Welcome to our in-depth guide on sophisticated tax loss harvesting strategies, a critical tool for any high-net-worth investor looking to enhance after-tax returns. While the core concept of selling losing investments to offset gains is widely understood, its true power is unlocked through nuanced, advanced techniques. Market volatility, in particular, creates unique opportunities to strategically manage tax liabilities and improve your financial position.

This article moves far beyond the basics. We provide a detailed roundup of seven powerful and distinct tax loss harvesting strategies designed for serious investors. Each section offers actionable insights, practical implementation examples, and specific tips tailored for those managing significant assets. You will learn not just what each strategy is, but how and when to apply it effectively within your broader investment framework.

We will explore everything from direct and systematic harvesting to more complex approaches involving ETFs, options, and multi-account coordination. Whether you prefer a hands-on method or seek an automated solution, these strategies will provide the knowledge needed to make more informed and tax-efficient decisions. Discover how to transform market downturns and unrealized losses into a tangible financial advantage that helps preserve and compound your wealth for the long term.

1. Direct Tax Loss Harvesting

Direct tax loss harvesting is the foundational strategy in this field and the most straightforward to execute. It involves the direct sale of an investment, such as a stock, mutual fund, or ETF, that is currently trading at a lower price than its purchase price (its cost basis). By selling the asset, you intentionally "realize" a capital loss, which can then be used on your tax return to offset capital gains and, in some cases, a portion of your ordinary income.

This approach is highly effective for its simplicity and direct impact. The core principle is to turn a market downturn into a tax-saving opportunity without significantly altering your long-term investment allocation. It's one of the primary tax loss harvesting strategies that investors use to enhance after-tax returns.

How It Works: A Practical Example

Imagine a high-net-worth investor purchased 500 shares of Tech Innovators Inc. (TII) at $200 per share for a total investment of $100,000. Later in the year, due to market volatility, the stock price drops to $150 per share, making the position worth $75,000.

To implement direct tax loss harvesting, the investor sells all 500 shares of TII. This action crystallizes a capital loss of $25,000 ($100,000 cost basis - $75,000 sale proceeds). This $25,000 loss can now be used to offset up to $25,000 in capital gains from other successful investments in the portfolio, potentially saving thousands in taxes.

Actionable Tips for Implementation

To execute this strategy effectively, precision is key. Follow these guidelines:

- Maintain Meticulous Records: Always track the cost basis for each security you own, including any reinvested dividends. Accurate records are essential for calculating the exact gain or loss.

- Time Your Sales: While you can harvest losses at any time, many investors focus on this near the end of the year when they have a clearer picture of their annual gains.

- Beware the Wash Sale Rule: The IRS's wash sale rule disallows a loss if you purchase a "substantially identical" security within 30 days before or after the sale. To maintain market exposure without violating this rule, you can reinvest the proceeds into a different but similar asset, such as an ETF that tracks the same sector but a different index.

- Factor in Costs: Always consider transaction fees or commissions associated with selling and buying securities, as these can slightly reduce the net benefit of the harvest.

Direct tax loss harvesting is a powerful tool for high-income earners looking to manage their tax liabilities proactively. To delve deeper into similar financial planning methods, explore these tax strategies for high income earners on commonsllc.com.

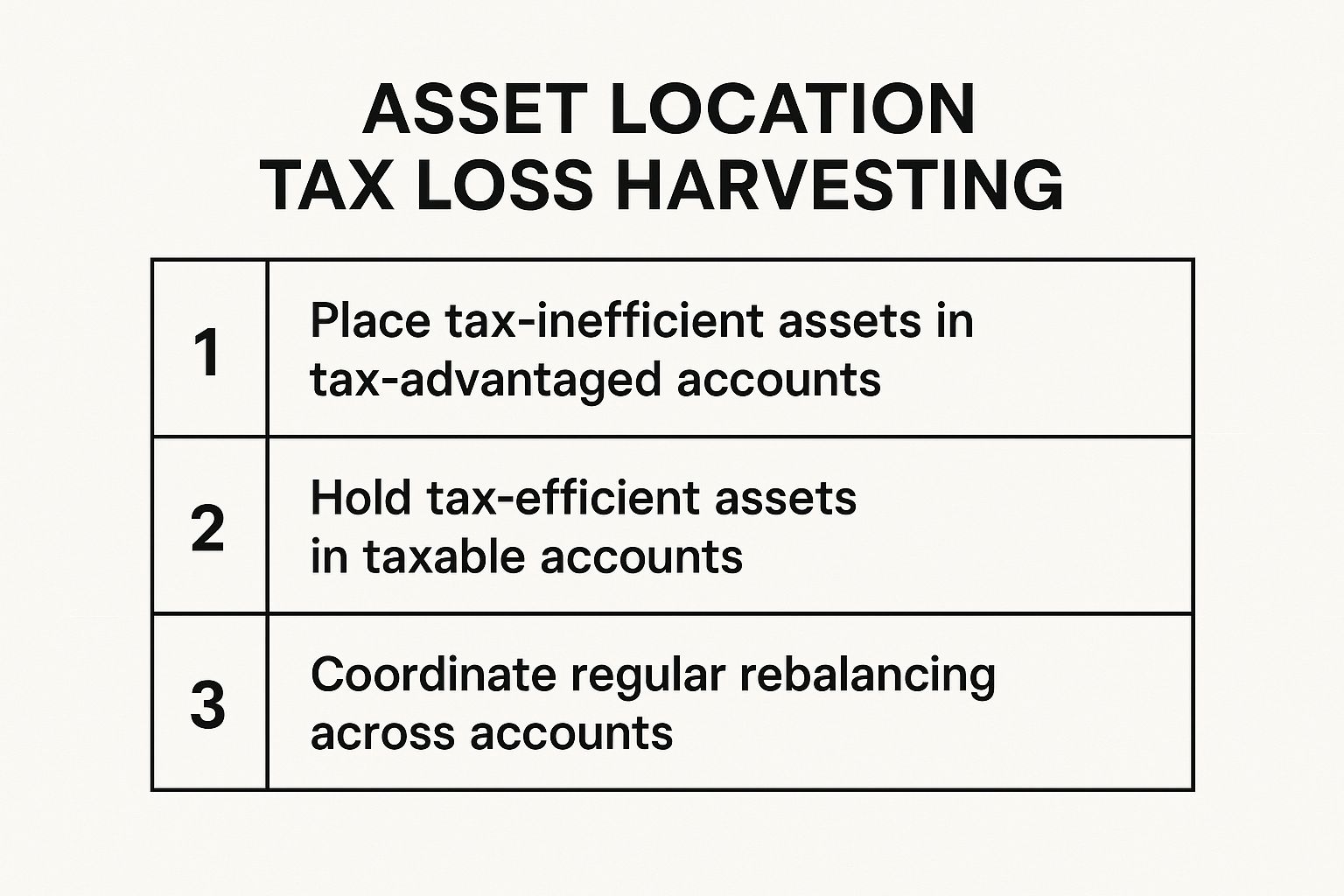

2. Asset Location Tax Loss Harvesting

Asset location is a sophisticated strategy that elevates tax loss harvesting by coordinating investments across different account types. It involves strategically placing assets in either taxable accounts (like a standard brokerage account) or tax-advantaged accounts (like a 401(k) or IRA) based on their tax efficiency. By doing so, you maximize long-term, after-tax returns and create more effective opportunities for harvesting losses.

This approach goes beyond individual security selection, focusing instead on the tax wrapper that holds the investment. The core principle is to shelter your most tax-inefficient assets from annual taxation, while keeping tax-efficient assets in taxable accounts where losses can be harvested. This makes it one of the most powerful tax loss harvesting strategies for investors with a mix of retirement and non-retirement accounts.

The following summary box provides a quick reference for the core principles of effective asset location.

These principles highlight how a holistic view of your portfolio is essential for optimizing tax outcomes.

How It Works: A Practical Example

Consider a high-net-worth investor who wants to allocate part of their portfolio to corporate bonds and another part to a broad-market equity ETF. Corporate bonds generate regular interest income, which is taxed at ordinary income rates, making them highly tax-inefficient. The equity ETF, conversely, primarily generates long-term capital gains (taxed at a lower rate) and qualified dividends.

With an asset location strategy, the investor would hold the corporate bonds inside their 401(k) or traditional IRA. In these accounts, the interest income grows tax-deferred, avoiding annual taxation. They would place the equity ETF in their taxable brokerage account. Here, its tax-efficient growth is preserved, and if the ETF's value declines, the investor can sell shares to harvest a capital loss and offset gains elsewhere.

Actionable Tips for Implementation

To properly execute an asset location strategy, a coordinated approach across your entire portfolio is necessary.

- Prioritize Tax-Inefficient Assets for Sheltering: Place investments that generate high annual income, like REITs, high-yield bonds, and actively managed funds with high turnover, inside your tax-advantaged retirement accounts.

- Keep Tax-Efficient Assets in Taxable Accounts: Growth stocks, index funds, ETFs, and municipal bonds are generally best suited for taxable accounts. This maximizes your ability to use tax loss harvesting strategies when market downturns occur.

- Rebalance Holistically: When rebalancing your portfolio, view all your accounts as one. If your stock allocation has grown too large, you might sell some winners in your taxable account while simultaneously buying more bonds within your IRA to maintain your target mix.

- Account for RMDs: For those approaching or in retirement, remember that traditional IRAs and 401(k)s have Required Minimum Distributions (RMDs). Plan for how these future withdrawals, taxed as ordinary income, fit into your long-term tax plan.

3. ETF Tax Loss harvesting with Similar Assets

ETF tax loss harvesting with similar assets is a sophisticated strategy that allows investors to realize a tax loss while maintaining continuous exposure to a specific market segment or asset class. This method involves selling a losing Exchange-Traded Fund (ETF) and immediately reinvesting the proceeds into a different but highly correlated ETF. By doing this, you capture a valuable tax deduction without sitting on the sidelines and risking a market rebound.

This technique is one of the most popular tax loss harvesting strategies used by automated robo-advisors and savvy financial professionals because it elegantly navigates the wash sale rule. The key is to select a replacement fund that is not "substantially identical" in the eyes of the IRS but still tracks the desired market exposure, ensuring your investment allocation remains intact.

How It Works: A Practical Example

Consider an investor who put $200,000 into the Vanguard Total Stock Market ETF (VTI). Following a broad market correction, the value of their position falls to $170,000. To harvest this loss without exiting the U.S. stock market, the investor decides to act.

They sell their entire VTI position, realizing a $30,000 capital loss. Immediately after, they use the $170,000 proceeds to purchase the SPDR Portfolio Total Stock Market ETF (SPTM). Since VTI tracks the CRSP US Total Market Index and SPTM tracks the S&P Total Market Index, they are not substantially identical. The investor successfully harvests a $30,000 loss to offset other gains while staying fully invested in the total U.S. stock market.

Actionable Tips for Implementation

Precision and research are vital for executing this strategy correctly and avoiding IRS scrutiny.

- Research ETF Correlation: Before making a switch, analyze the correlation between the old and new ETFs. The goal is a high correlation to maintain your investment thesis, but ensure they track different underlying indexes to avoid the wash sale rule.

- Compare Expense Ratios: When choosing a replacement ETF, pay close attention to its expense ratio. A seemingly small difference can impact your long-term returns, so aim for a fund with comparable or lower fees.

- Document Everything: Keep detailed records of the sale and subsequent purchase, including the date, amount, and the specific ETFs involved. This documentation is crucial for justifying your tax position if ever questioned.

- Use Limit Orders: When executing trades, especially with large sums, use limit orders instead of market orders. This gives you control over the execution price for both the sale and the purchase, preventing slippage in volatile markets.

This approach is a cornerstone of modern portfolio management. To understand how these techniques fit into a broader wealth strategy, explore the details of our investment management services on commonsllc.com.

4. Robo-Advisor Automated Tax Loss Harvesting

Robo-advisor automated tax loss harvesting leverages sophisticated algorithms to continuously monitor and optimize a portfolio for tax efficiency. This strategy automates the process of selling securities at a loss to offset capital gains, executing trades whenever opportunities arise without requiring manual intervention from the investor. It democratizes one of the more complex tax loss harvesting strategies by making it accessible and hands-off.

Platforms like Betterment and Wealthfront pioneered this approach, using technology to scan portfolios daily for potential harvesting opportunities. This constant vigilance allows for more frequent and potentially more effective loss harvesting than a typical once-a-year manual review, aiming to maximize after-tax returns while maintaining the investor's target asset allocation and risk profile.

How It Works: A Practical Example

Consider a high-net-worth individual with a $1 million portfolio managed by a robo-advisor like Wealthfront. The portfolio includes a position in an S&P 500 ETF. When the market experiences a minor dip, the algorithm identifies that this ETF is trading below its cost basis, creating a potential harvesting opportunity.

The system automatically sells the S&P 500 ETF to realize the capital loss. Almost instantly, it reinvests the proceeds into a "substantially different" but highly correlated replacement ETF, such as one tracking a different large-cap U.S. index. This action harvests the loss for tax purposes while keeping the portfolio's exposure to the U.S. large-cap market intact, all without violating the wash sale rule. The harvested loss is now available to offset gains elsewhere, a process that can repeat multiple times throughout the year.

Actionable Tips for Implementation

To effectively use automated tax loss harvesting, a strategic approach to platform selection and oversight is necessary.

- Compare Platform Fees and Features: Robo-advisors charge management fees, which can vary. Evaluate how a platform's fee structure (e.g., Betterment's percentage-based fee) compares to the potential tax savings it can generate for your specific portfolio size and activity.

- Understand the Algorithm: While the process is automated, it’s crucial to understand the logic. Review the platform's methodology for identifying losses, selecting replacement securities, and managing the wash sale rule.

- Review Your Tax Reports: At the end of the year, the robo-advisor will provide detailed tax documents (like Form 1099-B). Carefully review these reports with a tax professional to ensure the harvested losses are correctly reported on your tax return.

- Check Minimum Balance Requirements: Many platforms, such as Schwab Intelligent Portfolios Premium, require a minimum investment to unlock their most advanced tax loss harvesting features. Ensure your account meets these thresholds.

5. Systematic Tax Loss harvesting

Systematic tax loss harvesting transforms the opportunistic nature of loss harvesting into a disciplined, automated process. Instead of reacting to market downturns on an ad-hoc basis, this strategy involves setting specific, predetermined criteria and a regular schedule for reviewing and executing trades. By establishing clear rules, it removes emotion from the decision-making process, ensuring that opportunities are captured consistently throughout the year.

This methodical approach is particularly valuable for sophisticated investors managing large and complex portfolios. It institutionalizes one of the key tax loss harvesting strategies, making it a routine part of portfolio management rather than a year-end scramble. This ensures that potential tax savings are maximized over the long term by capturing losses as they occur, not just when they are noticed.

How It Works: A Practical Example

Consider a high-net-worth individual with a multi-million dollar portfolio. They establish a systematic harvesting plan with their financial advisor. The rules are simple: on the last business day of each month, the portfolio is scanned for any position that is down more than 7% from its cost basis and has an unrealized loss exceeding $5,000.

In March, the scan identifies an ETF holding with a $7,500 unrealized loss. The system automatically flags it, and the advisor sells the position to realize the loss. The proceeds are immediately reinvested into a pre-approved replacement ETF to maintain the desired asset allocation without violating the wash sale rule. By November, this systematic process has already accumulated $48,000 in harvested losses to offset gains, all without any emotional debate or market timing guesswork.

Actionable Tips for Implementation

To implement a systematic approach successfully, discipline and clear parameters are essential.

- Set Clear Thresholds: Define specific triggers for harvesting. This could be a percentage decline (e.g., 10% below cost basis) or a specific dollar amount (e.g., any loss over $2,000). The right threshold will depend on your portfolio size and trading costs.

- Create a Regular Review Calendar: Schedule your portfolio reviews consistently. This could be monthly, quarterly, or semi-annually. A fixed schedule ensures you never miss an opportunity because you forgot to look.

- Document Your Criteria: Write down your rules and stick to them. This documentation helps maintain discipline, especially during periods of high market volatility when emotions can run high.

- Integrate Wash Sale Tracking: Your system must include a robust method for tracking sales and subsequent purchases to avoid the wash sale rule. This often involves maintaining a log of sold securities and their "do not buy" periods.

A well-structured systematic approach is a cornerstone of advanced portfolio management. To see how this fits into a broader wealth strategy, explore the benefits of comprehensive financial planning on commonsllc.com.

6. Tax Loss Harvesting with Options Strategies

For high-net-worth investors seeking more sophisticated methods, integrating options can elevate a standard tax loss harvesting plan. This advanced strategy involves using derivatives like calls and puts to harvest losses while managing or maintaining exposure to the underlying security. It allows for greater flexibility than direct selling, especially when an investor is still bullish on a stock but wants to capitalize on a temporary price dip for tax purposes.

This approach merges the principles of realizing losses with the strategic advantages of options, such as controlling a large position with less capital or creating a synthetic position. By doing so, it provides a powerful way to navigate the wash sale rule while retaining potential for upside gain. These nuanced tax loss harvesting strategies are commonly employed by sophisticated hedge funds and family offices to optimize after-tax returns with precision.

How It Works: A Practical Example

Consider an investor who owns 1,000 shares of a tech company, purchased at $150 per share for a total cost basis of $150,000. The stock has since fallen to $120, creating an unrealized loss of $30,000. The investor believes the stock will rebound but wants to harvest the loss.

Instead of just selling the stock and waiting 31 days to repurchase it (and risk missing a rebound), the investor sells all 1,000 shares, realizing the $30,000 loss. Immediately after, they purchase call options on the same stock. For a relatively small premium, these calls give them the right to buy the stock back at a set price, allowing them to participate in any potential upside during the 30-day wash-sale window. This locks in the tax loss while keeping a stake in the stock's future performance.

Actionable Tips for Implementation

Successfully blending options with tax loss harvesting requires careful planning and a deep understanding of derivatives.

- Understand Options Taxation: The tax treatment of options can be complex and differs from stocks. Gains and losses on options are typically short-term or long-term capital gains, depending on the holding period. Consult a professional to ensure compliance.

- Factor in All Costs: The cost of the option premium, along with commissions and fees, must be weighed against the potential tax savings. These costs reduce the net benefit of the strategy.

- Monitor Implied Volatility: Implied volatility significantly impacts option prices. High volatility will make options more expensive, potentially making this strategy less cost-effective.

- Develop a Clear Exit Strategy: Know your plan for the options before they expire. Will you exercise them, sell them for a profit, or let them expire worthless? Each outcome has different financial and tax implications.

- Be Aware of Constructive Sales: Certain options strategies, such as creating a "collar," can be deemed a "constructive sale" by the IRS, which would trigger a gain and negate the purpose of the loss harvest.

7. Multi-Account Tax Loss Harvesting

Multi-account tax loss harvesting extends the principles of direct harvesting across an investor's entire financial landscape. This comprehensive strategy coordinates the sale of losing positions across multiple taxable accounts, such as individual brokerage, joint, and trust accounts, treating them as a single, integrated portfolio for tax optimization purposes.

This approach is particularly powerful for high-net-worth individuals and families whose assets are often spread across various legal structures. By looking at the bigger picture, you can maximize loss realization without disrupting the overall asset allocation of the combined holdings. This holistic view makes it one of the most sophisticated tax loss harvesting strategies available for managing complex financial situations.

How It Works: A Practical Example

Consider a married couple with three separate taxable accounts: a personal brokerage account for the first spouse, another for the second, and a joint account for shared investments. The first spouse's account holds an ETF tracking the S&P 500 that is at a significant loss. The joint account, however, holds a different S&P 500 ETF that has a large unrealized gain.

Instead of only looking at each account in isolation, a multi-account strategy allows them to sell the losing ETF in the individual account to realize a loss. This loss can then be used on their joint tax return to offset the capital gain from a potential sale in the joint account. This coordination prevents a situation where one account realizes a taxable gain while another sits on a tax-saving loss.

Actionable Tips for Implementation

Executing this strategy requires careful coordination and robust tracking systems.

- Use Portfolio Management Software: Employ technology that can aggregate data from all your taxable accounts. This provides a unified view of your positions, cost bases, and unrealized gains or losses, making it easier to identify harvesting opportunities.

- Centralize Record-Keeping: Maintain meticulous, centralized records for every transaction in each account. This is crucial for accurate tax reporting and for ensuring compliance across the board.

- Coordinate with Professionals: This strategy often involves multiple parties (spouses, trustees) and complex tax filings. Work closely with a financial advisor and a tax professional to ensure all actions are aligned and properly documented.

- Apply Wash Sale Rules Holistically: The IRS wash sale rule applies across all accounts owned by an individual or a couple filing jointly. If you sell a security for a loss in your individual account, you cannot repurchase a "substantially identical" one in your joint account or even your IRA within the 30-day window. A consolidated view is essential to avoid violations.

7-Strategy Tax Loss Harvesting Comparison

Integrating Advanced Strategies into Your Wealth Plan

Navigating the landscape of sophisticated investment management requires more than just picking winning stocks; it demands a proactive, strategic approach to preserving wealth. Throughout this guide, we've dissected a spectrum of powerful tax loss harvesting strategies, moving from the foundational principles of direct harvesting to the nuanced complexities of options integration and multi-account coordination. The core takeaway is clear: tax loss harvesting is not a one-size-fits-all solution but a dynamic toolkit that, when applied correctly, can significantly enhance your portfolio's after-tax returns.

By now, you understand that selling a losing position is just the first step. The real art lies in the execution, whether it's replacing an asset with a similar yet not "substantially identical" ETF, strategically placing assets in tax-advantaged versus taxable accounts, or automating the entire process with a robo-advisor to capture losses as they occur. For the high-net-worth investor, these are not mere academic exercises; they are essential components of a robust wealth management framework.

From Theory to Tangible Returns

Mastering these concepts transforms your investment approach from reactive to strategic. Instead of simply looking at market volatility as a source of risk, you can begin to view downturns as opportunities to generate valuable tax assets. The key is to integrate these tactics into a year-round, holistic financial plan rather than treating them as a last-minute, year-end scramble.

Here are the pivotal insights to carry forward:

- Consistency is Crucial: The most effective tax loss harvesting strategies are systematic, not sporadic. Implementing a consistent, year-round process, like the systematic approach we discussed, ensures you capture losses in real-time, preventing the "rebound effect" where a losing position recovers before you can act.

- Coordination Across Accounts Matters: For investors with multiple brokerage accounts, IRAs, and 401(k)s, a siloed approach is inefficient. Multi-account tax loss harvesting prevents accidental wash sales across your entire household portfolio, ensuring every harvested loss is compliant and valuable.

- Complexity Demands Expertise: As we explored with asset location and options-based strategies, the level of complexity can increase exponentially. These advanced methods offer significant benefits but also carry risks if implemented incorrectly, underscoring the value of professional guidance to navigate SEC rules and market intricacies.

Key Insight: Effective tax loss harvesting is an ongoing discipline, not an isolated event. It is the practice of turning inevitable market downturns into a tangible financial advantage that compounds over time, directly boosting your net returns.

Your Actionable Path Forward

The true power of these strategies is unlocked when they are tailored to your unique financial circumstances, risk tolerance, and long-term objectives. A strategy that works perfectly for a tech entrepreneur with concentrated stock positions may be entirely different from what’s optimal for a family managing a diversified, multi-generational portfolio.

Your next steps should involve a comprehensive review of your current investment plan. Ask yourself: Is my current approach to tax management proactive or reactive? Am I systematically identifying and capturing losses, or am I leaving money on the table? Answering these questions honestly is the first step toward building a more tax-efficient and resilient investment portfolio. By implementing even one of the advanced tax loss harvesting strategies detailed in this article, you are taking a definitive step toward optimizing your wealth and ensuring your financial plan works as hard as you do.

At Commons Capital, we specialize in transforming these complex financial concepts into personalized, actionable wealth management plans for our clients. Our team excels at integrating sophisticated tax loss harvesting strategies into a cohesive financial framework designed to maximize your after-tax returns. If you're ready to move beyond basic tax management and implement a truly proactive strategy, connect with an advisor at Commons Capital to see how we can help you achieve your financial goals.