When you leave a job, one of the biggest financial decisions you'll face is what to do with your 401k. You have four main choices, and the path you take can significantly impact your retirement savings. You can leave it with your former employer, roll it over into an IRA, move it to your new job's plan, or cash it out. Each option has distinct rules and financial consequences, making it a critical decision to get right for your long-term financial health.

Your Four Main 401k Options After Leaving a Job

Leaving a job isn't just a career shift—it's a pivotal moment for your retirement strategy. The choice you make about your old 401k will create a ripple effect, influencing your long-term wealth, the control you have over your investments, and the ease of managing your overall portfolio.

Understanding these options is the essential first step. Let's break down the four main paths you can take with your old 401k.

Introducing the Core Strategies

- Leave It With Your Former Employer: Often the simplest choice, this is the "do nothing" option. If your old plan offers excellent, low-cost investment choices and your balance exceeds $5,000, you can usually leave your money where it is.

- Roll It Over to an IRA: An Individual Retirement Account (IRA) offers maximum freedom. A rollover allows you to consolidate your retirement savings into an account you fully control, opening up a vast universe of investment options like stocks, bonds, and ETFs.

- Move It to Your New 401k: If you're starting a new job with a 401k plan, you can often transfer the old account into the new one. This simplifies your financial life by keeping all your retirement funds in one place.

- Cash It Out: This means withdrawing the entire balance. While the idea of a lump-sum payment can be tempting, this option nearly always comes with a harsh combination of income taxes and early withdrawal penalties. It is rarely the best move for your financial future.

The decision of what to do with a 401k after leaving a job isn't just administrative—it's a strategic choice that impacts your investment control, fees, and long-term growth potential.

To help you see how these choices stack up, we've put together a quick comparison. Think of it as a cheat sheet to guide your thinking.

A Quick Comparison of Your 401k Choices

This table gives you the 30,000-foot view. Now, we'll get into the nitty-gritty of each option to help you figure out which strategy makes the most sense for your specific situation.

Leaving Your 401(k) With a Former Employer

When you leave a job, the path of least resistance is often to just leave your 401(k) behind. While that might feel like putting off a decision, it can actually be a smart, strategic financial move—if the circumstances are right.

This option is typically on the table as long as your account balance is above $5,000, which prevents your old employer from forcing you out of the plan. Staying put means you don't have to make any immediate moves, which can be a relief during a job change. But the real value isn't just about convenience; it’s about the unique features your old plan might offer.

When Staying Put Makes Financial Sense

Let’s be clear: not all 401(k) plans are created equal. Some plans, especially those from large corporations, provide access to investment options that you simply can't get as an individual investor.

These top-tier plans might include:

- Institutional-Class Funds: Think of these as the wholesale version of mutual funds. They come with exceptionally low expense ratios, which means more of your money stays invested and works for you. Over decades, these cost savings can be massive compared to the retail funds you'd find in a typical IRA.

- Unique Investment Vehicles: Some 401(k)s offer things like stable value funds or other specialized assets that aim for steady, reliable returns with low volatility. These can be incredibly valuable for a diversified portfolio, particularly as you get closer to retirement.

- Strong Fiduciary Protections: Your 401(k) is protected under the Employee Retirement Income Security Act of 1974 (ERISA). This federal law holds plan fiduciaries to a high standard, requiring them to act in your best interest. It also provides robust creditor protections that are often much stronger than what you'd get for an IRA under state law.

Choosing to leave a 401(k) with a former employer is a deliberate act of recognizing the unique, often superior, investment structure and legal protections that the plan offers over other available options.

Analyzing the Potential Downsides

While there are good reasons to leave an old 401(k) behind, it’s not without potential headaches. One of the biggest issues is the risk of creating a messy, fragmented retirement portfolio. If you move jobs every few years and leave a trail of old 401(k)s, it becomes a nightmare to manage your overall asset allocation and track your performance.

Communication can also become a problem. You're no longer an active employee, which can make it harder to get information, make changes, or start taking withdrawals. You’re also stuck with the investment menu of the old plan, which might not fit your financial goals down the road.

The average 401(k) balance varies wildly by age, from around $7,000 for workers in their 20s to over $300,000 for those nearing retirement. Keeping track of multiple accounts of different sizes just gets more complicated over time. This complexity is exactly why a consolidation strategy is usually a good idea—unless a specific plan offers compelling reasons to stay. You can find more about typical retirement savings benchmarks on Bankrate.com.

Ultimately, the decision comes down to a careful cost-benefit analysis. You have to weigh whether the unique funds and stronger protections of your old plan are valuable enough to outweigh the inconvenience and lack of flexibility. For some high-net-worth individuals, the access to institutional-grade investments alone makes it the superior choice.

Taking Control with a Strategic 401(k) Rollover to an IRA

For anyone who wants to take a more hands-on approach with their retirement money, rolling an old 401(k) into an Individual Retirement Account (IRA) is a powerful move. It’s easily the most popular answer to the "what to do with my old 401(k)" question, mainly because it unlocks a level of control and flexibility that you just can't get in an employer's plan.

The biggest win here is the massive expansion of your investment universe. A typical 401(k) might give you a dozen or so mutual funds to choose from, but an IRA throws the doors wide open. Suddenly, you can invest in individual stocks, bonds, ETFs, real estate investment trusts (REITs), and in some cases, even alternative assets. This freedom lets you build a portfolio that’s truly dialed into your personal risk tolerance and financial goals.

Understanding Your IRA Rollover Choices

When you make the move, you have two primary destinations for your money:

- Traditional IRA: If your 401(k) contributions were pre-tax, they can slide right into a Traditional IRA without triggering a tax bill. The money keeps growing tax-deferred, and you’ll pay income taxes on withdrawals when you retire.

- Roth IRA: You also have the option to move the funds into a Roth IRA. This is called a Roth conversion, and it’s a taxable event. You'll owe income tax on the entire amount you convert for the current year. The trade-off is huge, though: all qualified withdrawals in retirement are 100% tax-free.

Deciding between a Traditional and Roth IRA really boils down to your tax situation. If you think you'll be in a higher tax bracket down the road, paying the taxes now with a Roth conversion can be an incredibly savvy long-term play.

A direct rollover is the cleanest and safest way to do this. The money goes straight from your old 401(k) plan to your new IRA custodian, which lets you sidestep the mandatory 20% tax withholding and potential penalties that come with an indirect rollover (where they send you a check).

Weighing the Potential Drawbacks

While an IRA rollover has some serious perks, it's not a one-size-fits-all solution. One key thing you give up is the robust creditor protection that comes with a 401(k). Those plans are covered by federal ERISA law, which offers strong, uniform protection from creditors. IRAs, however, fall under state laws, which can be a mixed bag. You can learn more about exactly how IRAs are protected from creditors in our detailed article.

Another thing to remember is that once the money is in an IRA, you can no longer take out a 401(k) loan against it. While you should only use those loans as a last resort, they can be a useful option in a true financial emergency. For federal employees, figuring out how to roll over a TSP to an IRA involves many of the same strategic considerations.

The table below breaks down the major differences between rolling over and leaving your money where it is.

IRA Rollover vs Leaving in Old 401k

This side-by-side analysis cuts to the chase, comparing the crucial differences in investment options, fees, and protections when you’re on the fence.

Ultimately, a strategic rollover is about taking direct command of your retirement assets. For the disciplined investor, the unparalleled choice and customization often outweigh the loss of 401(k)-specific features like loans and federal creditor protections. It's a move toward a more personalized and proactive retirement strategy.

Consolidating Into Your New Employer's 401k

For anyone who values simplicity in their financial life, deciding what to do with an old 401k often has one clear answer: consolidate it by rolling it into your new employer's plan.

This is a straightforward way to keep all your retirement assets under one roof, making it much easier to track your portfolio, rebalance your investments, and see a complete picture of your retirement savings.

This move is especially powerful when your new plan is a significant upgrade from your old one. A superior 401k plan can dramatically accelerate your long-term growth.

When Consolidation Is a Smart Financial Move

Let's be clear: not all 401(k) plans are created equal. Getting into a better one can put your retirement savings on the fast track. You should give this option a hard look if your new employer’s plan has some compelling perks.

Here are the key features you should be looking for:

- Lower Administrative and Investment Fees: It might not sound like much, but even a small difference in fees can compound into tens of thousands of dollars over a career. If the new plan has lower expense ratios, that's a major win.

- A Superior Investment Menu: Your new plan might offer a wider, higher-quality lineup of investments. Think low-cost index funds, target-date funds that match your timeline, or even access to entirely different asset classes.

- Valuable Plan Features: Some modern 401(k)s come with extras like professional advisory services, financial wellness tools, or the ability to take out a 401(k) loan—a feature you'll lose if you roll the money into an IRA.

Consolidating into a new 401(k) isn't just about making life easier. It's a strategic move to get your money into a plan with better tools, lower costs, and more powerful investment options.

Scrutinizing Your New 401k Plan

But hold on—this isn't a decision you should make on autopilot. You have to do your homework on the new employer's plan before you move a dime. A blind rollover could mean shifting your life savings into a plan with higher fees or a lousy investment lineup, which would be a huge financial mistake.

Before you start any paperwork, get a copy of the new plan's documents and fee disclosures. You need to sit down and compare its investment options, expense ratios, and any administrative fees against what you've got in your old plan. If the new plan is more expensive or the fund selection is lackluster, you're probably better off leaving the money where it is or thinking about an IRA rollover instead.

Employer contributions are the secret sauce of 401(k) growth. Data shows over 90% of people in large plans get some kind of employer match, a critical part of building wealth. While your new match only applies to new money you put in, the quality of the plan itself will dictate how your rolled-over funds grow.

It's surprising how many people don't know the details of their own plans; fewer than 40% of Americans can answer basic questions about 401(k) rules. By carefully vetting the new plan, you put yourself in a position of strength. To dig deeper, you can find more key insights on 401k plans and participation from the Investment Company Institute. This simple act of diligence ensures your consolidated retirement funds will work as hard for you as possible.

The True Cost of Cashing Out Your 401(k) Early

Tapping your 401(k) after leaving a job often gets filed under "break glass in case of emergency." There's a good reason for that. While a sudden lump sum of cash can feel like a lifeline during a tough transition, pulling the trigger comes with brutal, often overlooked, financial penalties that can permanently hobble your retirement.

This isn't just a simple withdrawal. It's an act that sets off a chain reaction of taxes, fees, and a colossal loss of future growth. Anyone weighing their 401(k) options needs to understand exactly what’s at stake.

The Immediate Financial Hit

When you cash out your 401(k) before age 59½, you're in for an instant and painful haircut. The IRS doesn't just let you walk away with the full balance.

Here’s how it breaks down:

- A Mandatory 20% Federal Tax Withholding: Right off the top, your former employer is legally required to withhold 20% of your balance for federal income taxes. On a $50,000 account, that means the check you get is only for $40,000.

- A 10% Early Withdrawal Penalty: On top of that, the IRS slaps on a 10% penalty for most early distributions. This is an extra tax you'll have to settle up when you file for the year.

- State Income Taxes: Don't forget about your state. Depending on where you live, you could owe state income taxes on the withdrawal, shrinking your take-home amount even further.

Cashing out a 401(k) doesn't just stop future growth; it actively shrinks your current net worth through a combination of mandatory tax withholdings and penalties, often costing you 30% or more of your savings right off the bat.

The Hidden Cost of Lost Compound Growth

The most devastating blow from cashing out isn't the immediate tax bill—it's the opportunity cost. You’re not just spending your savings; you're killing decades of potential tax-deferred compound growth. This is the real, hidden cost that can wreck a retirement plan.

Let’s run the numbers. Picture a 35-year-old with a $50,000 401(k). If they cash out, they might only see $35,000 after all the taxes and penalties. But what if they left that $50,000 alone to grow?

Historical data suggests 401(k) investments have averaged annual returns around 8.0%. At that rate, the original $50,000 could swell to over $342,000 by the time they hit 60. By cashing out, they didn't just lose $15,000 today—they forfeited nearly $300,000 in future retirement money. You can explore more about these potential investment returns on Fidelity's website.

While a true financial crisis can make this option feel like the only one, it should be the absolute last resort. Every other avenue—from personal loans to serious budget cuts—should be explored before you sacrifice the foundation of your financial future. The long-term damage is simply too great to ignore.

How to Choose the Right 401k Strategy for You

When you leave a job, you hit a major financial fork in the road: what to do with your 401(k). Once you know the pros and cons of each path, you can make a move. The right choice is deeply personal and hinges on your confidence as an investor, how you feel about fees, and what your long-term goals look like.

There’s no one-size-fits-all answer here. A young professional who enjoys managing their own portfolio might jump at the chance to roll their 401(k) into an IRA, where the investment options are nearly limitless. On the other hand, someone closer to retirement might prefer to stick with their old 401(k) to keep access to unique, low-cost institutional funds or stable value funds, prioritizing safety over selection.

Asking the Right Questions

To figure out your next step, you need to be honest about your financial personality and what you want to achieve. A few key questions can guide you to the right decision.

Run through this checklist to get a clearer picture of your priorities:

- How hands-on do I want to be? If you love the idea of researching funds and building your own portfolio from scratch, an IRA rollover gives you that control. If you'd rather set it and forget it, rolling your old account into your new 401(k) is probably your best bet.

- How much do fees matter to me? This is a big one. You need to compare the expense ratios in your old and new 401(k) plans against what you’d pay in a typical IRA. Over decades, even a tiny difference in fees can add up to tens of thousands of dollars in lost growth.

- Do I need to access this money before I retire? Don't forget that 401(k)s often allow for loans, but IRAs do not. That's a critical difference if you think you might need to tap into those funds down the road.

- What's my new 401(k) plan actually like? Don't just assume the new plan is an upgrade. Take a hard look at its investment options, fees, and any special features before you decide to move your money over.

To make an informed choice, it helps to have a solid grasp of the fundamentals. If you're just getting started, a primer on how to start investing as a beginner can be invaluable.

Understanding the Financial Stakes

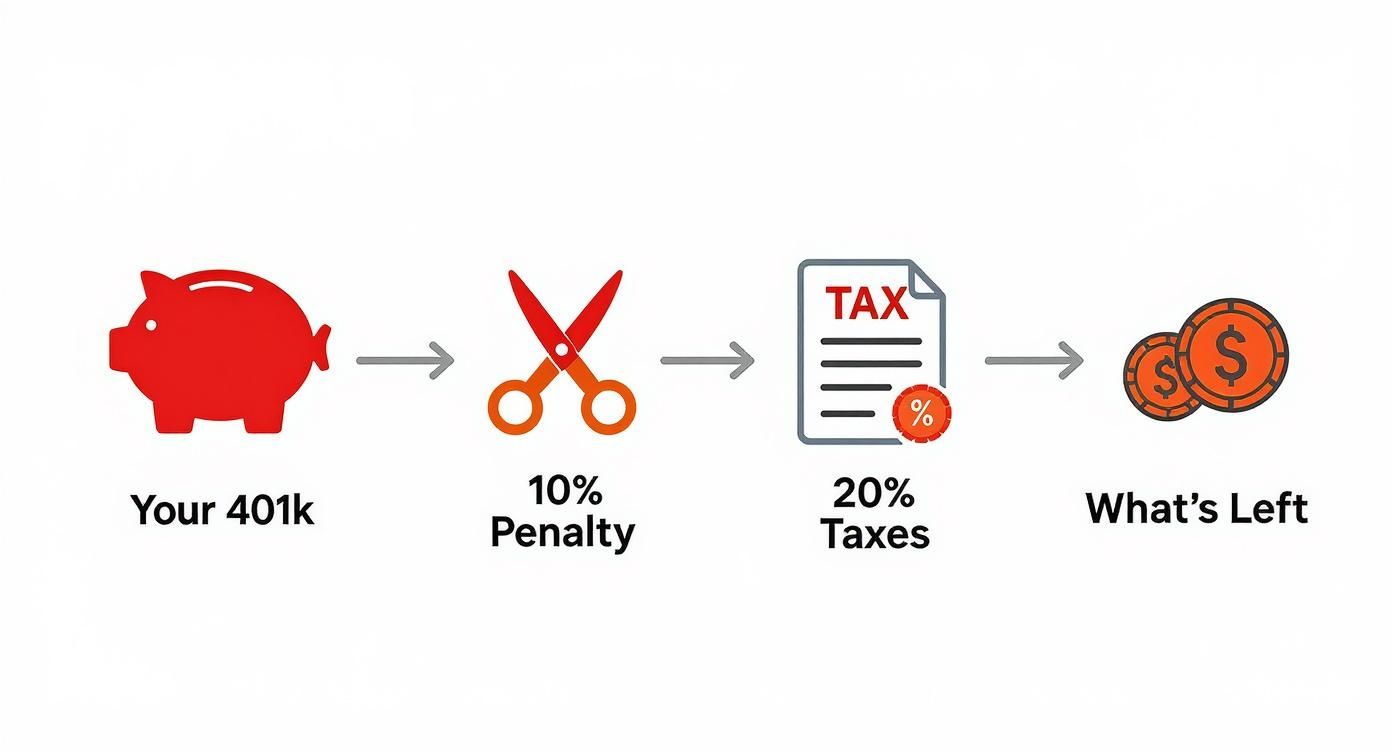

Beyond just your personal preferences, it’s crucial to understand the real-world financial impact of each option. Cashing out, for example, comes with immediate and harsh consequences that can completely throw your retirement off track.

This visual breaks down how penalties and taxes immediately take a bite out of your savings if you cash out a 401(k) early.

As you can see, a 10% penalty on top of a mandatory 20% federal tax withholding means you could lose nearly a third of your money right off the bat—and that doesn't even account for state taxes.

The best 401(k) strategy is not just about maximizing future returns; it’s about aligning your retirement assets with your life goals, risk tolerance, and desire for simplicity or control.

At the end of the day, your decision needs to fit into your bigger financial picture. This means thinking about how your 401(k) funds work with your overall asset allocation and your long-term retirement withdrawal strategies. By weighing these factors carefully, you can confidently pick the 401(k) strategy that will best support you on the path to a secure retirement.

Your Top 401(k) Questions, Answered

When you change jobs, a whole new set of questions about your old 401(k) inevitably crops up. Let's cut through the noise and get you some direct answers so you can move forward with confidence.

How Do I Start a Direct Rollover?

Kicking off a direct rollover is usually pretty straightforward. Your first move is to open the account where you want the money to land—this could be an IRA at a brokerage or the 401(k) plan with your new company.

Once that new account is ready to go, you’ll get in touch with your old 401(k) plan administrator. They'll hand over the paperwork needed to greenlight the transfer. In a direct rollover, the money moves straight from your old plan to the new one, which is exactly what you want to avoid any tax headaches.

Can I Have Multiple 401(k) Accounts?

Yes, you absolutely can. It's perfectly legal to have multiple 401(k) accounts from various jobs you’ve held over the years.

But just because you can doesn't always mean you should. Juggling several different plans can get complicated fast, making it a real challenge to stick to a unified investment strategy or even just track your performance. It's why so many people opt to consolidate old 401(k)s into a single IRA or their current employer's plan.

Leaving old 401(k) accounts scattered across former employers often leads to a messy portfolio and higher fees, which can slowly eat away at your long-term retirement goals.

What Happens if My 401(k) Balance Is Under $5,000?

If your vested 401(k) balance is less than $5,000 when you leave a job, your old employer can legally push you out of their plan. They won't just pocket the money, but they can trigger what's called a force-out rollover.

For balances between $1,000 and $5,000, the plan administrator will typically roll your funds into a default IRA they set up for you. If your balance is under $1,000, they might just cash you out and mail a check—a move that could land you with an unexpected tax bill and penalties. It’s always better to take control and make the decision yourself.

Can My Beneficiaries Inherit My 401(k)?

They sure can. Your designated beneficiaries are in line to inherit your 401(k), but the rules and tax implications can get tricky. Getting a handle on the specifics is a key part of smart estate planning, and you can dive deeper into the inheritance tax on a 401(k). Simply making sure your beneficiary information is current is one of the most powerful things you can do for your account.

Figuring out what to do with your 401(k) is one of those big financial crossroads. At Commons Capital, we guide high-net-worth individuals through these decisions, ensuring their retirement assets are aligned with their complete financial picture. Contact us today to ensure your retirement assets are positioned for optimal growth.