As your income and net worth expand, the complexity of your financial picture grows exponentially. The standard tax advice that serves the average household becomes insufficient, often leaving significant savings on the table. For high-income earners, business owners, and investors, a proactive and sophisticated approach to tax planning is not just beneficial—it's essential for wealth preservation and growth. Merely earning a high income doesn't guarantee financial success; effectively managing your tax liability is a critical component of building lasting wealth.

This guide is specifically designed to address that need, providing a detailed roadmap of the best tax strategies for high income earners. We will move beyond elementary tips to provide a comprehensive overview of powerful, actionable techniques that can substantially reduce your tax bill. You'll learn how to strategically optimize every aspect of your financial life, from investment portfolios and business structures to retirement planning and philanthropic goals.

We will explore seven distinct, high-impact strategies, including:

- Advanced methods for maximizing retirement account contributions.

- Sophisticated tax-loss harvesting to offset capital gains.

- Strategic charitable giving that benefits both you and your chosen causes.

- Business entity optimization for maximum tax efficiency.

- Leveraging powerful real estate investment tax benefits.

- Utilizing municipal bonds for tax-free income.

- Integrating life insurance into your broader estate planning.

Each section offers a clear explanation, practical implementation steps, and real-world examples to help you and your financial advisor apply these concepts directly to your situation. By implementing these proven strategies, you can take definitive control of your tax destiny.

1. Maximize Retirement Account Contributions

For high-income earners, maximizing contributions to tax-advantaged retirement accounts is a foundational and powerful tax-reduction strategy. These accounts allow your investments to grow tax-deferred or tax-free, significantly lowering your current taxable income while simultaneously building wealth for the future. This approach is a cornerstone of the best tax strategies for high income earners because it offers a direct, dollar-for-dollar reduction in your adjusted gross income (AGI) for contributions made to traditional accounts.

The immediate tax savings can be substantial. By contributing the maximum amount, you are effectively shielding a portion of your income from your highest marginal tax bracket. This strategy provides a guaranteed return on your money in the form of tax savings, regardless of market performance.

How to Implement This Strategy

The key is to contribute the maximum allowable amount to every available tax-advantaged account. The specific accounts and limits depend on your employment status and income level.

- Corporate Employees: Focus on your workplace 401(k) or 403(b). For 2024, the employee contribution limit is $23,000. If you are age 50 or older, you can make an additional catch-up contribution of $7,500, for a total of $30,500.

- Self-Employed Individuals: You have more flexibility. A SEP-IRA allows you to contribute up to 25% of your compensation, not to exceed $69,000 for 2024. A Solo 401(k) offers the same employer contribution limit plus the employee deferral of $23,000, creating a powerful combination.

- High Earners Exceeding Roth IRA Limits: If your income is too high to contribute directly to a Roth IRA, you can utilize the Backdoor Roth IRA strategy. This involves contributing to a non-deductible Traditional IRA and then promptly converting it to a Roth IRA.

Real-World Example: The Mega Backdoor Roth

A highly effective, yet often overlooked, strategy for those whose 401(k) plans allow it is the Mega Backdoor Roth IRA. This allows you to make after-tax contributions to your 401(k) beyond the standard employee limit, up to the total IRS limit of $69,000 for 2024 (or $76,500 if 50+).

An executive earning $500,000 maxes out her standard $23,000 401(k) contribution. Her company's plan allows for after-tax contributions and in-service withdrawals. She contributes an additional $46,000 in after-tax dollars to her 401(k) and immediately converts it to her Roth IRA. This $46,000 will now grow completely tax-free for the rest of her life.

Actionable Tips for Maximization

- Front-Load Contributions: Contribute the maximum amount as early in the year as possible to give your investments more time to grow tax-deferred.

- Review Your 401(k) Plan: Check if your employer's plan allows for after-tax contributions and in-service distributions, the two components necessary for the Mega Backdoor Roth strategy.

- Coordinate with Your Spouse: If you are married, ensure both spouses are maximizing their respective retirement accounts, including any available catch-up contributions.

2. Tax-Loss Harvesting

For investors with significant taxable brokerage accounts, tax-loss harvesting is a sophisticated and highly effective method for minimizing capital gains taxes. This strategy involves intentionally selling investments that have decreased in value to realize a capital loss. These losses can then be used to offset capital gains from other investments, directly reducing your tax liability. This makes it one of the best tax strategies for high income earners as it transforms market downturns into valuable tax-saving opportunities.

The power of this strategy lies in its ability to generate tax "alpha" without fundamentally altering your investment allocation. By systematically harvesting losses, you can defer taxes, allowing more of your capital to remain invested and compound over time. If your losses exceed your gains, you can deduct up to $3,000 per year against your ordinary income, with any remaining losses carried forward indefinitely to offset future gains.

How to Implement This Strategy

The core principle is to sell a security at a loss and immediately reinvest the proceeds into a similar, but not "substantially identical," asset. This maintains your desired market exposure while booking a loss for tax purposes. The IRS "wash-sale rule" prohibits you from claiming a loss if you buy back the same or a substantially identical security within 30 days before or after the sale.

- Identify Losses: Regularly review your taxable investment portfolio for positions that are trading below your cost basis.

- Sell and Replace: Sell the underperforming asset to realize the capital loss. Immediately reinvest the proceeds into a comparable alternative (e.g., sell an S&P 500 ETF and buy a different large-cap U.S. stock ETF).

- Offset Gains: When you file your taxes, use the harvested losses to offset any realized capital gains. Short-term losses must first offset short-term gains, and long-term losses must first offset long-term gains.

Real-World Example: Systematic Loss Harvesting

A high-earning investor has a taxable portfolio with a mix of ETFs. During a market dip, their U.S. large-cap ETF is down $15,000. Earlier in the year, they realized a $20,000 short-term capital gain from selling a different stock.

The investor sells the U.S. large-cap ETF, "harvesting" the $15,000 loss. They immediately use the cash to purchase a different U.S. large-cap blend ETF to maintain their allocation. At tax time, they use the $15,000 loss to offset their gain, reducing their taxable capital gain from $20,000 to just $5,000. This saves them thousands in taxes at their high marginal rate.

Actionable Tips for Maximization

- Be Proactive, Not Reactive: Don't wait until December. Market volatility can occur at any time, so monitor your portfolio year-round for harvesting opportunities.

- Prioritize Short-Term Losses: Harvest short-term losses first, as they can offset short-term gains which are taxed at higher ordinary income rates.

- Avoid the Wash-Sale Rule: Be meticulous in tracking your trades. When you sell for a loss, ensure your replacement security is not "substantially identical." Using a different ETF provider for a similar index is a common approach.

- Automate with Technology: Consider using robo-advisors like Betterment or Wealthfront, which pioneered automated tax-loss harvesting services, making this complex strategy accessible and efficient.

3. Charitable Giving Strategies

For high-income individuals, strategic charitable giving is not just about philanthropy; it's a sophisticated financial tool that can significantly reduce tax liability. By moving beyond simple cash donations, you can employ advanced strategies to maximize your tax deductions, eliminate capital gains taxes, and support the causes you care about most. This approach is one of the best tax strategies for high income earners because it aligns personal values with powerful financial benefits.

The core principle is to give smarter, not just more. Donating highly appreciated assets instead of cash, for instance, provides a double tax benefit: a full fair market value deduction and the complete avoidance of capital gains tax on the asset's growth. This method allows you to give more to charity and keep more of your wealth.

How to Implement This Strategy

Effective charitable tax planning involves choosing the right vehicle and timing for your donations. The best approach depends on your assets, income level, and philanthropic goals.

- Donate Appreciated Securities: Instead of selling stock and donating the cash, transfer the stock directly to a public charity or a Donor-Advised Fund (DAF). If held for over a year, you can deduct the full fair market value and avoid paying capital gains tax.

- Bunching Donations with a Donor-Advised Fund (DAF): If your annual charitable giving is close to the standard deduction, consider "bunching." You can contribute several years' worth of donations into a DAF in a single high-income year to exceed the standard deduction and itemize. You can then grant the funds to charities over the following years.

- Charitable Remainder Trusts (CRTs): For very high-net-worth individuals, a CRT allows you to place assets into a trust, receive an immediate partial tax deduction, and get an income stream for a set term or for life. The remainder of the assets goes to charity upon your passing.

Real-World Example: The Appreciated Stock Donation

This strategy is highly effective for executives or early investors with significant holdings in appreciated company stock. It provides a direct and substantial tax benefit that cash donations cannot match.

A tech executive wants to donate $1,000,000 to her alma mater. Her company stock, which she bought for $100,000 years ago, is now worth $1,000,000. Instead of selling the stock, paying $238,000 in federal capital gains taxes (20% LTCG + 3.8% NIIT), and donating the rest, she donates the shares directly. She avoids the entire capital gains tax and gets a $1,000,000 tax deduction, saving hundreds of thousands in taxes.

Actionable Tips for Maximization

- Audit Your Portfolio: Identify highly appreciated assets like stocks, mutual funds, or real estate that have been held for more than one year as prime candidates for donation.

- Plan Around High-Income Years: Use strategies like donation bunching in years when you have a large bonus, sell a business, or experience another significant liquidity event to maximize your deduction.

- Consult Professionals: Work with financial advisors and tax professionals to structure complex gifts like CRTs or to navigate the rules around DAFs. You can learn more about developing a plan for your charitable giving and social impact on commonsllc.com.

4. Business Entity Optimization

For high-income earners with business activities, side hustles, or consulting income, structuring these operations within the right legal entity is a crucial tax-planning tool. Choosing the correct structure, such as an S-Corporation or an LLC, can unlock significant savings on self-employment taxes and create eligibility for powerful deductions. This is one of the best tax strategies for high income earners because it fundamentally changes how your business income is taxed, offering a more favorable outcome than operating as a sole proprietor.

The primary benefit lies in separating business income from personal wages. This allows for strategic tax management, particularly in mitigating the 15.3% self-employment tax and maximizing deductions like the Section 199A Qualified Business Income (QBI) deduction.

How to Implement This Strategy

The ideal entity depends on your specific income level, business type, and long-term goals. The goal is to move from being a sole proprietorship, where all net income is subject to self-employment tax, to a more sophisticated structure.

- S-Corporation Election: By forming an S-Corp (or an LLC taxed as an S-Corp), you can pay yourself a "reasonable salary" subject to payroll taxes. Any additional profits are distributed as dividends, which are not subject to self-employment taxes.

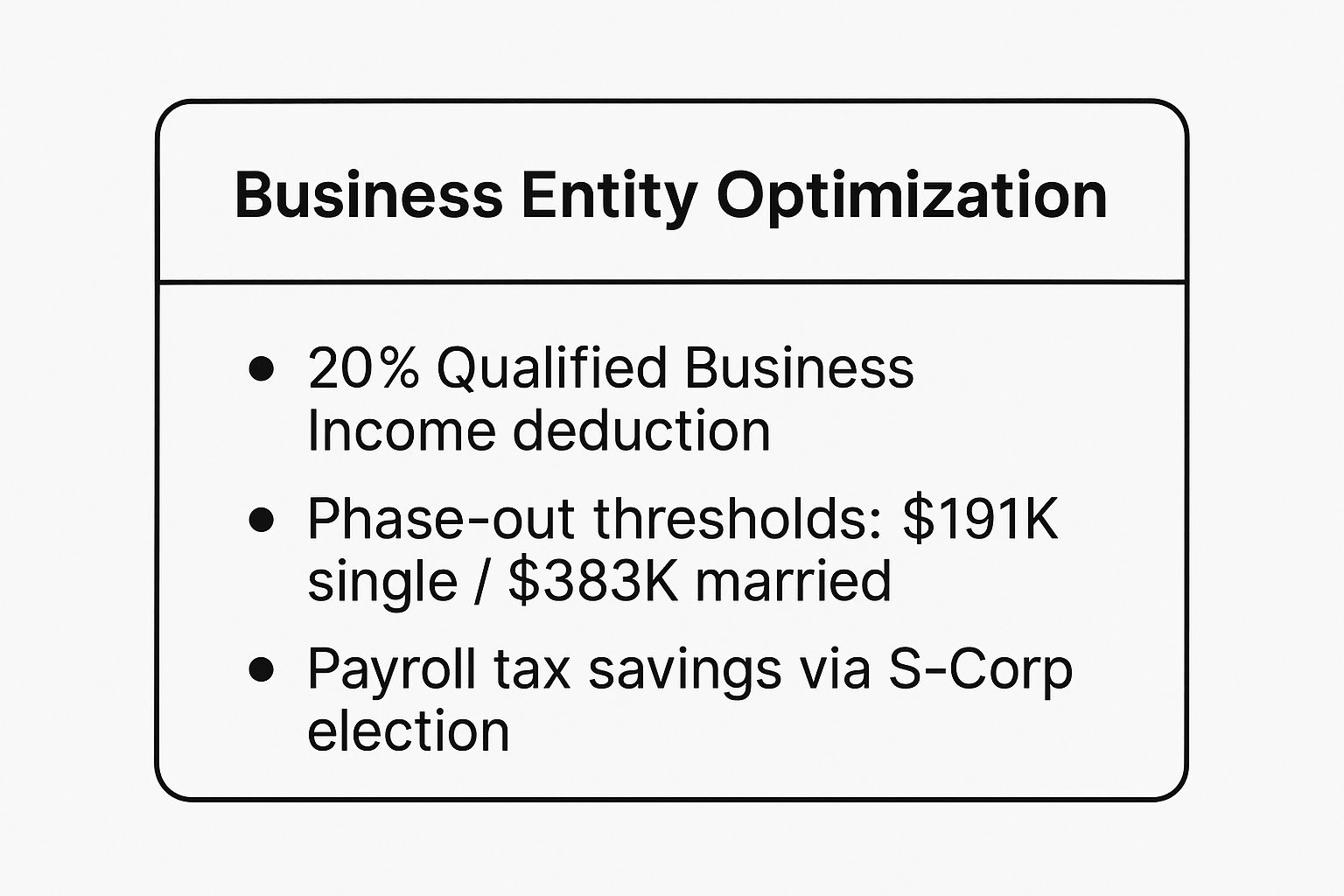

- Qualified Business Income (QBI) Deduction: The Section 199A deduction allows owners of pass-through businesses (S-Corps, partnerships, LLCs) to deduct up to 20% of their qualified business income. This is a direct reduction of your taxable income, but it is subject to income-based phase-outs.

- Solo 401(k) for Business Owners: If you are self-employed with no employees (other than a spouse), a Solo 401(k) allows you to contribute as both the "employee" and the "employer," enabling contributions up to $69,000 for 2024, far exceeding standard IRA limits.

Real-World Example: S-Corp Tax Savings

Proper entity selection provides a direct and immediate impact on your tax liability. The savings on self-employment tax alone can be substantial.

A consultant earns $300,000 in net income as a sole proprietor and would typically pay about $33,000 in self-employment taxes. By forming an S-Corp, she pays herself a reasonable salary of $120,000. She pays payroll taxes only on this salary. The remaining $180,000 is distributed as a dividend, completely avoiding the 15.3% self-employment tax and saving her approximately $27,540 annually.

This summary box highlights the core components of optimizing your business structure for tax efficiency.

The key takeaways are the significant 20% QBI deduction, the payroll tax savings from an S-Corp, and the critical income thresholds you must monitor to remain eligible for these benefits.

Actionable Tips for Maximization

- Monitor QBI Phase-Outs: For 2024, the QBI deduction begins to phase out for specified service businesses at taxable incomes of $191,950 for single filers and $383,900 for married couples filing jointly.

- Set a Reasonable Salary: If you elect S-Corp status, you must pay yourself a reasonable W-2 salary for the services you provide. The IRS scrutinizes this, so document how you determined the amount.

- Maintain Meticulous Records: Separate business and personal finances completely. Meticulous bookkeeping is essential for justifying all business expense deductions and defending your entity structure if audited.

- Strategically Time Income and Expenses: As a business owner, you may have more control over when you recognize income or incur expenses. Use this flexibility to manage your taxable income from year to year.

5. Real Estate Investment Tax Benefits

For high-income individuals, direct real estate investing offers a uniquely powerful set of tax advantages that are difficult to replicate in other asset classes. Unlike stocks or bonds, real estate allows for significant deductions, tax deferral, and special classifications that can shelter substantial portions of your income. Leveraging these benefits is one of the best tax strategies for high income earners because it allows you to generate wealth while simultaneously creating paper losses to offset other taxable gains.

The core tax benefit is depreciation, a non-cash expense that allows you to deduct a portion of your property's value from your rental income each year. This can often result in a taxable loss on paper, even when the property is generating positive cash flow. These tax advantages, popularized by real estate investors like Robert Kiyosaki, can dramatically reduce your overall tax liability.

How to Implement This Strategy

Successfully using real estate for tax reduction involves more than just buying a property. You must strategically utilize specific provisions within the tax code that are particularly beneficial for high-income earners.

- Depreciation and Cost Segregation: The IRS allows you to depreciate residential rental properties over 27.5 years. A cost segregation study can accelerate this process by identifying components of the property that can be depreciated over a shorter period (5, 7, or 15 years), creating larger deductions in the early years of ownership.

- 1031 Exchange: This powerful tool allows you to sell an investment property and defer paying capital gains tax on the profit, provided you reinvest the proceeds into a new "like-kind" property within a specific timeframe. This enables you to continuously grow your real estate portfolio tax-deferred.

- Real Estate Professional Status (REPS): For those who qualify, REPS allows you to deduct unlimited rental losses against your ordinary income (such as your W-2 salary or business income), bypassing the standard passive activity loss limitations. This requires spending more than 750 hours and more than half your working time on real estate activities.

Real-World Example: Qualifying as a Real Estate Professional

This strategy is a game-changer for high-income households where one spouse can meet the stringent time requirements. It transforms passive rental losses into active losses that can shelter high-earning W-2 or business income.

A surgeon earns $500,000 annually, while their spouse works to qualify as a real estate professional, managing their extensive rental portfolio. Through aggressive depreciation (including bonus depreciation), their properties generate a paper loss of $100,000. Because the spouse qualifies for REPS, they can deduct this entire $100,000 loss directly from the surgeon's income, reducing their taxable income to $400,000 and saving them over $35,000 in federal taxes.

Actionable Tips for Maximization

- Maintain Meticulous Records: If aiming for Real Estate Professional Status, keep a detailed, contemporaneous log of all hours spent on real estate activities to substantiate your claim in an audit.

- Engage a Qualified Intermediary: For a 1031 exchange, you must use a qualified intermediary to hold the funds from the sale. Plan your exchange well in advance to meet the strict 45-day identification and 180-day closing deadlines.

- Explore Opportunity Zones: If you have capital gains from selling other assets like stocks, investing those gains into a Qualified Opportunity Fund can allow you to defer and potentially reduce that tax liability.

6. Municipal Bond Investing

For high-income individuals seeking to reduce their tax burden on investment income, investing in municipal bonds is a classic and highly effective solution. Municipal bonds, or "munis," are debt securities issued by states, cities, counties, and other government entities to fund public projects. Their primary appeal is that the interest income they generate is typically exempt from federal income tax, and in many cases, also from state and local taxes, making them one of the best tax strategies for high income earners.

This tax-free nature creates a significant advantage when compared to taxable corporate bonds or other fixed-income investments. For an investor in the highest marginal tax bracket, the tax-equivalent yield of a municipal bond can be substantially higher than its stated interest rate, providing a more attractive after-tax return.

How to Implement This Strategy

The core of this strategy is to allocate a portion of your investment portfolio to high-quality municipal bonds or bond funds, particularly for assets held in taxable brokerage accounts. The key is to calculate the tax-equivalent yield to make an apples-to-apples comparison with taxable investments.

- Calculate Tax-Equivalent Yield: The formula is: Tax-Equivalent Yield = Municipal Bond Yield / (1 - Your Marginal Tax Rate). This calculation reveals the yield a taxable bond would need to offer to match the after-tax return of a muni.

- Consider In-State Bonds: If you live in a state with a high income tax, such as California or New York, purchasing bonds issued by entities within your state can provide a double tax benefit: exemption from both federal and state income taxes.

- Use a Bond Ladder: To manage interest rate risk, high earners can build a municipal bond ladder. This involves purchasing bonds with staggered maturity dates (e.g., 2, 4, 6, 8, and 10 years). As each bond matures, the principal can be reinvested in a new long-term bond, helping to smooth out returns and provide predictable income.

Real-World Example: Maximizing After-Tax Income

Understanding the tax-equivalent yield is crucial for seeing the true power of this strategy for those with high incomes. It directly translates into keeping more of your investment returns.

An executive in the 37% federal tax bracket is considering two bonds: a corporate bond yielding 6.35% and a municipal bond yielding 4%. While the corporate bond's yield looks higher initially, its after-tax yield is only 4% (6.35% x (1 - 0.37)). In this scenario, the 4% tax-free yield from the municipal bond provides the exact same take-home return, often with potentially lower risk.

Actionable Tips for Maximization

- Focus on High-Tax States: If you reside in a state with a high income tax, prioritize in-state municipal bonds to secure the valuable double tax exemption.

- Diversify Your Holdings: Avoid concentrating your investment in a single issuer. Diversify across various issuers, projects, and maturities to mitigate credit and concentration risk.

- Be Mindful of the AMT: Some municipal bonds, often those financing private activities like airports or stadiums, may be subject to the Alternative Minimum Tax (AMT). Confirm the tax status of any bond before investing. As market conditions shift, it is important to stay informed; it could be a great time for bonds depending on the interest rate environment.

7. Life Insurance and Estate Planning Integration

For affluent individuals and families, integrating advanced life insurance strategies with comprehensive estate planning is a sophisticated method for wealth preservation and tax-efficient transfer. This approach goes beyond simple life insurance, using specialized policies and legal structures to create tax-free liquidity, protect assets from creditors, and ensure a seamless transfer of wealth to the next generation. This is one of the best tax strategies for high income earners because it addresses the significant threat of federal estate taxes, which can be as high as 40%.

By properly structuring life insurance, the death benefit payout can be entirely free from both income and estate taxes. This provides crucial, tax-free capital to heirs, which can be used to pay estate taxes on other, less liquid assets like real estate or a family business, preventing a forced sale. The cash value within certain policies can also grow on a tax-deferred basis, offering an additional layer of tax-advantaged investment.

How to Implement This Strategy

Effective integration requires careful coordination between financial advisors, insurance specialists, and estate planning attorneys. The goal is to select and structure policies within legal entities that shield the proceeds from the taxable estate.

- Irrevocable Life Insurance Trust (ILIT): This is the most common tool. You create a trust that owns your life insurance policy. Since you do not personally own the policy, the death benefit is not included in your gross estate and is not subject to estate tax. You make annual gifts to the trust to cover premium payments.

- Private Placement Life Insurance (PPLI): For ultra-high-net-worth individuals, PPLI offers a way to invest in hedge funds and other alternative investments within a life insurance policy wrapper. This allows the investments to grow and be passed on tax-free, bypassing both capital gains and estate taxes.

- Split-Dollar Arrangements: Often used in a business context, this is an agreement where an employer and an employee (or a trust) share the costs and benefits of a permanent life insurance policy. It can be a powerful tool for executive compensation and business succession planning.

Real-World Example: Using an ILIT for Estate Liquidity

A high-net-worth family has a taxable estate valued at $30 million. They anticipate a significant federal estate tax liability upon their passing. To address this, they work with their advisor to establish an ILIT.

The family creates an ILIT and the trust purchases a $10 million life insurance policy on their lives. They use their annual gift tax exclusion to fund the trust, which then pays the policy premiums. Upon their death, the ILIT receives the $10 million death benefit completely free of estate and income tax. Their heirs, as beneficiaries of the trust, can use this tax-free liquidity to pay the estate taxes, preserving the family's core assets for future generations.

Actionable Tips for Maximization

- Work with an Experienced Team: This is a complex area. A coordinated team of a CFP, an estate planning attorney, and a qualified insurance professional is essential. You can explore expert guidance and learn more about trust and estate planning strategies at commonsllc.com.

- Fund the ILIT Correctly: Ensure premium payments are structured as gifts to the trust using your annual gift tax exclusion to avoid gift tax complications.

- Conduct Regular Policy Reviews: Periodically review your policies with your advisor to ensure they are performing as expected and that the strategy remains aligned with your overall estate plan and current tax laws.

Integrating Your Tax Strategy for Maximum Impact

Navigating the complexities of the U.S. tax code can feel like piecing together an intricate puzzle. We have explored some of the most powerful tools available to high-income earners, from maximizing retirement accounts and leveraging tax-loss harvesting to sophisticated charitable giving and real estate investment strategies. Each of these methods offers a distinct advantage, a single piece of the puzzle that can significantly reduce your tax burden.

However, the true mastery of tax planning doesn't come from applying these strategies in isolation. The most profound and sustainable results emerge when you weave them together into a single, cohesive financial tapestry. This integrated approach transforms a collection of individual tactics into a powerful, unified strategy that works synergistically to protect and grow your wealth.

The Power of Synergy in Tax Planning

Think of it this way: tax-loss harvesting can offset capital gains, but when combined with a Donor-Advised Fund (DAF), you can use appreciated assets to fund your charitable goals, effectively eliminating capital gains tax on those assets while still capturing a deduction. Similarly, the depreciation benefits from a real estate investment can be strategically used to offset active income from your business, especially if you have optimized your business entity structure for maximum tax efficiency.

This synergy creates a compounding effect, where the combined benefit is far greater than the sum of the individual parts. It's about seeing the big picture and understanding how each financial decision impacts the others.

Key Takeaway: The best tax strategies for high income earners are not a checklist of one-off actions. They are interconnected components of a dynamic, long-term financial plan designed to align with your specific goals, risk tolerance, and life circumstances.

Actionable Next Steps: Building Your Cohesive Plan

Understanding these concepts is the crucial first step. Now, the challenge is to translate that knowledge into a personalized, actionable plan. Here’s how you can move forward with confidence:

- Conduct a Comprehensive Review: Start by assessing your current financial situation. Look at your income sources, investment portfolio, business structure, and charitable intentions. Where are the biggest tax drains? Where are the untapped opportunities?

- Model Different Scenarios: Work with a financial professional to model how implementing various strategies would impact your tax liability. For example, how would converting a portion of your traditional IRA to a Roth IRA affect your long-term tax outlook? What are the tax implications of selling a specific asset?

- Establish a Proactive Cadence: Tax planning is not a once-a-year event. It requires regular monitoring and adjustments. Schedule quarterly or semi-annual reviews with your advisory team to stay ahead of legislative changes and adapt your strategy as your personal and financial life evolves.

Mastering these sophisticated approaches is not just about keeping more of your hard-earned money; it is about achieving greater financial freedom and control. It empowers you to direct your capital toward what matters most, whether that's growing your business, securing your family's future, or making a meaningful impact through philanthropy. By taking a proactive and integrated approach, you can transform your tax liability from a significant headwind into a powerful tailwind, accelerating your journey toward your ultimate financial goals.

Navigating this complex landscape requires specialized expertise. The team at Commons Capital excels at creating bespoke financial and tax mitigation plans for high-net-worth individuals, integrating these advanced strategies into a seamless and effective long-term plan. If you are ready to build a cohesive strategy that optimizes your wealth, contact us to learn how we can help secure your financial future.