A Crummey trust is a clever estate planning tool that allows you to pass significant wealth to your beneficiaries, such as children or grandchildren, while minimizing or avoiding federal gift taxes. The core of what a Crummey trust is revolves around a smart legal feature that transforms what would normally be a future, taxable gift into a present gift that qualifies for the annual gift tax exclusion.

The magic happens by giving your beneficiaries a brief, temporary window to withdraw any money you contribute to the trust. This simple right of withdrawal is the key to its powerful tax advantages.

Turning Future Gifts Into Tax-Free Transfers Today

At its heart, a Crummey trust is a gateway for moving wealth efficiently. Normally, if you just put money into an irrevocable trust for someone, the IRS sees it as a “future interest” gift. Why? Because the beneficiary can’t get their hands on it right away. Gifts like that don’t qualify for the annual gift tax exclusion.

This is where the Crummey trust flips the script. It has a special feature: a temporary right to withdraw. Every time you contribute cash, the beneficiaries get a notice and a brief period—usually 30 to 60 days—to take out their share.

This immediate, though fleeting, right of access is what legally transforms your contribution into a “present interest” gift in the eyes of the IRS. Problem solved.

Where Did That Strange Name Come From?

The trust gets its unusual name from a groundbreaking 1968 tax court case involving a man named Clifford Crummey. He took on the IRS and won, successfully arguing that gifts to his irrevocable trust should qualify for the annual gift tax exclusion because his beneficiaries had a real, unrestricted (though temporary) right to the money.

That ruling fundamentally changed the game for high-net-worth families, creating a reliable way to structure their estate plans. This legal maneuver is the very foundation of what a Crummey trust is and why it remains so effective today.

The genius of the Crummey trust lies in a simple, yet powerful, legal fiction. By granting a temporary withdrawal power, it satisfies IRS requirements for tax-free gifting without you having to give up long-term control over how the assets are managed and eventually distributed.

To get a clearer picture of how these pieces fit together, let's break down the key players and terms you’ll encounter.

Key Roles and Concepts in a Crummey Trust

This table outlines the essential components and participants in a Crummey trust, giving you a quick reference for understanding how it all works.

Understanding these roles is the first step. Once everyone is in place and the rules are set, the real power of the strategy becomes clear.

Why Is This Strategy So Important?

For families looking to pass on significant wealth without writing a huge check to the IRS, this strategy is a cornerstone of modern estate planning. It allows you to:

- Maximize Your Annual Gifting: You can make gifts up to the annual exclusion limit to as many people as you want, every single year. A married couple with three children could potentially transfer over $100,000 annually, completely free of gift tax.

- Protect Family Assets: Once money is inside an irrevocable trust, it's generally shielded from the beneficiaries' future creditors, messy divorces, or just plain bad financial decisions. You can get more clarity on your personal situation by exploring if you need a trust for your specific goals.

- Control How the Money Is Used: As the grantor, you set the terms. You can decide when and how the bulk of the trust funds are distributed—for instance, when a child reaches a certain age, for educational expenses, or to help with the down payment on a first home.

How a Crummey Trust Actually Works

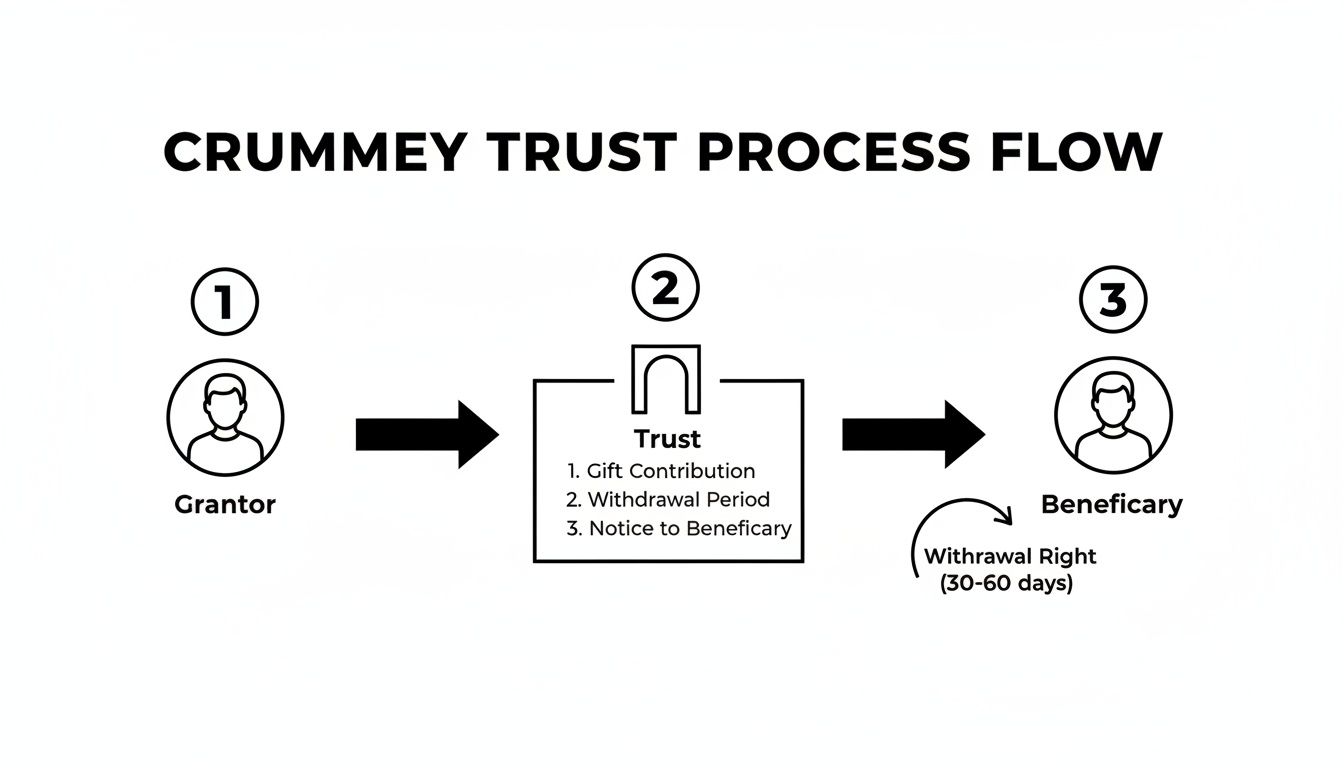

To really get your head around what a Crummey trust is, you need to see it in motion. Setting one up isn't a one-and-done deal; it's a living, breathing process that demands attention every single year. Miss a step, and you could lose its powerful tax advantages.

It all starts when the grantor—the person setting up the trust—decides to put money into it. They'll make a contribution, usually cash, aiming to use their annual gift tax exclusion. That simple transfer is what kicks the whole machine into gear.

The All-Important Crummey Notice

Once the trust has the money, the trustee's most critical job begins. They have to immediately send out a formal, written notification to every single beneficiary. This document is known as a Crummey Notice or Crummey Letter, and it’s the legal linchpin of the whole strategy.

This isn't just a friendly heads-up; it's a non-negotiable legal requirement. The notice tells each beneficiary that a gift has been made for them, the exact amount they can take out, and—this is crucial—the deadline for doing so. Typically, they get 30 to 60 days to make a decision.

This flowchart maps out the standard journey of funds and notifications.

As you can see, it’s a clear sequence: grantor to trust to beneficiary. That temporary window to withdraw the cash is the clever mechanism that makes the gift eligible for the tax exclusion.

That right to withdraw has to be real. It must be absolute and legally enforceable. Even if there's a quiet family understanding that nobody will actually take the money, the power to do so has to be genuine. If the IRS suspects it's a sham, they can—and will—disallow the gift tax exclusion, which torpedoes the trust's main purpose.

The Withdrawal Right and Why It Lapses

During that 30- or 60-day window, the beneficiary has total control over their share of the gift. They can demand the funds, and the trustee is legally bound to hand them over. But in the real world, beneficiaries almost never exercise this right. Why? Because doing so would likely mean the grantor stops making future gifts.

When the window closes, the beneficiary's right to withdraw simply lapses, or expires. The money then officially stays put, locked inside the trust to be managed according to the rules you, the grantor, laid out. This could mean investing it for long-term growth, paying for college tuition, or just holding it until the beneficiary hits a certain age.

The temporary withdrawal right is the legal magic that transforms a "future interest" gift (which is generally taxable) into a "present interest" gift (which qualifies for the annual exclusion). The IRS goes along with this because the beneficiary had a real, immediate chance to get their hands on the cash.

But that lapse—the act of not taking the money—creates another potential tax wrinkle, this time for the beneficiary.

The "5 and 5 Power": A Built-In Safeguard

Here's a tricky concept: when a beneficiary lets their withdrawal right lapse, the IRS could interpret that as them making a gift back to the other beneficiaries in the trust. This could create a gift tax headache for them.

To sidestep this problem, most Crummey trusts are drafted with a special provision known as the "5 and 5 Power."

This rule, straight from the Internal Revenue Code, says that a lapsed withdrawal right isn't considered a taxable gift as long as the amount is the greater of:

- $5,000, or

- 5% of the total value of the trust's assets.

By capping the withdrawal right at an amount that fits inside this "5 and 5" window, the trust protects the beneficiaries from facing their own gift tax issues. It’s a small but critical detail that keeps the entire process clean and tax-efficient, year after year. It's what makes the whole structure hang together from a tax law perspective.

Maximizing Your Annual Gift Tax Exclusion

This is where a Crummey trust really starts to shine: it’s built to wring every drop of value out of the annual gift tax exclusion. We're not talking about a minor tax loophole here. This is a foundational strategy for methodically moving significant wealth out of your taxable estate over many years, all without touching your much larger lifetime gift tax exemption. It turns a simple yearly gift into a powerful wealth-transfer engine.

The mechanics are straightforward but potent. Grantors can make contributions that benefit multiple people at once, multiplying the tax-free amount they can shift out of their estate each year. The more beneficiaries you have, the bigger the opportunity for tax-efficient gifting.

The Power of Multiplication in Action

Let’s run the numbers for a high-net-worth family to see how this plays out in the real world. Meet David and Sarah, a married couple looking to provide for their two children and three young grandchildren.

If they just handed over cash, the kids and grandkids would have immediate control, which might not be what David and Sarah intend. But by using a Crummey trust, they can make gifts that qualify for the annual exclusion while a trustee manages the assets for the long haul.

Here’s a quick look at their annual gifting capacity:

- Number of Donors: 2 (David and Sarah)

- Number of Beneficiaries: 5 (2 children + 3 grandchildren)

- Annual Gift Tax Exclusion: $18,000 per person (for 2025)

By channeling their gifts through the trust, the math gets impressive fast:

2 Donors × 5 Beneficiaries × $18,000 = $180,000 per year

Just like that, David and Sarah can move $180,000 out of their taxable estate every single year. They don't have to file a single gift tax return or use a penny of their lifetime exemption. Stick with that plan for a decade, and they've transferred $1.8 million completely tax-free—and that’s before counting any investment growth inside the trust.

A Growing Opportunity for Estate Planning

What makes this strategy even better over the long term is that the annual exclusion amount isn't set in stone. The IRS periodically adjusts it for inflation.

Think about it: the exclusion is $18,000 per person in 2025, but it was just $14,000 back in 2015. This steady climb gives your Crummey trust more and more firepower over time. This slow-and-steady approach is exactly what a Crummey trust is designed for. It allows families to chip away at a future estate tax bill while making sure their heirs don’t get the money before they’re ready for it. To round out your planning, it's also wise to look at broader strategies to minimize Inheritance Tax for UK families, which can offer a more global perspective on wealth preservation.

Ultimately, the goal is to turn a simple annual tax rule into a multi-generational wealth strategy. By compounding these tax-free gifts year after year, families can build a lasting legacy that's shielded from unnecessary taxes and the risks of giving too much, too soon.

When you're looking to really maximize your estate protection, a powerful combination is pairing a Crummey trust with an Irrevocable Life Insurance Trust, or ILIT. Think of it as a one-two punch for your legacy planning. This approach lets you turn those annual, tax-free gifts into a substantial, tax-free death benefit for your heirs, giving them crucial liquidity right when they need it most.

It's a sophisticated but elegant way to build and protect wealth for the next generation.

Here’s the basic idea: you create an ILIT, which then goes out and buys a large life insurance policy on you. Every year, you make gifts into the ILIT to cover the policy’s premiums. By building Crummey withdrawal powers into the trust, those gifts become eligible for the annual gift tax exclusion, which means you can fund a massive policy without ever touching your lifetime exemption.

The Twofold Tax Benefit

This is where the magic really happens. The synergy between these two tools creates a remarkable double-barreled tax advantage.

First, the money you put in for premiums is completely shielded from gift taxes because of those Crummey withdrawal rights you gave the beneficiaries. Second, the ILIT owns the policy—not you. That simple fact means the entire death benefit is paid out to your heirs completely free of federal estate tax.

You're effectively taking a massive asset completely off your taxable estate's balance sheet, while ensuring your family gets the full, unreduced value of the policy. For anyone with a significant net worth, this can literally translate into millions of dollars in tax savings.

One of the most effective applications for a Crummey trust is funding an irrevocable life insurance trust (ILIT). This allows high-net-worth families to cover policy premiums using tax-free gifts while ensuring the massive death benefit is excluded from their taxable estate. Data from wealth management firms suggests that 65% of family offices with clients having over $500k in investable assets deploy Crummey ILITs, particularly for volatile earners like those in the entertainment industry who face career-ending risks.

To get this strategy off the ground, a crucial first step is to compare various whole life insurance policies, since they are often used within ILITs for their guarantees and predictable growth.

A Real-World Scenario: Providing Liquidity

Let's walk through an example to see how this plays out in the real world.

Meet Maria, a successful entrepreneur who built a thriving tech company from scratch. Her business is valued at a hefty $25 million, but it's an illiquid asset—you can't just slice off a piece to pay the bills.

Maria is worried that when she dies, her kids will get hit with a massive estate tax bill. Without enough cash on hand, they could be forced into a fire sale of the family business just to pay the IRS. It's a common nightmare for owners of family companies, large real estate portfolios, or valuable art collections.

To head off this problem, Maria and her advisors set up a Crummey ILIT.

- The Goal: Make sure her estate has enough cash (liquidity) to cover taxes without having to sell the company.

- The Plan: The ILIT purchases a $10 million life insurance policy on Maria's life.

- The Funding: Each year, Maria gifts $90,000 to the trust to pay the premium. She names her five children and grandchildren as beneficiaries with Crummey withdrawal powers, keeping the entire gift under her available annual exclusions.

When Maria passes away, the ILIT receives the $10 million death benefit—100% tax-free. The trustee can then use that cash to buy assets from her estate, like a portion of the company stock, or simply lend the estate the money it needs. This injection of cash allows the estate to pay all its taxes and administrative costs without a problem.

The result is a seamless transition. The business stays in the family, just as she always wanted. This is a perfect illustration of how you can minimize estate taxes through careful planning. The Crummey ILIT didn’t just save the family a fortune in taxes; it preserved her life's work for the next generation.

The Good, The Bad, and The Paperwork

A Crummey trust can be an incredibly effective tool in your estate planning arsenal, letting you pass significant wealth to the next generation with impressive tax efficiency. But like any sophisticated financial strategy, it's not a simple "set it and forget it" solution. You've got to weigh the powerful benefits against some very real risks and administrative headaches.

The biggest draw—and the whole reason these trusts were invented—is the tax savings. By using the annual gift tax exclusion, you can methodically transfer chunks of your wealth out of your taxable estate, year after year. This lets you save your much larger lifetime exemption for other, bigger transfers. Over time, this consistent, disciplined approach can add up to a mountain of tax savings.

The Upside: Control and Protection

Beyond the tax angle, a Crummey trust offers a couple of major advantages that you just don't get with straightforward cash gifts.

First, you, as the grantor, stay in the driver's seat. You write the rules for the trust, spelling out exactly when and how your beneficiaries can tap into the money. This is a game-changer if you're gifting to young adults or beneficiaries who might not be ready to handle a large sum. You can ensure the money goes toward meaningful goals—a down payment on a house, college tuition, or seed money for a business—instead of being squandered.

Second, the assets tucked inside an irrevocable trust are typically shielded from a beneficiary's financial troubles. We're talking about protection from future creditors, messy divorces, or lawsuits. It's a layer of security that helps guarantee the wealth you're passing down actually serves its intended purpose. If you want to go deeper on this, we've got a full breakdown of the pros and cons of irrevocable trusts right here.

The Downside: Red Tape and Real Risks

Now for the flip side. The biggest hurdle is the strict, non-negotiable requirement to issue Crummey notices every single year. This isn't just a suggestion; it's a legal must-do. Every time you contribute money, the trustee has to send a formal, written notice to each beneficiary, letting them know they have a temporary window to withdraw the funds.

Dropping the ball here can have serious consequences. Even with a massive $13.6 million lifetime gift and estate tax exemption, the $18,000 annual exclusion that a Crummey trust leverages is still a key strategy for unlimited tax-free gifting. Yet, IRS audits have shown that failing to follow the notice rules can get the trust's tax benefits thrown out in as many as 25% of audited cases, according to insights from GBQ.com on the continued relevance of Crummey trusts.

The most overlooked risk is complacency. A "set it and forget it" mindset is the enemy of a successful Crummey trust. Diligent administration, particularly the annual issuance of Crummey notices, is the bedrock of its tax-advantaged status.

There's also the small but real risk that a beneficiary might actually take the money and run. That withdrawal power has to be legitimate for the trust to work. If a beneficiary decides they want their share, the trustee has no choice but to hand it over. This really highlights how important it is to have open communication and a strong foundation of trust with your beneficiaries.

Finally, choosing the right trustee is absolutely critical. This isn't a job for just anyone. Your trustee needs to be responsible, meticulous, and completely on top of their legal duties. A careless trustee can easily sink the entire strategy with simple paperwork errors, leading to a world of tax problems and legal headaches you were trying to avoid in the first place.

So, Is a Crummey Trust Right for You?

Deciding if a Crummey trust makes sense for your family comes down to a hard look at your finances and what you want for the future. This isn't a one-size-fits-all solution. But for the right family, it’s an incredibly powerful tool for passing wealth to the next generation while keeping the tax man at bay.

So, who is the ideal candidate?

Typically, we see this strategy work wonders for high-net-worth individuals who want to steadily chip away at their taxable estate. If you’re looking to make significant annual gifts to your kids or grandkids but hesitate to just hand them a big check, this structure is your answer. It's a way to move wealth out of your name efficiently, but without completely giving up the reins.

It All Comes Down to Control

The real magic here is control. A Crummey trust lets you call the shots. You can set the rules for how and when the money is used—think education, a down payment on a first home, or other major life milestones—instead of worrying it might get spent unwisely. This makes it perfect for younger beneficiaries who aren't quite ready for that level of financial responsibility.

Ask yourself a few key questions:

- Is your main goal to transfer wealth over many years in the most tax-efficient way possible?

- Do you need to shield those assets from a beneficiary's potential creditors or even a messy divorce down the road?

- Is it critical for you to have a say in when and why distributions are made?

If you're nodding your head "yes," then a Crummey trust is probably a great fit. On the other hand, if your estate is comfortably below the federal exemption limit and you're fine with making direct gifts, a simpler path might be better. Outright gifts are far less complicated and don't come with the administrative upkeep a trust requires.

Think of a Crummey trust as a strategic vehicle for anyone who values both tax efficiency and long-term control. It’s for people who want to give generously, but also wisely, ensuring their legacy actually helps future generations the way they intended.

Your Next Steps

Let's be clear: setting up a Crummey trust is not a weekend DIY project. The complexity of how these trusts are drafted and managed demands professional expertise. Your first move should be to get the right team in your corner to map out a strategy for your unique situation.

This team should include:

- An Estate Planning Attorney: They will be the architect, drafting a legally solid trust document that reflects your family’s specific needs and dynamics.

- A Certified Public Accountant (CPA): This is your tax guru, who will handle the gift tax implications and make sure all the reporting is done correctly.

- A Wealth Advisor: They’ll help you see the big picture, making sure the trust works in harmony with your broader financial plan and investment goals.

With their combined guidance, you can build a trust that truly fits your life and lets you move forward with confidence.

Common Questions About Crummey Trusts

Estate planning gets complicated fast, and Crummey trusts are no exception. Let's tackle some of the most frequent questions that come up when clients are weighing this strategy.

What If a Beneficiary Actually Takes the Money?

This is the big "what if" that worries many people. If a beneficiary decides to exercise their right and withdraw the gift, the trustee is legally bound to hand over the cash, up to the annual gift amount.

It almost never happens. Why? Because beneficiaries usually understand that taking the money is a surefire way to convince the grantor not to make any more gifts to the trust. But the right to withdraw has to be real and legally enforceable—if it's not, the whole tax strategy falls apart. A well-written trust document will spell out exactly how to handle a withdrawal request, which highlights just how important it is for everyone involved to be on the same page.

Can You Put More Than Just Cash in a Crummey Trust?

Absolutely. While cash is the most straightforward asset to use—especially when the trust's main job is to pay life insurance premiums for an ILIT—a Crummey trust is surprisingly flexible. You can structure it to hold a variety of assets.

These could include things like:

- Stocks and bonds

- Real estate

- Shares in a family business

But be warned: using non-cash assets makes things more complex. You'll need a formal appraisal to determine the gift's value for tax purposes, and the trustee will need a higher level of expertise to manage those assets properly.

Do I Have to Set Up a New Trust Every Year?

Thankfully, no. A Crummey trust is an irrevocable trust you establish just once. Think of it as a permanent vehicle for your gifting strategy.

Once it's created, you make your annual contributions to that same trust. The crucial part that does happen every year is the administrative work. For every single contribution, the trustee must send out fresh Crummey notices to the beneficiaries. This is non-negotiable; it's what ensures each gift qualifies for the annual gift tax exclusion.

A lot of people think this is a "set it and forget it" tool. The reality is, a Crummey trust's success depends on diligent, year-after-year administration. Timely and legally sound withdrawal notices are everything.

This ongoing management is the lynchpin. If you get sloppy and skip these formal steps, even just once, you could undo all the tax benefits you worked so hard to put in place. It's why choosing a responsible, detail-oriented trustee is one of the most critical decisions you'll make in this entire process.

At Commons Capital, we specialize in creating financial strategies that protect and grow your wealth for generations to come. If you're exploring whether a Crummey trust is the right fit for your family, our team is here to provide the expert guidance you need. Learn more about our private wealth management services by visiting us at https://www.commonsllc.com.