Finding a local wealth advisor isn't just about managing money; it's about finding a strategic partner to quarterback the financial life of high-net-worth individuals and families. A local wealth advisor steps in to coordinate every single part of a complex financial picture, from investment management to your family's long-term legacy goals, all within the context of your community.

While a typical financial advisor might focus on your 401(k) or IRA, a true wealth advisor is orchestrating a much bigger game plan. They’re integrating everything—investment management, tax planning, estate structuring, and philanthropic goals—into one cohesive strategy. This guide will walk you through how to find the right wealth advisor near you.

What Does a Wealth Advisor Actually Do?

It’s easy to get the terminology mixed up. People often confuse a wealth advisor with a stockbroker or a general financial planner, but the roles are fundamentally different. A stockbroker is there to execute trades. A financial planner might help you map out a basic retirement savings plan.

A wealth advisor, on the other hand, takes a 30,000-foot view of your entire financial world.

Think of them as the chief financial officer (CFO) for your family. A corporate CFO doesn't just watch the company’s bank account. They’re deep in the weeds on investments, tax strategy, risk management, and long-term capital planning. Your wealth advisor does the exact same thing, making sure every moving part of your personal wealth works in perfect harmony.

The Quarterback Analogy

Picture a quarterback standing on the field. He doesn't personally block, tackle, or kick the ball. His job is to see the whole field, know the strengths of every player, read the opposing team’s strategy, and call the play that brings everyone together to score.

That's precisely what a high-caliber wealth advisor does for your finances. They don't replace your CPA or your estate planning attorney—they direct them. They make sure your tax strategy aligns perfectly with your investment decisions and that your legal structures are actually built to support your family's legacy.

Without that quarterback, you get financial silos. And that's dangerous. A brilliant investment that triggers a massive, unexpected tax bill isn't a net win.

We are on the cusp of the "Great Wealth Transfer," with an estimated $84 trillion expected to be passed down through inheritances over the next two decades. A wealth advisor's oversight is absolutely critical to navigating this shift, ensuring assets are transferred efficiently and in a way that reflects your family's core values.

Who Needs This Level of Service?

Look, anyone can benefit from solid financial advice. But the all-encompassing services of a wealth advisor are really built for people whose financial lives have outgrown a simple retirement plan. Their expertise becomes essential when you're juggling challenges that go far beyond just saving for the future.

This usually includes people like:

- Business Owners: Figuring out succession planning, managing the windfall from a business sale, or untangling personal and corporate finances.

- Athletes and Entertainers: Handling huge, irregular paychecks, managing sudden wealth, and planning for careers with much shorter earning windows.

- High-Net-Worth Families: Tackling multi-generational wealth transfer, pursuing philanthropic goals, and navigating complex estate tax minefields.

- Executives: Dealing with concentrated stock positions, executive compensation packages, and sophisticated tax-minimization strategies.

For these folks, wealth isn't just a number in an account. It's a living, breathing thing with serious legal, tax, and personal implications. A skilled wealth advisor brings the strategic oversight needed to manage that complexity. To get a sense of how roles can differ across the pond, you might find it interesting to see what a UK Independent Financial Advisor does.

Decoding Financial Titles: Who Can You Trust?

Walking into the world of finance can feel like you've stumbled into a bowl of alphabet soup. You’re hit with a barrage of acronyms and titles, and it’s not always clear who does what. But here’s the thing: not all advisors are the same, and knowing the difference is the first—and most important—step in finding someone you can actually trust with your money.

People often throw around terms like "financial advisor" and "wealth advisor" as if they mean the same thing. They don't. The distinctions can signal huge differences in expertise, services, and, most critically, their legal duty to you.

Let's start with "financial advisor"—it’s really a catch-all phrase. Anyone from the person selling you an insurance policy to a stockbroker placing trades can use this title. Many are great at what they do, but the title itself doesn't come with any specific training requirements or a guaranteed standard of care. Some work under a suitability standard, which simply means their recommendations have to be suitable for you, but not necessarily what's in your absolute best interest.

That might seem like a subtle difference, but it has massive implications for your portfolio. For instance, a "suitable" investment could be a mutual fund that pays the advisor a hefty commission, even when a lower-cost fund with similar performance is available. It ticks the box for suitability, but it’s definitely not the best choice for your bottom line.

The Fiduciary Gold Standard: CERTIFIED FINANCIAL PLANNER™

This is where you see a major step up. To earn the CERTIFIED FINANCIAL PLANNER™ (CFP®) designation, an advisor has to jump through some serious hoops—we’re talking rigorous coursework, a monster of an exam, years of experience, and signing on to a strict code of ethics.

The most important part? CFP® professionals are legally bound to a fiduciary standard. This is a game-changer. It means they have a legal and ethical obligation to always act in your best interest, period.

A fiduciary duty isn't just a suggestion; it's a legal requirement. It means your advisor must put your financial well-being first, even if a different decision would make them more money. This is the absolute foundation of a trusting client-advisor relationship.

When you work with a fiduciary, the entire dynamic shifts. You can be confident that the advice you're getting is built around your goals, not theirs. It provides a layer of protection and peace of mind you just don't get otherwise.

So, What Is a True Wealth Advisor?

This brings us to the wealth advisor. While the best wealth advisors are also fiduciaries and often hold a CFP® designation, their role is much broader than traditional financial planning. They’re specialists who handle the complex, intertwined financial lives of high-net-worth individuals and families—typically those with $500,000 or more to invest.

A wealth advisor takes a 30,000-foot view. They’re not just looking at one piece of the puzzle; they're looking at how all the pieces fit together to solve problems most people never have to think about.

Key Distinctions of a Wealth Advisor:

- Integrated Strategy: They aren't just picking stocks. They're on the phone with your CPA to coordinate tax-loss harvesting and working with your attorney to structure a multi-generational estate plan.

- Complex Problem-Solving: Their world involves planning for huge events, like the sale of a business, managing a large block of company stock, or setting up a charitable foundation.

- Access to Specialized Investments: They can often open doors to alternative investments, like private equity or real estate deals, that aren't available on the public market, helping you build a truly diversified portfolio.

Think of it like this: a financial advisor might help you pick the right funds for your IRA. A wealth advisor helps you structure a trust to pay for your grandkids’ college tuition in the most tax-efficient way possible, all while planning for the eventual sale of your company. They’re the quarterback for your entire financial life, not just a player on the field.

To help clear up the confusion, here’s a quick rundown of how these roles typically stack up.

Financial Professional Designations at a Glance

This table breaks down the key differences between the most common titles you'll encounter.

Ultimately, knowing these distinctions helps you ask the right questions and find an advisor whose qualifications and legal obligations align with your needs.

Core Services Your Portfolio Demands

When you're just starting out, financial advice usually centers on a pretty standard playbook: save for retirement and build a basic investment plan. But as your net worth grows, so does the complexity. Suddenly, that simple playbook doesn't cut it anymore.

This is where a true wealth advisor steps in. They're not just playing the same game on a bigger field; they're playing an entirely different sport. Their job is to deliver sophisticated, specialized strategies designed to protect and grow serious capital. Think of it less as a simple map and more as having a seasoned guide for a trek through the Himalayas.

Integrated Investment Management

For high-net-worth families, investing is rarely as simple as a 60/40 mix of stocks and bonds. A wealth advisor’s real value is in building a strategy that weaves together both public and private markets, creating a portfolio that’s far more resilient and diversified.

It’s not just about picking stocks. It’s about understanding how a private equity stake in a new tech company complements your municipal bonds and international holdings. The goal is to manage risk from every angle while uncovering growth opportunities the average investor never sees.

- Public Markets: This goes beyond simple buy-and-hold. It involves strategic management of stocks and bonds, with a sharp focus on tax-efficient vehicles.

- Private Markets: Gaining access to alternative investments like private equity, venture capital, and direct real estate deals can offer returns that don't move in lockstep with the stock market.

- Risk Management: When you have a concentrated stock position from a business sale or IPO, you need sophisticated hedging strategies to protect your wealth from market volatility.

This holistic approach means every investment decision is made with your complete financial picture in full view.

Proactive Tax Coordination

Taxes are one of the biggest—and most silent—drags on long-term wealth. A wealth advisor doesn't just help you file your returns in April; they work hand-in-glove with your CPA all year long to actively minimize what you owe. This is a critical service that sets them apart.

Imagine you’re about to sell a large block of company stock. Without proper planning, you could be handing a huge chunk of your proceeds straight to the IRS. A wealth advisor sees that event on the horizon and puts strategies in place before it happens.

It’s been shown that advisors can add what’s called an "advisor's alpha" through smart tax moves like asset location and tax-loss harvesting. For high-income earners with complex investments, this value-add can be massive.

Your advisor becomes the quarterback, ensuring your investment team and your tax professionals are all running plays from the same playbook. No more costly surprises, just a clear path toward maximizing your after-tax returns.

Sophisticated Estate and Legacy Planning

What happens to everything you’ve built when you’re no longer here? Answering this question is one of the most important things a wealth advisor does. Their role is to translate your values and goals into a durable plan that protects your family for generations.

This is worlds away from just drafting a will. It involves structuring complex trusts, planning for charitable giving, and making sure your assets transfer seamlessly with the smallest possible tax hit. A huge piece of this puzzle involves comprehensive estate planning and probate law, making sure every detail is legally airtight.

For instance, they might help you set up a generation-skipping trust. This is a powerful tool that allows you to pass assets to your grandchildren while potentially bypassing a round of estate taxes, keeping more of your wealth in the family.

Liquidity Event and Family Office Services

For many of our clients, a huge portion of their wealth is tied to a single event—the sale of a business, a company IPO, or even a pro athlete’s signing bonus. A wealth advisor specializes in planning for these make-or-break moments.

Turning a one-time windfall into lasting, generational wealth requires a plan. Your advisor helps structure the deal, manage the enormous tax implications, and design a long-term investment strategy for the proceeds of these liquidity events.

For families with truly substantial assets, an advisor might help establish or manage a family office. This is essentially your family’s own private wealth management firm, handling everything from investments and philanthropy to paying bills and family governance. You can get a better sense of how this works in our guide on private wealth management.

Ultimately, these services show the profound difference between basic financial advice and true wealth management. It's about having a dedicated strategist to help you navigate the complexities that always come with success.

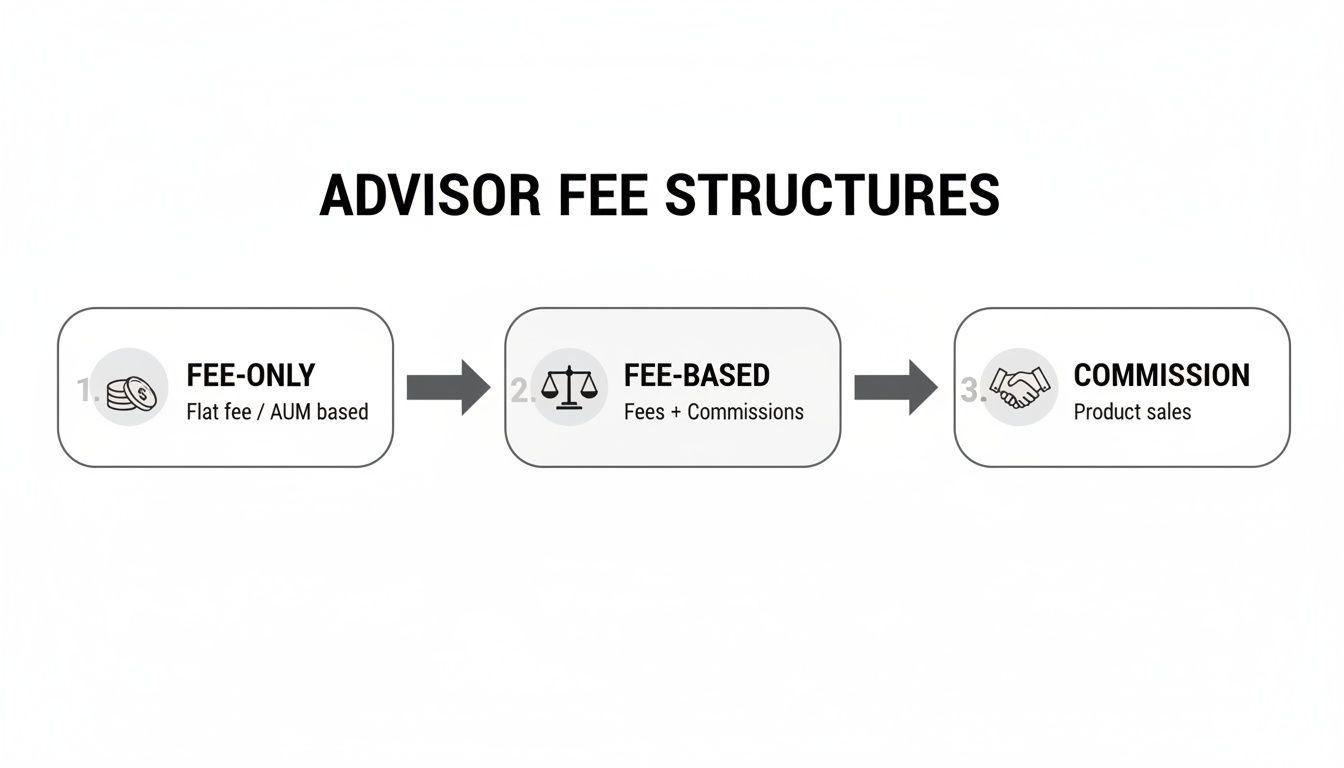

How Wealth Advisors Get Paid and Why It Matters

Let's talk about one of the most important, yet often overlooked, parts of hiring an advisor: how they get paid. This isn’t just a detail buried in the fine print; it’s the single biggest clue to whose interests they’re really serving.

How an advisor is compensated directly shapes the advice you receive and the investments they recommend. Before you sign anything, you have to understand this part of the relationship. It's the ultimate test of whether their success is truly tied to yours.

Fee-Only: The Gold Standard of Transparency

By far the cleanest and most client-focused model is fee-only. It’s exactly what it sounds like: the advisor is paid only by you, the client, for their expertise and management. There are no third-party kickbacks, no hidden commissions from insurance companies, and no incentives to push a particular product.

This structure puts you and your advisor on the same side of the table. Their success is directly linked to the growth of your portfolio.

The most common fee-only arrangement is based on Assets Under Management (AUM).

In an AUM model, the advisor charges a straightforward percentage of the assets they manage for you—typically around 1% annually. If your portfolio grows, they make more. If it shrinks, they make less. That simple alignment is a powerful motivator for them to act in your best interest.

Fee-Based: A Potential Conflict Zone

This is where the language gets tricky, and you need to pay close attention. "Fee-only" and "fee-based" sound almost the same, but they represent two completely different worlds. A fee-based advisor can make money in two ways: from the fees you pay them directly and from commissions they earn by selling you certain financial products, like annuities or insurance policies.

This creates a built-in conflict of interest. Is your advisor suggesting that insurance product because it's the perfect fit for your estate plan, or because it comes with a juicy 5-7% commission? You can never be entirely sure. While not every fee-based advisor lets commissions guide their hand, a local wealth advisor should be transparent about how these conflicts are managed.

Commission-Based: The Traditional Sales Model

The oldest and most problematic model is commission-based compensation. Here, the advisor makes a living almost entirely from commissions earned by selling financial products. Their income depends on transactions, not on the long-term health and performance of your money.

This model incentivizes activity over outcomes. An advisor might be encouraged to suggest frequent trades or push high-commission mutual funds, even if a simple, low-cost strategy would serve you far better. For anyone looking for objective, ongoing guidance, this model is a massive red flag.

A Clear Comparison of Advisor Fees

Choosing the right advisor starts with understanding these distinctions. When you look closer, it becomes obvious why the fee structure is so critical. For a more detailed breakdown, our guide offers a comprehensive wealth management fees comparison.

Here’s a simple breakdown of how the three models stack up:

Ultimately, working with a fee-only wealth advisor ensures you're paying for unbiased advice. Your financial success becomes their primary goal because their paycheck depends on it. This alignment is the bedrock of any trusting, productive, and long-term partnership.

Your Step-By-Step Vetting Process

Choosing a wealth advisor is one of the most critical financial decisions you'll ever make. This isn’t something to rush. It's a partnership that will shape your family's future, so you need a methodical, structured approach to find a true partner whose values and expertise are a perfect match for your goals.

Jumping into the search without a clear plan can feel overwhelming. But with the right process, you can turn this challenge into an empowering experience, giving you the confidence that you’ve found the right local wealth advisor to lead your team.

Stage 1: Initial Research And Candidate Sourcing

First things first, you need to build a short list of potential advisors. A quick Google search for something like "wealth advisor near me" is a starting point, but to find high-caliber professionals, you’ll need to be more strategic.

A fantastic place to start is by asking for referrals from the trusted professionals already in your corner, like your CPA or attorney. They often have deep networks and can point you toward reputable advisors who specialize in situations just like yours.

Next, expand your search by tapping into professional directories:

- The National Association of Personal Financial Advisors (NAPFA): This is the go-to resource for finding fee-only advisors who are legally bound to act as your fiduciary.

- The CFP Board: Use their official site to find a CERTIFIED FINANCIAL PLANNER™ professional near you. This credential ensures a high standard of expertise and ethical commitment.

As you build out your list, try to land on three to five strong candidates. This gives you enough options for comparison without leading to decision paralysis. For a deeper dive into finding local professionals, our guide on finding a financial advisor near me has some great additional tips.

Stage 2: Background Checks And Due Diligence

Before you even think about scheduling a meeting, it’s time to do some digging. This is a non-negotiable step to protect yourself from anyone with a history of misconduct or regulatory skeletons in their closet. Luckily, there are some powerful—and free—tools to help you.

Your first stop should be FINRA's BrokerCheck. This public database is a goldmine of information, detailing an advisor’s entire employment history, certifications, and—most importantly—any customer disputes, disciplinary actions, or other red flags. It takes just a few minutes and offers incredible transparency.

Another must-read is the advisor’s Form ADV, which they file with the Securities and Exchange Commission (SEC). This document lays out their business practices, fee structures, services, and any potential conflicts of interest. You can find it on the SEC's Investment Adviser Public Disclosure website.

A clean record on BrokerCheck and a straightforward Form ADV are the absolute minimum. If an advisor seems hesitant to share these or you find something that makes you uneasy, consider it a major red flag and walk away.

Part of your due diligence is also understanding exactly how an advisor gets paid. The differences between fee-only, fee-based, and commission structures create entirely different incentives, as this infographic illustrates.

As you can see, a fee-only structure is widely considered the gold standard. It minimizes conflicts of interest and aligns the advisor's success directly with your own.

Stage 3: Conducting Meaningful Interviews

Once you’ve done your homework and feel good about a candidate’s background, it’s time to sit down for a conversation. This is your chance to look past the resume and really gauge the personal fit, their communication style, and the true depth of their expertise.

Remember, this meeting isn't just a sales pitch for them; it's an interview where you are the one doing the hiring. Come prepared with a list of open-ended questions designed to get them talking beyond their rehearsed answers.

To help you get started, here is a list of essential questions to ask any prospective wealth advisor. Think of it as a checklist to ensure you cover all the critical bases before making a decision.

These questions aren't just a formality; they're designed to peel back the layers and reveal the substance behind the sales pitch.

A methodical vetting process like this empowers you to make a smart, confident choice. By moving deliberately from research to due diligence and finally to insightful interviews, you can find a wealth advisor who isn't just qualified, but is the right strategic partner for your family's entire financial journey.

Critical Red Flags to Avoid

Knowing what makes a great wealth advisor is only half the battle. You also have to know what to run from.

Spotting the warning signs early on can protect your family’s wealth from mismanagement, costly conflicts of interest, or even outright fraud. The best advice I can give is to trust your gut—if something feels off, it probably is.

One of the most obvious red flags is the promise of “guaranteed” high returns. Think about it: legitimate markets involve risk. Anyone guaranteeing a specific, lofty outcome is selling you a fantasy, not an investment strategy. This is usually a high-pressure sales tactic designed to short-circuit your better judgment. A real pro focuses on a disciplined, evidence-based process, not impossible promises.

Another major warning sign is a lack of transparency. If an advisor gets cagey about their fees, seems reluctant to hand over their Form ADV, or hesitates when you ask for a few client references, your alarms should be going off. A professional who operates with integrity and is proud of their work will be an open book.

Your relationship with an advisor has to be built on absolute clarity. If they can't—or won't—explain exactly how they get paid or what you're paying for, it's a huge sign their interests might not be aligned with yours.

Deceptive Practices and Conflicts of Interest

You have to be a detective when it comes to how an advisor is paid. We’ve already talked about the different models, but it’s crucial to spot the hidden conflicts that often come with a commission-based sales pitch.

Is an advisor pushing a specific annuity or a high-fee mutual fund? It might be because it pays them a fat commission, not because it’s the right move for you. You need to ask, point-blank: “How do you get paid for this recommendation?”

On a similar note, be very wary of any advisor who isn't a committed fiduciary. A non-fiduciary operates under a looser "suitability" standard. This means their advice only needs to be suitable, not necessarily in your absolute best interest. It’s a subtle distinction, but one that can cost you dearly over the years in higher fees and investments that just aren't quite right.

Keep an eye out for these other critical red flags:

- High-Pressure Sales Tactics: An advisor who rushes you into making a decision isn't respecting the importance of the partnership. This is your life's savings we're talking about; it’s not a one-day-only sale.

- Custody of Assets: A legitimate wealth advisor will never ask you to make checks payable directly to them or their firm. Your money should be held at a major, independent third-party custodian, like Fidelity or Charles Schwab. This is a non-negotiable safety measure.

- Lack of a Clear Process: If they can’t clearly explain their investment philosophy or walk you through their financial planning process, it signals a lack of discipline. A real strategy isn't a secret sauce; it's a repeatable, understandable method.

Confidently steering clear of these red flags is one of the most important things you can do to protect your wealth and find a true long-term partner.

Common Questions About Wealth Advisors

Stepping into the world of high-net-worth finance always kicks up a few questions. It’s completely natural. Here are some straightforward answers to the things people most often ask when they're thinking about bringing a wealth advisor onto their team.

What’s the Minimum to Get Started?

This definitely varies from firm to firm, but for the kind of comprehensive, all-in-one service we're talking about, you'll typically see a minimum of $500,000 to $1 million in investable assets.

There’s a reason for this. That threshold is usually the point where someone’s financial life becomes complex enough to really benefit from the sophisticated strategies a true wealth advisor brings to the table. It also ensures the advisory team can pour the necessary time and resources into managing your portfolio the right way.

How Often Will We Talk?

Any good advisor will map out a communication plan right from the start. You should absolutely expect formal review meetings, probably quarterly or semi-annually, to go over performance, check in on strategy, and discuss anything new happening in your life.

But the real value isn’t just in scheduled meetings; it’s in their proactive availability. The relationship should feel like a partnership. You need an open line of communication for those key moments that inevitably pop up, like:

- When the market gets choppy and you need a steady hand.

- Major life events, whether it's a marriage, an inheritance, or selling the company.

- Big financial decisions, like buying a second home or figuring out what to do with a bonus.

Can a Wealth Advisor Help With My Business?

Absolutely. In fact, this is where a great advisor really shines. For entrepreneurs and business owners, personal and business finances are almost always tangled together.

An experienced advisor acts as the quarterback, coordinating everything from succession planning to getting you ready for a sale. They'll work directly with your CPA to make sure your tax strategy is seamless across both your personal and business balance sheets, preventing the kind of costly mistakes that happen when these two worlds are kept in separate silos.

Is My Money Actually Safe?

This is probably the most important question you can ask, and the answer comes down to one critical concept: asset custody.

Here’s the deal: a reputable wealth advisor will never hold your money directly. Your assets—your stocks, bonds, and cash—are held at a completely separate and independent custodian. Think of big, established institutions like Charles Schwab, Fidelity, or BNY Mellon Pershing.

This separation is your single biggest protection. The custodian is the one sending you independent statements, giving you online access, and providing insurance for your assets (like SIPC insurance). This setup creates a crucial system of checks and balances. Your advisor can manage the investments, but they can't just walk away with your money. Always, always confirm that an advisor uses a major, independent custodian before you sign anything.

At Commons Capital, we bring the clarity and strategic thinking high-net-worth families need to move toward their financial future with real confidence. If you're ready to partner with a dedicated wealth advisor, we invite you to learn more about our approach.