Let's be clear: when you inherit a 401(k), the federal government isn't going to hit you with a direct inheritance tax. But that doesn't mean it's tax-free. You will almost certainly owe income tax on every dollar you withdraw from a traditional 401(k). The key takeaway is that the distributions are treated as part of your regular income for that year, which can have a significant tax impact.

Your Quick Guide to Inherited 401(k) Taxes

When you inherit a 401(k), you’re not just handed a lump sum of cash. You're inheriting a very specific set of tax rules and deadlines that come attached. It helps to think of the 401(k) as a tax-deferred container. The original owner put money in before taxes were paid, and it grew for years without the IRS taking a cut.

Now that the money is coming out, it's time for the tax man to get his due. Understanding this is the key to making smart decisions. The biggest change for most non-spouse beneficiaries is the 10-year rule, which came out of the SECURE Act. This rule is simple but strict: you must withdraw the entire account balance by the end of the tenth year after the original owner's death.

Key Rules for Beneficiaries

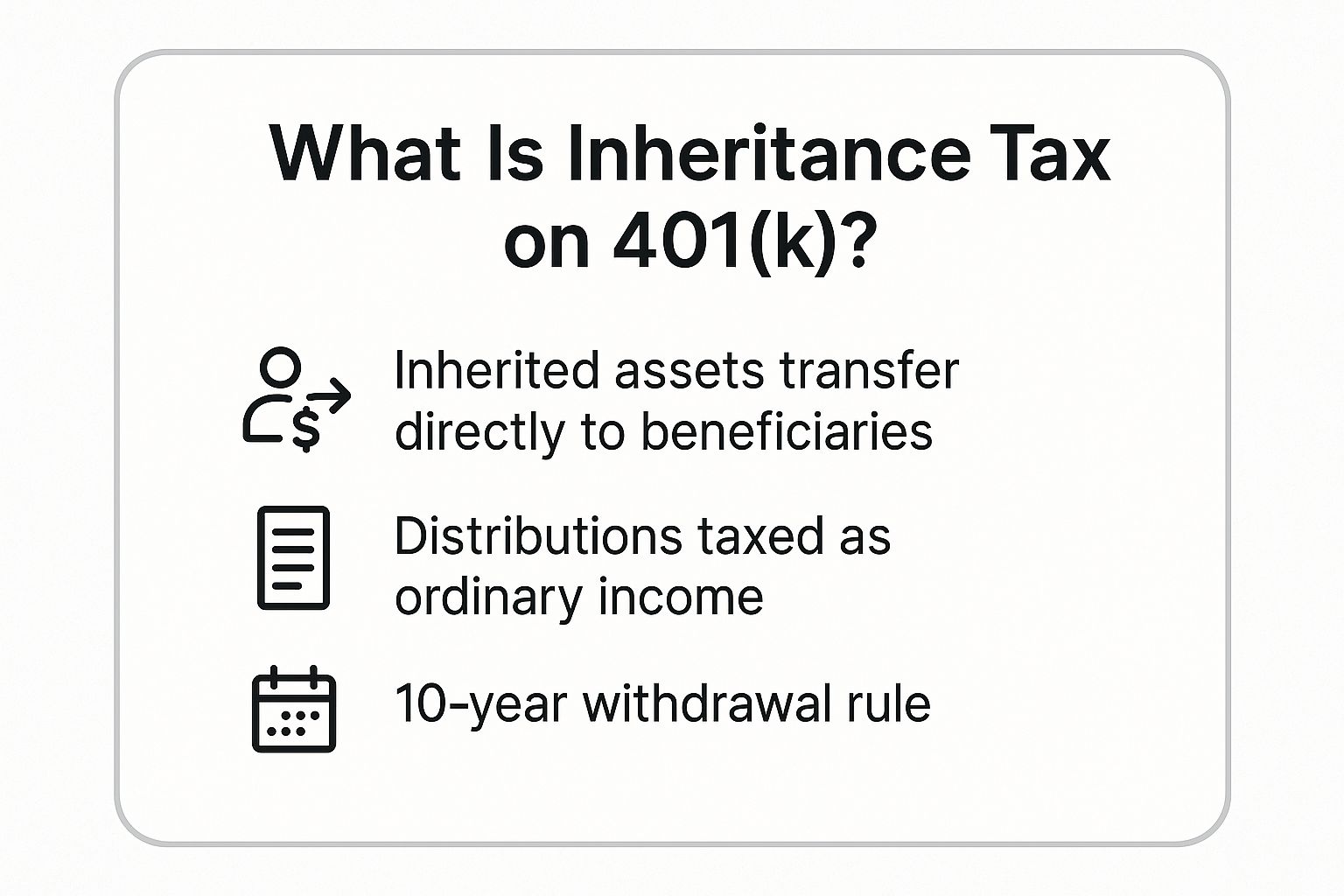

This infographic boils down the core ideas you need to grasp when you're figuring out the tax impact of an inherited 401(k).

As the visual lays out, withdrawals get taxed as ordinary income, and for most, the clock is ticking on that 10-year deadline. This compressed timeline can seriously inflate your tax bill if you don't plan your withdrawals strategically.

Knowing the rules is just the starting line. Applying them in a way that works for your financial situation is what really counts. For a wider view on managing a sudden influx of assets, take a look at our guide on what to do with inheritance money. It will help you see how this new account fits into your bigger financial picture without stumbling into common pitfalls.

Why Inherited 401(k)s Create a Tax Bill

It often comes as a shock when beneficiaries discover that an inherited 401(k) carries a tax bill. The confusion is completely understandable. After all, most other assets you inherit—like a house or a stock portfolio—get a "step-up in basis." This resets their value to the date of death, often wiping out any capital gains tax for the heir.

But traditional 401(k)s play by a completely different set of rules.

Think of a traditional 401(k) as a tax-deferred container. For years, the original owner contributed pre-tax dollars, which lowered their taxable income while they were working. All the dividends, interest, and market gains compounded inside that account without a dime being paid in taxes along the way.

When you inherit that account, you also inherit the deferred tax liability. The IRS sees it as a bill that has finally come due. Every dollar you pull out is treated as ordinary income, not a tax-free inheritance, and is taxed at your personal income tax rate in the year you take it.

The Critical Difference Between Pre-Tax and Post-Tax Accounts

The single most important factor determining your tax hit is the type of 401(k) you’ve inherited. The distinction is simple, but the financial consequences are massive.

- Traditional (Pre-Tax) 401(k)s: This is the most common type. Contributions were made before income tax was paid. As a result, all withdrawals you make as a beneficiary are fully taxable as ordinary income.

- Roth (Post-Tax) 401(k)s: Contributions here were made with after-tax dollars. Since the taxes were already paid upfront, qualified withdrawals by a beneficiary are completely tax-free.

This fundamental difference means inheriting a $500,000 Roth 401(k) is a world apart from inheriting a $500,000 traditional 401(k). The Roth account delivers its full value to you, while the traditional account’s value will be whittled down by federal and possibly state income taxes.

Understanding Your Income Tax Obligation

While an inherited 401(k) typically sidesteps federal estate tax, beneficiaries are on the hook for income tax on every withdrawal from a traditional account.

These withdrawals are taxed at your ordinary income tax rate, which can range from 10% to 37% federally, depending on your total income for the year. A single large withdrawal can easily bump you into a higher tax bracket, taking a much bigger bite than you might expect. You can dig deeper into how inherited retirement assets are taxed in this helpful guide from SmartAsset.

This tax treatment makes strategic withdrawal planning absolutely essential, especially now that the 10-year rule is in place for most non-spouse beneficiaries.

Special Rules for a Surviving Spouse

The tax rules bend significantly for a surviving spouse, recognizing their unique financial position. A spouse is the only type of beneficiary who has the option to treat the inherited 401(k) as if it were their own.

This spousal rollover is an incredibly powerful planning tool. It allows the surviving spouse to move the funds into their own IRA, delay required minimum distributions (RMDs) until they reach age 73, and manage the assets as part of their own long-term retirement strategy.

This is a game-changer. Non-spouse beneficiaries, like children or siblings, don't get this option. They're stuck with more restrictive rules that usually require them to empty the account within a decade. This key difference gives spouses a massive advantage, allowing them to manage the tax impact over a much longer timeline and let the funds continue to grow tax-deferred.

How the SECURE Act Changed the Rules

For decades, inheriting a 401(k) from a loved one came with a powerful tax strategy: the "stretch IRA." This approach was a game-changer for non-spouse beneficiaries, like children or grandchildren. It allowed them to take small, required annual distributions based on their own life expectancy, not the original owner's.

The game plan was simple but incredibly effective. You could stretch the withdrawals out over a lifetime, keeping the bulk of the assets growing tax-deferred and minimizing the annual income tax hit. But that all changed with the SECURE Act of 2019. This piece of legislation completely dismantled the stretch strategy for most heirs, fundamentally altering the landscape for inheriting retirement accounts.

The End of the Stretch IRA Era

Before the SECURE Act, a 35-year-old who inherited a 401(k) could potentially take distributions for nearly 50 more years. Think about that. Small, manageable withdrawals each year, often keeping them in a lower tax bracket while the majority of the inherited funds stayed invested, continuing to grow tax-deferred for decades.

This was a cornerstone of generational wealth transfer. It gave beneficiaries tremendous flexibility and significant long-term tax advantages. Lawmakers, however, saw this extended tax deferral as lost revenue and decided to accelerate the collection process, leading directly to the new rules.

Introducing the Strict 10-Year Rule

The SECURE Act threw out the lifetime stretch and replaced it with a much more aggressive timeline for most non-spouse beneficiaries: the 10-year rule. This new regulation is exactly what it sounds like. The entire balance of the inherited 401(k) must be completely withdrawn by the end of the tenth year after the original owner's death.

This shift has profound implications for the inheritance tax on 401k assets—or more accurately, the income tax liability. Instead of spreading a tax bill over a lifetime, beneficiaries are now forced to deal with it in a single decade.

The move from a lifetime stretch to a 10-year payout window is one of the biggest changes to retirement account rules we've seen in years. It forces heirs to recognize that income much, much faster, which can lead to a substantially higher tax bill if not planned for carefully.

This compressed timeline means beneficiaries can't just let the money sit and grow for decades. They need a strategic plan to draw down the account, which often involves careful tax bracket management to sidestep costly mistakes. Now, comprehensive estate planning for wealthy individuals is essential to account for this new reality and protect heirs from a surprise tax bomb.

Who Is Affected by the 10-Year Rule

The 10-year rule applies to most designated beneficiaries who aren't the surviving spouse. Congress essentially eliminated the stretch provision for these individuals, forcing them to empty the inherited 401(k) within a decade. This move speeds up tax payments to the government and can potentially increase the lifetime tax bill for a beneficiary by thousands.

However, Congress did carve out a few important exceptions for a specific group known as Eligible Designated Beneficiaries (EDBs). These individuals are exempt from the 10-year rule and can still use the old-school lifetime stretch method.

The EDB category is fairly narrow and includes:

- The surviving spouse of the account owner

- A minor child of the account owner (but only until they reach the age of majority)

- A disabled or chronically ill individual

- An individual who is not more than 10 years younger than the deceased account owner (like a sibling close in age)

For everyone else—adult children, grandchildren, nieces, nephews, or friends—the 10-year clock starts ticking the moment they inherit. This makes understanding how to calculate your tax hit and develop a smart withdrawal strategy more critical than ever.

Calculating Your Federal Income Tax Hit

Knowing you owe income tax on an inherited 401(k) is one thing. The real question is: how much will you actually have to write a check for? There’s no simple answer, because the final number depends entirely on how you take the money out, what your other income looks like, and the federal tax brackets for that specific year.

Here's the crucial part to remember: every single dollar you withdraw from that inherited 401(k) gets stacked right on top of your regular taxable income for the year. A big withdrawal can have a surprisingly powerful—and expensive—ripple effect on your overall tax bill.

Identifying Your Marginal Tax Bracket

Before you touch a dime of that inheritance, you need to figure out where you stand with the IRS. We’re talking about your marginal tax bracket, which is just the tax rate you pay on your very last dollar of income. It's the highest tax bracket your total income pushes you into, and it's the rate that will apply to distributions from the 401(k).

To get a rough idea, take your gross income and subtract your likely deductions. That gives you your taxable income. Now, just compare that number to the current federal income tax brackets to see which one you fall into.

For instance, say you're a single filer with a taxable income of $95,000 in 2025. That puts you in the 22% bracket. At first glance, you might think any money you pull from the 401(k) will be taxed at 22%, but that can change in a hurry.

The Costly Mistake of "Bracket Creep"

This is where so many beneficiaries get into trouble. "Bracket creep" is what happens when a sudden influx of cash—like a 401(k) payout—shoves your total income into a higher tax bracket than you're used to. A withdrawal that seemed perfectly reasonable at your normal tax rate can suddenly become a lot more expensive when a huge chunk of it gets taxed at a much higher percentage.

Let's walk through a real-world example.

Example One: The Lump-Sum Withdrawal

Imagine you're a single filer with $100,000 in taxable income for 2025, which places you squarely in the 24% tax bracket. You inherit a $250,000 traditional 401(k) and, wanting to get it over with, you decide to take it all at once in a lump sum.

- Your new total taxable income for the year rockets to $350,000 ($100,000 + $250,000).

- This massive jump pushes you from the 24% bracket all the way up into the 35% bracket.

- A huge portion of that inheritance is now being taxed at much higher rates (32% and 35%) than your original 24%.

That one decision could easily cost you tens of thousands of extra dollars in taxes compared to a more measured approach.

Using the 10-Year Rule to Your Advantage

The 10-year rule might feel restrictive, but it's also a powerful tool for managing your tax bill. Instead of taking one massive tax hit, you have a full decade to spread out the income and, by extension, the taxes. This gives you incredible control, letting you decide how much extra income to recognize each year and keep that dreaded bracket creep at bay.

Example Two: The Strategic Withdrawal

Let's stick with our single filer who has $100,000 in income and inherited $250,000. Instead of grabbing it all at once, they decide to stretch the withdrawals over the full 10 years, taking out $25,000 annually.

- Their new taxable income each year is a much more manageable $125,000 ($100,000 + $25,000).

- This keeps them comfortably inside the 24% tax bracket every single year.

- They completely avoid getting pushed into those higher 32% and 35% brackets.

By simply being strategic about the timing, this beneficiary keeps a lot more of their inheritance. This methodical approach is really the cornerstone of minimizing the inheritance tax on a 401k.

The goal isn't just to empty the account within 10 years. It’s to do so in the most tax-efficient way possible. By modeling your withdrawals against your projected income, you can turn a potential tax nightmare into a manageable financial plan.

The table below shows just how different these two approaches are, and how a little planning can lead to huge savings.

Tax Impact of Different Withdrawal Strategies

Here's a side-by-side comparison for a $250,000 inherited 401(k), highlighting why strategy matters.

As you can see, taking your time isn't just about delaying the tax bill—it's about actively shrinking it.

Navigating State Taxes on Your Inheritance

Once you've wrapped your head around the federal rules, don't forget the next player at the table: your state's tax department. Forgetting about state taxes is an easy mistake to make, and it can be a costly one. The rules can be wildly different from one state to the next, which means your zip code has a huge say in how much of that inheritance you actually get to keep.

The bill from Uncle Sam is only half the story. The total tax bite on an inherited 401(k) isn't final until you've factored in what your own state wants.

How State Income Taxes Chip Away at Your Inheritance

For the most part, states with an income tax see your 401(k) withdrawals the same way the federal government does: as taxable income. Every time you pull money out, a piece goes to Washington D.C., and another piece goes to your state capital. That one-two punch can seriously shrink your inheritance if you aren't ready for it.

Someone inheriting in a high-tax state like California, for example, is looking at a top marginal rate of 13.3%. That's a much bigger slice of the pie than what a beneficiary in a state with a low, flat tax rate would pay. It just goes to show how critical your location is when planning for an inherited 401(k).

The map below gives you a quick visual of just how varied the state income tax landscape really is.

As you can see, you've got everything from states with progressive brackets to those with a single flat rate—and a lucky few with no income tax at all. This creates completely different financial outcomes for beneficiaries across the country.

The Best and Worst States for Inherited 401(k)s

It can't be said enough: where you live really, truly matters. The difference between inheriting a $250,000 401(k) in Florida versus New York is staggering, and that's just because of state income tax. Getting a handle on your state's rules is non-negotiable for smart financial planning and avoiding a nasty surprise come tax time.

- No-Income-Tax States: If you live in a place like Florida, Texas, Nevada, or Washington, you've got a massive head start. Your only concern is the federal income tax on your withdrawals, which lets you hold onto a much larger portion of the money.

- High-Income-Tax States: On the flip side, residents of California, Hawaii, New York, and Oregon face a much steeper climb. Their high state income tax rates are stacked right on top of federal taxes, resulting in a significantly smaller net inheritance.

To put it plainly, a beneficiary in a no-tax state could pocket tens of thousands of dollars more than someone in a high-tax state who inherited the exact same amount.

Don't Forget State Inheritance and Estate Taxes

On top of income tax, a handful of states have their own inheritance tax or estate tax. These aren't taxes on the 401(k) directly, but the account's value gets lumped into the deceased's total estate. If the estate is large enough, it could trigger these taxes before the assets are even passed on to you.

The rules for state-level taxes on inherited retirement funds are a tangled web. For instance, some states like Kansas will tax your 401(k) withdrawals as ordinary income with rates climbing from 3.1% to 5.7%, while other states might offer unique exemptions. You can discover more insights about how different states tax retirees on Kiplinger.com. These details make it clear why you have to build your state's tax laws into your withdrawal strategy from day one.

Advanced Strategies to Minimize Taxes

Simply spreading your withdrawals over 10 years is a good start, but proactive planning can unlock far more significant tax savings. This is where you move from basic compliance to strategic action, looking at the entire financial picture and using the inheritance as a tool for wealth preservation—not just a new source of taxable income.

With the right approach, an inherited 401(k) becomes a powerful asset. These advanced strategies do require some foresight and financial maneuvering, but the payoff can be huge, potentially saving you tens of thousands in taxes over the decade.

Timing Withdrawals for Low-Income Years

The 10-year rule gives you a generous window to plan. One of the most effective strategies is to align your withdrawals with years when your personal income is expected to be lower. This lets you absorb the inherited 401(k) distribution without getting bumped into a punishingly high tax bracket.

Think about these scenarios as prime opportunities:

- A Planned Sabbatical: Taking a year off work? Your income will naturally drop, creating the perfect window to take a larger distribution at a much lower tax rate.

- Career Transitions: The gap between jobs often results in a lower-income year. This is an ideal time to pull funds from the inherited account.

- Early Retirement: If you retire before drawing Social Security or other retirement income, you might have a few low-income years to strategically empty the account.

By timing your withdrawals to coincide with these income dips, you can manage your inheritance tax on 401k obligations far more effectively than if you pulled out money during your peak earning years.

Using Inherited Funds to Max Out Your Own Accounts

This strategy is about turning a tax liability into a tax-advantaged asset. Instead of just spending the inherited money, you can use the distributions to fund your own retirement accounts. You're essentially replacing taxable money with tax-sheltered money, compounding your own wealth for the future.

Here’s how it works in practice:

Imagine you withdraw $23,500 from the inherited 401(k). After setting aside what you'll owe for taxes, you use the rest to max out your contribution to your own 401(k) at work. While you pay income tax on the withdrawal, you simultaneously get a tax deduction for contributing to your pre-tax 401(k), which can largely cancel out the tax hit.

This method is a powerful way to convert a time-limited inheritance into a long-term asset under your control. You’re not just taking a distribution; you’re reinvesting in your own tax-deferred future.

Proactive Planning for the Original Account Owner

Often, the best time to minimize taxes on an inherited 401(k) is before the inheritance even happens. The original account owner holds some powerful cards that can ease the future tax burden on their beneficiaries.

The Lifetime Roth Conversion

One of the most effective moves an account owner can make is to systematically convert funds from their traditional 401(k) or IRA to a Roth account during their lifetime. Yes, they pay income taxes on the converted amount now, but once that money is in a Roth, it grows tax-free forever.

For the beneficiary, this is a game-changer. Inheriting a Roth account means all qualified distributions are 100% tax-free. The 10-year rule still applies, but you get to keep every single dollar. It's a profound gift that shifts the tax burden from the heir to the original owner, who can often manage it more effectively during their lower-income retirement years.

Naming a Charity as a Beneficiary

Another potent strategy involves philanthropy. If the account owner has charitable intentions, naming a qualified charity as the direct beneficiary of a traditional 401(k) is an incredibly tax-efficient move.

- The charity is a tax-exempt organization, so it pays zero income tax on the distribution.

- The full, pre-tax value of the 401(k) goes directly to a cause the person cared about.

- The estate may also receive an estate tax deduction for the charitable gift.

This approach allows the account owner to leave other, more tax-friendly assets (like real estate or a stock portfolio with a stepped-up cost basis) to their family. Exploring these kinds of options is a core part of effective wealth management. You can learn more by reviewing our guide on 3 ways to minimize your tax liability.

Frequently Asked Questions

When inheriting a 401(k), many beneficiaries mistakenly worry about a direct inheritance tax on 401k funds. In reality, the primary concern is income tax. Each withdrawal you take is treated and taxed as ordinary income for that year. Understanding this distinction is the first step toward smart planning.

Here are the questions we hear most from beneficiaries:

- Do I Have To Take All The Money Out Of An Inherited 401k?

You have options. Under the SECURE Act, most non-spouse heirs get 10 years to distribute the full balance. Sure, you can take it all at once, but that lump-sum often triggers a big tax spike. A more common strategy is to spread withdrawals over the decade to manage the tax impact. - Is An Inherited Roth 401k Taxed Differently?

Yes, and the difference is significant. Provided the account has been open for at least 5 years, qualified withdrawals are 100% tax-free. However, non-spouse beneficiaries must still empty the inherited Roth 401(k) within the 10-year timeframe. - Can I Roll An Inherited 401k Into My Own IRA?

This option is reserved for surviving spouses. A spouse can roll the inherited 401(k) into their own IRA, which allows them to treat the funds as their own and defer required distributions. Non-spouse heirs must leave the assets in a specifically titled inherited account and follow the 10-year rule.

Key Considerations

- Track Your Income: Keep a close eye on your annual taxable income to avoid being unintentionally pushed into a higher tax bracket by your withdrawals.

- State Taxes Matter: Remember to factor in your state's income tax rules for 401(k) distributions, as they can vary widely and significantly impact your net inheritance.

- Seek Professional Guidance: Consider working with a financial advisor or tax professional to time your distributions strategically and align them with your overall financial picture.

Following these tips will help you sidestep surprises and keep your cash flow smooth. Before making any withdrawal, double-check key deadlines and current tax rates. Next, let’s look at how to turn these insights into a concrete plan.

Spreading distributions over the full 10-year window can dramatically lower your overall tax bill by keeping you in lower brackets.

Planning Your Next Step

Talk with a trusted advisor who understands how the income tax on an inherited 401(k) impacts your personal return. A professional can help you map out a distribution schedule that aligns with your financial goals and minimizes your tax liability over the 10-year period.

For personalized assistance, contact Commons Capital: Commons Capital