A layoff isn't just about losing a job—it's a strategic business decision that rarely has anything to do with an individual's performance. For executives and high-net-worth individuals, understanding this distinction is the first critical step. It’s how you turn an unexpected career detour into a moment of powerful financial and professional recalibration, especially if you are facing a layoff in 2024.

Why Even Profitable Companies Conduct Layoffs

In today's dynamic economy, a layoff is not the red flag it once was. It is not necessarily a sign of a failing company. More often than not, it signals a strategic pivot—a deliberate decision by leadership to shift resources, streamline operations, or prepare for future market conditions.

Think of it like a seasoned ship captain charting a new course. To navigate changing economic waters efficiently, they must adjust the crew and cargo. For executives caught in these shifts, it's crucial to depersonalize the event. The decision to eliminate your role was likely driven by broad macroeconomic factors or an internal reorganization, not your capabilities. Understanding the layoff process helps frame the situation correctly.

The Key Drivers Behind Modern Layoffs

Several powerful forces compel even wildly successful companies to restructure. These aren't signs of weakness; they're proactive measures to stay competitive and maintain financial health.

Here’s what’s usually happening behind the scenes:

- Market Shifts and Economic Headwinds: When consumer demand changes, interest rates climb, or a recession looms, companies get proactive about cutting costs. Trimming headcount is often a primary move to protect profitability and ensure they can weather potential storms.

- Technological Advancements: The rise of artificial intelligence and automation is completely reshaping entire industries. As new technology handles tasks once done by people, companies often restructure their teams to focus on higher-value, strategic work, which can lead to layoffs in certain departments.

- Internal Restructuring and Mergers: When companies merge or acquire another business, roles often become redundant. A layoff becomes a necessary step to create a more efficient, integrated organization without duplicate positions.

Layoff vs. Fired: The Critical Distinction

It’s absolutely essential to understand the difference between being laid off and being fired for cause. This distinction changes everything, from your severance negotiation strategy to your prospects for future employment.

A layoff is a termination of employment due to business needs, like restructuring or downsizing, and is not related to your individual performance. In contrast, being fired is a termination for cause, directly linked to performance issues, misconduct, or a violation of company policy.

This is precisely why a layoff should be seen as a strategic, impersonal business event. The national economic landscape shows just how common this has become. Over the past 25 years, U.S. companies have seen an average of 1.9 million monthly layoffs and discharges. That number skyrocketed to an unprecedented 13.5 million in March 2020 during the pandemic, a stark reminder of how widespread economic shocks can trigger massive, impersonal workforce changes.

You can explore more data on U.S. job market trends to see these patterns for yourself. Recognizing this context helps reframe what’s happened, allowing you to approach your next steps after a layoff from a position of clarity and control, not self-blame.

Your First 48 Hours: A Financial Action Plan After a Layoff

The first few hours after hearing you’ve been laid off are a blur. It's disorienting, and the natural impulse is to react emotionally. But this is the most critical window to take control of the situation. Your immediate goal isn’t to map out your entire future; it’s about financial triage.

Think of it like a first responder at an accident scene. You assess the situation, stabilize what you can, and stop any immediate bleeding before thinking about the long road to recovery. Your finances are the patient, and your calm, deliberate actions are the treatment.

Secure Your Essential Documents

Before your access to company systems disappears, your absolute first priority is to gather every piece of financial paperwork you can. Trying to get these documents after you’re gone is a bureaucratic nightmare. Act fast.

You need to download or get hard copies of these items:

- Your employment agreement and offer letter: This contract outlines your compensation, equity, and the original terms you agreed to.

- Recent pay stubs: These are your proof of earnings and deductions.

- Performance reviews: Positive reviews can be surprisingly powerful leverage if you decide to negotiate a better severance package.

- Benefits information: Get all the details on your health, dental, life, and disability insurance plans.

- Retirement and stock plan documents: This means your 401(k) statements, stock option agreements (ISOs/NSOs), and RSU vesting schedules.

This is also the time to get firm details on your final paycheck. Ask when it will arrive and exactly what it will cover—things like unused vacation time, pending commissions, or bonuses. Get this confirmation in an email to avoid any disputes down the line.

Assess Your Liquidity and Create a Transition Budget

With your documents in hand, it's time for a frank look at your cash situation. This isn’t a full-blown net worth calculation. It’s a quick snapshot of the cash you can access right now. Add up what’s in your checking, savings, and money market accounts. That’s your liquidity number.

This number is the foundation for your transition budget. The immediate goal is to slash your cash outflow. Go through your spending and pause everything that isn't absolutely essential. Subscriptions, fancy dinners, vacation plans—put them on hold. It might feel drastic, but creating this financial buffer buys you incredibly valuable time and peace of mind.

The point of the first 48 hours isn't to solve every problem. It's to create breathing room. By getting a grip on your spending and knowing exactly what resources you have, you shift from a state of shock to a position of control.

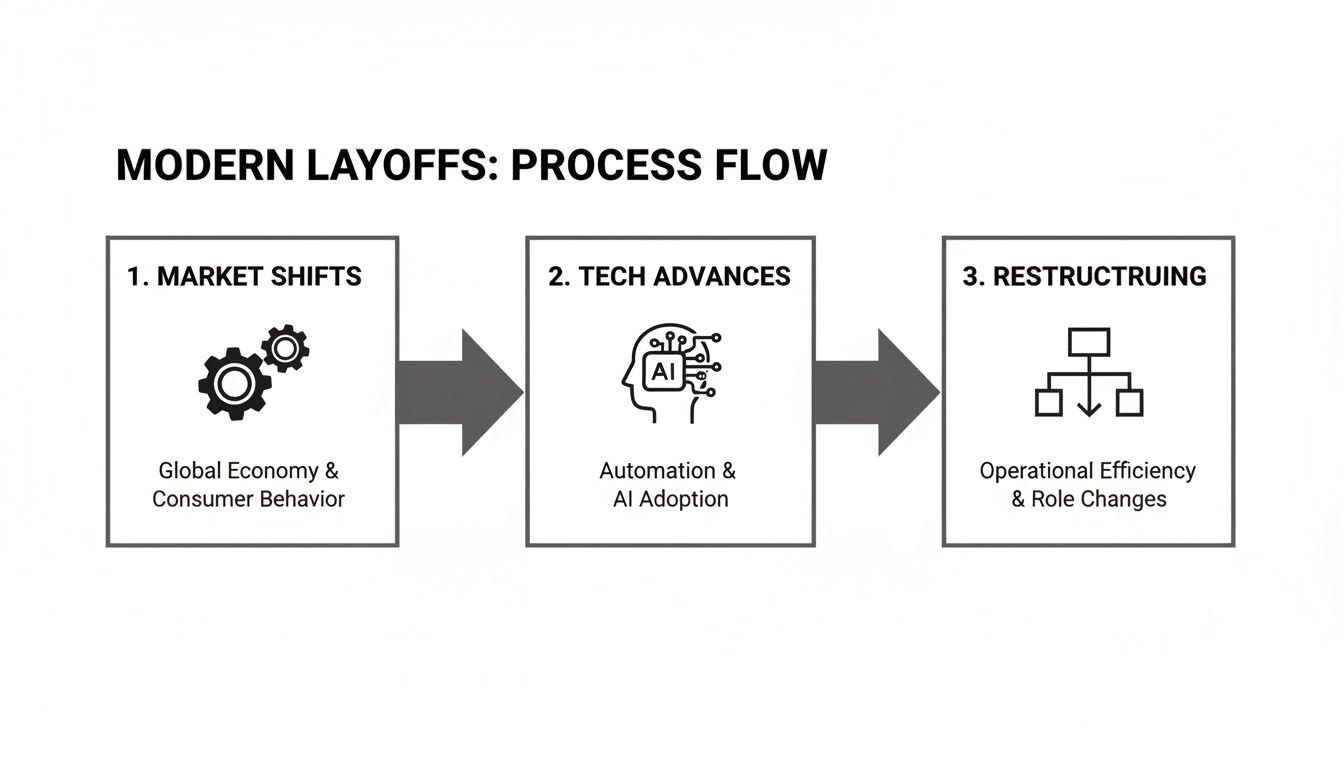

This disciplined approach is crucial. Layoffs can happen for any number of reasons, from broad market shifts and new technology to a simple internal reorganization.

The image below shows how these forces often converge, leading to workforce changes.

Ultimately, the "why" behind the company's decision doesn't matter as much as the "what now" for your own financial plan.

To help you stay on track during this high-stress period, use this checklist to guide your immediate financial actions.

Layoff Financial Triage Checklist

This checklist isn't about long-term planning; it’s about ensuring you’ve covered the urgent bases right away.

Understand Your Benefits and Next Steps

Finally, get concrete answers about what happens to your benefits after a layoff. For most people, health insurance is the biggest worry. You need to ask your HR contact for the specific details on COBRA (Consolidated Omnibus Budget Reconciliation Act), including how much it will cost you per month and what the deadline is to enroll. It's usually expensive, but it's a critical safety net.

At the same time, you should start looking into state unemployment benefits. Every state has different rules, and figuring them out early is key. For a complete guide on this, you can learn more about how to get unemployment after a layoff here. Tackling these steps in the first two days ensures you won't miss a critical deadline and helps you navigate the initial shock with a clear head.

How To Negotiate Your Severance Package After a Layoff

When a severance agreement lands on your desk after a layoff, it’s easy to assume it’s a done deal. But in reality, that document is often just a starting point. For executives and high-earning professionals, the first offer is rarely the best one, and a smart negotiation can turn a standard payout into a solid financial bridge to your next big move.

Approach this like any other high-stakes business deal. Remember, the company wants a smooth and clean separation. That gives you leverage. Your job is to calmly and professionally make the case for terms that truly reflect your contributions and set you up for success.

Deconstructing the Initial Offer

Before you can even think about negotiating, you have to know exactly what’s on the table. A typical severance agreement is made up of several moving parts, and each one is a potential area for improvement. Don't rush this—take the time to analyze every detail.

Most packages will include:

- Salary Continuation: The core of the offer, usually a certain number of weeks or months of pay based on your tenure.

- Healthcare Coverage: This section outlines how long the company will help pay for your health insurance premiums, typically through COBRA.

- Unvested Equity: It will specify what happens to your unvested stock options or Restricted Stock Units (RSUs).

- Outplacement Services: Help with career coaching, resume writing, or other job-hunting resources.

- Non-Compete and Non-Disclosure Agreements (NDAs): Legal clauses that limit where you can work next and what you can say about the company.

Each of these is a lever you can potentially pull.

Identifying Your Leverage Points

Your negotiating power comes directly from your track record. For senior leaders and proven top performers, your history with the company is your greatest asset in securing a better package.

Think about these key leverage points:

- Past Performance: Your history of strong performance reviews, successful projects, and measurable contributions is your best evidence. Frame every request around the value you already delivered.

- Unvested Equity: Walking away from a significant amount of unvested equity is a real financial hit. You can argue for partial or accelerated vesting as fair compensation for the value you would have continued to create.

- Restrictive Covenants: A non-compete clause can seriously hamstring your ability to find another job in your field. You can push to have it removed or ask for more compensation in return for signing it.

- Company Precedent: If you know that others in similar situations received more generous packages, you can use that information as a benchmark.

This isn’t about making emotional demands. It’s about building a compelling business case for why a better package is both fair and reasonable. Present your points with a level head, backed by documentation like old performance reviews.

Advanced Negotiation Tactics for High Earners

Beyond the basics, high-net-worth individuals need to dig deeper, focusing on the structure of the payout and other high-value benefits. This calls for a more strategic approach that weighs the long-term financial impact of every decision.

The broader economic environment can also play a role in a company's flexibility. The job market has seen significant churn in recent years. In fact, 2023 saw over 721,000 job cuts in the U.S., a significant increase from the previous year. A tough job market can strengthen your argument for needing extended benefits and a larger safety net.

Structuring the Payout: Lump Sum vs. Salary Continuation

One of the most important decisions you'll make is how to receive the money. Choosing between a single lump-sum payment and continued salary payments has major tax and cash flow implications.

It's critical to model the tax impact of both scenarios with a financial advisor before you decide. A layoff is also a natural time to reassess your retirement strategy; our guide on what to do with your 401(k) after leaving a job is a great place to start. By negotiating your severance thoughtfully, you can build a more secure financial runway for whatever comes next.

Optimizing Your Wealth During a Career Transition After a Layoff

A layoff can feel like a financial earthquake, but once the ground stops shaking, you might find a rare opportunity to rebuild your entire financial house, stronger than before. This isn't just about damage control; it's a chance to move from autopilot to active, strategic wealth management. With a clear head and a deliberate plan, this transition can become a powerful moment to fortify your long-term financial health.

It all starts with shoring up your cash reserves and taking a hard look at your investment portfolio to see if it still makes sense for your new reality. This is also the time to untangle complex compensation structures and make smart moves with your retirement accounts—decisions that can pay dividends for decades.

Rebalancing Your Investment Portfolio

Your investment strategy was likely built for a world with a steady paycheck. A layoff pulls that foundation out from under you, meaning your portfolio's risk tolerance needs an immediate check-up.

Right now, the name of the game is capital preservation. You need enough liquidity to cover your expenses without being forced to sell assets at the worst possible time. This is a moment for a defensive posture, not aggressive growth plays.

One powerful tactic to consider is tax-loss harvesting. This involves strategically selling investments that are currently down to "harvest" the loss. You can then use those capital losses to cancel out capital gains elsewhere in your portfolio, which could seriously lower your tax bill for the year. In a year where your income is already lower due to a layoff, this move becomes especially potent.

Navigating Complex Equity Compensation

For many high-level professionals, a huge chunk of their net worth is tied up in company stock. A layoff brings urgent, and often complicated, decisions about these assets to the forefront.

- Stock Options (ISOs & NSOs): Your company will give you a post-termination exercise (PTE) window—often a shockingly short 90 days—to exercise your vested options. If you miss it, they're gone for good. You have to decide quickly if you want to exercise them, a move that requires cash on hand and immediately triggers a taxable event.

- Restricted Stock Units (RSUs): Any unvested RSUs are typically forfeited when you leave. But, as we covered in severance negotiations, this isn't always set in stone. You may be able to negotiate for some or all of them to vest.

You absolutely have to understand the fine print of your equity agreements. The financial difference between exercising your options versus letting them expire, or successfully negotiating for your RSUs, can be massive.

A layoff forces a critical review of your entire financial plan. It's an opportunity to shift from autopilot to active management, ensuring every component of your wealth—from investments to retirement accounts—is aligned with your new circumstances.

Strategic 401(k) and Retirement Planning

That 401(k) from your old job is one of your most critical assets. What you do with it now will echo through your retirement for years to come. Cashing it out is almost always a terrible idea, resulting in a brutal tax hit and steep penalties. You have much better, more strategic choices.

Each option comes with its own set of trade-offs regarding investment choices, fees, and overall control.

Here’s a breakdown of your main choices for that old 401(k) and what they really mean for you.

Comparing 401(k) Options After a Layoff

While no one welcomes a layoff, this period of unemployment creates a unique window for smart financial moves, like a Roth conversion, that can set you up for significant long-term success. As you map out your next move, whether it's finding a new role or exploring different income streams, taking control of your financial picture is key. If you're looking for your next career step, you might find these resources on the highest paid remote job opportunities helpful. By being proactive and informed, you can turn this career disruption into a catalyst for building a more resilient financial future.

Tailored Advice for Founders and Professionals After a Layoff

Cookie-cutter financial plans just don't cut it when high-net-worth individuals face a major career shift. For founders, business owners, and professionals with less predictable income—think athletes or entertainers—a layoff or a sudden drop in earnings demands a completely different playbook. The standard advice for a salaried employee simply won't work.

Entrepreneurs often live with a blurred line between their personal and business finances, and a sudden downturn can put both at risk. The very first priority is building a firewall between your personal assets and business liabilities. You have to ensure a professional crisis doesn't spiral into a personal financial catastrophe.

This means taking a hard look at your business structure (like an LLC or S-corp), any personal guarantees you’ve signed on business loans, and maybe even securing personal lines of credit before you’re in a tight spot. We get into the weeds on these specific strategies in our guide on wealth management for entrepreneurs.

Navigating Volatile Income Streams

Professionals in sports and entertainment grapple with a unique kind of volatility. Their careers often consist of short, incredibly high-earning windows, which can be followed by long stretches of uncertainty. When a contract ends, it’s not just a job loss; it’s a seismic shift in cash flow that requires a proactive plan.

The trick is to build a financial foundation strong enough to bridge those long gaps between projects or paychecks. This usually involves:

- Aggressive Savings During Peak Years: A much higher percentage of income needs to be socked away and invested to create a durable financial base for the future.

- Structured Cash Flow Management: We often advise creating different "buckets" for taxes, living expenses, and long-term investments. It helps bring discipline to otherwise sporadic, lump-sum payments.

- Post-Career Financial Modeling: Planning for a second act—whether it's starting a business, investing, or a new career entirely—has to start early.

The Founder’s Financial Pivot

Take the classic case of a tech founder whose company gets acquired, making their own role redundant. They might be sitting on a significant cash windfall from the sale, but their professional identity and steady income stream have just vanished. Their immediate challenge is figuring out how to redeploy that capital smartly, manage a concentrated stock position in the acquiring company, and map out their next venture without burning through their newfound liquidity.

This scenario has become all too common. After a massive hiring boom during the pandemic, the global technology sector saw a major contraction. In the first quarter of 2023 alone, tech companies announced a staggering 167,600 layoffs worldwide, a trend that has continued as the industry recalibrates. This volatility just hammers home why founders need a rock-solid personal financial strategy that exists independently of their company’s day-to-day success.

For those thinking about using this transition to jump into their own venture, a guide on how to start a business can be an invaluable resource. Ultimately, the right advice can help turn a period of intense uncertainty into a strategic opportunity for long-term growth.

Common Questions After a Layoff

When you're dealing with a layoff, a flood of questions comes right along with it. It’s natural. Below, we've tackled some of the most immediate concerns we hear from clients, reinforcing the concepts from this guide to help you move forward with clarity.

What Happens to My Unvested Stock Options or RSUs After a Layoff?

This is a big one. The answer lies deep in your company's stock plan and your separation agreement. In most cases, any unvested equity simply disappears when you leave.

But—and this is important—it doesn't always have to be that way. This is often a point of negotiation, especially for senior roles. You can absolutely make a case for accelerated vesting or at least partial vesting as part of your exit package. Make sure you dig up your original grant agreements and look for the "post-termination exercise period" for any options that have already vested. That window can be shockingly short, sometimes just 90 days.

Should I Take My Severance as a Lump Sum or as Continued Salary?

This choice has major tax and cash flow implications, so you need to think it through carefully. Taking a lump sum gives you all the cash upfront, which can feel secure. The downside? It can easily launch you into a much higher tax bracket for the year, meaning a nasty surprise from the IRS.

Salary continuation, on the other hand, spreads the payments—and the tax hit—out over time. This gives you a predictable stream of income, making it easier to budget while you figure out your next move. It might also keep you on the company's benefits plan for longer. Before you decide, you have to run the numbers on your immediate cash needs and model out the tax impact of both scenarios.

This is exactly where a financial advisor can be a huge help. They can project the after-tax reality of each option, making sure your decision is based on a sound financial strategy, not a gut reaction.

When Is the Right Time to Call a Financial Advisor After a Layoff?

Immediately. Don't wait. The ideal time to get in touch is as soon as you know a layoff is coming, even before you've signed any final paperwork.

An advisor brings a calm, objective perspective to what is an incredibly stressful time. Their expertise is critical for a few key reasons:

- Sizing Up the Severance Offer: They can help you see the real value of what's on the table and pinpoint where you might be able to negotiate for more.

- Navigating the Tax Minefield: They'll walk you through the tax consequences of different payout options and what to do with your equity.

- Making Smart Moves: They provide clear guidance on what to do with your 401(k), how to adjust your investments, and how to build a plan that protects you for the long haul.

What Are the Biggest Financial Mistakes to Avoid After a Layoff?

The weeks following a layoff are a minefield for potential financial blunders, most of which are driven by stress and emotion.

Steer clear of these common pitfalls at all costs:

- Panic-Selling Investments: It's tempting to react to the uncertainty by liquidating your portfolio, but selling into a down market just locks in your losses. Stick to your long-term strategy.

- Raiding Your 401(k): This is one of the most destructive financial moves you can make. You’ll get slammed with massive taxes and early withdrawal penalties, kneecapping your retirement savings in the process.

- Taking the First Severance Offer: Never assume the first offer is the best one. Always give yourself time to review it, understand it completely, and see where there's room to negotiate.

A successful transition is all about staying calm and being methodical. Build a budget, understand all your options, and get professional advice before you make any big decisions with your money.

Working through the complexities of a layoff requires an expert in your corner. At Commons Capital, we specialize in helping high-net-worth individuals and families manage major career and financial shifts with confidence. Let our team help you turn this challenge into a strategic opportunity. Contact us today to secure your financial future.