If you've ever wondered what is a trust fund and how does it work, you're not alone. The term often brings to mind images of old money and inherited fortunes, but the reality is much more practical and accessible. A trust is simply a legal tool for managing your assets, a bit like a personalized playbook for your wealth, that offers powerful benefits for families of many different financial backgrounds.

A trust fund is a formal legal arrangement where you (the grantor) hand over assets to a trusted person or institution (the trustee). Their job is to manage those assets for the people you’ve chosen to receive them (the beneficiaries). It’s a strategic way to ensure your wishes are carried out with precision, often providing more privacy and control than a will ever could. This guide will walk you through the essential components of a trust, from the key roles involved to the real-world advantages it offers.

What Is a Trust Fund? A Practical Explanation

At its heart, a trust is built on a fiduciary relationship. That's a fancy way of saying it's a legal and ethical duty to act in someone else's best interest. It works by separating the legal ownership of an asset from the benefit of owning it.

Think of it like this: you want to set aside money for your grandchild's college education. You (the grantor) put the funds into a special account (the trust) and appoint your financially savvy sister (the trustee) to manage it. Your instructions are clear: she must invest the money wisely and use it only for tuition when your grandchild (the beneficiary) turns 18. Your sister doesn't own the money, but she’s legally in charge of protecting and distributing it according to your rules.

This basic structure is a cornerstone of modern financial planning. A trust isn't just a bank account; it's a legal container that can hold almost anything of value:

- Cash, stocks, and bonds

- Real estate, from a family home to commercial properties

- Shares in a private business

- Life insurance policies

- Even valuable collections like art or classic cars

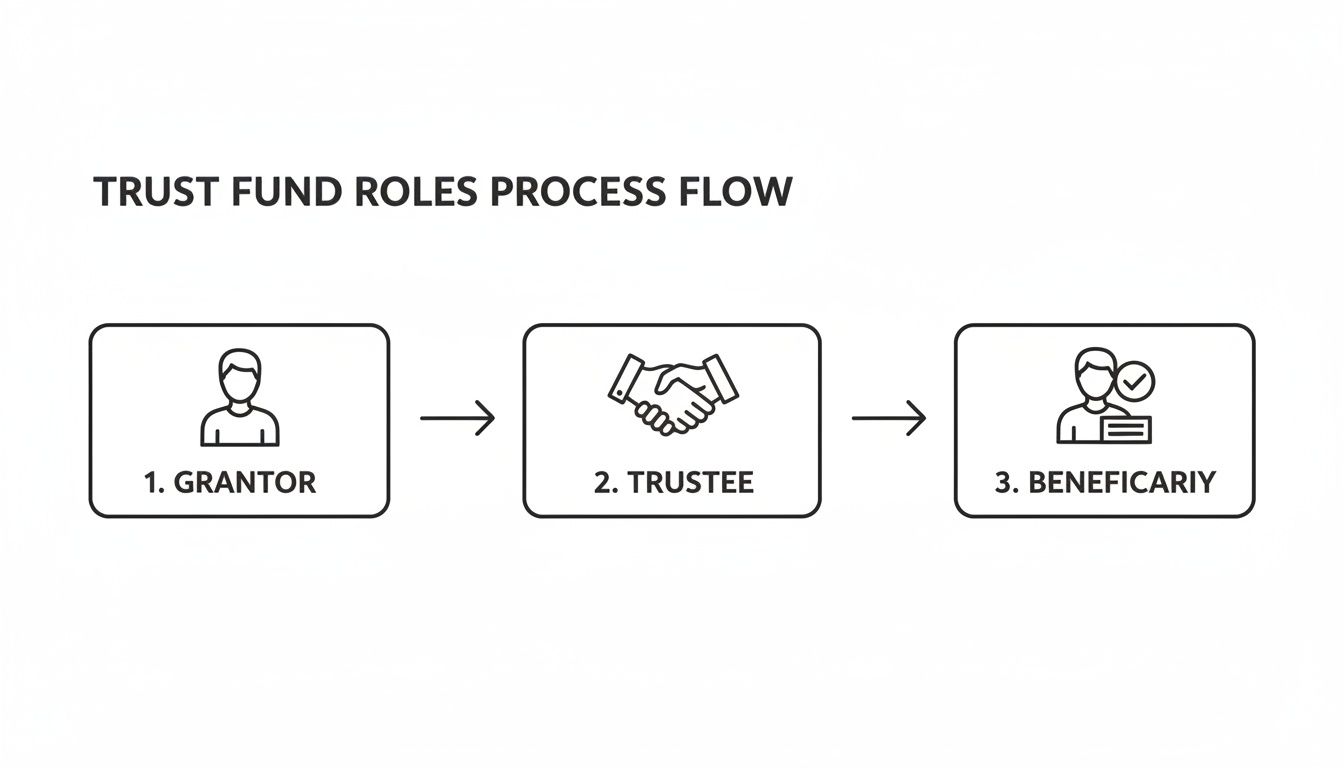

The Three Key Roles in a Trust

Every trust, no matter how simple or complex, revolves around three key players. Once you understand who does what, the whole concept becomes much clearer.

Here’s a quick breakdown of the essential parties involved in every trust and their main jobs.

The Three Key Roles in a Trust Fund

This three-part structure is incredibly versatile, making trusts a go-to tool for families worldwide. In fact, personal trust services are a massive and growing global industry, active in 195 countries. If you're interested in the scale of this market, you can find more details in this detailed industry report.

Ultimately, setting up a trust is about creating certainty and control. It provides a clear, structured path for managing your wealth that can protect it from creditors, reduce estate taxes, and avoid the lengthy, public process of probate court. Of course, it’s a big decision, so it’s wise to explore the pros and cons of a trust before moving forward.

How a Trust Fund Works Step by Step

Think of a trust fund as a game plan for your assets. Once you understand the sequence of play, the whole concept clicks into place. A trust isn't a one-time event; it’s a living arrangement with four distinct stages that guide your wealth from you to the people you want to benefit.

The entire process kicks off with your vision and a legal document, moves into a management phase, and ultimately ends with the assets being distributed exactly as you intended. This structured flow is what guarantees your wishes are carried out.

Stage 1: Creating the Trust

First things first, you have to formally create the trust. This is done through a legal document called a trust agreement. This document is the rulebook, spelling out every detail of how the trust will operate. In it, the person creating the trust (the grantor) names the key players: the trustee who will manage everything and the beneficiaries who will eventually receive the assets.

The agreement also dictates precisely how and when those assets are handed out. For example, a grantor might specify that a beneficiary can only get money for college tuition or after they reach a certain age, like 30. This document is the cornerstone; it legally binds the trustee to follow the grantor's instructions to the letter.

Stage 2: Funding the Trust

A trust agreement with no assets is just an empty box—all plan, no substance. The second stage, funding, is where you actually transfer assets into the trust. This is a critical legal step where ownership of your property officially moves from your name into the name of the trust.

You can put almost any kind of asset into a trust, including:

- Real Estate: The deed for your home or an investment property is re-titled to the trust.

- Financial Accounts: Bank and brokerage accounts are officially registered under the trust's name.

- Business Interests: You can assign shares in a private company to the trust.

- Personal Property: High-value collections, like art or classic cars, are legally transferred.

Properly funding the trust is what gives it its power. It ensures those specific assets are governed by the trust's rules, not by your personal will.

This simple flowchart shows the powerful chain of responsibility in a trust—from the grantor who starts it, to the trustee who manages it, and finally to the beneficiary who benefits from it.

Stage 3: Administering the Trust

Once it's funded, the trust enters the administration phase. This is where the trustee really steps into the spotlight. If it's a living trust, the grantor might manage it themselves for a while. But after the grantor passes away or becomes unable to manage their affairs, the successor trustee takes the reins.

The trustee has a fiduciary duty—a legal obligation—to manage the trust's assets wisely and always act in the best interest of the beneficiaries. These responsibilities are serious and legally enforceable.

A trustee isn't just a gatekeeper. They are a legal steward responsible for everything from investing assets and filing tax returns to keeping meticulous records and communicating with beneficiaries. This duty of care is what makes the trust run correctly over the long haul.

For a trust to work as planned, it's vital to have a solid grasp of what's involved, especially when it comes to understanding trustee responsibilities after death.

Stage 4: Distributing the Assets

The final stage is the distribution—the moment the beneficiaries receive the assets as laid out in the trust agreement. This is the payoff for all the careful planning.

Distributions can be structured in almost endless ways. For example, a trust could be set up to pay out a single lump sum to a beneficiary when they turn 25. Or, it could provide a steady income stream for the beneficiary's entire life. The rules defined by the grantor back in stage one control every part of this final step, ensuring their legacy is fulfilled exactly as they imagined.

Choosing the Right Type of Trust for Your Goals

Trusts aren't a one-size-fits-all solution. Think of them less like a generic container and more like a set of specialized tools, each one crafted for a very specific job. The right choice comes down to what you're trying to accomplish—whether that's staying flexible, shielding your assets from risk, or building a philanthropic legacy.

Your journey starts with a foundational decision that shapes everything that follows: will your trust be revocable or irrevocable? This single choice determines how much control you keep and how the trust will function for years to come.

The Core Decision: Revocable vs. Irrevocable Trusts

Think about writing a crucial document. Do you use a pencil, knowing you can erase and rewrite it as needed? Or do you sign it in permanent ink, making it final and binding? This simple analogy cuts right to the heart of the difference between revocable and irrevocable trusts.

A revocable trust, often called a living trust, is the pencil. As the grantor, you hold all the power. You can change the terms, add or remove assets, or even tear the whole thing up whenever you want. This gives you maximum flexibility, but it comes at a cost—because you still technically own everything in it, the trust offers almost no protection from creditors or lawsuits.

On the other hand, an irrevocable trust is the permanent ink. Once you create it and transfer assets into it, the deal is done. You give up control, and the terms are essentially locked in. It’s a huge step, but it’s what gives the trust its power to protect assets from creditors and reduce the size of your taxable estate. This permanence is a strategic trade-off for some very significant long-term benefits.

A revocable trust is all about flexibility and control during your lifetime. An irrevocable trust is built for robust asset protection and tax advantages, creating a true legal separation between you and your assets. Your primary goals will tell you which one is right.

To make an informed decision, it's essential to understand the trade-offs. For anyone leaning toward the more permanent option, taking a deep dive into the pros and cons of an irrevocable trust is a critical next step.

To make it even clearer, here’s a quick breakdown of how the two stack up.

Revocable vs. Irrevocable Trusts At a Glance

This table offers a direct comparison of the two main categories of trusts, highlighting their key differences in flexibility, asset protection, and tax implications.

As you can see, the choice isn't about which one is "better" but which one aligns with your specific objectives.

Specialized Trusts for Specific Life Circumstances

Beyond that initial choice, the world of trusts opens up to all kinds of specialized vehicles designed for unique family and financial situations. These are far more than just legal documents; they are carefully constructed solutions for life's complexities.

Here are a few common examples of how trusts can be tailored to meet very specific needs:

- Spendthrift Trusts: Have a beneficiary who might not be ready to handle a large inheritance? A spendthrift trust is the answer. It gives the trustee the authority to manage distributions, which protects the funds from the beneficiary’s creditors—or their own poor spending habits.

- Special Needs Trusts (SNTs): This is a lifeline for families with a loved one who has a disability. An SNT is structured to provide for their needs without kicking them off crucial government benefits like Medicaid or Supplemental Security Income (SSI). The trust funds supplement, rather than replace, this aid, paying for things that improve their quality of life.

- Charitable Trusts: For anyone wanting to make philanthropy a part of their legacy, these trusts are powerful tools. A Charitable Remainder Trust can give you or your heirs an income stream for a set period, with whatever is left over going to your favorite charity. A Charitable Lead Trust does the opposite—it pays the charity first, and your heirs receive the remainder.

These examples show just how practical a trust can be. When you understand the different types available, you can choose the one that truly protects your assets and provides for your loved ones exactly how you wish. The right trust is more than a legal agreement; it's a powerful reflection of your values and goals.

Why Bother With a Trust? The Real-World Advantages

So, we've covered the "what" and the "how" of trusts. But the real question is why? Why go through the trouble of setting one up? The truth is, beyond the legal jargon, a trust is one of the most powerful tools available for smart wealth management. It's about protecting your assets, your family, and your peace of mind in a way a simple will just can't.

A well-designed trust offers a trifecta of benefits that make it a cornerstone of any solid estate plan: privacy, tax savings, and serious asset protection.

Bypassing the Probate Process

Probably the biggest and most immediate win of having a trust is avoiding probate. Probate is the court-supervised process of settling your estate, and frankly, it can be a nightmare.

Think of it as a public airing of your financial laundry. The process can drag on for months, sometimes even years. Everything—your will, your assets, your debts—becomes public record for anyone to see. On top of that, the legal and court fees can take a serious bite out of your estate, often calculated as a percentage of its total value. That's money that should be going to your loved ones.

By putting your assets into a trust, they are no longer legally part of your personal estate. When you pass away, the trustee can simply follow your instructions and distribute everything privately, without court intervention. It saves an incredible amount of time, money, and heartache for your family.

This smooth, private transfer is priceless. To really dig into the mechanics, check out our guide on how to avoid probate court.

A Powerful Tool for Tax Planning

Nobody wants to give more to the IRS than they absolutely have to. While a basic revocable trust won't do much for your taxes while you're alive, certain irrevocable trusts are absolute game-changers for minimizing estate taxes.

The federal estate tax exemption is pretty generous in 2024, but for high-net-worth families, it's surprisingly easy to blow past that limit. When you move assets into a properly structured irrevocable trust, they are officially removed from your taxable estate. This simple move can shield your beneficiaries from a massive tax bill.

Here are just a few ways this plays out:

- Generation-Skipping Trusts are fantastic for passing wealth directly to grandchildren while navigating complex transfer tax rules.

- Charitable Trusts not only let you support the causes you believe in but also give you significant tax deductions.

- Grantor Retained Annuity Trusts (GRATs) are a sophisticated strategy for passing asset growth to your heirs with little to no gift or estate tax.

Each of these is a specialized tool designed to keep more of your hard-earned wealth within the family.

Building a Fortress Around Your Assets

We live in a litigious world. Protecting what you've built from creditors, lawsuits, or a business deal gone wrong is more important than ever. This is where an irrevocable trust truly shines, creating a strong legal shield around your assets.

Let's say you're a business owner. If your company gets hit with a lawsuit or runs into financial trouble, your personal assets could be on the line. But if your home, your brokerage account, and other key assets are held in an irrevocable trust, they're generally untouchable.

Since you no longer technically "own" them, creditors can't come after them to settle your debts. It’s like building a financial fortress for your family, ensuring that the wealth you've created is safe, no matter what storms you might face.

How to Set Up a Trust for Your Family

Putting a trust together might sound like a daunting legal marathon, but it's really more of a practical project to safeguard your family's future. Think of it as a series of clear, straightforward steps that turn your financial wishes into a powerful legal reality. It all starts with one simple question: What do you want your wealth to accomplish?

This first step is all about getting to the heart of your goals. Are you focused on funding your children’s education? Is your priority protecting a loved one with special needs? Or is the main objective to make sure your assets sidestep the notoriously slow probate process? Your answers here will be your North Star, guiding every other decision you make.

Defining Your Trust’s Purpose and Parties

With your vision clear, it’s time to name the key players: your beneficiaries and your trustee. The beneficiaries are the people, charities, or organizations you want to receive assets from the trust. The more specific you can be about who gets what and when, the better.

Choosing a trustee is arguably the most important decision in this whole process. This individual or institution will be legally responsible for managing the trust’s assets and carrying out your instructions to the letter. You need to pick someone with unquestionable integrity, sharp financial sense, and a real grasp of what it means to be a fiduciary.

It’s the classic dilemma: should you pick a family member or a professional corporate trustee? A loved one knows your family inside and out, but a corporate trustee brings impartiality, deep expertise, and continuity, ensuring the trust is managed professionally for decades to come.

This choice is fundamental to understanding how a trust fund works in the real world. The trustee’s skill and judgment directly determine whether your plan succeeds.

Selecting the Right Trustee: A Key Decision

Picking the right manager for your trust isn’t just an administrative task—you're choosing a guardian for your legacy. It’s a decision that deserves serious consideration.

Let's break down the two main options:

- Individual Trustee (Family Member or Friend):

- Pros: They have personal insight into your family dynamics, might charge lower fees (if any), and intuitively understand what you intended.

- Cons: Their appointment can stir up family conflict, they may not have the necessary investment or legal expertise, and their own life events could interfere with their duties.

- Pros: You get professional asset management, in-house legal and tax knowledge, and complete neutrality. Plus, they are regulated and insured, adding a layer of security.

- Cons: They charge professional fees for their services, the relationship can feel less personal, and they often have minimum asset levels for accounts they’ll manage.

The best path forward often depends on your family’s specific needs and the complexity of your assets. Some people even appoint co-trustees—pairing a family member with a corporate entity—to get the perfect blend of personal touch and professional oversight.

The value of this kind of professional management is widely recognized. A 2025 Global Investor Survey revealed that institutional investors managing over $50 billion in assets lean heavily on trusts for risk management, and around 90% of private equity firms outsource their trust administration to specialists. You can discover more insights on global investor strategies on pwc.com. This just goes to show how critical professional guidance becomes when significant wealth is involved.

Working with an experienced estate planning attorney is the final, essential step to pull it all together and create a trust that truly lasts.

Your Top Trust Fund Questions, Answered

Once you get the basics of how a trust works, the practical questions start bubbling up. It’s one thing to understand the concept, but another to see how it applies in the real world. Let's tackle some of the most common questions we hear, clearing up the details of setting up and managing a trust.

How Much Money Do I Need to Start a Trust?

There’s a persistent myth that trusts are only for the mega-rich. The truth is, there’s no legal minimum amount of money required to set one up. The real question isn't "how much do I have?" but "what do I want to accomplish?"

A trust becomes a powerful tool when you have specific goals in mind—like shielding assets from the public probate process, ensuring a child with special needs is cared for, or protecting your wealth from future creditors. Yes, there are legal fees to draft the trust document, but for many families, that initial investment is a small price to pay for the future savings on estate taxes and the headaches of probate.

Can I Be the Trustee of My Own Trust?

Absolutely. In fact, for a revocable living trust, it's the standard way to do it. The person creating the trust (the grantor) typically serves as the initial trustee, giving them full control over their assets for as long as they live.

You simply name a "successor trustee" in the trust document—this is the person or institution you designate to step in and manage things if you become incapacitated or pass away. For certain irrevocable trusts, however, you can't be your own trustee. The entire point of those is to legally separate the assets from you for tax or asset protection reasons, and that requires giving up direct control.

What Happens if a Beneficiary and Trustee Disagree?

Disputes can and do happen, which is why a well-drafted trust agreement is your best defense. Think of the trust document as the official rulebook; it should clearly spell out the trustee's powers, duties, and limitations.

If a beneficiary is concerned about how the trust is being managed, the first step is always direct communication. They can, and should, request a formal accounting of the trust's finances. If the disagreement continues and the beneficiary suspects mismanagement or a breach of the trustee's duties, they have the right to take the matter to court.

A judge can step in to interpret the trust’s language, force the trustee to act, or even remove a trustee who isn't fulfilling their obligations. This legal safety net is precisely why choosing a competent, impartial, and trustworthy trustee is one of the most important decisions in this entire process.

Is a Trust Better Than a Will?

This is a classic question, but it sets up a false choice. They aren't rivals; they're teammates in a well-built estate plan. Each one does a different job.

- A Will: This document gives instructions for any assets still held in your personal name at death. Those assets have to go through probate court, which is a public and often slow-moving process.

- A Trust: This is a private entity that holds and manages the assets you transfer into it. Assets inside a trust completely bypass probate, offering far more privacy and control.

For anyone with significant assets, complex family situations, or a desire to keep their affairs private, a trust offers advantages a will simply can't. The key is figuring out how to use both effectively. For a deeper dive into this, check out our guide on whether you need a trust for your unique situation.

How Long Can a Trust Last?

A trust lasts for exactly as long as you want it to. The duration is entirely defined by the terms you set in the trust document.

Some trusts are built for a specific, short-term purpose. For instance, you might create one to hold an inheritance for a child until they reach a mature age, like 25 or 30. Once that condition is met, the trustee distributes the remaining assets, and the trust is dissolved.

Others are designed to last for generations. A dynasty trust, for example, can provide a financial backstop for your children, grandchildren, and even great-grandchildren. While state laws like the "rule against perpetuities" used to limit how long a trust could exist, many states have updated their rules to allow trusts to last for centuries, or even forever. This makes them an incredible tool for building a true family legacy.

At Commons Capital, we specialize in navigating the complexities of wealth management and estate planning for high-net-worth individuals and families. If you're ready to create a strategy that protects your assets and secures your legacy, we're here to help. Contact us today to learn more about our financial advisory services.