Knowing how to diversify investments before a recession means more than just sprinkling your money across different stocks. It’s a deliberate, strategic shift toward assets that can actually hold their ground when the economy starts to wobble. This guide will provide a comprehensive answer to your questions about building a resilient portfolio for uncertain times.

This isn’t about timing the market perfectly. It’s about recognizing the signs and proactively trimming your exposure to high-flying, speculative names while beefing up your allocation to quality. Think stable, dividend-paying companies and defensive workhorses like government bonds and certain alternatives. This kind of rebalancing is what protects your capital when volatility spikes.

Your Pre-Recession Diversification Playbook

With economic indicators flashing yellow, the smart move is preparation, not panic. Many investors rely on outdated diversification models that aren't built for the pressures of a modern downturn. What you need is a forward-thinking framework designed to build a truly resilient portfolio, a key part of any pre-recession investment strategy.

The whole game plan revolves around a calculated shift toward durability. It all starts with a brutally honest look at your own risk tolerance, followed by a thorough stress test of your current holdings. This is where you find the weak spots — the parts of your portfolio most vulnerable to a slowdown. Before you can build a solid defense, you first need to master the fundamentals of how to diversify your investment portfolio.

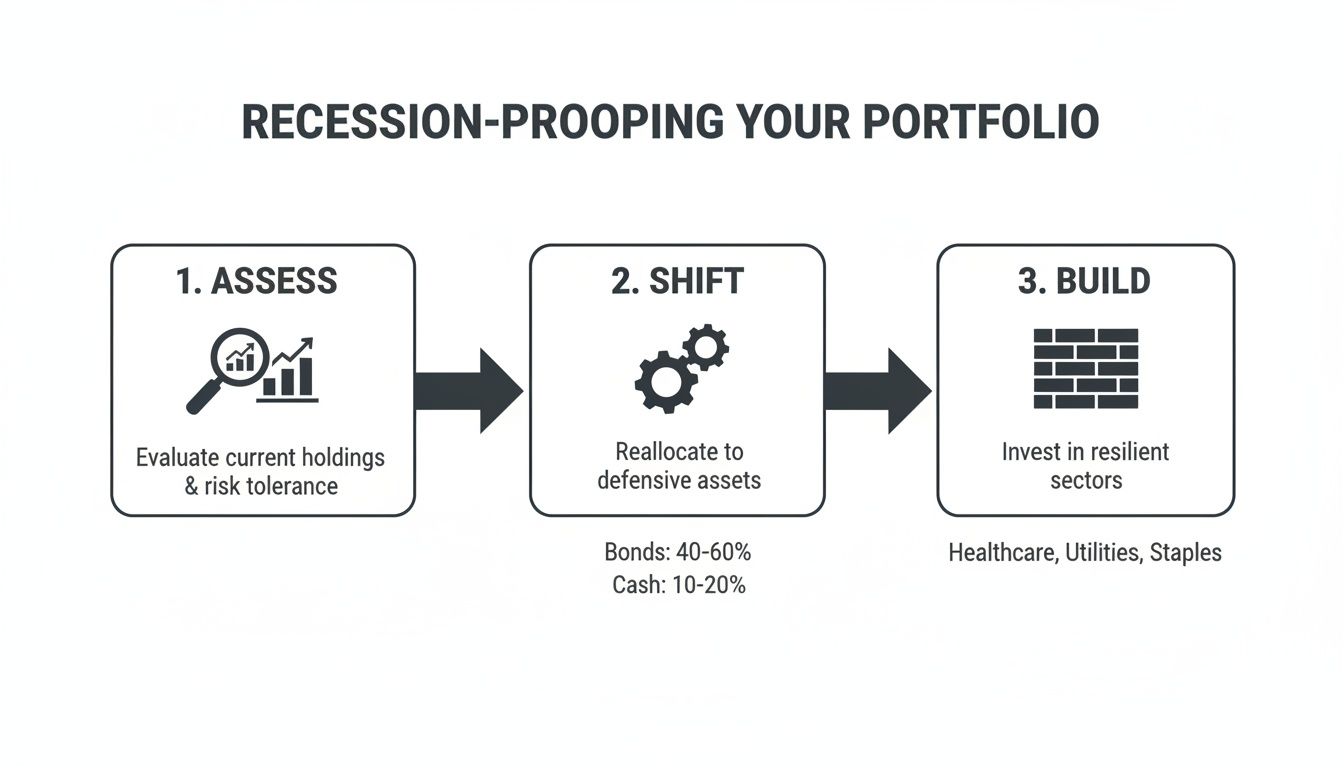

Key Strategic Shifts To Consider

Pivoting from a growth-at-all-costs mindset to a more defensive posture doesn't mean you have to run for the hills and exit the market. It’s about making smart, calculated adjustments. History gives us a pretty clear roadmap here, showing that certain sectors and asset classes tend to fare much better when consumers start pinching pennies and uncertainty is in the air.

This is where a real-world approach to portfolio adjustments comes into play. It’s about making specific changes that reflect the new economic reality.

Key Diversification Shifts for a Pre-Recession Portfolio

To prepare for a potential downturn, it’s helpful to visualize the specific adjustments you might make. The table below outlines how a typical portfolio strategy might shift to a more defensive, pre-recession stance.

These shifts aren't about abandoning your long-term goals; they're about ensuring your portfolio is durable enough to reach them. By thoughtfully repositioning, you're building a buffer against volatility.

This guide will walk you through these critical adjustments, laying out a clear roadmap for protecting your wealth. We’ll dive into the specifics of how to:

- Rebalance Your Stock Holdings: Move capital from economically-sensitive growth stocks toward stable, non-cyclical sectors like consumer staples and healthcare.

- Fortify Your Fixed Income: Upgrade your bond portfolio by prioritizing high-quality government and corporate debt over riskier high-yield bonds.

- Embrace True Alternatives: Explore assets like gold, real estate, and specific hedge fund strategies that often zig when the broader stock market zags.

A well-diversified economy, much like a well-diversified portfolio, tends to experience less volatility and more consistent growth over time. This principle of economic resilience is directly applicable to personal wealth management, especially when preparing for a downturn.

By internalizing these strategic shifts, you can reposition your assets to not only ride out a potential storm but also to be in a prime position for the eventual recovery. The next sections will give you a detailed framework to put this playbook into action.

Stress-Testing Your Current Investment Portfolio

Before you make a single move, you need an honest, unflinching look at your portfolio's weak points. Think of it as a pre-flight check in turbulent skies. Too many investors get a nasty surprise during a downturn, discovering the assets they thought were diversified were actually moving in lockstep.

A real stress test isn't just a quick glance at your holdings. It’s a deep dive. We’re talking about digging into your sector concentrations, your geographical exposures, and just how sensitive your investments are to big economic shifts like rising interest rates. Getting this right is the foundation of any solid recession-proofing strategy, and it starts with mastering portfolio valuation to see where you truly stand.

Simulating Past Economic Crises

One of the most powerful things you can do is run your portfolio through the gauntlet of history. How would your exact mix of stocks, bonds, and alternatives have held up during the 2008 global financial crisis? What about the dot-com implosion of the early 2000s? This isn't just some academic exercise; it reveals hidden risks in plain sight.

You might discover your tech-heavy stock allocation would have been absolutely decimated in 2001. Or maybe those "safe" bonds you're holding are packed with corporate debt that would've been junk-rated overnight in 2008.

These simulations, whether run with sophisticated software or with your financial advisor, pinpoint the specific holdings likely to drag you down. This lets you make surgical adjustments instead of panicked, wholesale changes.

The whole idea is to systematically assess your weak spots, shift your allocation, and build a more resilient structure for what’s ahead.

This flow from assessment to resilience isn't just a nice graphic — it's the disciplined approach required to truly prepare your investments for the storm.

Evaluating Concentration and Correlation Risk

Next up: concentration risk. It's a classic mistake. Are you way too heavy in a single industry, one or two companies, or a specific country? You might own 50 different stocks, but if they're all in the tech sector, you're not diversified. You're just making a concentrated bet.

And you have to look for the less obvious connections, too. For instance, luxury retail brands and high-end hotel chains might seem unrelated, but both get hammered when consumers slam their wallets shut. Finding and trimming these hidden correlations is crucial for building a portfolio that can actually withstand widespread economic pain.

A common blind spot for investors is underestimating how interconnected their assets become during a crisis. In a true market panic, correlations often converge toward one — meaning assets that seemed unrelated suddenly move in lockstep, erasing the benefits of superficial diversification.

Assessing Your Liquidity Needs

Finally, let's talk about cash. In a recession, cash isn't just a boring, defensive play — it's a powerful, strategic weapon. Having enough liquidity on hand is what keeps you from being forced to sell your best assets at fire-sale prices just to cover expenses.

Figure out what you need to live on for the next 12-24 months, and make sure that amount is sitting in something safe and easily accessible, like a high-yield savings account or short-term T-bills. This cash buffer gives you peace of mind. More importantly, it gives you the dry powder to scoop up incredible opportunities when everyone else is panicking.

The ability to ride out a downturn without touching your core long-term holdings is often what separates the winners from the losers.

Rebalancing Your Equities for Market Resilience

When storm clouds gather on the economic horizon, the gut reaction for many is to dump all their stocks. While it’s true that equities often take the first and hardest hit in a recession, a complete fire sale is almost never the right call. The smarter move? An intelligent rebalance.

Think of it as a strategic pivot, not an exit. We’re looking to add resilience to your portfolio without totally giving up on the long-term growth that stocks provide. It’s a core part of how to diversify investments before a recession, and it's less about timing the market and more about fortifying your positions for what’s to come.

The objective is to shift your equity holdings from an all-out offensive posture to a more defensive one. This means trimming exposure to the high-flying, speculative growth stocks that need a roaring economy to thrive and rotating that capital into companies built to last.

Shifting to Defensive Sectors and Quality Companies

When times get tough, people change how they spend money. Suddenly, that luxury vacation or designer handbag gets put on the back burner, but the grocery bill and the electric bill still get paid. This predictable shift in behavior gives us a clear roadmap for rebalancing our stock holdings.

It’s time to consider reducing your stake in cyclical sectors — think technology, consumer discretionary, and industrials — and beefing up your allocation to the defensive players.

- Consumer Staples: We’re talking about the companies that sell things we buy no matter what: food, drinks, soap, toothpaste. Think Procter & Gamble or Coca-Cola. Demand for their products is what economists call "inelastic" — it just doesn't change much, recession or not.

- Healthcare: People get sick and need medicine in good times and bad. From big pharma to hospital operators, these companies tend to have remarkably stable revenue streams that aren't tied to the economic cycle.

- Utilities: The lights have to stay on. Water, gas, and electricity are non-negotiable expenses for pretty much everyone. As a bonus, utility companies are often reliable dividend payers, which can provide a welcome stream of income when stock prices are flat or falling.

Beyond just the sector, you need to zero in on quality. Look for businesses with bulletproof balance sheets, very little debt, a long track record of consistent earnings, and a history of not just paying, but growing their dividends. These are the "blue-chip" market leaders that have seen a recession or two before and lived to tell the tale.

Using Factor Investing to Build a Buffer

If you want to get a bit more sophisticated, you can fortify your portfolio using factor investing. This isn't about picking individual stocks. Instead, it’s a strategy that involves tilting your portfolio toward specific, proven drivers of return, known as "factors."

Think of factor investing as adding a layer of statistical defense to your equity allocation. You're systematically leaning into characteristics that have historically held up better when the market gets choppy.

History shows that certain factors really shine when investors get nervous. Looking at U.S. market data going all the way back to the 1920s, the Momentum factor (stocks with strong recent performance) actually delivered an annualized excess return of +6.7% in the five months leading up to a recession.

Once the recession officially hits, the story changes. Factors like Investment (companies that are conservative with their capital), Quality, and Profitability have all historically outperformed the broader market, which on average posted a -4.2% decline. You can dive into the numbers yourself by reviewing the in-depth research on factor performance.

The key defensive factors to focus on are:

- Quality: High-quality companies with stable earnings and low debt.

- Low Volatility: Stocks that simply don't swing up and down as wildly as the overall market.

- Momentum: Stocks that have been demonstrating a strong upward price trend.

By incorporating ETFs or mutual funds that are built around these factors, you can methodically dial down your portfolio's sensitivity to a market downturn. This isn't just about playing defense; it’s a disciplined approach that positions you to capture opportunities when the recovery eventually begins. If you're looking for a deeper dive into the mechanics, our guide on what is portfolio rebalancing breaks down the entire framework.

Fortifying Your Portfolio with Bonds and Alternatives

So, you’ve trimmed some of the risk from your stock holdings. The big question now is, where does that money go? The classic move is to fortify your portfolio with high-quality bonds and a smart allocation to alternatives. This isn't just about playing defense; it's about building a ballast that can steady the ship when the market waters get rough.

But "just buy bonds" is terrible advice. The devil is truly in the details. When the economy is flashing warning signs, not all bonds are created equal, and not all alternatives are the safe havens they claim to be. You need a clear-eyed strategy to build a multi-layered defense that preserves capital, generates some income, and holds its ground when your growth assets are taking a hit.

The Strategic Role of Fixed Income

As we edge closer to a potential recession, the job of your bond portfolio changes. It’s less about chasing high yields and more about capital preservation and stability. The number one priority? Credit quality. In a downturn, the risk of companies defaulting on their debt shoots up, which can hammer high-yield (or "junk") bonds.

The smart money rotates into the safest corners of the fixed-income world:

- U.S. Treasury Securities: There's a reason they're called a "safe haven." T-bills, notes, and bonds are backed by the full faith and credit of the U.S. government, making them the gold standard for safety.

- Investment-Grade Corporate Bonds: This isn't the time for speculation. Stick to debt from rock-solid companies with healthy balance sheets and predictable cash flows (think ratings of BBB or higher).

- Municipal Bonds: If you’re in a higher tax bracket, high-quality "munis" can be a fantastic source of tax-free income and relative stability. We've actually gone into more detail on whether municipal bonds are a good investment in another article.

Another piece of the puzzle is duration, which is just a measure of a bond's sensitivity to interest rate changes. Short-duration bonds offer more stability because they’re less affected by rate swings. On the flip side, long-duration government bonds often rally hard when the Fed starts cutting rates during a recession, giving you a powerful hedge against falling stocks. Many experienced investors use a "barbell strategy" — holding both short- and long-duration bonds — to get the best of both worlds.

Embracing Alternatives for True Diversification

If you want a truly diversified portfolio, you need assets that don't just zig when the stock market zags. This is where alternatives come in. Their whole purpose is to have a low correlation to traditional markets, smoothing out your returns when things get ugly.

Gold and other precious metals are the classic example. Gold has been a "safe-haven" asset for centuries, and its value often climbs when fear grips the market. Think of it as an insurance policy against a flight from risk.

Then you have real assets — tangible things that have intrinsic value.

- Recession-Resistant Real Estate: While the housing market as a whole might get shaky, certain pockets are incredibly durable. Think multifamily housing (people always need a roof over their heads), self-storage (demand often picks up when people downsize), and healthcare facilities.

- Infrastructure: Assets like toll roads, airports, and utilities are the backbone of the economy. They provide essential services and generate steady, predictable cash flows, making them far less vulnerable to the economic cycle.

A well-structured alternatives sleeve does more than just play defense. It aims to generate returns that are independent of the broader market's direction, providing a source of growth even when traditional assets are struggling.

Incorporating Market-Neutral and Hedged Strategies

For those with a higher tolerance for complexity, market-neutral or absolute return strategies can add another powerful layer of protection. These strategies, typically found in hedge funds or specialized liquid alt funds, use tools like short-selling to aim for positive returns no matter which way the market is heading.

A well-designed allocation to alternatives can make a huge difference. One playbook we've seen work well suggests putting 20% into alternatives: 10% in absolute return funds, 5% in hedged equities, and 5% in niche risks. This kind of diversification proved its worth during the sharp 2020 recession, where alternatives actually beat bonds by 3%. A portfolio structured this way can navigate downturns with 10-15% less volatility, putting you in a much stronger position to recover quickly on the other side.

Advanced Hedging and Tax-Aware Strategies

When you're managing significant wealth, simple diversification just doesn't cut it. A sharp downturn can still inflict serious damage. That’s when the conversation needs to shift to more specialized tactics for recession-proofing your investments.

This is where we get into the nitty-gritty of advanced hedging and tax-aware maneuvers. Think of these as more than just asset allocation; they are structural safeguards and proactive tax management designed to build a robust defense for substantial portfolios. For high-net-worth families and family offices, getting this right is non-negotiable for preserving wealth through the cycle.

Implementing Sophisticated Hedging Techniques

Let's be clear: hedging is a form of financial insurance. It comes with a cost, but it can be the difference between a painful drawdown and a catastrophic one. The point isn't to sidestep all risk — that's impossible — but to put a firm boundary on your potential losses.

A straightforward way to do this is with options contracts. For instance, buying put options on a major index like the S&P 500 effectively creates a "floor" for your equity exposure. If the market tanks past your strike price, the gains from those puts can help cushion the blow to your stock holdings.

A well-executed hedging strategy provides more than just downside protection; it offers the clarity and confidence to stay invested through a downturn, preventing emotional decisions that can derail a long-term financial plan.

History shows us that once the initial shock of a recession wears off, certain alternative strategies, like absolute return hedge funds, have often outpaced traditional safe havens. Their expected returns can be 2-5% higher annually, offering both a shield and a source of positive performance.

Look at the 2008 financial crisis. The S&P 500 plummeted by 37%, but hedged equity managers managed to limit their clients' losses to an average of just -15%. It's a powerful demonstration of what active volatility management can achieve. The team at Partners Capital has a great recession playbook that dives deeper into these kinds of numbers.

Leveraging Private Investments for Defense

Most people think of private investments for their growth potential, but they can be incredibly defensive too. Private credit, in particular, acts as a fantastic stabilizer. These are direct loans to companies, and they often carry floating interest rates. That's a huge advantage when central banks are hiking rates to fight inflation — a classic recession precursor.

Because these assets aren't traded on public exchanges, they’re insulated from the daily mood swings of the stock and bond markets. This delivers a stream of steady, predictable income and much lower volatility, serving as a reliable anchor when everything else feels chaotic.

Other private assets that build resilience include:

- Recession-Resistant Real Estate: Think about sectors where demand doesn't just disappear in a downturn. Multifamily housing, self-storage facilities, and healthcare properties all provide stable cash flow when the broader economy is on shaky ground.

- Infrastructure: Essential assets like toll roads and utilities operate on long-term, inflation-linked contracts. Their revenue streams are largely disconnected from the typical business cycle.

These private market positions offer a type of diversification you simply cannot replicate in public markets alone.

Executing Crucial Tax-Aware Maneuvers

Smart tax planning isn't an afterthought; it's a core part of defending your wealth. In fact, a market downturn presents some of the best opportunities to improve your portfolio's tax efficiency for years to come.

The undisputed champion here is tax-loss harvesting. It’s a simple concept: you strategically sell investments that are down to "realize" the loss for tax purposes. These losses can then be used to offset capital gains you might have elsewhere, directly lowering your tax bill. The trick is to immediately reinvest the cash into a similar — but not identical — asset to stay in the market. If you really want to dial this in, it's worth exploring the different tax-loss harvesting strategies available.

Another key move is strategic asset location. This is all about putting your assets in the right type of account. Tax-inefficient holdings — like high-yield bonds or certain actively managed funds that churn out gains — should live in tax-advantaged accounts like a 401(k) or IRA. Conversely, tax-efficient investments like index funds or municipal bonds are better suited for your taxable brokerage accounts. Getting this alignment right can dramatically reduce the tax drag on your returns over the long haul.

Putting Your New Strategy to Work — And Sticking With It

Getting your recession game plan on paper is a huge first step. But a brilliant strategy is worthless without disciplined execution. This is where the real work begins — moving from theory to action and making sure your plan can actually withstand the psychological storm of a market downturn.

The whole point is to shift from making emotional, gut-wrenching decisions to following a systematic, rules-based process. You need a clear framework that tells you when and why to make changes. This prevents fear or greed from hijacking your portfolio when market stress is at its peak.

A Smarter Way to Rebalance

Forget blindly rebalancing your portfolio just because the calendar says it's the end of the quarter. In the volatile lead-up to a recession, that's just not dynamic enough. A much better approach is to set up a trigger-based, or tolerance-band, rebalancing schedule.

Here’s how it works: you set your target allocations and only step in to make a trade when an asset class drifts too far from its goal. For instance, if you've targeted a 50% allocation to equities, you might set a rule to rebalance only if it climbs to 55% or drops to 45%. This method forces you to systematically trim your winners and buy more of what's been beaten down — a classic "buy low, sell high" discipline, automated.

Building an Unshakeable Mindset

Let's be honest. The biggest threat to your portfolio during a recession isn't the market — it's you. Watching your account balance drop can rattle even the most experienced investors. That's why fortifying your mindset is every bit as important as fortifying your portfolio.

The real battle in a downturn is behavioral. A solid governance framework is your circuit breaker, forcing you to pause and think logically when every instinct is screaming "sell everything!"

This is exactly why having a formal Investment Policy Statement (IPS) is a non-negotiable. Think of it as your personal financial constitution. It’s a written document that locks in your goals, risk tolerance, and the rules of engagement for managing your money. When a crisis hits, you pull out the IPS to remind yourself of the long-term plan you made with a clear, unemotional head.

For the equity portion of your portfolio, one proven technique to build resilience is by tilting toward specific factors. For example, you could construct a portfolio with a 30% allocation to Momentum, 30% to Quality, and 20% to the Investment factor, with the rest in a broad market index. This kind of structure can cut volatility by 15-20% compared to a standard index. But the plan doesn't stop there. Crucially, it must also include a trigger to rotate back into factors like Size and Value after the recession, as they have historically led the charge in a recovery. You can dig into the in-depth research on how these factors perform to see the data for yourself.

Common Questions About Pre-Recession Portfolio Strategy

When you see a potential downturn on the horizon, a lot of questions pop up. It's only natural. Let's tackle some of the most common ones I hear from investors trying to figure out how to diversify investments before a recession.

What Investments Are Actually "Recession-Proof"?

Look, no investment is a magic bullet that's completely immune to a downturn. But some assets are incredibly resilient and tend to hold their ground far better than others.

Based on what we've seen in past cycles, you'll want to focus on areas that cater to non-negotiable needs:

- Consumer Staples: Think about it — people will always need to buy food, soap, and toilet paper, regardless of what the economy is doing. Companies in this space have remarkably stable demand.

- Healthcare: Medical needs don't just vanish in a recession. Demand for pharmaceuticals and essential health services stays pretty constant.

- High-Quality Government Bonds: U.S. Treasuries are the classic "flight to safety" asset. When fear is high, investors pile into them, seeking security.

- Gold and Precious Metals: Gold, in particular, has a long history as a store of value when confidence in currencies or the broader economy wanes.

- Certain Types of Real Estate: Not all property is created equal here. We're talking about assets tied to essential needs, like multifamily housing (people always need a place to live) and self-storage units. Fun fact: during the 2008 downturn, demand for self-storage actually went up as people downsized their homes.

How Much Cash Should I Be Holding?

Having enough cash on hand before a recession is crucial. The old rule of thumb — and it’s a good one — is to have 12 to 24 months of living expenses tucked away in cash or very safe, liquid equivalents like short-term Treasury bills.

This cash reserve does two incredibly important things for you. First, it's your emergency buffer, preventing you from ever being forced to sell your long-term investments at the worst possible time just to cover a surprise expense. Second, it's your "dry powder." When markets are panicking and quality assets go on sale, this is the capital you can deploy to seize those rare opportunities.

Should I Just Sell All My Stocks and Wait It Out?

This is probably the most tempting — and most dangerous — idea out there. Trying to time the market by selling everything is a losing game. It almost never works.

A complete exit from the market means you have to be right twice: when to sell and when to get back in. Historically, the market's best days often occur shortly after its worst, and missing that rebound can severely damage long-term returns.

A much smarter move is to rebalance your portfolio defensively. This means you stay in the market but shift your focus. You might trim positions in high-flying, cyclical growth stocks and move that capital into high-quality, dividend-paying companies in more stable sectors, like utilities and consumer staples.

This pivot lets you ride out the storm with less volatility while making sure you're still invested and ready for the eventual recovery.

Getting these decisions right requires a steady hand and a clear, forward-looking strategy. At Commons Capital, our entire focus is on building resilient portfolios designed not just to survive economic cycles, but to thrive through them and achieve your most important financial goals. https://www.commonsllc.com