Meta title: Grantor Retained Annuity Trust Guide

Meta description: Learn when a grantor retained annuity trust works, its risks, tax rules, and how HNW investors use GRATs with volatile assets.

If you have a concentrated stock position, a growing private company, or equity compensation with real upside, you may be facing a familiar estate planning problem. You want your family to benefit from the future appreciation, but you do not want to make a large taxable gift today or consume valuable exemption unnecessarily.

That is where a grantor retained annuity trust often enters the conversation. Used well, it can move future growth out of your estate while returning a stream of annuity payments back to you over a defined term. Used poorly, it can become an expensive exercise that produces little more than paperwork.

For high-net-worth families, the primary question is not whether a GRAT is complex. It is whether it is the right tool for the asset, the timing, the family objective, and the grantor’s risk profile. Clients exploring broader strategies to minimize estate taxes often find that a GRAT belongs in the discussion when they hold assets with credible upside and want to preserve flexibility around lifetime exemption.

An Introduction to Tax-Efficient Wealth Transfer

A successful founder sells part of a business but keeps a meaningful stake. A senior executive holds low-basis stock that could appreciate sharply. A family office owns private investments that may have a liquidity event ahead. In each case, the same tension appears. The next phase of growth could create substantial family wealth, but transferring that growth outright can trigger gift tax exposure at the wrong time.

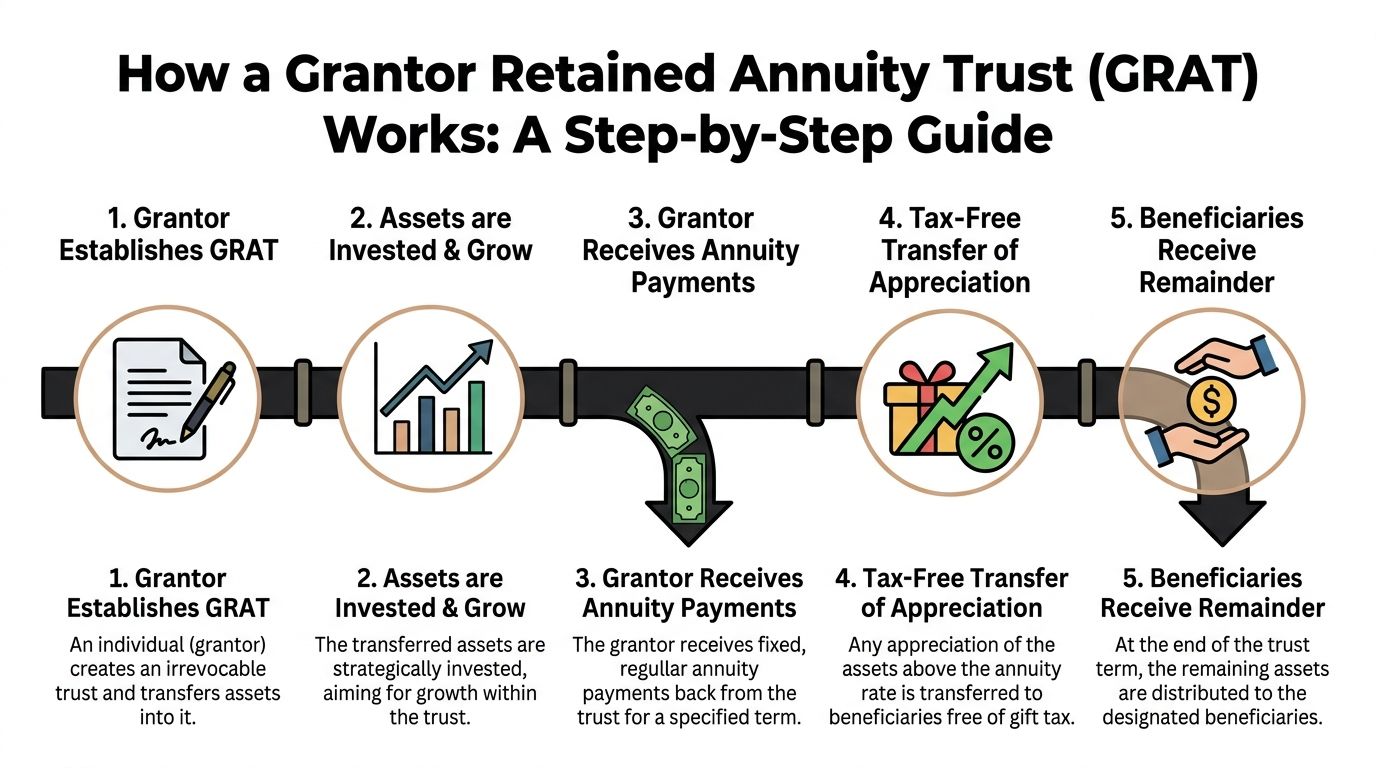

A Grantor Retained Annuity Trust, or GRAT, was established under Internal Revenue Code Section 2702 and is designed to address that problem. The grantor transfers assets into an irrevocable trust, keeps the right to receive fixed annuity payments for a set term, and lets any excess appreciation pass to beneficiaries with minimal or zero gift tax if the structure is drafted correctly.

The appeal is practical. A GRAT can “freeze” the current value for transfer tax purposes while shifting future upside to heirs. If the assets outperform the IRS hurdle rate, the excess can move outside the taxable estate. If they do not, the result is often less dramatic than many clients expect. In a poorly performing GRAT, the grantor typically receives the value back through annuity payments, and the strategy produces little or no remainder for heirs.

That feature is why seasoned planners often treat a GRAT less like a gamble and more like a targeted asset-transfer vehicle. The structure works best when there is a strong reason to believe appreciation may occur during a defined period, but there is hesitation about using exemption or making an outright transfer today.

A GRAT is usually most attractive when you want to transfer future appreciation, not when your main goal is to move assets out of your name as quickly as possible.

How a Grantor Retained Annuity Trust Works

The mechanics become easier once you view the GRAT as a controlled pipeline for appreciation. You place selected assets into the trust, the trust pays you an annuity for a set term, and whatever remains at the end goes to beneficiaries.

The basic flow

A GRAT has three core parties.

- Grantor. The person who creates and funds the trust.

- Trustee. The person or institution that administers the trust according to the trust agreement.

- Beneficiaries. The individuals who receive the remainder if assets are left at the end of the term.

The trust is irrevocable. Once the assets go in, the deal is set by the governing document.

What happens from start to finish

The lifecycle usually looks like this:

- Fund the trust with targeted assets. Public securities, concentrated positions, and business interests are common candidates when there is a credible case for appreciation.

- Set the annuity term. The trust agreement defines how long annuity payments run.

- Calculate the annuity. The annuity is fixed under the governing rules and is tied to the value contributed and the IRS rate in effect at funding.

- Make annuity payments back to the grantor. The trust pays the grantor during the term.

- Distribute the remainder. If assets in the trust grow beyond what is needed to satisfy the annuity stream, the remainder passes to beneficiaries.

A concrete example shows the economics clearly. If a grantor transfers $1,000,000 in assets to a four-year GRAT when the IRS Section 7520 rate is 4%, the trust pays annual annuity payments of $275,489. If the assets grow at 20% annually, $594,771 can remain for beneficiaries tax-free after all payments are made, according to Holland & Knight’s GRAT illustration.

Why the annuity matters so much

The annuity is not just a distribution feature. It is the reason the strategy can be so tax efficient.

The grantor is retaining a valuable interest in the trust. Because the grantor keeps that annuity right, the taxable value of what is considered gifted to the beneficiaries can be very small. In some structures, it is designed to be effectively zero at inception.

That is why many wealthy families use GRATs with assets they believe may appreciate sharply over a relatively short window. The annuity returns substantial value to the grantor. The excess appreciation, if it materializes, goes where the tax advantage is greatest.

Where GRATs tend to work operationally

In practice, administration is smoother when the asset can be valued and managed with discipline. Public securities are straightforward. Closely held business interests can work, but they require more coordination among valuation professionals, estate counsel, tax advisors, and the trustee.

The right GRAT asset is not merely an asset with upside. It is an asset with upside and a realistic path to valuation, administration, and annuity funding.

Understanding the Tax and Valuation Rules

A GRAT is won or lost on math, timing, and valuation discipline. High-net-worth families often focus first on upside. The IRS rules decide how much of that upside can move with little or no taxable gift.

The Section 7520 hurdle rate

The starting point is the Section 7520 rate. The IRS publishes it each month, and it is used to value the annuity the grantor retains. That valuation drives the size of the taxable gift at the moment the GRAT is funded.

In practical terms, the Section 7520 rate is the hurdle. If the assets in the trust outperform that assumed rate during the GRAT term, the excess appreciation can pass to the remainder beneficiaries with strong transfer-tax efficiency. If the assets only match it, or fall short, little or nothing is left at the end.

That is why timing matters. A GRAT is often more attractive when the hurdle rate is relatively low, but the better question is whether the asset has a realistic path to outpacing that hurdle over the selected term.

Why zeroing out the gift matters

Many GRATs are structured as zeroed-out GRATs. The annuity is calculated so the present value of what the grantor keeps is roughly equal to the value contributed to the trust. The result is a taxable gift that is nominal or near zero at inception.

For a client with volatile stock, pre-liquidity business equity, or concentrated options exposure, that structure changes the decision-making process. A large outright gift consumes exemption immediately. A zeroed-out GRAT lets the client test a thesis about future appreciation without making a large taxable transfer on day one.

The trade-off is clear. If the expected growth never arrives, the strategy may produce little transfer value after legal, valuation, and administrative work. If the asset appreciates sharply within the term, the GRAT can move that spread out of the estate very efficiently.

Valuation is where good GRATs hold up under scrutiny

Public securities are usually easier to fund into a GRAT because the opening value is easier to support and the annuity payments are easier to satisfy. Private company interests, carried interests, and nonpublic equity can be more attractive economically, but they require tighter execution.

That execution starts with the initial appraisal. A weak valuation can create problems on audit, distort the annuity calculation, and undermine the intended gift tax result. I generally view valuation work as part of the strategy, not a filing formality.

Several practical rules shape whether the GRAT is worth doing:

- Match the term to the expected catalyst. If the likely appreciation event is a financing round, liquidity event, or concentrated stock recovery, the GRAT term should fit that window.

- Use an asset that can support annuity payments. A great asset with no practical liquidity plan can force bad decisions later, including in-kind distributions at the wrong time.

- Coordinate valuation and drafting early. The annuity formula, funding date, and appraisal assumptions need to align.

- Be realistic about audit exposure. The more subjective the asset value, the more important the documentation.

These points matter most for clients using a GRAT with assets that are hard to price but capable of sharp appreciation. That is often where the best estate planning opportunity sits. It is also where sloppy execution causes the most damage.

The income tax burden stays with the grantor

A GRAT is generally structured as a grantor trust for income tax purposes, so the grantor pays the income tax on trust earnings. For many affluent families, that is a feature, not a defect. The tax is paid outside the trust, which allows more of the trust property to remain in place for the remainder beneficiaries.

That can improve the economics meaningfully over time, especially when the GRAT holds appreciating assets that do not need to be sold to cover the tax bill inside the trust.

The best GRAT candidates are not merely assets with upside. They are assets with upside, a defendable valuation, a clear annuity funding plan, and a realistic chance of beating the IRS hurdle within the selected term.

Strategic Use Cases for High-Net-Worth Clients

A client owns founder stock, expects a financing round or sale process within the next 12 to 24 months, and does not want to burn gift tax exemption on an outright transfer that may prove premature. That is often the point at which a GRAT moves from technical concept to serious strategy discussion.

A GRAT works best when three facts line up. The asset has credible upside. The current value is supportable. The client can tolerate the possibility that the strategy produces little or no transfer if performance disappoints. For high-net-worth families, the primary question is rarely whether a GRAT can work in theory. The better question is whether this asset, at this moment, justifies the term, complexity, and mortality risk.

Concentrated public stock

Concentrated stock is one of the cleanest GRAT candidates, especially when the family expects a recovery, a catalyst, or a period of above-market volatility. A sale may be unattractive because of capital gains, insider trading restrictions, optics, or simple conviction that the position still has room to run.

In that setting, a GRAT can separate current value from future appreciation. If the shares outperform the IRS hurdle rate during the trust term, that excess growth can pass to the remainder beneficiaries with little or no taxable gift.

Short-term rolling GRATs often appeal to clients in this category because they break one large timing call into a series of smaller ones. That structure does not eliminate risk, but it gives the family more chances to reset if rates change, the stock moves sharply, or concentration concerns become more urgent.

Pre-IPO and private company equity

In such cases, GRAT planning becomes highly strategic.

Founders, early employees, and senior executives often hold equity that may be worth far more after a financing, recapitalization, or liquidity event than it is on the funding date. A GRAT can be a strong fit when there is a defined inflection point ahead and the client wants to transfer that appreciation without making a large taxable gift today.

It can also be the wrong tool. If the timing of the event is unclear, if the valuation position is too aggressive, or if the company interest cannot realistically support the annuity stream, the plan can fail for practical reasons even if the tax theory is sound. I generally view a GRAT as most persuasive when the family has both upside visibility and enough liquidity planning to avoid forced moves later.

Business owners balancing transfer planning and control

Some owners want to start shifting value out of the estate but are not ready to hand over business interests outright. A GRAT can help because the grantor retains the annuity interest, which often makes the economics and family conversation easier than an immediate gift.

Still, the trust solves a narrow problem. It addresses appreciation transfer. It does not resolve voting control, buy-sell restrictions, distribution policy, or succession management. Families comparing a GRAT with different trusts used in estate planning should evaluate those governance issues separately, because they usually determine whether the broader plan holds together.

Clients with uneven income or concentrated career-related wealth

Athletes, entertainers, and senior executives often accumulate wealth in lumpy, highly concentrated forms. Equity compensation, profit interests, brand-related business stakes, and option exercises can create substantial upside, but not always stable liquidity.

A GRAT can fit when the objective is precise. Move appreciation from a concentrated asset while preserving a retained payment stream. It fits poorly when near-term cash demands are already tight or the asset is so unpredictable that annuity planning becomes speculative.

When rolling GRATs are the better decision

Some families prefer repetition over commitment to a single long-term structure. A rolling GRAT program can make sense for volatile holdings because each new trust reflects updated values, current rates, and the family’s revised outlook.

That flexibility has a cost. The family signs up for repeated execution, repeated administration, and repeated valuation work. For many wealthy clients, that trade-off is acceptable because the strategy matches how they already make investment decisions. They prefer several controlled entries over one long-duration bet.

The strongest GRAT cases usually involve a specific catalyst, a realistic valuation position, and an asset with enough upside to justify the work. The weakest cases start with the tax idea and try to force the asset to fit it.

Exploring Common GRAT Variations

A GRAT should be built around the asset and the decision in front of you. A founder heading toward a sale, an executive with concentrated stock, and a family holding illiquid private-company equity may all use a GRAT, but they should not use the same version.

Zeroed-out GRATs

The zeroed-out GRAT remains the starting point for many high-net-worth clients because it is designed to produce little or no taxable gift when funded. That preserves transfer-tax exemption for other planning moves while still giving the family a path to shift future appreciation if the asset performs well enough.

That design is attractive for clients who want a measured bet rather than a large upfront gift. If the asset outperforms the Section 7520 rate, the remainder can pass efficiently to heirs. If it does not, the economic result is often disappointing, but the transfer-tax cost at inception was limited.

Short-term versus long-term GRATs

Term selection is usually the primary strategic choice.

Short-term GRATs fit best when the family expects a specific catalyst. A financing round, liquidity event, option exercise, tender offer, or sharp dislocation in a public stock can justify a shorter window. They also reduce the exposure to mortality risk because the grantor has to survive the GRAT term for the transfer strategy to work as intended.

Long-term GRATs ask for a stronger conviction. They can work for assets with a longer growth runway, but they also lock the plan to a longer period of market risk, family risk, and policy risk. For many clients, that is too much uncertainty unless the asset has unusually strong appreciation potential and the cash flow demands are easy to model.

Standard annuity versus increasing annuity structures

Payment design matters more than many clients expect. A GRAT can use level annuity payments or increasing payments, subject to the governing rules, and that choice should reflect how the contributed asset is likely to behave over the term.

For an asset that may not produce liquidity early, an increasing annuity can be the better fit because it reduces pressure on the trust in the first years. That does not make it automatically better. It adds drafting complexity, increases the importance of clean projections, and can create less room for error if timing slips.

This is usually where planning shifts from theory to execution.

A family comparing GRAT designs should also keep in mind the broader trade-offs of irrevocable structures, including control, flexibility, and administrative burden. A good starting point is this review of irrevocable trust pros and cons.

Choosing the variation that fits

Families comparing a GRAT with other structures often benefit from understanding the broader menu of different trusts used in estate planning. The right choice depends on the asset, the timing, the client’s survival outlook, and whether the family is solving for appreciation transfer, liquidity retention, or both.

| GRAT variation | Main advantage | Main limitation | Best fit |

|---|---|---|---|

| Zeroed-out GRAT | Preserves exemption by minimizing the taxable gift at inception | Only the appreciation above the hurdle rate creates a meaningful transfer result | Clients who want upside transfer without using much exemption |

| Short-term GRAT | Better suited to volatile assets and event-driven timing | Less time for appreciation to compound | Concentrated stock, stock options, or business interests with a near-term catalyst |

| Long-term GRAT | Gives the asset a longer period to appreciate | Greater exposure to mortality, market shifts, and changing objectives | Assets with a longer expected growth cycle and stable planning assumptions |

| Increasing annuity GRAT | Better alignment with assets that may produce liquidity later | More complex modeling and administration | Illiquid or unevenly maturing assets |

The strongest variation is the one that matches the asset’s timing and the family’s tolerance for execution risk. That is why GRAT planning is less about picking a template and more about making the right call on when to act, how long to commit, and which asset deserves the slot.

Weighing the Pros Cons and Critical Risks

A client contributes pre-IPO shares or a concentrated stock position to a GRAT because the upside case looks strong over the next 12 to 24 months. If the timing is right, the transfer can work extremely well. If the asset stalls, the term runs too long, or the client dies during the annuity period, the result can range from disappointing to counterproductive.

The practical advantage of a GRAT is precision. It can transfer future appreciation with little or no taxable gift at inception, while the grantor keeps a defined annuity stream. That combination makes sense for high-net-worth families who expect meaningful upside but do not want to commit large exemption amounts to an outright gift.

The trade-off is just as important. A GRAT is narrow by design. It works best when the asset has a credible path to outperform the IRS Section 7520 rate, the valuation is supportable, and the timing of that appreciation is reasonably identifiable. That is why GRATs often fit volatile business interests, concentrated equity, or stock options better than stable, low-return holdings.

Where the benefits are real

A well-structured GRAT can solve a specific problem. It shifts appreciation above the hurdle rate to heirs, gives the grantor scheduled annuity payments, and in a zeroed-out design preserves exemption for other planning opportunities.

For the right client, that is powerful.

It is especially useful when the family wants upside transfer without making a large current gift, or when there is a near-term catalyst such as a liquidity event, recapitalization, financing round, or expected stock rebound. In those cases, the question is rarely whether the GRAT is technically available. The key question is whether this asset, this term, and this family’s risk tolerance line up.

The risks that matter in practice

Performance risk comes first. If the trust assets do not beat the Section 7520 rate, little or nothing passes to beneficiaries. The structure may still return value to the grantor through the annuity, but the planning work, legal expense, and valuation effort did not produce the intended wealth transfer.

Mortality risk is just as important. If the grantor dies during the GRAT term, some or all of the trust assets may be included in the estate under IRC Section 2036. Term selection is not a drafting detail. It is a judgment call that has to reflect the client’s age, health, and tolerance for a failed transfer result.

Legislative risk also belongs in the analysis. GRATs have been the subject of repeated policy proposals, including proposals that would require longer minimum terms and a taxable gift at formation, as noted earlier in Gainbridge’s review of GRAT mechanics, hurdle rates, and proposed changes. A family should implement a GRAT because the current rules support the strategy now, not because they assume those rules will remain unchanged.

Where clients make the wrong call

The most common mistake is using a GRAT because it sounds efficient in the abstract.

Asset selection drives the outcome. A low-volatility fixed income portfolio usually does not justify the effort. An illiquid asset with a weak valuation story can create administrative strain and audit exposure. A business interest that may appreciate substantially after a defined catalyst is a different case entirely.

I also see clients focus too heavily on the upside case and too lightly on execution. Can the annuity be paid on schedule without forcing a bad sale? Is the valuation defensible? Is the term short enough to manage mortality risk but long enough to capture the expected appreciation cycle? Those are the questions that separate a strong GRAT from a disappointing one.

Clients weighing broader irrevocable trust pros and cons should keep one point in view. Once the GRAT is signed and funded, flexibility narrows. That is manageable when the asset and timing are well chosen. It is expensive when they are not.

How GRATs Compare to Other Wealth Transfer Vehicles

A GRAT is not the universal answer. It is one of several ways to move wealth efficiently, and it tends to shine in a narrow set of facts.

The broad backdrop matters. The federal estate tax exemption is expected to be cut in half in 2026, and GRATs are drawing attention because they can be structured to avoid using the Generation-Skipping Transfer Tax exemption, according to National Advisors’ GRAT Q&A on the projected 2026 exemption change.

The practical comparison

An outright gift is straightforward. You transfer the asset and the future appreciation is no longer yours. The downside is equally clear. You use exemption immediately and give up control over the transferred value.

A GRAT is more surgical. It is designed for clients who want to transfer upside while retaining an annuity stream and minimizing current gift value.

A sale to an intentionally defective grantor trust can be more powerful in the right case, especially for clients willing to accept more complexity and different planning trade-offs. Families comparing the two often benefit from understanding the mechanics of an intentionally defective grantor trust before deciding which tool better fits the objective.

A charitable lead annuity trust belongs in a different bucket. It is relevant when philanthropy is part of the transfer plan, not when tax efficiency is the main goal.

GRAT vs Other Estate Planning Tools

| Strategy | Primary Benefit | Key Risk | Best For |

|---|---|---|---|

| GRAT | Transfers appreciation with minimal or zero taxable gift if structured properly | Asset underperformance and grantor death during term | Volatile or high-upside assets where the grantor wants annuity payments |

| Outright gift | Simplicity | Immediate use of exemption and loss of retained economics | Families comfortable making a direct transfer now |

| Sale to IDGT | Can shift significant future value with flexible planning design | Greater complexity and execution risk | Larger estates with advanced planning teams |

| CLAT | Combines transfer planning with charitable intent | Best only when charitable goals are genuine | Philanthropic families |

The best planning tool is the one that matches the family’s real objective. If the goal is to move future appreciation from a specific asset while keeping the current value economically close, the grantor retained annuity trust often deserves serious consideration.

Determining Your Next Steps in Estate Planning

A grantor retained annuity trust is most effective when it is used with precision. The right client has the right asset, the right timing window, and a clear reason to transfer future appreciation rather than present value. The wrong client has a vague objective, uncertain liquidity, or an asset that does not justify the complexity.

Execution matters as much as design. The annuity calculation, valuation support, trust drafting, and administrative follow-through all need to line up. Even document management can become a bottleneck when advisors, attorneys, valuation professionals, and trustees are all working from different timelines. For firms building that support infrastructure, resources on Paralegal Assistants can be useful when legal teams need added administrative capacity around trust preparation and workflow.

Most families should not decide on a GRAT in isolation. They should evaluate it alongside gifting, trust sales, charitable structures, liquidity planning, and the family’s broader estate goals. A GRAT can be excellent. It can also be the wrong tool for a client who needs simplicity more than financial optimization.

Commons Capital works with high-net-worth individuals, families, business owners, and clients in sports and entertainment to evaluate complex strategies like GRATs in the context of the full balance sheet. If you want help deciding whether a grantor retained annuity trust fits your estate plan, connect with Commons Capital.