategies.

Actionable Tips for Optimization:

- Start Planning Early: Begin succession planning when business valuations are lower to maximize the value you can transfer under gift and estate tax exemptions.

- Utilize Gifting and Discounts: Work with an appraiser to establish defensible valuation discounts for minority stakes, gifting portions of your business annually to family members.

- Implement Buy-Sell Agreements: Establish a clear buy-sell agreement funded with life insurance to provide liquidity for estate taxes and ensure a smooth transition of ownership upon death or retirement.

- Leverage Trusts: Use trusts, such as GRATs or Irrevocable Life Insurance Trusts (ILITs), to move assets out of your taxable estate, providing control and significant tax advantages.

Top 10 Tax Strategy Comparison for Business Owners

Integrating Your Tax Strategy for Long-Term Success

Navigating the complexities of the tax code is not merely an annual obligation; it is a strategic imperative for any serious entrepreneur. Throughout this article, we’ve explored a range of powerful tax strategies for business owners, from optimizing your entity structure and maximizing the Section 199A QBI deduction to leveraging retirement plans and strategically timing income and expenses. Each of these tactics, whether it’s accelerating depreciation on new assets or employing family members, represents a distinct opportunity to reduce your tax burden and retain more of your hard-earned capital.

However, the greatest value is unlocked not by applying these strategies in isolation, but by weaving them into a cohesive and dynamic financial framework. Think of your tax plan as an integrated system, where decisions about equipment purchases (depreciation), retirement contributions, and succession planning are interconnected. A choice in one area has ripple effects across your entire financial picture, influencing both your current tax liability and your long-term wealth accumulation. This holistic approach transforms tax planning from a defensive, reactive chore into a proactive tool for growth.

Key Takeaways for Proactive Tax Management

To truly master this discipline, remember these core principles:

- Tax Planning is Year-Round: The most effective strategies are implemented long before the tax deadline. Consistent, proactive planning throughout the year allows you to make informed decisions when opportunities arise, rather than scrambling to find deductions in the final quarter.

- Documentation is Your Defense: Meticulous record-keeping is non-negotiable. Whether tracking business expenses, justifying deductions, or documenting income-splitting arrangements with family, clear and organized records are your best defense in an audit and the foundation of a sound strategy.

- Adaptability is Essential: The tax code is not static. Laws change, business circumstances evolve, and personal financial goals shift. Your tax strategy must be flexible enough to adapt to these changes, requiring regular reviews and adjustments with your financial team.

Your Actionable Next Steps

Mastering the concepts we've discussed is the first step. The next is implementation. Begin by conducting a comprehensive review of your current financial situation. Identify which of these tax strategies for business owners you are currently using and, more importantly, which ones you are not. Assess your business structure, evaluate your retirement contributions, and analyze your expense-tracking procedures. This self-audit will reveal immediate opportunities for optimization.

Ultimately, integrating these sophisticated strategies requires specialized expertise. The difference between a good tax outcome and a great one often lies in the nuanced application of these rules to your unique situation. By embracing a strategic, forward-looking approach to tax management, you are not just saving money; you are building a more resilient, profitable, and valuable enterprise for the future.

Ready to build a truly integrated financial plan that aligns your business growth with sophisticated tax-saving strategies? The team at Commons Capital specializes in providing comprehensive financial advisory services tailored to the unique needs of business owners, high-net-worth families, and investors. Schedule a consultation with us today to see how our expertise can help you optimize your financial future.