You’ve built real wealth. Now the easy answers stop working.

If you’re married, have meaningful assets, and expect tax law to get less generous after 2025, “leave everything to my spouse” is often too simplistic. It may be fine. It may also be a costly mistake.

That’s where what is a disclaimer trust becomes the right question. Not because it’s a trendy estate planning term, but because it gives your family something rare in this area: flexibility after the first death, when the facts are finally clear.

The High-Net-Worth Dilemma Planning for an Uncertain Future

A high-net-worth family usually wants four things at once.

They want the surviving spouse taken care of. They want assets to reach children efficiently. They want to reduce transfer tax friction where possible. They also want protection against future messes, including creditors, remarriage complications, and family conflict.

Those goals don’t always fit neatly inside a simple will.

A disclaimer trust works well because it gives a married couple a “wait-and-see” option. You don’t lock in every decision years before it matters. Instead, your documents create the option for the surviving spouse to redirect certain inherited assets into a trust after the first spouse dies.

That flexibility matters when the law is moving, family needs are changing, and the asset mix isn’t static.

Why affluent families use this strategy

Think of your estate plan like a ship’s route. A rigid plan assumes the weather will cooperate. A disclaimer trust assumes conditions may change, so it keeps a course correction available.

That’s especially useful if your estate includes:

- Concentrated wealth: business interests, stock positions, or real estate that may appreciate quickly

- Blended family concerns: children from a prior marriage or second-marriage planning

- Liability exposure: public-facing careers, business ownership, or industries where claims are more common

- State tax pressure: especially if you live in a state with its own estate tax rules

A good plan also accounts for later-life care decisions. Families often underestimate how quickly healthcare and long-term care questions can reshape planning priorities. If that’s part of your conversation, a practical resource on Medicare coverage for nursing home stays helps frame what Medicare does and doesn’t cover.

The strategic point many overlook

A disclaimer trust isn’t mainly about legal wording. It’s about control at the moment when control matters most.

Practical rule: If your family’s net worth, tax exposure, or liability risk could look very different in a few years, flexibility has value by itself.

For many affluent couples, the right estate plan isn’t the one with the most moving parts. It’s the one that gives the surviving spouse a usable decision at the right time.

Understanding the Core Mechanics of a Disclaimer Trust

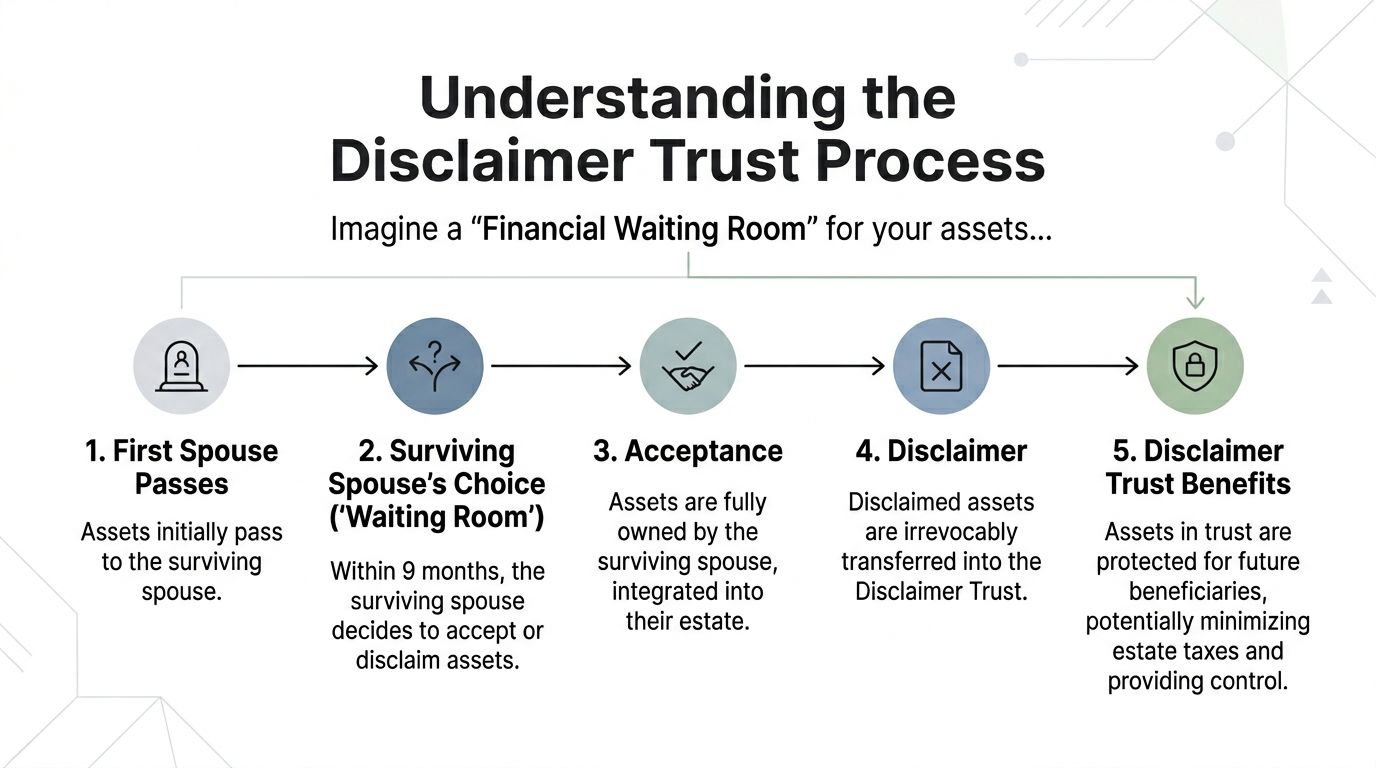

A disclaimer trust is easiest to understand if you stop thinking about it as a trust first and start thinking about it as a decision window.

The assets don’t automatically have to land in the trust. The surviving spouse gets a limited period to decide whether some inherited assets should stay in their own hands or be redirected into a protected structure.

Think of it as a financial waiting room

The best analogy is a financial waiting room.

When the first spouse dies, assets are set up to pass to the surviving spouse. But before that transfer is fully accepted, the surviving spouse can refuse part or all of what they would otherwise inherit. That refusal is the disclaimer.

The refused assets then pass into the disclaimer trust under the terms already built into the estate plan.

If you accept the inheritance outright, those assets generally become part of your estate. If you disclaim them properly, they move into the trust instead.

The legal requirements are strict

Consequently, legal requirements are strict, and errors can lead to undesirable outcomes.

According to Western & Southern’s explanation of disclaimer trusts, a disclaimer trust allows a surviving spouse to disclaim inherited assets so they pass into an irrevocable trust to use the deceased spouse’s estate tax exemption and help shield assets from future taxes, creditors, and claims. The disclaimer must be a qualified disclaimer under IRS Section 2518, and it must be in writing, irrevocable, and completed within 9 months of the first spouse’s death.

That deadline is not a planning suggestion. It’s a hard stop.

How the sequence usually works

The estate plan is drafted in advance.

The will or revocable trust includes disclaimer trust provisions.The first spouse dies.

Assets are positioned to pass to the surviving spouse, subject to the disclaimer option.The surviving spouse evaluates the situation.

This includes tax law, state estate tax exposure, asset values, creditor concerns, and family dynamics.A written qualified disclaimer is signed if appropriate.

Once made, it’s irrevocable.Disclaimed assets fund the trust.

From there, those assets are managed under the trust terms for the spouse and eventual heirs.

Who plays which role

This setup is easier when you know who does what.

- Deceased spouse: creates the structure that allows the option to exist

- Surviving spouse: decides whether to accept assets outright or disclaim them

- Trustee: manages the trust once funded

- Children or other heirs: receive what remains under the trust terms later

In many families, the surviving spouse may still benefit from the trust. That’s the point. The strategy isn’t to disinherit the spouse. It’s to separate ownership from benefit in a deliberate way.

Why mechanics matter more than theory

A disclaimer trust is powerful because it turns uncertainty into a decision process.

That’s very different from a plan that auto-funds no matter what, and it’s very different from a plan that leaves everything outright and hopes portability or later fixes will be enough.

If you’re still sorting out whether a trust structure fits your broader estate plan, this overview on do I need a trust is a useful starting point.

The best disclaimer trust plans feel quiet before they’re needed and decisive when they are.

One practical example from the same Western & Southern discussion is worth noting once because it shows how state-level planning can drive the decision. In that example, spouses with $5.5 million in combined assets could save over $500,000 in New York estate taxes by disclaiming assets into the trust and using the deceased spouse’s state exemption, rather than letting those assets remain in the survivor’s estate and create tax on the second death.

That is the heart of the mechanism. The trust isn’t magic. The timing, legal form, and prebuilt design are what make it work.

Disclaimer Trust vs Other Common Inheritance Strategies

Most estate planning mistakes happen because families compare one strategy against nothing.

That’s the wrong frame.

You should compare a disclaimer trust against the actual alternatives your attorney might put on the table: outright inheritance, a QTIP trust, and a traditional bypass trust. Each works. Each also forces tradeoffs.

The practical comparison

An outright inheritance is simple. Simplicity is appealing, especially after a death. But simple isn’t the same as efficient or protected.

A QTIP trust can provide control over where assets go after the surviving spouse dies. That’s often useful in second-marriage planning. But it doesn’t give the surviving spouse the same post-death choice that a disclaimer trust does.

A bypass trust captures the first spouse’s exemption automatically. That can be effective, but it removes the “wait-and-see” advantage. You’re funding the trust because the document says so, not because the post-death facts justify it.

Inheritance Strategy Comparison

| Feature | Disclaimer Trust | Outright Inheritance | QTIP Trust | Bypass Trust |

|---|---|---|---|---|

| Flexibility after first death | High. Surviving spouse can decide whether to disclaim assets into trust | Low. Assets pass directly and become personal property | Moderate. Structure is fixed, with less post-death choice for survivor | Low to moderate. Trust typically funds automatically |

| Asset protection | Stronger than outright ownership because assets placed in trust are separated from survivor’s personal estate | Weak. Assets are exposed as part of survivor’s estate | Can offer structure and control, but depends on design | Strong. Assets in trust are generally more protected than outright ownership |

| Tax planning adaptability | Strong because decision happens after facts are known | Weak. Few built-in corrections once assets pass outright | Useful in some marital planning situations, but less flexible in timing | Strong on exemption use, weaker on flexibility |

| Control over ultimate heirs | Strong. Trust terms can direct assets to children or other beneficiaries | Weak if survivor later changes plan | Strong. Often used when first spouse wants to control final disposition | Strong |

| Ease of administration | Moderate. Requires timely action and coordination | High. Easiest path operationally | Moderate to high depending on assets | Moderate |

| Best fit | Families who want optionality, tax awareness, and protection | Families prioritizing simplicity over control and shielding | Families focused on controlling ultimate inheritance after survivor’s death | Families comfortable committing to trust funding in advance |

Where outright inheritance falls short

Outright inheritance is the default because it’s easy to explain.

It’s also the path of least resistance for families who haven’t thought through second-order risk.

If the surviving spouse owns everything personally, those assets are usually easier to reach through future claims, easier to redirect through a changed estate plan, and easier to include fully in the survivor’s taxable estate. For a modest estate, that may be acceptable. For a substantial one, it can be lazy planning.

When a QTIP trust is the better tool

A QTIP trust earns its keep when control over the remainder beneficiaries is the central issue.

For example, if a spouse wants to provide income and support to a surviving spouse but ensure the remaining assets pass to children from a prior marriage, a QTIP may be the cleaner tool. The tradeoff is reduced flexibility at the decision point after death.

A disclaimer trust is usually better when your family wants options later. A QTIP is often better when the first spouse wants to lock in a specific path from the start.

Why bypass trusts still matter

Bypass trusts still solve a real problem. They force use of the first spouse’s exemption and keep those assets outside the survivor’s estate.

That automatic feature is both their strength and their weakness.

If tax law shifts, exemptions remain generous, or the family’s asset picture changes, the trust may be funded in a way that no longer feels ideal. The disclaimer trust avoids that rigidity.

My recommendation for affluent families

If your estate is substantial, your family dynamics are layered, or your liability risk is real, don’t default to outright inheritance.

Use a disclaimer trust when flexibility is the goal. Use a QTIP when control over ultimate beneficiaries is the main objective. Use a bypass trust when certainty matters more than optionality.

If you’re still comparing baseline estate planning structures, this breakdown of a living trust will helps clarify how those documents fit together.

Good estate planning doesn’t chase the fanciest structure. It chooses the structure that best handles your family’s likely problems.

The Portability Dilemma When a Trust Beats the Exemption

The most common objection to a disclaimer trust is straightforward.

“If portability exists, why add a trust?”

Because portability solves only part of the problem.

What portability does well

Portability lets a surviving spouse use the deceased spouse’s unused federal estate tax exemption if the proper election is made.

That’s administratively appealing. It can preserve tax capacity without forcing trust funding right away. For many couples, especially those with more straightforward estates and low liability concerns, that simplicity is attractive.

But simplicity has a cost.

Where portability stops helping

Portability does not create a protective wrapper around the assets.

According to GK Legal’s discussion of disclaimer trusts and portability, the federal estate tax exemption is projected to revert to approximately $7 million in 2026 from its current high. That same source notes that portability offers no creditor protection, and for high-net-worth individuals with estates above $14 million after that projected reversion, failing to fund a trust could expose assets to a 40% federal estate tax. It also notes that for clients in higher-risk professions such as sports or entertainment, creditor claims rose 15% in 2025, which makes trust-based protection more compelling.

This highlights the core distinction.

Portability is a tax election. A disclaimer trust is a structural solution.

Why 2026 changes the conversation

The temporary generosity of the current exemption environment has encouraged complacency.

Many affluent couples assumed their federal estate tax issue had faded. That assumption may not hold if the exemption drops as projected. Families who were comfortably below the threshold may find themselves closer than expected, especially if their balance sheet includes a business, appreciated securities, private investments, or real estate.

A disclaimer trust helps because it preserves a decision after the first death. If the projected lower exemption materializes and you need to plan around it, the surviving spouse can act.

Asset protection is the non-tax reason that matters

Asset protection is the non-tax reason that matters. Many advisors, I believe, undersell this issue.

If your wealth sits outright with the surviving spouse, you’ve simplified ownership but increased exposure. For clients in sports, entertainment, entrepreneurship, or any field with public visibility or litigation risk, that matters a lot.

A trust can also protect family intent. If the surviving spouse remarries, changes course, or faces outside influence, trust terms can keep the original family wealth moving to the intended beneficiaries.

That’s one reason families often start with the broader estate-planning question of the difference between a will and a trust. The distinction isn’t academic. A trust can accomplish things a will alone cannot do once risk enters the picture.

My view on the portability debate

Use portability when it fits. Don’t worship it because it’s convenient.

For affluent families, portability is often the backup tool, not the primary strategy. It can preserve an exemption. It can’t create control, creditor shielding, or disciplined inheritance design.

Bottom line: If your concern is only federal exemption carryover, portability may be enough. If your concern includes protection, control, and post-2025 uncertainty, a disclaimer trust is usually the more complete answer.

Real-World Scenarios for High-Net-Worth Families

The value of a disclaimer trust becomes clearer when you stop treating it as a document and start treating it as a response to a family’s actual risks.

The athlete with visibility and liability risk

A professional athlete’s planning problem is rarely just taxes.

The bigger issue is exposure. Public profile creates attention. Attention creates claims, disputes, and pressure. Even when a claim has no merit, the target still spends time, money, and energy dealing with it.

In this family, the couple had substantial earnings, endorsement income, and a fast-changing asset base. Some years looked ordinary. Other years didn’t. They didn’t want an estate plan that assumed the same balance sheet forever.

The disclaimer trust fit because it left room to decide after the first death whether assets should move into a protected structure rather than pass outright to the survivor.

The logic was simple:

- If the estate and legal environment looked benign, the surviving spouse could accept assets outright.

- If exposure appeared high, the spouse could disclaim selected assets into trust.

- If children were still young, the trust could add discipline around when and how inherited wealth would eventually pass.

Affluent families benefit greatly from optionality in this type of situation. The athlete’s family didn’t need maximum complexity. They needed the right lever available at the right moment.

The family office focused on legacy control

Another family had a different concern.

They already had wealth spanning generations, and their anxiety wasn’t centered on immediate estate tax alone. They were focused on keeping family wealth inside the family line while still treating the surviving spouse generously.

One adult child had a stable marriage. Another child’s personal life looked less predictable. The parents didn’t want inherited assets drifting into a future divorce battle or being redirected by someone outside the family.

A disclaimer trust helped because it separated support from outright ownership. The surviving spouse could still benefit from trust assets, but the family’s governing documents could maintain guardrails over where those assets ultimately went.

Wealth transfer fails when parents confuse affection with structure. You can be generous and still be precise.

This kind of planning is especially important when multiple households, second marriages, or uneven maturity among heirs are involved. Families often assume “everyone will do the right thing later.” That’s not a strategy. That’s hope wearing a suit.

The entrepreneur with an illiquid business

A business owner faces a different challenge. Their balance sheet may look large on paper while remaining awkward in real life.

One spouse owned the family company. Much of the household net worth sat inside that business. The couple wanted to preserve flexibility because they didn’t know what the company would be worth at the first death, whether a sale would be pending, or whether the surviving spouse would want liquidity, control, or both.

An automatic trust funding formula would have forced decisions too early. Outright inheritance would have solved for simplicity but ignored future exposure.

The disclaimer trust created breathing room.

After the first death, the surviving spouse and advisory team could evaluate:

- business valuation and liquidity,

- whether a sale process was underway,

- whether family members would remain involved,

- and whether the survivor needed direct ownership or protected economic benefit.

In practice, that flexibility can reduce pressure at exactly the wrong time. A surviving spouse doesn’t have to make every major estate and ownership decision before the dust settles. But they also can’t drift indefinitely. The decision window forces focus.

Why these scenarios matter

These families don’t share the same profile.

One is exposed to public claims. One is worried about family-line preservation. One is managing an illiquid operating asset. The common thread is that each family benefits from a structure that doesn’t require total commitment before the facts are known.

That’s why I recommend disclaimer trusts most often for affluent households with any combination of:

- Volatile asset values

- Liability concerns

- Complex family relationships

- Strong desire to direct where wealth ultimately lands

The trust isn’t always funded. That’s part of its strength.

The point is to build a plan that gives your family a high-quality choice later, rather than a rushed choice or no choice at all.

Implementing a Disclaimer Trust Steps and Key Advisor Questions

A disclaimer trust only works if it’s built correctly before it’s needed and handled correctly after a death.

That sounds obvious. Families still miss it all the time.

The implementation roadmap

Start with the estate planning documents.

Your attorney has to draft the disclaimer trust provisions into the will or revocable trust. If the language isn’t there, the strategy usually isn’t available later. You can’t improvise this after the first spouse dies.

Then make sure the asset map matches the plan.

Beneficiary designations, titling, and overall ownership structure should be reviewed together. A beautifully drafted trust provision won’t help much if the wrong assets bypass the plan entirely.

Once the first spouse dies, the advisory team needs to move quickly. The surviving spouse, estate attorney, CPA, and wealth advisor should evaluate whether disclaiming makes sense based on the legal, tax, and family circumstances that exist at that moment.

The decision checklist after the first death

- Review the deadline: The disclaimer window is time-sensitive, so the family needs a calendar-driven process immediately.

- Assess state tax exposure: In many cases, state law is what drives the value of the trust.

- Evaluate liability risk: If the surviving spouse has meaningful exposure, trust funding becomes more attractive.

- Check family dynamics: Remarriage concerns, beneficiary maturity, and blended-family issues matter.

- Consider cash flow needs: The surviving spouse still needs enough access and support under the trust terms.

Questions to ask your attorney, CPA, and advisor

Some questions should be blunt.

Ask your estate planning attorney

- How does my state treat estate tax planning for married couples?

- What assets are best positioned to pass through a disclaimer path rather than outright?

- Can the surviving spouse serve in a fiduciary role without creating tax or control problems?

- How are remainder beneficiaries defined if family relationships change later?

Ask your CPA

- What tax filings and elections become critical after the first death?

- How will the chosen structure affect basis, reporting, and future administration?

- Which state-level issues should we model now rather than later?

Ask your wealth advisor

- How would trust funding change the portfolio design and liquidity plan?

- Which assets should remain readily available to the surviving spouse?

- How should investment oversight work if the trust becomes funded?

If you want a stronger list before that meeting, these questions to ask a wealth manager are a useful prompt.

The mistake I’d avoid

Don’t treat the disclaimer trust as a legal ornament.

It should be integrated with investment management, tax planning, insurance review, and family governance. If the trust exists only in your documents and not in your decision-making process, it’s not a strategy. It’s paperwork.

Your estate plan should function like an operating system, not a stack of disconnected files.

Frequently Asked Questions About Disclaimer Trusts

Can a surviving spouse disclaim only part of the inheritance

Yes, a disclaimer can apply to some assets rather than all assets, assuming the documents and legal requirements support that approach.

That partial flexibility is one reason disclaimer trusts are useful. The surviving spouse may want some assets outright for liquidity and convenience while moving others into the trust for protection or transfer-tax reasons.

Can the surviving spouse still benefit from the trust

Often, yes.

A well-designed trust can allow the surviving spouse to receive income and, depending on the terms, additional distributions under a defined standard. The point isn’t to cut the spouse off. The point is to avoid outright ownership while still providing support.

What’s the biggest downside

Irrevocability.

Once a qualified disclaimer is made, it can’t be undone. That’s why this strategy requires careful analysis during the decision window. It also brings administrative work because a funded trust has to be managed, invested, and documented properly.

Is a disclaimer trust only about taxes

No.

Tax planning is one reason to use it, but many affluent families care just as much about creditor shielding, remarriage risk, and controlling where assets ultimately go.

Does it work with retirement accounts

Potentially, but this area gets technical fast.

Retirement accounts involve separate beneficiary rules, tax consequences, and drafting issues. If IRAs or other tax-deferred accounts are a major part of the estate, your attorney and CPA need to review them carefully rather than assume the disclaimer approach works cleanly across the board.

Who should seriously consider one

Married couples with substantial assets, meaningful state estate tax exposure, creditor concerns, complex family relationships, or a strong desire for legacy control should have this conversation.

If your plan has to survive law changes, market changes, and family changes, a disclaimer trust deserves a hard look.

If you’re weighing whether a disclaimer trust belongs in your estate plan, Commons Capital can help you think through the wealth planning side of the decision. We work with high-net-worth individuals, families, business owners, and clients in sports and entertainment to align estate strategy with investment management, tax awareness, and long-term family goals.