When evaluating irrevocable trust pros and cons, think of it as a sealed vault for your assets. Once the door closes, your funds gain creditor protection, significant estate-tax savings, and advanced estate planning strategies—but you also surrender day-to-day control.

These features make it a powerful estate planning strategy, especially for high-net-worth individuals considering Medicaid planning trusts or dynasty trust benefits.

Irrevocable Trust Pros And Cons Explained

Below is a snapshot of how these trusts stack up:

- Creditor protection: Assets are legally removed from your estate to defend against lawsuits and claims.

- Estate tax reduction: Moving property outside your taxable estate can lower both federal and state tax bills.

- Medicaid planning: After a five-year look-back, trust assets won’t count against eligibility limits.

- Loss of control: You can’t modify or revoke the trust without beneficiary or court approval.

- Costs and complexity: Setup fees often run between $2,000 and $20,000+, plus annual trustee and tax-prep expenses.

- Inflexibility: Adjusting for life changes requires formal amendments and sometimes legal sign-off.

Security Versus Control

With an irrevocable trust, you trade daily access for long-term protection.

When To Consider An Irrevocable Trust

This structure makes sense if you’re facing potential creditor claims or seeking hefty estate-tax relief. Seasoned estate planners turn to it for clients who:

- Are high-risk professionals needing lawsuit shields

- Have estates above the federal exemption threshold

- Want to plan for Medicaid eligibility down the road

For example, a business owner concerned about litigation may lock assets into a trust for protection, while weighing the impact on liquidity.

Summary Of Irrevocable Trust Pros And Cons

Before you pull the trigger, this table lays out the key advantages and drawbacks side by side.

Use this summary to decide if an irrevocable trust aligns with your long-term plan. When you’re ready to dive deeper into estate planning, check out our guide on whether you need an estate plan: Learn more about whether you need an estate plan

Understanding Irrevocable Trusts

At its core, an irrevocable trust works like handing your family’s most prized heirlooms to a safety-deposit box manager—you can’t just swing by and demand them back. Once assets move in, they’re legally detached from your estate.

You give up ownership and day-to-day control. A trustee steps in, handling investments, distributions and all the paperwork. Beneficiaries then receive those assets under the precise rules you’ve written down.

It’s called “irrevocable” because courts rarely let you change the terms without everyone’s OK. That permanence delivers powerful protection but leaves little room for last-minute tweaks.

Key Parties And Roles

Every trust revolves around three key players:

- Grantor: Contributes assets and surrenders legal ownership

- Trustee: Manages the trust, handles tax filings, and ensures compliance

- Beneficiary: Receives distributions once the trust’s conditions are met

This structure creates built-in checks and balances. For instance, a trustee can’t exceed the powers you’ve granted in the trust document.

Contrast With Revocable Trusts

Revocable trusts let you change beneficiaries or reverse course at any time—but they offer almost no creditor shield. If you face a lawsuit, those assets can still be reached.

By contrast, once you place property in an irrevocable trust, it’s off-limits to personal creditors. You lose flexibility, but gain a fortress.

Asset Lock

When property enters an irrevocable trust, courts see it as belonging to the trust rather than you.

Legal Framework

Irrevocable trusts live at the intersection of state trust statutes and the federal tax code. They require:

- A properly drafted trust deed signed and witnessed per state rules, following guidelines such as those from the American Bar Association (https://www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/)

- All assets to be re-titled or formally assigned into the trust

- Trustee’s fiduciary duty—prudent management and loyalty to beneficiaries

- Annual filings and tax returns in compliance with IRS regulations

For more detailed IRS requirements, see IRS Publication 559 (https://www.irs.gov/forms-pubs/about-publication-559). Skip any of these steps, and you risk losing the very benefits you set out to secure.

Creating A Mental Model

Think of an irrevocable trust as a glass jar full of coins, sealed with a coded lock you can’t reset. The coins accumulate interest and pass to heirs when the lock opens, but you can’t pry it off yourself.

This mental picture highlights why an irrevocable trust:

- Shields assets from creditors and legal claims

- Prevents you from dipping into the holdings on a whim

- Forces every transaction to run through the trustee

By picturing that sealed jar and understanding the legal framework, you’re better equipped to weigh the benefits and constraints of an irrevocable trust.

Key Takeaways

- An irrevocable trust locks assets away to guard against creditors and potential tax bites

- Grantors give up control but gain legal detachment and protection

- Trustees carry strict fiduciary duties, bound to follow the trust’s instructions

- Beneficiaries inherit under the precise conditions you’ve set

With these essentials in place, you can now compare irrevocable trusts against other vehicles and explore their real-world advantages. Next, we’ll dive deeper into scenarios where they shine—like estate-tax planning and long-term family wealth preservation.

Tip: Engage your estate attorney or financial advisor early to tailor the trust’s structure to your unique situation.

Key Advantages Of Irrevocable Trusts

Guard your wealth like a fortress. An irrevocable trust isn’t just another paperwork exercise—it’s a legal barrier that keeps assets out of reach when someone comes knocking. Unlike a revocable trust, once you place property inside, you give up control in exchange for that extra layer of protection.

A business owner I worked with, facing potential litigation, moved equity into an irrevocable trust. Overnight, that stake in the company felt as untouchable as jewels in a high-security vault.

That permanence can be daunting. You trade flexibility for security, so weighing the pros and cons carefully is crucial.

- Asset Protection Shield your holdings from lawsuits, bankruptcies, divorces and government claims

- Estate Tax Planning Transfer policy proceeds and other high-value assets outside your taxable estate

- Medicaid Eligibility Isolate resources under the five-year look-back rule

- Family Legacy Use dynasty trusts to pass wealth across generations

Asset Protection Enhancements

Think of an irrevocable trust as its own legal entity—courts treat trust assets almost like offshore accounts or buried treasure, beyond a creditor’s reach.

According to a UBS Global Wealth Management survey, 34% of ultra-high-net-worth individuals already rely on these trusts for protection, and another 16% are planning to adopt them soon. For more on trust regulations, refer to IRS Publication 559 (https://www.irs.gov/forms-pubs/about-publication-559).

Discover more insights about irrevocable trust costs in litigation risk centers worldwide Read the full research on cost of irrevocable trusts.

Assets inside an irrevocable trust are legally detached and beyond creditors’ reach.

Key jurisdictions for offshore trusts include:

- Cook Islands statutes that offer robust secrecy protections

- Nevis privacy rules designed to deter creditor claims

- Belize frameworks that avoid grantor-home-country taxes

By some estimates, the global market for irrevocable trusts is set to reach $6.77 billion by 2028, expanding at a 7.53% CAGR, reflecting growing confidence in their protective power.

Back on U.S. soil, states like South Dakota and Nevada boast onshore options with strong anti-creditor statutes. Clients in high-risk fields—entertainment, construction or oil—often hear these recommendations first.

Estate Tax Savings Through ILIT

An Irrevocable Life Insurance Trust (ILIT) removes life insurance proceeds from your estate for both federal and state tax purposes.

- Setup fees typically run $3,000–$6,000

- Annual compliance (Crummey notices, trustee services) costs around $250–$1,000

Once the trust owns the policy, payouts go straight to beneficiaries—avoiding probate and giving them quick access to cash for taxes or debts.

- At a 40% federal estate-tax rate, placing a $2 million policy in an ILIT can save heirs up to $800,000

- For an estate valued at $12 million, ILIT planning can trim more than $3 million off your tax bill when thresholds shift

- Premiums funded by annual gifts stay under gift-tax limits

- Cash value growth remains outside your estate

- Trust-held benefits bypass probate, accelerating distributions

Multigenerational Wealth Transfer

Dynasty trusts act like a perpetual family endowment. They let your heirs use capital for education or business ventures without repeated estate taxes chipping away at the principal.

In jurisdictions without perpetuity rules—Delaware or Alaska, for example—these trusts can run indefinitely, locking in benefits for third, fourth and even fifth generations. You decide when and how funds are distributed, and custom reporting keeps everything transparent.

Consider provisions such as:

- Charitable giving or a family council to oversee distributions

- Clawback clauses to reclaim assets if a beneficiary encounters legal trouble

- Built-in mechanisms for periodic reviews to adapt to changing family dynamics

Benefits For Medicaid Planning

Medicaid Asset Protection Trusts (MAPTs) help seniors safeguard resources under the five-year look-back rule. By moving assets early, applicants avoid home equity assessments that might otherwise disqualify them.

A professional trustee times transfers to fit each state’s Medicaid rules, steering clear of common pitfalls.

For strategies avoiding court delays, check out our guide on how to avoid probate court.

Irrevocable trusts demand thoughtful setup, but once in place they become the backbone of many estate plans—offering lasting security, tax savings and creditor defense. Always partner with your advisor to tailor the details to your unique situation.

Key Limitations Of Irrevocable Trusts

Locking assets into an irrevocable trust is like sealing valuables in a safety-deposit box. You gain a sturdy layer of protection from creditors and taxes—but you also hand over the key forever.

Before funding a trust, step back and consider how rigid it can be. Life throws curveballs—business shifts, family changes, medical emergencies—and an unchangeable agreement can become a burden if you can’t adapt.

- Loss of Control

Once assets move in, you cannot tweak trust terms without beneficiary or court approval. What once felt smart can quickly feel like a straitjacket. - Trustee Discretion

The appointed trustee holds wide authority over distributions and investments. If relatives disagree, that power can spark heated disputes. - Administrative Complexity

Irrevocable trusts carry ongoing tasks—annual tax filings, Crummey notices and detailed accounting. You’ll need professional support, and those invoices add up fast. - High Costs

Setup fees range from $2,000 to over $20,000, plus yearly trustee and tax-prep expenses of $500–$3,000. - Rigidity When Needs Shift

If markets falter or family priorities evolve, adjusting an irrevocable trust usually requires court intervention—and extra legal fees.

Family Disputes And Trustee Power

Picture Thanksgiving with Uncle Joe in charge of the gravy boat—he doles out each pour, and you just watch. Swap gravy for trust distributions, and you get the idea.

When beneficiaries feel sidelined, disagreements can escalate into costly litigation.

With an irrevocable trust, you hand over the carving knife, trusting someone else to carve the turkey.

Despite these hurdles, irrevocable trusts have climbed in popularity. A 2020 survey by WealthCounsel, LLC and Trusts & Estates magazine found 63% of attorneys reporting increased usage, 34% of ultra-high-net-worth individuals already holding one, and another 16% planning to set one up within five years.

Data Bridge Market Research projects the global market growing at a 7.53% CAGR, hitting $6.77 billion by 2028.

Learn more about irrevocable trust trends

Case Studies Of Changing Circumstances

Consider a retired couple who funded a trust to cover long-term care. When one spouse lost mobility, they couldn’t tap into those funds fast enough for home modifications.

They waited months for court approval to adjust the trust. In that time, construction costs soared and care options dwindled—turning a sound plan into a costly scramble.

Administrative And Legal Burdens

Every clause in an irrevocable trust document carries weight. A misplaced phrase can trigger penalties or render a provision unenforceable.

- Professional fees at setup can range from $2,500–$10,000.

- Trusts file separate tax returns, with steep fines for missed deadlines.

- Crummey notices require precise mailing to each gift beneficiary on schedule.

These expenses mount quickly, especially if your trust spans multiple states or asset types.

Weighing Long-Term Trade Offs

Irrevocable trusts demand a forward-looking mindset. You must anticipate business pivots, family dynamics and healthcare needs years ahead.

Some grantors strike a balance: keep core assets revocable and move only select holdings into an irrevocable vehicle.

- Map out life events against trust terms to spot clashes early.

- Run scenarios by your attorney before signing.

- Keep beneficiaries in the loop to align expectations.

- Consider a trust protector role for limited amendment powers.

Balancing permanence and adaptability is key—too much rigidity can cost more than protection offers.

Flexibility Options And Alternatives

If absolute inflexibility feels too risky, mix and match. A revocable trust handles everyday estate planning, while smaller irrevocable trusts shield life insurance or business interests.

Hybrid setups often appoint a trust protector to approve changes under predefined conditions. You might also explore:

- LLCs or Family Limited Partnerships: Provide liability protection and operational control, though governance can get complex.

- Trust Protector Clauses: Grant a neutral third party limited amendment powers, adding oversight without full control.

Your ideal structure depends on your asset mix, risk tolerance and willingness to involve outside decision-makers.

Key Takeaways On Limitations

An irrevocable trust is a trade-off: ironclad protection in exchange for permanent control loss.

Weigh setup and maintenance costs against the security you gain. Chart potential future events—divorce, business sale or health crises—and test whether your trust terms still fit.

If you need more flexibility, consider hybrid strategies or alternative vehicles that strike a better balance between security and adaptability.

Comparing Irrevocable And Revocable Trusts

Think of your assets as either stashed in sealed safety-deposit boxes or held in an open debit account.

A revocable trust is like that debit account—you can dip in whenever you like, but it offers only modest protection.

By contrast, an irrevocable trust locks your assets away. You give up direct control, but you gain robust creditor protection and advanced tax planning options.

Key Differences And Use Cases

A revocable trust gives you complete flexibility. You can tweak terms or dissolve it at any point. That makes sense if you expect your circumstances to shift.

However, your assets remain in your taxable estate and are fair game for creditors.

Irrevocable trusts ask for an upfront commitment. Once you transfer property, it’s off your balance sheet.

That step unlocks strategies like Medicaid planning or designing a multi-generation dynasty trust.

- Use an irrevocable trust to shelter assets from lawsuits and reduce estate taxes.

- Opt for a revocable trust when you want to avoid probate yet keep decision-making power.

- Draft a pour-over will to catch any assets you forgot to transfer.

- Form a family limited partnership if you need both liability protection and operational flexibility.

Weigh your appetite for control against your exposure to creditors and tax obligations.

When To Choose Each Option

If you’re looking at Medicaid’s five-year look-back rule, an irrevocable asset protection trust often outperforms a revocable setup.

High-net-worth families wanting to minimize estate taxes frequently layer in ILITs or dynasty trusts.

When privacy and a streamlined probate-avoidance process top your list, revocable trusts usually win. They’re simple to modify and don’t impose permanent constraints.

- Medicaid Planning: Shield assets from eligibility calculations over an extended look-back period.

- Probate Avoidance: Keep details of your estate private and bypass court delays.

- Business Succession: Transfer ownership interests with built-in valuation discounts.

You might also appreciate our in-depth analysis of the Intentionally Defective Grantor Trust. It dives deep into grantor trust tax mechanics and explains where they fit in a broader estate plan.

Strategic Decision Factors

Choosing between these vehicles means balancing irrevocable trust pros and cons with your family’s timeline, cash flow, and risk tolerance.

Consider setup and maintenance costs, ongoing administrative demands, and any built-in flexibility—like trust protectors or limited amendment clauses.

Many plans combine a revocable “core” trust for flexibility with specialized irrevocable trusts for assets like life insurance or investment accounts. That hybrid approach can give you the best of both worlds.

- Compare costs versus benefits for formation and annual oversight.

- Decide how much control you’re willing to relinquish in exchange for protection.

- Account for family dynamics and each generation’s comfort with trust structures.

Putting these tools side by side clarifies which model aligns with your goals. Evaluate liquidity needs, tax exposure, and legacy objectives before settling on the right trust strategy.

A clear comparison empowers you to choose confidently and craft a plan that reflects your family’s story.

Next up: detailed, step-by-step guidance on drafting and funding your chosen trust vehicle.

Practical Steps to Establish an Irrevocable Trust

Turning a plan into reality means moving beyond theory. In the following sections, we’ll walk you through each stage—whether you’re setting up an ILIT, dynasty trust, or charitable trust—so you can balance control, protection, and tax benefits with confidence.

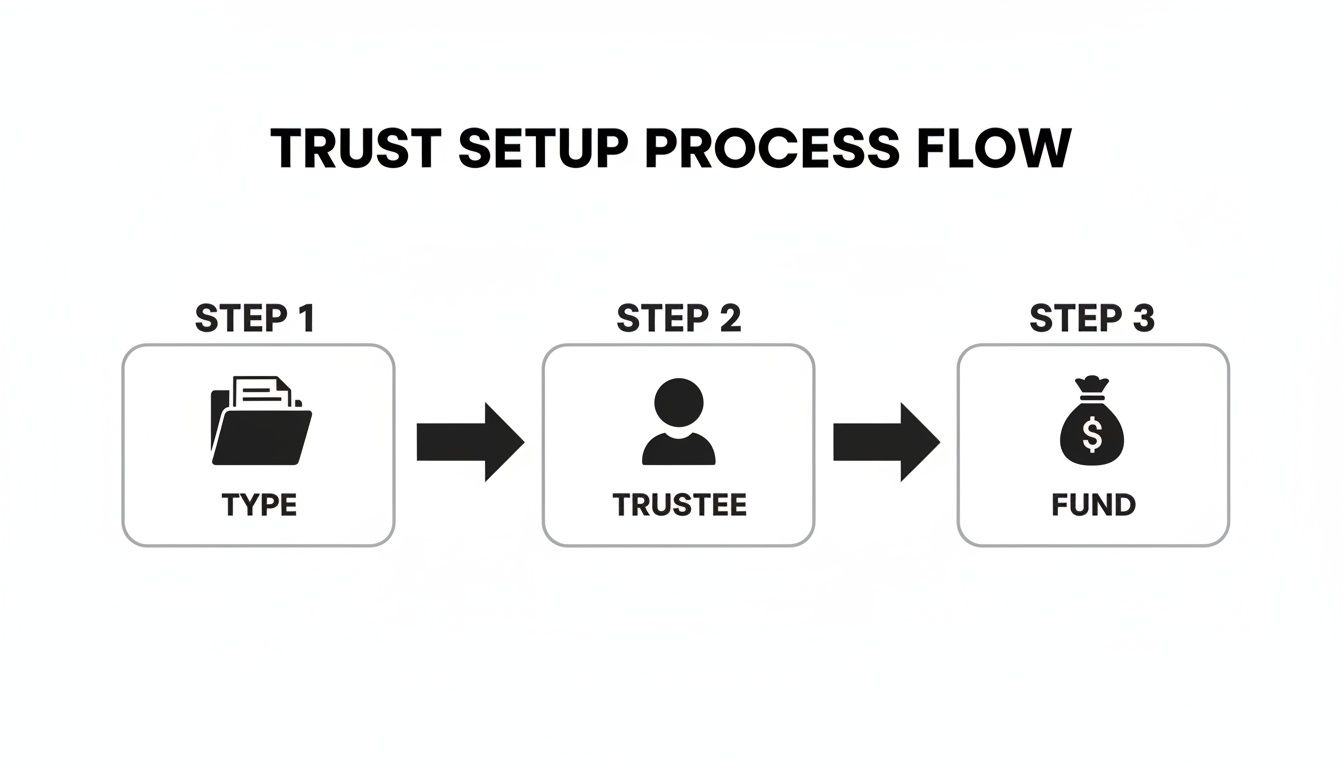

Choose Your Trust Type

Think of trust selection like picking the right vehicle for a journey—it needs to fit both your roadmap and your passengers.

- ILIT for keeping life insurance proceeds out of your taxable estate.

- Dynasty Trust to preserve wealth across several generations.

- Charitable Trust when you want to support causes while unlocking tax deductions.

Each structure carries its own trade-offs. Pause here to weigh flexibility against the protection each trust provides.

Select a Qualified Trustee

Now imagine handing over the car keys to someone you trust on a cross-country trip. Your trustee is that driver, responsible for steering assets and following your directions.

- Proven fiduciary experience in estate or trust administration.

- A clear understanding of family dynamics and long-term goals.

- Professional firms or banks when the asset mix is complex.

A capable trustee isn’t just paperwork—it’s the difference between smooth compliance and costly missteps.

The following infographic visualizes the three core steps in a horizontal process flow: selecting trust type, appointing trustee, and funding assets.

Notice how each phase builds on the last, underscoring the seamless flow from decision to funding.

Fund the Trust Correctly

With a trustee in place, funding your trust cements the plan and activates its protections.

- 1. Retitle bank and investment accounts in the trust’s name.

- 2. Transfer real estate deeds, vehicle titles, and business interests.

- 3. Obtain a separate EIN for tax reporting.

- 4. Send Crummey notices to beneficiaries to secure gift-tax exclusions.

- 5. Update beneficiary designations on IRAs or 401(k)s where allowed.

- 6. Record deeds and file transfers with the proper state agencies.

Skip any step and you risk voiding key protections or triggering unexpected tax liabilities.

Execute Documents and Avoid Common Pitfalls

After funding, finalize every trust document to lock in your strategy.

A fully funded trust only protects assets you’ve properly retitled.

Watch out for these missteps:

- Forgetting to transfer property deeds.

- Overlooking state-specific trust code requirements.

- Neglecting annual filings, accounting, and notices.

To stay on track, try these best practices:

- Map out deadlines on a simple timeline.

- Schedule annual reviews with your estate attorney.

- Keep beneficiaries informed to minimize disputes.

When the details start piling up, don’t hesitate to bring in additional counsel. Their guidance ensures you remain compliant and aligned with your objectives. Ultimately, a clear roadmap helps you lock in asset protection and tax savings while managing the trade-offs.

Monitor and Review Regularly

An irrevocable trust isn’t a “set-it-and-forget-it” plan. Regular check-ins keep it aligned with changing laws and personal circumstances.

- Review asset allocations and trust investments on an annual basis.

- Confirm state law changes haven’t affected trust provisions or required filings.

- Update Crummey notice templates and beneficiary contact information.

Clients often uncover opportunities to refine distribution schedules or add successor trustees. Small course corrections now can prevent costly disputes later. Loop in your attorney or financial advisor at each review for airtight compliance. This ongoing diligence turns your trust into a living strategy that continues protecting your assets over time.

By following these practical steps—from choosing the right type to monitoring performance—you’ll navigate the top irrevocable trust pros and cons with clarity and confidence, ensuring your estate plan runs smoothly.

Frequently Asked Questions

What Are The Primary Benefits And Risks Of An Irrevocable Trust?

When you transfer assets into an irrevocable trust, you’re swapping flexibility for protection. You lock in creditor shields and estate-tax savings, but you also give up the ability to change terms later and incur setup costs.

Consider a business owner who places company equity in a trust to guard against lawsuits. The trade-off is clear: strong legal walls at the expense of future adjustments. Planning ahead makes all the difference.

How Does An Irrevocable Trust Protect Assets From Creditors And Lawsuits?

Imagine sliding valuables into a fireproof safe. Once inside, they’re legally detached from your estate. Creditors can’t grab what they can’t reach—unless they challenge the trust’s validity in court.

Assets in an irrevocable trust are like valuables in a sealed vault—untouchable without a court key.

- Assets held in trust are separate from your personal estate

- Most creditor claims are blocked, keeping your wealth out of harm’s way

Ongoing Tax And Reporting Obligations

After funding, an irrevocable trust stands on its own for tax purposes. You’ll need to:

- Obtain an EIN

- File Form 1041 annually

- Distribute Schedule K-1 to each beneficiary

- Send Crummey notices if you’re using gift-tax exclusions

Miss a step and you risk penalties or unintended tax consequences. Working with a tax professional ensures you stay on track.

When To Seek Professional Advice

Drafting an irrevocable trust is a complex endeavor. Consult an estate-planning attorney first to craft airtight terms and navigate state statutes.

Once the trust is in place, bring a financial advisor on board to:

- Select investments that align with your goals

- Help choose and oversee trustees

Combining legal and financial expertise lets you sidestep pitfalls and make the most of your trust.

—

Ready to protect your wealth? Contact Commons Capital for expert guidance designed for high-net-worth clients.