After decades of saving, you've finally reached the starting line of retirement. It's a huge shift. All those years of carefully building your nest egg are behind you, and now the focus flips from accumulation to decumulation—the art of drawing down your assets to fund your life. This new phase requires a totally different mindset and, more importantly, a real plan. Without solid retirement withdrawal strategies, even a healthy portfolio can run dry faster than you'd think.

Your Blueprint for a Secure Retirement Income

Think of your retirement savings like a reservoir of water you need to last for decades. A good withdrawal strategy is the system of pipes and valves that controls the flow. It ensures you get exactly what you need, when you need it, without draining the reservoir too quickly—especially during a drought (a market downturn).

The Core Challenges of Retirement Income

Putting together a successful withdrawal plan means navigating a few key challenges that can throw even the best-laid plans off course. The biggest worry for most retirees is simply outliving their money. With people living longer than ever, your portfolio might need to provide income for 30 years or more, which makes your starting strategy absolutely critical.

Another major hurdle is something called sequence of returns risk. This is the danger of hitting a stretch of bad investment returns right at the start of your retirement. Pulling money from your portfolio during a down market can lock in those losses and do serious damage to its long-term health. A smart plan is your best defense.

Finally, you have to account for the big economic forces you can't control:

- Inflation: This is the silent thief that eats away at your buying power year after year. Your strategy has to be built to grow your income just to keep up with rising costs.

- Market Volatility: The stock market's wild swings can be unsettling. Your approach needs to build in some stability for when things get choppy.

This is exactly why a "wing it" approach is so dangerous. A structured withdrawal strategy is your financial roadmap, giving you direction and discipline right when you need it most.

This guide will walk you through several proven retirement withdrawal strategies, from the famous 4% rule to more flexible methods like dynamic withdrawals and the bucket strategy. Our goal is to give you the knowledge you need to pick and implement a plan that fits your financial goals, your comfort with risk, and the life you want to live.

Decoding the Classic 4% Rule

If you’ve spent any time researching retirement, you’ve almost certainly run into the 4% rule. It’s the OG of withdrawal strategies, a simple but powerful idea that has guided retirees for decades. Think of it less as a strict law and more as a foundational starting point for turning your nest egg into a steady paycheck.

The core concept is refreshingly simple. In your first year of retirement, you pull out 4% of your total portfolio value. After that, you pretty much ignore what the market is doing and just adjust that initial dollar amount for inflation each year. It’s designed to give you a predictable, stable income—a huge relief for many people just starting their retirement journey.

How the 4% Rule Works in Practice

Let's walk through a quick example. Say you retire with a $1 million portfolio.

- Year One Withdrawal: Your first year's income is $40,000 (4% of your $1 million). Easy enough.

- Year Two Adjustment: Now, let's imagine inflation was 3% last year. You don't recalculate based on your portfolio's new balance. Instead, you just give your withdrawal a cost-of-living raise. Your second-year withdrawal becomes $41,200 ($40,000 x 1.03).

- Continuing the Pattern: You just keep repeating this process. If inflation is 2% the next year, your third-year withdrawal bumps up to $42,024 ($41,200 x 1.02). This happens whether your portfolio has soared to $1.2 million or dipped to $900,000.

This whole approach was developed by financial planner William Bengen back in 1994, based on crunching historical market data. His research showed that a 4% initial withdrawal, adjusted for inflation, had a very high chance of lasting at least 30 years with a balanced mix of stocks and bonds. You can see how Bengen's original findings stack up against more modern approaches for a deeper dive.

The Pros and Cons of This Classic Strategy

While its simplicity is a big draw, the 4% rule isn’t a one-size-fits-all solution. It’s crucial to understand both its strengths and its weaknesses before deciding if it’s the right fit for you.

Advantages of the 4% Rule:

- Simplicity: It’s incredibly easy to understand and calculate. This removes a lot of the complex, stressful decisions from your annual planning.

- Predictable Income: By adjusting a fixed dollar amount, you create a stable income stream that helps maintain your purchasing power year after year.

- Historical Backing: The rule isn’t just a guess; it’s based on extensive historical data, giving it a solid track record through past market ups and downs.

But the financial world looks a lot different than it did in the 1990s, and the rule’s rigid nature can be a major liability.

The biggest risk with a fixed strategy like the 4% rule is its complete inflexibility when markets turn sour. Continuing to pull out the same inflation-adjusted amount when your portfolio is down forces you to sell low, which can speed up how quickly you burn through your savings.

Disadvantages of the 4% Rule:

- Rigidity in Down Markets: The rule doesn’t care if the market is booming or busting. Withdrawing the same amount during a bear market means you’re selling more shares at lower prices, which can permanently hobble your portfolio’s ability to recover.

- Ignores Modern Longevity: The original study was built around a 30-year retirement. With people living longer than ever, a 40- or even 50-year retirement is no longer out of the question, and that can put a serious strain on this fixed approach.

- Potentially Too Conservative: On the flip side, during a roaring bull market, the rule can be too restrictive. It might prevent you from enjoying your portfolio’s strong growth, potentially leaving you with a huge unspent surplus late in life.

At the end of the day, the 4% rule is an excellent educational tool and a solid baseline for planning. But for most modern retirees, it works best as a reference point—a starting block from which to build a more nuanced and flexible withdrawal strategy.

How Dynamic Withdrawals Adapt to Market Changes

While the 4% rule has a certain appeal in its simplicity, its rigid nature can be a real liability when the market gets choppy. Let's be honest, the economy doesn't move in a straight line. This inflexibility is exactly why smarter, more adaptive retirement withdrawal strategies were developed—ones designed to react to what the market is actually doing. We call these dynamic withdrawal strategies, and they offer a much more flexible way to manage your retirement income.

Think of it this way: a fixed strategy is like setting your car's cruise control at 65 mph and never touching it again, no matter if you're going uphill, downhill, or into a traffic jam. A dynamic strategy is like being an engaged driver, easing off the gas or speeding up when conditions allow. It just makes sense. This approach lets your annual income breathe a little, rising and falling in sync with your portfolio's performance.

This adaptability is absolutely critical for neutralizing one of the biggest threats to a long and happy retirement: sequence of returns risk. By pulling back on withdrawals during down markets, you avoid selling off assets when their prices are low. This preserves your capital and gives your portfolio the breathing room it needs to recover.

Introducing the Guardrails Approach

One of the most popular and effective dynamic methods is the "guardrails" strategy. The name says it all. This approach sets upper and lower boundaries—the guardrails—for your withdrawal rate to keep your retirement plan from veering off the road. It gives you a clear, structured way to adjust your spending without having to make gut-wrenching decisions in the heat of the moment.

Here’s a simplified look at how it works, assuming you start with a 5% withdrawal rate:

- Upper Guardrail (e.g., 6%): Let's say a bull market sends your portfolio soaring. Your fixed withdrawal amount is now a smaller piece of a much bigger pie, maybe just 4%. The guardrails approach gives you the green light to increase your income by 10% for the next year. You get to enjoy some of the upside.

- Lower Guardrail (e.g., 4%): On the flip side, a market downturn shrinks your portfolio. Suddenly, that same withdrawal amount represents a bigger chunk—maybe it's now over the 6% threshold. The rule kicks in, telling you to trim your income by 10% for the following year. It’s a temporary belt-tightening to protect your nest egg from being depleted too fast.

This system gives you the best of both worlds: you get the discipline of a rules-based system combined with the flexibility to navigate the real world.

Why Dynamic Strategies Are So Effective

The real magic of dynamic strategies is their power to soften the blow from bad market timing. We can't control when the next downturn will hit, but we can control how we react. Studies have shown this flexibility can dramatically extend the life of a retirement portfolio, which is especially vital for anyone who happens to retire right before a market slump. By automatically pumping the brakes on withdrawals during those critical early years, the strategy gives the portfolio a fighting chance to bounce back.

The research on this is pretty compelling. An analysis by T. Rowe Price ran simulations on hypothetical retirees and found something remarkable: when using a dynamic approach, none of the portfolios ran out of money over multiple 15-year periods. That held true even for those starting in the toughest market environments. It's a massive improvement in sustainability compared to fixed strategies. You can read the full analysis on dynamic withdrawal performance to see just how well it handles sequencing risk.

By tying your withdrawals to your portfolio's actual performance, you shift from a passive passenger to an active pilot of your retirement finances. This control can provide immense peace of mind.

This isn't about making wild swings in your lifestyle from one year to the next. The adjustments are usually modest and predictable, so you're not forced into sudden, painful spending cuts. Instead, it creates a sustainable rhythm—allowing for a little more income in the good years while protecting your capital in the bad ones. The result is a more secure and resilient retirement journey.

Using the Bucket Strategy for Stability and Growth

While dynamic strategies offer some much-needed flexibility, many retirees just feel more comfortable with a structured way to see and manage their money. This is where the bucket strategy really shines. Instead of viewing your portfolio as one giant pot of money, this method helps you mentally divide it into different "buckets," each with its own specific job and timeline.

The real power of this approach is psychological. It creates a mental firewall that protects your long-term investments from short-term panic. When the market inevitably takes a dive, you can pull from your cash bucket with confidence, knowing your growth assets have plenty of time to recover without being sold at a loss.

How the Three Buckets Work Together

The classic version of this strategy uses three distinct segments to cover your spending needs over different periods. Each bucket holds different asset types, creating a nice balance between safety for today and growth for tomorrow.

Let's break down the role of each one:

- Bucket 1: The Cash Bucket (Short-Term): This is your immediate spending money. It holds 1 to 3 years of living expenses in the safest places possible—think cash, high-yield savings accounts, or money market funds. Its only job is to fund your daily life so you never have to sell other investments when the market is down.

- Bucket 2: The Income Bucket (Mid-Term): This bucket is designed to cover your expenses for the next 3 to 10 years. It usually contains a mix of high-quality bonds, conservative bond funds, and other stable, income-generating assets. Think of it as a buffer, providing a reliable source of funds to refill your cash bucket without dipping into your growth investments.

- Bucket 3: The Growth Bucket (Long-Term): This is your portfolio’s engine, holding the money you won’t need for 10+ years. It’s invested mainly in stocks and other assets with high growth potential. Its job is to outpace inflation and make sure your portfolio can last for the long haul.

Setting Up and Managing Your Buckets

Putting the bucket strategy into action is a two-step process: you set it up, and then you maintain it. It’s not as complicated as it sounds.

Let’s walk through a simple example. Say you’re retiring with a $1.2 million portfolio and figure you need $50,000 a year to live comfortably.

The Initial Setup:

- Cash Bucket: You'd put two years of expenses, or $100,000, right into this bucket.

- Income Bucket: Next, you'd allocate the following eight years of expenses, or $400,000, into bonds and similar stable assets.

- Growth Bucket: The remaining $700,000 goes into your stock portfolio, set aside for long-term growth.

The secret sauce that makes the bucket strategy work is the "refilling" process. This isn't a "set it and forget it" plan; it requires a little bit of thoughtful management each year to keep the system running smoothly.

The Art of Refilling Your Buckets

Your main goal is to keep Bucket 1 full. About once a year—or whenever the market gives you a good opportunity—you’ll sell some assets to replenish the cash you've spent down.

- During a Good Year: If the stock market has been doing well, you’d sell some of the gains from your Growth Bucket (Bucket 3) to top off your Cash Bucket (Bucket 1). You might also trim some profits from Bucket 2 if it has performed well, rebalancing as you go.

- During a Bad Year: If your stocks are down, you leave Bucket 3 completely alone. Instead, you sell assets from your more stable Income Bucket (Bucket 2) to refill your Cash Bucket. This simple move gives your growth investments the breathing room they need to recover without you having to lock in losses.

This disciplined process helps you systematically sell high and avoid selling low—a cornerstone of successful investing. The bucket strategy isn't magic, but it provides a logical and emotionally comforting framework that can make your retirement withdrawals far more resilient.

Comparing Top Retirement Withdrawal Strategies

Choosing a retirement withdrawal strategy can feel like a high-stakes decision, and it is. Each approach comes with its own set of trade-offs, and the best one for you hinges on your risk tolerance, how hands-on you want to be, and your need for flexibility when the market gets choppy.

Putting them side-by-side really clarifies what you’re signing up for. The classic 4% rule, for instance, is beautifully simple but offers zero wiggle room when markets head south. On the other hand, dynamic strategies give you that flexibility but require you to be okay with an income that might change from one year to the next.

Then there’s the bucket strategy. It provides a fantastic psychological cushion against downturns, but it also demands the most attention and active management to keep everything in balance.

Evaluating Key Decision Factors

The right strategy isn't just about crunching numbers; it's about finding a rhythm that fits your financial personality. Let's break down how these three popular approaches stack up across the factors that matter most to retirees.

Comparison of Retirement Withdrawal Strategies

To make the choice clearer, this table lays out a direct comparison of the three primary strategies. Think of it as a cheat sheet for understanding the core give-and-take of each method.

Looking at the table, you can see there’s no silver bullet. Each strategy forces you to prioritize what's most important, whether that's simplicity, market responsiveness, or long-term risk management.

Interpreting the Trade-Offs

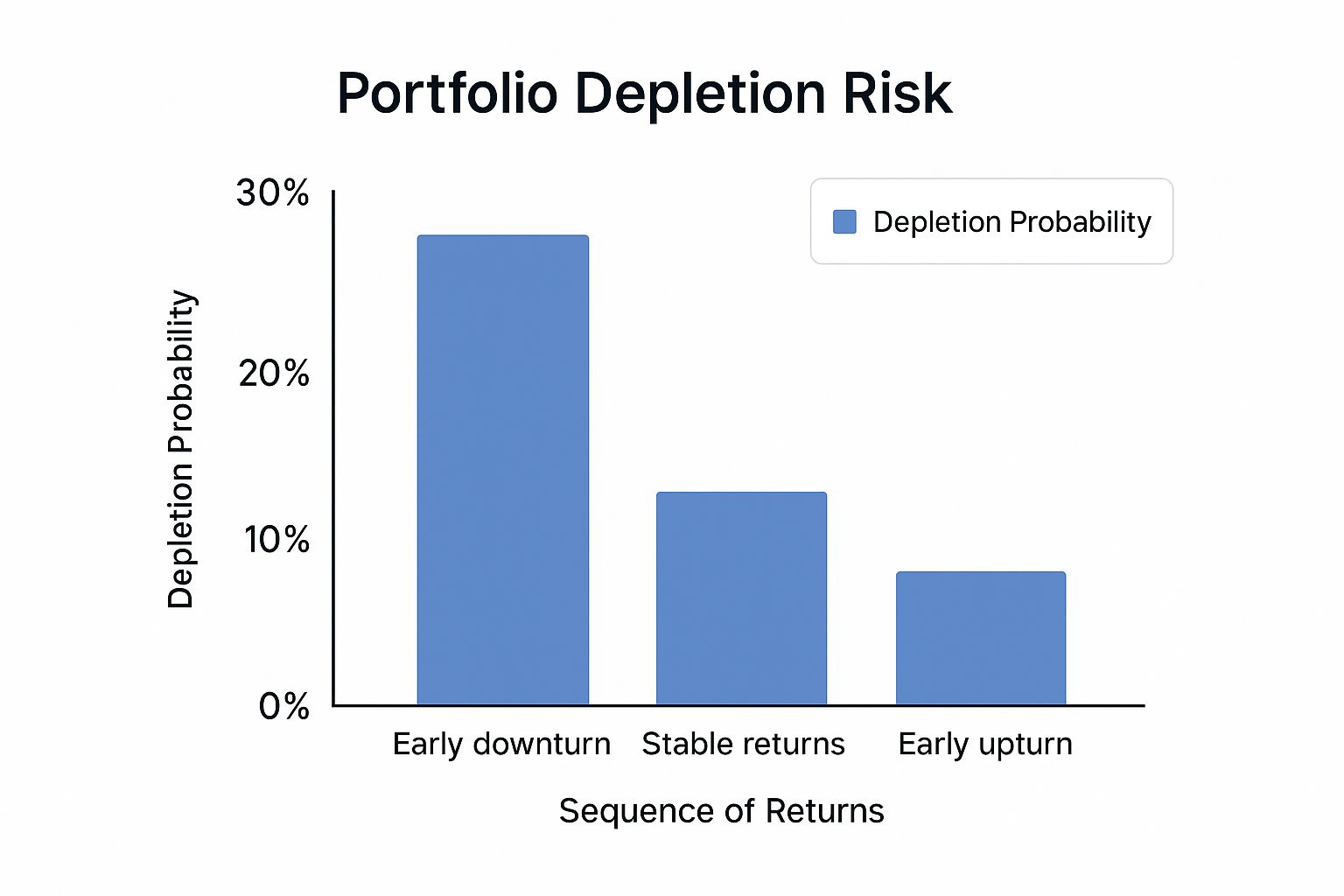

As the comparison shows, there's no single "best" strategy—only the one that’s best for you. The 4% rule's greatest strength is its simplicity, but that comes at the cost of being vulnerable to sequence of returns risk. If a nasty bear market hits right after you retire, a fixed withdrawal plan can put your entire nest egg in jeopardy.

This is a critical concept to grasp, and this visual helps explain why.

The chart makes it painfully clear: a downturn early in retirement dramatically increases the odds of running out of money. It’s a powerful argument for building a strategy that can adapt to reality.

This risk has also led experts to rethink old rules of thumb. For instance, updated research from Morningstar now suggests that a more conservative initial withdrawal rate of around 3.7% might be a safer bet for a 30-year retirement in today's market environment. You can read the full research about these updated withdrawal rate findings.

Key Takeaway: Your choice of strategy should reflect how you want to balance simplicity against risk management. If you're willing to actively manage your finances, a dynamic or bucket approach can provide greater long-term security.

Of course, any withdrawal method is only as good as the financial plan it's part of. For those with significant assets, knowing which accounts to pull from and when is just as important. For more on that, check out our guide on the best tax strategies for high-income earners to learn how to optimize your income streams.

Creating a Tax-Efficient Withdrawal Plan

Picking a retirement withdrawal strategy is only half the battle. How you actually take the money out is just as critical as how much you withdraw each year. If you're not careful, taxes can become a silent partner in your retirement, quietly eating away at your income stream. A smart, tax-efficient withdrawal plan is all about making sure you keep more of your hard-earned savings.

The secret lies in understanding that not all retirement accounts are created equal in the eyes of the IRS. Each one gets a different tax treatment, and the order you tap them in can make a massive difference to your lifetime tax bill.

Understanding Your Three Tax Buckets

It helps to think of your retirement savings as being held in three distinct tax buckets. Knowing which bucket to dip into—and when—is the bedrock of a tax-savvy withdrawal plan.

- Taxable Accounts: This is your standard brokerage account. You're already paying taxes on dividends and capital gains each year. When you pull money out, your original contributions come out tax-free, but you’ll owe capital gains tax on any growth when you sell.

- Tax-Deferred Accounts: This is where your traditional IRAs and 401(k)s live. You got a nice tax deduction on the way in, and the money grew without being taxed along the way. The catch? Every single dollar you withdraw in retirement is taxed as ordinary income.

- Tax-Free Accounts: Welcome to the home of Roth IRAs and Roth 401(k)s. You put after-tax money into these, which means qualified withdrawals in retirement are 100% tax-free. This is your most powerful bucket.

The Conventional Wisdom on Withdrawal Order

A time-tested approach to sequencing your withdrawals is designed to let your most tax-advantaged accounts grow for as long as possible. For most people, this means spending down your accounts in a specific order to keep your lifetime tax bill as low as possible.

- Tap Taxable Accounts First: It usually makes sense to start by spending from your brokerage accounts. Long-term capital gains are often taxed at much lower rates (0%, 15%, or 20%) than the ordinary income rates that apply to your 401(k) withdrawals. This makes it a highly efficient first source of funds.

- Move to Tax-Deferred Accounts Next: Once your taxable accounts are spent down, you can begin taking withdrawals from traditional IRAs and 401(k)s. Many retirees do this strategically, pulling out just enough each year to "fill up" the lower tax brackets without spilling into higher ones. This is often called tax bracket smoothing.

- Save Your Tax-Free Accounts for Last: Your Roth accounts are your ace in the hole. By leaving them untouched for as long as possible, you give them the maximum amount of time to compound completely tax-free. They also serve as an incredible safety net, giving you a source of tax-free cash for big, unexpected expenses without the risk of pushing you into a higher tax bracket for the year.

Navigating the RMD Hurdle

The government doesn't let you keep money in your tax-deferred accounts forever. Once you reach a certain age (currently 73, though this can change), you have to start taking money out. These are called Required Minimum Distributions (RMDs).

RMDs are not a suggestion. If you fail to take the full amount, the IRS can hit you with a stiff penalty. These mandatory withdrawals are fully taxable as ordinary income, and if you haven't planned for them, they can cause a major spike in your tax bill.

This is where being proactive pays off in a big way. Strategies like converting some traditional IRA funds to a Roth IRA during your lower-income years (before RMDs kick in) can shrink the future balance of your tax-deferred accounts. A smaller balance means smaller future RMDs and, ultimately, a lower lifetime tax bill.

Learning these techniques is a crucial part of a complete retirement plan. You can explore 3 ways to minimize your tax liability in our detailed guide. A truly thoughtful plan doesn't just pick a withdrawal rate; it integrates that rate with RMD management to make every dollar of your retirement income as efficient as it can be.

Common Questions About Retirement Withdrawals

Even the most buttoned-up retirement plan will spark a few questions once you start putting it into practice. The stakes are high, after all. Getting clarity on these points is key to feeling confident about the decades ahead.

Let's walk through a few of the most common questions we hear from retirees.

What Is the Safest Withdrawal Rate for Retirement?

The old 4% rule has been a trusted benchmark for years, but it’s not the definitive answer it once was. More recent analyses point to a more conservative rate—around 3.7%—as a safer bet for a 30-year retirement in today's market.

But here’s the thing: the "safest" rate is deeply personal. It really depends on your specific portfolio, how you feel about risk, and your retirement timeline.

Ultimately, dynamic strategies that flex with the market are often considered safer than sticking to a rigid, fixed percentage. They're designed to protect your nest egg during downturns, which is precisely when your portfolio is most vulnerable.

How Does Inflation Affect My Withdrawal Strategy?

Inflation is the silent portfolio killer. It slowly but surely erodes your purchasing power, and a solid withdrawal strategy absolutely has to account for it. The classic 4% rule, for instance, was designed with an annual inflation adjustment baked right in to help you maintain your lifestyle.

Newer approaches, like the dynamic and bucket strategies, also tackle this by aiming for portfolio growth that outpaces the rate of inflation. If you don't plan for rising costs, the income that feels comfortable today might not even cover the basics a decade from now.

Key Insight: Your withdrawal strategy isn't just about pulling out cash. It's about generating an income stream that maintains its value, year after year. Factoring in inflation is non-negotiable for long-term success.

Should I Hire a Financial Advisor?

While it's certainly possible to build a withdrawal strategy on your own, a qualified financial advisor can add tremendous value. They can help you honestly assess your risk tolerance, see your entire financial picture clearly, and build a personalized, tax-efficient plan that’s truly wired for your goals.

Perhaps just as important, an advisor acts as a steady hand during market swings, helping you stick to your long-term plan instead of making emotional decisions you might later regret.

This is especially true when life throws you a curveball. Our guide on what to do with inheritance money explores just one of many complex situations where professional guidance can be indispensable. An advisor makes sure all the moving parts of your financial life work together as one.

Figuring out the complexities of retirement withdrawals is one of the most important steps in securing your financial future. At Commons Capital, we specialize in creating sophisticated, personalized wealth management plans for high-net-worth individuals and families.

If you’re ready to build a resilient and tax-efficient retirement income strategy, we invite you to connect with our team.