Think of private wealth management as the financial quarterback for your entire life. It’s a comprehensive, high-touch service designed for individuals and families whose financial pictures are anything but simple. This goes far beyond just picking stocks; it's about coordinating every piece of your financial puzzle—from investments and taxes to estate planning and charitable giving—into a single, unified strategy. This guide offers an in-depth look at what private wealth management entails and how it can secure your legacy.

What Does a Private Wealth Manager Actually Do?

Imagine hiring a typical financial advisor. They're like a star wide receiver on a football team—incredibly skilled at their specific role, which might be managing a mutual fund or picking promising stocks. A robo-advisor? That's the kicking machine, executing one automated task with precision. Both are useful, but their focus is narrow.

Private wealth management, on the other hand, is the head coach and quarterback all in one. It’s not just about one part of the game. The role is to design the entire playbook, manage the team, and call the shots on the field to win the championship. For you, that championship is achieving your long-term financial goals and building a legacy that lasts.

A Holistic and Integrated Approach

This high-level coordination is the key difference. It’s an approach built for people whose financial lives have a lot of moving parts that absolutely must work together.

A client might be a founder getting ready to sell their company, a tech executive juggling stock options and RSUs, or a family looking to pass wealth to the next generation. For them, making an investment decision in a vacuum could create a massive tax headache or complicate their estate plans down the road.

Private wealth management ensures your investment strategy, tax planning, and legacy goals aren't treated as separate silos. They're woven together into a seamless plan designed to protect and grow your wealth in the most efficient way possible.

More Than Just Managing Money

The real value is in that strategic integration. For example, instead of just buying a set of stocks, a wealth manager might structure those investments to minimize your tax bill. They’ll work directly with your CPA and estate attorney to make sure your will and trusts align perfectly with your portfolio, avoiding expensive conflicts later on. You can see how we handle this core function by reading about our philosophy on investment management.

This kind of detailed oversight is more important than ever. The demand for coordinated financial guidance is exploding. In the U.S. alone, wealth managers are forecasting an average asset under management (AUM) growth of 17.6%. This growth is fueled by market dynamics and the simple fact that as wealth becomes more complex, the need for a dedicated financial quarterback becomes undeniable.

The Core Services That Safeguard Your Future

A truly comprehensive wealth management strategy isn't just a collection of services; it's a single, integrated plan where every piece works together. Think of it less like an à la carte menu and more like a custom-engineered vehicle—every component is designed to work in harmony to get you where you want to go, smoothly and safely.

The goal is to grow, protect, and eventually transfer your wealth in a way that aligns perfectly with your vision for the future.

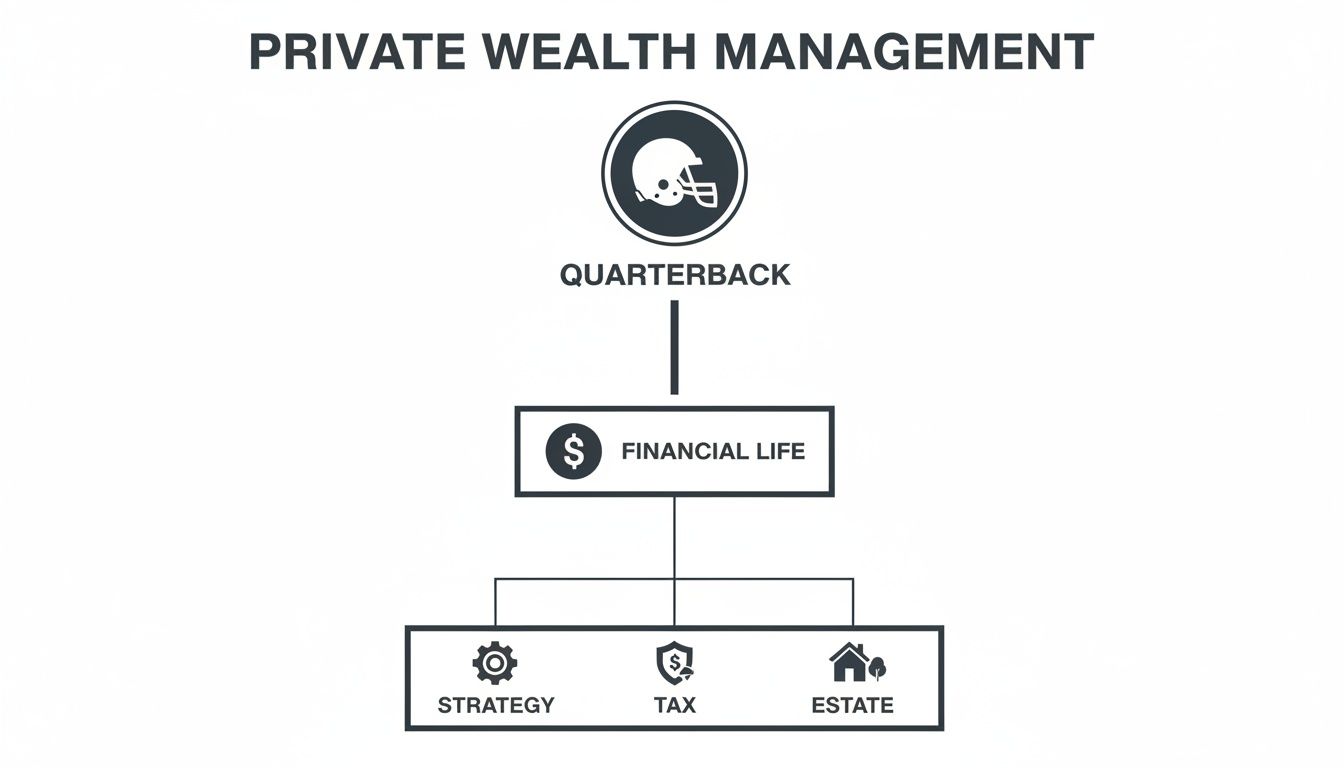

This is why many people think of their private wealth manager as the "quarterback" of their financial life. They’re the central coordinator calling the plays and making sure the entire team—from tax advisors to estate attorneys—is executing the same strategy.

As you can see, real wealth management is a top-down approach. One central point of contact oversees the critical pillars of investment strategy, tax planning, and your estate, ensuring nothing falls through the cracks.

Below is a quick look at how these core services come together to support the needs of high-net-worth clients.

Private Wealth Management Services Overview

Each of these pillars is essential for building a resilient financial future. Let's dig into what each one really entails.

Investment Management

At its core, investment management is the engine that drives your portfolio forward. For high-net-worth individuals, this is so much more than just picking a few stocks and bonds. It's about crafting a highly sophisticated asset allocation plan that’s built around your specific goals, timeline, and comfort with risk.

A key part of this is gaining access to investment opportunities that simply aren't available to the average investor. We're talking about things like private equity, venture capital, and direct real estate deals. In fact, 92% of financial advisors are now integrating these kinds of alternative investments into their clients' portfolios. It's a clear move toward greater diversification and tapping into new sources of growth.

Financial and Tax Planning

While smart investing grows your wealth, proactive financial and tax planning is what helps you keep it. A great wealth manager doesn’t just clean up your tax situation at the end of the year; they build tax efficiency into your financial DNA from day one.

This involves deploying specific strategies throughout the year, such as:

- Tax-loss harvesting: Intentionally selling investments at a loss to offset the capital gains taxes you owe on your winners.

- Asset location: Strategically placing different types of investments in the most tax-friendly accounts (like putting high-growth assets in a tax-free Roth IRA).

- Smart charitable giving: Using tools like donor-advised funds to maximize your philanthropic impact while also minimizing your tax bill.

By weaving these tactics into your overall plan, every financial decision is made with an eye on the tax implications. Over the long run, this can have a massive impact on your net returns.

Estate and Trust Planning

What happens to everything you've built after you're gone? This is perhaps the most important question that estate and trust planning answers. The whole point is to create a durable legacy that reflects your values and provides for your loved ones in the most efficient way possible.

Here, your wealth manager works hand-in-hand with legal experts to structure your estate. They make sure your assets are transferred smoothly, with as little lost to taxes as possible. This involves much more than just investments; it means getting strategic about the legal nuts and bolts, like wills, trusts, and estate planning.

The goal is to design a plan that not only preserves wealth but also prepares your heirs for the responsibilities that come with it, preventing potential disputes and protecting your legacy for generations.

Thoughtful planning is the difference between a seamless transition and a messy, expensive legal headache for your family. By tackling these issues ahead of time, you can secure your legacy. You can find a more in-depth look at this process in our guide on Trust and Estate Planning.

Philanthropic Advisory

For many successful individuals and families, wealth becomes a powerful tool for making a difference. Philanthropic advisory services are there to help you turn your good intentions into a structured, high-impact giving strategy.

Your advisor can help you identify causes you’re passionate about, properly vet charitable organizations, and set up the right giving vehicles, whether that’s a private foundation or a donor-advised fund. This approach ensures your contributions aren't just generous but also strategic, creating a lasting impact that truly aligns with your personal mission.

Navigating Modern Investment Strategies

The days of leaning on a simple mix of stocks and bonds are long over. That classic 60/40 portfolio, once the gold standard of investing, just doesn't have the muscle to deliver the kind of growth and protection high-net-worth families need today. Modern private wealth management operates on a much more sophisticated playbook, one designed for the realities of today's interconnected global markets.

This shift isn't just about chasing bigger numbers. It’s about building a financial foundation that’s truly resilient. That means looking beyond the familiar public markets and into a world of opportunities with entirely different risk-and-return characteristics.

The Shift Toward Private Markets

A cornerstone of any modern wealth strategy is a deliberate allocation to private markets. These are simply investments in companies or assets that aren’t listed on a public stock exchange like the NYSE.

Here's a good analogy: public stocks are like famous artists whose work is widely available in major galleries. Private market investments are like discovering a brilliant, under-the-radar artist before they hit the big time. The opportunities are exclusive and can be far more rewarding, but you absolutely need an expert guide to find them.

This isn’t just a niche trend; major capital is moving in this direction. Projections for 2025 show that 83% of limited partners plan to maintain or increase their capital deployment into private markets, and 43% of institutional investors are set to boost their own allocations.

Why Alternative Investments Are Essential

Private markets fall under a wider umbrella called alternative investments. These are assets that don't fit neatly into the traditional boxes of stocks, bonds, or cash. For qualified investors, they bring some serious advantages to the table.

Key types of alternative investments include:

- Private Equity: This involves investing directly in private companies. It could be a promising startup or an established business you’re helping to grow, all with the goal of a significant return when the company is eventually sold or goes public.

- Private Credit: Think of this as being the bank. You're lending money directly to businesses, which can generate a steady, predictable income stream that often isn't tied to the daily drama of the stock market.

- Real Estate: Investing in physical properties like commercial buildings or apartment complexes can provide both rental income and the potential for long-term appreciation.

These assets are absolutely critical for diversification. When public markets get choppy, private investments often march to the beat of their own drum, helping to smooth out your portfolio’s performance and protect your capital. This is exactly why they are becoming a core part of so many portfolios. You can learn more about specific high-net-worth investment strategies in our detailed guide.

Unlocking Growth and Managing Risk

The appeal of alternatives isn't just about playing defense. They offer access to unique sources of growth you simply can’t find in public markets. When you invest in a private company, you're directly participating in its story—its innovation, its expansion—in a way that buying a few shares of a mega-cap stock just can't match.

Of course, these opportunities come with their own rulebook. We’re talking about longer holding periods, less liquidity, and the need for intense due diligence. This is precisely where a skilled private wealth management team proves its worth. They act as your filter and your guide, vetting opportunities and structuring deals to fit your long-term goals.

A smart advisor also keeps an eye on the bigger picture, like the effects of economic shifts on wealth, which can have a massive impact on your portfolio’s real-world value. Their job is to help you navigate these exclusive markets, ensuring you can capitalize on the potential while keeping the risks firmly in check.

Is Private Wealth Management Really for You?

So, who actually needs this level of white-glove service? It’s a fair question. The truth is, private wealth management isn’t for everyone—and that’s by design. It's built for those whose financial lives have become so complex that off-the-shelf advice just doesn't cut it anymore.

The real question isn't "Am I rich enough?" It's "Is my financial life complicated enough to need a dedicated team?"

The Magic Number (and Why It's Not So Magical)

You'll often hear that the entry point for private wealth management is around $500,000 in investable assets. While that's a common benchmark for many firms, it’s not some arbitrary gate. It's the point where a person's financial world usually starts getting messy enough to need the kind of integrated, high-touch service we’ve been talking about—things like access to private investments or sophisticated tax strategies.

But don't get too hung up on the dollar amount. Complexity is the real tell. You might have a straightforward, multi-million dollar portfolio of stocks and bonds that a good financial advisor can manage perfectly well. On the other hand, someone with less in assets but a tangled web of business interests, real estate, and stock options might desperately need a wealth manager to get things in order.

Who Truly Gets the Most Out of It?

While everyone's situation is different, a few types of people consistently get the most value from a private wealth management relationship. These aren't just folks looking to pick the next hot stock; they need a strategic co-pilot to navigate all the moving parts of their financial lives.

It's less about the size of your net worth and more about the complexity of your financial life. When your investment, tax, and legacy planning start to overlap and conflict, it's a strong sign you've outgrown basic financial advice.

Let’s dig into a few real-world scenarios where having this kind of quarterback becomes a game-changer.

Common Client Scenarios

The need for a dedicated wealth manager often pops up during major life events or when dealing with assets that don't fit neatly into a brokerage account. Here are a few classic examples of people who are prime candidates:

- Business Owners Nearing an Exit: Selling a business is a once-in-a-lifetime financial event. It's a maze of tax planning, succession strategies, and figuring out how to reinvest the proceeds to fund your next chapter. A wealth manager is the one who brings the lawyers and accountants together to make it a smooth, tax-efficient transition.

- Executives with Complicated Paychecks: Top corporate leaders often get paid in more than just cash. Their compensation is a mix of stock options, RSUs, and deferred comp plans. These aren't simple assets; they require careful planning to manage the tax hit, diversify away from having all your eggs in one company basket, and make sure it all aligns with your personal financial goals.

- Families Building a Legacy: When the goal is to pass wealth down through generations, the planning gets a lot bigger than just one person's retirement. Wealth management helps structure trusts, set up a system for family decision-making (governance), and get the next generation ready to be smart, responsible stewards of what's been built.

- Professionals with "Lumpy" Income: Think athletes, entertainers, or high-end consultants. They might have massive earning years followed by leaner ones. A wealth manager brings the discipline and long-term strategy to turn those peak years into a lifetime of financial security, smoothing out the highs and lows.

If any of these sound like you, your financial needs have probably outgrown what a standard advisor can offer. The real prize isn't just about chasing higher returns; it's the profound peace of mind that comes from knowing an expert is making sure every piece of your financial puzzle fits together perfectly.

How to Choose the Right Wealth Management Firm

Picking a wealth management firm isn't like choosing a stock or a new bank account. It's one of the most critical financial decisions you'll ever make. You're not just hiring a service; you're bringing a long-term strategic partner into your inner circle. The right fit can feel like finding a co-pilot for your family's entire financial journey. The wrong one? It can lead to years of frustration, missed opportunities, and unnecessary stress.

Making a good choice goes way beyond slick presentations or a fancy downtown office. You have to look under the hood. It’s a process of careful evaluation, digging into a firm's core philosophy, how they make money, and—most importantly—where their loyalties legally lie.

Start with Fiduciary Duty

Before you get into any other detail, there's one concept you absolutely must understand: the fiduciary standard. This isn't just industry-speak; it's a legal and ethical line in the sand. A fiduciary is required, by law, to act in your best interest. Period.

This means they must put your financial well-being ahead of their own and their firm's. It’s a world away from the much weaker "suitability standard," where an advisor only has to recommend products that are suitable for your situation—even if there's a better or cheaper option available that would make them a smaller commission.

The very first question for any potential advisor should be direct and simple: "Do you act as a fiduciary 100% of the time?" The only acceptable answer is an immediate "yes." If you get a long-winded explanation or any hesitation, that’s a massive red flag.

Getting this right from the start ensures the advice you get is truly about your goals, not about padding their bottom line.

Evaluate Their Experience and Specialization

Wealth management is not a one-size-fits-all business. Some firms are brilliant at handling the complex stock options of tech founders. Others have built their reputation on guiding professional athletes through short, high-earning careers. Still others are masters of managing multi-generational family trusts.

Look for a firm that has walked this path before with people just like you. A wealth manager who already gets your world—the specific challenges you face and the unique opportunities you have—is going to be light-years more effective than a generalist. Their niche expertise means they've already seen and solved the problems you’re just starting to think about.

Key Questions to Ask a Potential Advisor

When you sit down for that first meeting, remember that you are the one doing the interviewing. This is a job interview for a crucial role in your life. Come prepared with questions that cut through the sales pitch and reveal how they actually think and operate.

Here are a few essential questions to get the conversation started:

- Investment Philosophy: "Walk me through your core investment philosophy. For a client like me, how would you approach building a portfolio and managing risk?" You're listening for a clear, disciplined process, not just promises to chase the latest hot trend.

- Client Experience: "Describe your typical client. Could you share some anonymous examples of how you've helped families in a similar position to ours?" This helps you see if you truly fit their model and if they have real-world experience that's relevant to you.

- Communication and Reporting: "How often can I expect to hear from you? What do your reports look like, and who will be my day-to-day contact?" There's no single right answer here, but you need to know their communication style matches your expectations.

- Navigating Downturns: "Tell me about the last major market downturn. How did you guide your clients through it? What was your strategy, and how did you communicate when things got scary?" A great advisor proves their worth when markets are volatile, not when they're soaring.

- Fee Structure: "Can you give me a complete, transparent breakdown of all your fees? I want to understand every single way you get paid." Insist on total clarity. Most firms charge a percentage of assets under management (AUM), but you need to be sure there are no hidden costs.

Putting in the time to do this homework is a direct investment in your financial peace of mind. Finding a firm that shares your values, understands your life, and is legally bound to put you first is the bedrock of a partnership that can last for generations.

What to Expect from Your Client-Advisor Partnership

Hiring a private wealth management firm isn't like making a simple transaction; it's the start of a deep, long-term partnership. This relationship is designed to grow and change with you, going far beyond a one-off piece of advice to become a core fixture in your financial life for decades.

The whole thing kicks off with a detailed discovery process. This is much more than just forms and numbers. It’s a series of candid conversations where your advisor gets to know not just your portfolio, but your personal values, your worries, and what you truly want out of life. Think of them as your financial biographer, learning your story so they can help you write the next chapter.

This first phase is all about creating a complete map of your financial universe. Your advisor will dig into every asset, every debt, and every income stream to get the full 360-degree view. The idea is to set a clear starting point and define what "success" actually means for you and your family.

The Initial Strategy and Implementation

Once your goals are crystal clear, your advisor translates them into a concrete financial plan. This isn't just a binder that sits on a shelf; it's your strategic roadmap. It will spell out the specific investment, tax, and estate planning moves required to get you where you want to go. This is where the integrated nature of private wealth management really shines.

Putting the plan into motion is a carefully coordinated effort. Your team will start shifting your assets to align with the new strategy. They'll also be in constant contact with your other key people—like your attorney and CPA—to make sure everyone is on the same page and working from the same playbook. Expect them to be proactive and completely transparent every step of the way.

Evolving with Your Life

A good financial plan is never set in stone. It’s a living, breathing document that has to adapt as your life changes. Your partnership with an advisor is built to be flexible, ready to respond to major life events as they happen.

The real value of a long-term advisory relationship reveals itself during moments of significant change. An advisor who deeply understands your history and goals can provide steady, trusted guidance when you need it most.

Life’s big moments demand strategic shifts and a calm, experienced hand. Your advisory team is there to help you navigate these transitions without a hitch.

- A Business Sale: Your advisor steps in to manage the influx of cash, helping you minimize the tax hit and structure the proceeds to fund whatever’s next.

- An Inheritance: They’ll guide you through the process of absorbing new assets into your plan, making sure the wealth transfer is as smooth and efficient as possible.

- Retirement: The entire strategy pivots from growing your wealth to protecting it and generating income. Your portfolio is re-engineered to provide the steady cash flow you need to live the life you want.

- Market Volatility: When markets get chaotic, your advisor becomes more of a behavioral coach. They help you stick to your long-term plan and avoid making emotional decisions based on short-term noise.

This ongoing collaboration is the absolute core of the client-advisor partnership. It ensures your financial strategy stays perfectly in sync with your life, giving you the confidence and clarity to face the future.

Your Questions About Private Wealth Management, Answered

When you're dealing with significant wealth, a lot of questions come up. It's only natural. Here, we'll tackle some of the most common ones we hear, giving you straightforward answers to help you understand the practical side of working with a private wealth management team.

Think of this as clearing the path, so you can decide if this level of dedicated service is the right move for you and your family.

How Do Wealth Managers Get Paid?

The most common model you'll see is a fee based on a percentage of your Assets Under Management (AUM). This usually falls somewhere between 0.5% and 1.25% per year, though the exact number can shift depending on how much you invest and how complex your financial picture is.

The beauty of this structure is that it puts us on the same side of the table. When your portfolio grows, our compensation does too. It creates a built-in incentive for us to perform well for you. While some firms might use a flat-fee or a blended approach, you should always ask for a crystal-clear breakdown of all costs before you sign anything. No surprises.

Isn't This Just a Family Office?

That's a great question, and while there's a lot of overlap, there's a core difference in who they serve. A private wealth management firm, like ours, works with a select group of high-net-worth individuals and families. We offer a deep bench of experts whose knowledge is shared across our client base.

A family office, on the other hand, is a dedicated company set up to serve just one ultra-wealthy family.

The key distinction really comes down to exclusivity. A family office is like having your own in-house CFO for everything, often handling personal tasks like managing properties or coordinating travel alongside the finances. A wealth management firm provides that same elite level of financial expertise, but to a broader clientele.

What Does It Mean to Be a Fiduciary?

This is one of the most important concepts to understand. A fiduciary is an advisor who has a legal and ethical obligation to act in your best interest. Always. It’s the highest standard of care in our industry, period.

Working with a fiduciary is non-negotiable. It's your assurance that the advice you're getting is based entirely on what's best for your financial goals, not on what might earn the advisor a bigger commission. Before you hire anyone, you should ask them point-blank: "Do you act as a fiduciary 100% of the time?" The answer should be an immediate and unequivocal "yes."

At Commons Capital, we're fiduciaries, plain and simple. We believe that providing this level of care and strategic guidance is the only way to manage the complexities of your financial life. To see how our integrated approach can help you build and protect your legacy, come see us at https://www.commonsllc.com.