When you receive a windfall, the first and most important thing to do is… absolutely nothing.

Seriously. For at least the first few months, your best move is to avoid making any significant financial decisions. This pause is the single most powerful action you can take to protect the assets and keep yourself from making a rash choice driven by emotion. Figuring out what to do with inheritance money is a marathon, not a sprint, and this initial period of inaction is your crucial first step.

Navigating Your First Steps With an Inheritance

An inheritance often shows up during a period of grief, a time when untangling complex financial knots is the last thing you want to do. The pressure to act—whether from well-meaning relatives or your own anxieties—can feel immense. But the wisest course is to create a temporary, secure holding pattern for the funds while you process everything and gather your thoughts.

This initial phase isn't about crafting a grand, long-term strategy. It's simply about stability and security. Think of it as docking a ship in a safe harbor before you even begin to chart its next voyage. Your only goal right now is to make sure the assets are safe, accessible, and not exposed to unnecessary risks or impulsive spending.

To help you through this critical period, here's a quick checklist of the immediate actions you should take. These steps are designed to secure the funds while giving you the breathing room you need to plan thoughtfully.

Immediate Action Checklist for Your Inheritance

Pause and Breathe - Prevents emotional, high-stakes decisions during a difficult time.

First 1-3 Months Secure Cash in an HYSA - Separates inheritance from daily funds and earns interest safely.

First Week Verify FDIC/NCUA Insurance - Protects your deposits up to $250,000 per institution.

First Week Gather Key Documents - Provides a clear picture of what you've inherited and any obligations.

First Month Notify Relevant Parties - Informs Social Security, banks, and creditors of the passing.

First 1-2 Months Consult Professionals - Get initial guidance from a financial advisor and/or an estate attorney.

Following these steps ensures nothing falls through the cracks and buys you the time necessary to make smart, deliberate choices for your future.

Secure the Assets Immediately

The very first thing to do is deposit any cash inheritance into a new, separate high-yield savings account (HYSA). This simple move accomplishes two critical goals. First, it keeps the inheritance money walled off from your daily finances, which is the easiest way to prevent it from getting accidentally spent. Second, a good HYSA allows the money to earn a competitive interest rate while staying completely liquid—meaning you can get to it whenever you're ready.

Make sure this account is at a federally insured institution, like a bank covered by the FDIC or a credit union by the NCUA. This insurance protects your deposit up to $250,000 per depositor, per institution. If your inheritance is larger than that, you can simply open accounts at multiple banks to ensure every dollar is protected.

Locate Essential Documents

Once the cash is safely parked, your next job is to go on a paper trail hunt. This administrative task is crucial for understanding the full picture of your inheritance and any strings that might be attached. The key documents you’ll need to track down include:

- The Will or Trust: This is the core legal document that spells out the deceased's wishes and your specific share.

- Life Insurance Policies: If you're a named beneficiary, you'll need the policy paperwork to file a claim.

- Retirement Account Information: You’ll need the details for any 401(k)s, IRAs, or pensions you're inheriting to claim the funds.

- Real Estate Deeds and Titles: If property is involved, these are essential for transferring ownership.

- Bank and Brokerage Statements: These show the value of any financial accounts as of the date of death.

Receiving an inheritance is a marathon, not a sprint. Grant yourself the time and grace to move slowly, make informed decisions, and honor the legacy you've been given by building a secure financial future.

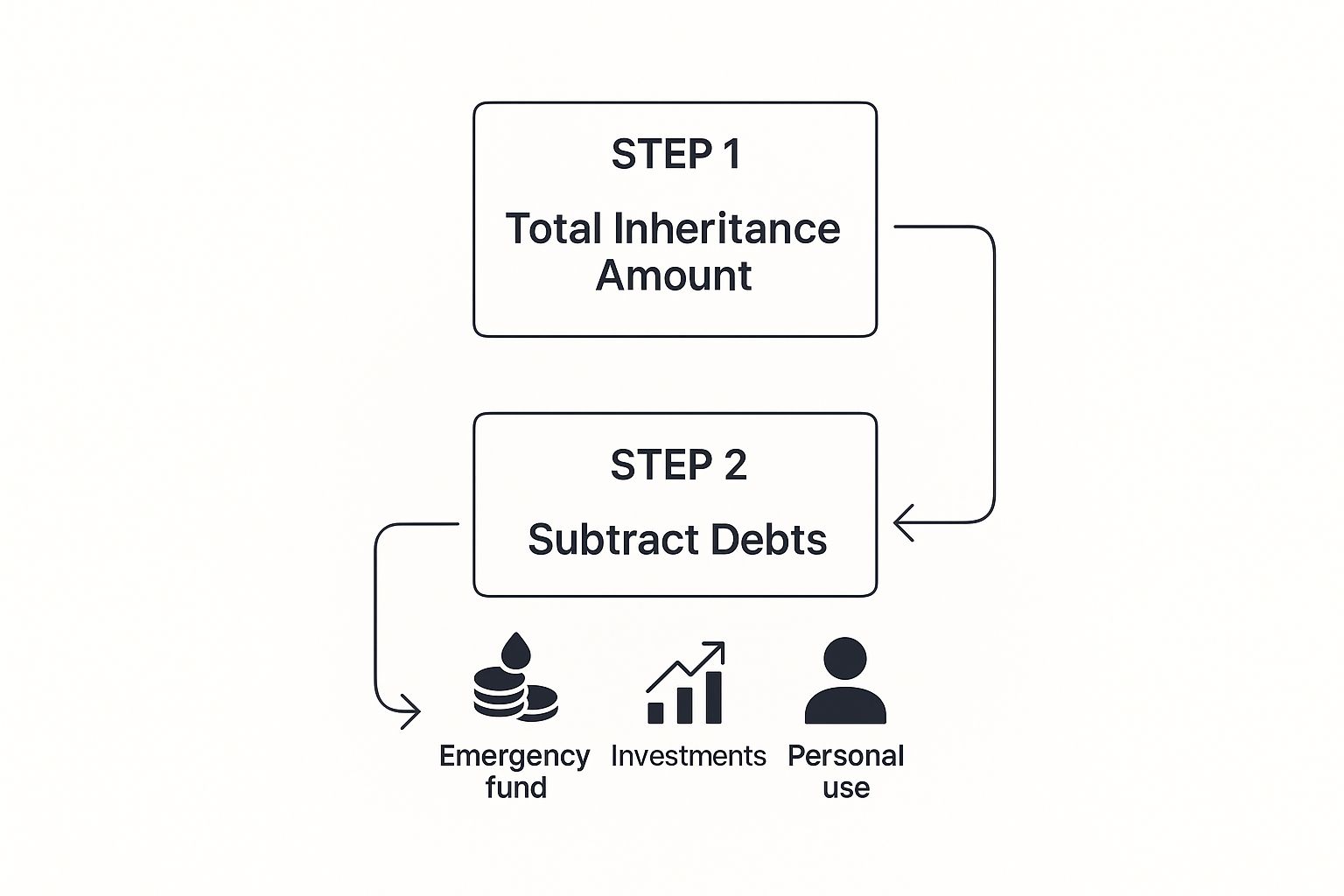

The simple process below shows how to think about your inheritance after you've taken this initial pause.

The key takeaway here is that you have to account for any outstanding debts or obligations before you can really know the net amount available to put toward your financial goals.

Assembling Your Financial Advisory Team

Managing a significant inheritance isn’t something you should do alone. Think about it: you wouldn’t build a house without an architect, an engineer, and a skilled construction crew. The same logic applies here. You're building a durable financial future, and that requires a team of qualified professionals.

Figuring out what to do with inheritance money brings up a tangle of legal, tax, and investment questions that honestly demand specialized expertise.

Going it alone can lead to costly mistakes, missed opportunities, and a whole lot of unnecessary stress. When you assemble a trusted team, you surround yourself with the knowledge and objectivity needed to make smart, level-headed decisions. This is your personal board of directors, all focused on helping you protect and grow these assets for the long haul.

Who Should Be on Your Financial Team?

Your financial "dream team" really comes down to three key players, each with a distinct and vital role. While their duties might overlap here and there, their core jobs address completely different parts of your financial well-being. Getting the right people in these seats is the first big step toward a solid plan.

- The Financial Advisor: This person is your architect. They help design the overall blueprint for your financial life by looking at the big picture—your goals, your comfort with risk, and your timeline—to craft a comprehensive investment strategy.

- The Tax Specialist (CPA): Your tax pro is the engineer, making sure your financial structure is sound and compliant with all the tax laws. They’ll be the one to analyze the tax hit from the inheritance itself and guide every financial move you make from that point forward.

- The Estate Planning Attorney: This is your master builder. They create the legal structures, like wills and trusts, that protect your assets and ensure they are passed on exactly how you want. Their work is all about building a legacy that lasts.

The Role of a Fiduciary Financial Advisor

When you start looking for a financial advisor, there's one word that matters more than any other: fiduciary. A fiduciary is legally and ethically bound to act in your best interest. Always.

This is a massive distinction from other advisors who operate under a "suitability" standard. That standard only requires their recommendations to be suitable, not necessarily what’s best for you.

A non-fiduciary might suggest an investment that’s suitable for your goals but just so happens to pay them a higher commission than a better-performing, lower-cost alternative. A fiduciary, on the other hand, is obligated to recommend that better, lower-cost option because it is unequivocally in your best interest.

By working with a fiduciary, you ensure the advice you get is objective and focused solely on your success, not on generating commissions for the advisor. This alignment of interests is the bedrock of a trusting and effective advisory relationship.

Key Questions to Ask Potential Advisors

Before you hire anyone, you need to interview them. Thoroughly. You’re entrusting this team with your financial future, so take the time to find the right fit. Treat it like a job interview where you’re the one doing the hiring.

Here are a few essential questions to ask any potential team member:

- "Are you a fiduciary?" For financial advisors, the answer needs to be a clear and immediate "yes." No hesitation.

- "How are you compensated?" You need to understand their fee structure. Do they earn a fee based on the assets they manage (fee-only), commissions on products they sell (commission-based), or a mix of both (fee-based)? Fee-only is often the cleanest structure, as it minimizes conflicts of interest.

- "What are your credentials and experience?" Look for established certifications like Certified Financial Planner (CFP®), Certified Public Accountant (CPA) for tax specialists, or Juris Doctor (JD) for attorneys.

- "Who is your typical client?" Make sure they have experience working with people in situations just like yours—specifically, individuals who have recently come into an inheritance.

By carefully selecting these three key professionals, you lay a rock-solid foundation for a successful financial strategy. This team will provide the guidance you need to navigate the complexities ahead, helping you make confident decisions that honor the legacy you've received.

Clearing Debt and Understanding Tax Implications

Before your inheritance can start building future wealth, it needs to shore up your current financial foundation. That means getting a handle on two of the biggest hurdles that can undermine long-term growth: existing debt and potential taxes. Tackling these issues right away is a crucial part of figuring out what to do with inheritance money.

Think of your financial life like a bucket. Before you can start filling it with new assets, you have to plug any existing holes. High-interest debt is a massive leak, constantly draining your resources and working against your efforts to grow your wealth.

By creating a clear plan for debt and taxes, you ensure that every dollar of your inheritance gets put to its best use, rather than being chipped away by interest payments or unexpected tax bills.

Creating a Strategic Debt Paydown Plan

An inheritance is a powerful tool for eliminating debt, but it requires a smart approach. Not all debt is created equal, so the best strategy is to prioritize the debts that are costing you the most.

The most damaging debts are typically those with high-interest rates and no tax deductions. We’re talking about credit card balances, personal loans, and auto loans, where interest rates can easily top 15% or even 20%. Wiping these out provides an immediate, guaranteed return on your money equal to the interest rate you were paying.

Using a portion of your inheritance to eliminate high-interest credit card debt is one of the smartest financial moves you can make. It’s like earning a guaranteed 20% return on your money, risk-free.

Lower-interest debt, like a mortgage or federal student loans, presents a more nuanced decision. The emotional security of being completely debt-free is a powerful feeling, but the math might point in a different direction. If your mortgage rate is 4%, but you can confidently expect to earn a 7% average return by investing in a diversified portfolio, you may be better off financially by investing the money instead. A financial advisor can help you weigh this "arbitrage" opportunity against your personal comfort with holding debt.

Demystifying Inheritance and Estate Taxes

One of the first questions on everyone’s mind is, "Am I going to owe taxes on this?" Fortunately, for most people in the United States, the answer is no. There is no federal inheritance tax, which means beneficiaries are not taxed directly by the federal government on the assets they receive.

However, it's crucial to understand the difference between two types of taxes:

- Federal Estate Tax: This is a tax paid by the estate of the deceased person, not by you. It only kicks in for estates with assets exceeding a very high federal exemption limit, so it impacts very few families.

- State Inheritance Tax: This is a tax paid by you, the beneficiary. Only six states currently have one: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. The tax rate often depends on your relationship to the person who passed away.

Beyond these, you should be aware of how inherited assets are treated down the road. Most inherited assets, like stocks or real estate, get a "step-up in basis." This is a huge tax advantage. It means the asset's cost basis is reset to its fair market value on the date of the original owner's death. This simple rule can erase decades of built-up capital gains, allowing you to sell the asset right away with little to no tax liability.

Our team can help you explore more ways to minimize your tax liability as you manage your new assets.

Building a Long-Term Investment Strategy

Once your financial foundation is solid, it's time to shift your thinking from preservation to growth. This is the moment your inheritance starts its real work, transforming from a lump sum into a powerful engine for your long-term financial well-being. The key is building a resilient, well-thought-out investment strategy.

This isn’t about chasing fads or trying to time the market. It's about crafting a durable portfolio that lines up with your personal goals, your timeline, and your comfort with risk. A proper strategy is designed to generate steady growth over many years—not deliver quick, unpredictable gains.

Defining Your Investment Philosophy

Before you invest a single dollar, you need a clear philosophy. Think of it as your personal investment constitution. It’s what will guide your decisions and help you stay the course when the market inevitably gets choppy.

Your philosophy should be built around three core pillars:

- Your Goals: What, exactly, do you want this money to do for you? Are you planning for retirement, funding a child's education, or buying a home? Specific, measurable goals will shape your entire approach.

- Your Timeline: When will you need to access these funds? A goal that’s 20 years away allows for a more growth-oriented strategy, while a goal just five years out requires a more conservative touch to protect the principal.

- Your Risk Tolerance: How would you really feel if your portfolio's value dropped by 15% in a month? Be honest with yourself. Understanding your emotional response to market swings is crucial for building a portfolio you can actually stick with.

This framework is the first step in a comprehensive financial planning process that makes sure your investment decisions always align with your life's objectives.

The Core Components of a Diversified Portfolio

You’ve heard the old saying, "don't put all your eggs in one basket." That’s the heart of portfolio construction. Diversification simply means spreading your investments across different types of assets to lower your risk. If one part of your portfolio is having a bad year, another part might be doing well, helping to smooth out your overall returns.

Your core portfolio will likely be built using three primary asset classes.

Stocks for Growth Potential

Stocks, also known as equities, represent ownership in a company. They offer the highest potential for long-term growth but also come with the most volatility. A simple and incredibly effective way to invest in a broad range of stocks is through low-cost index funds or Exchange-Traded Funds (ETFs).

An ETF that tracks the S&P 500, for instance, gives you instant diversification across 500 of the largest U.S. companies. This keeps your success from being tied to the fate of just a handful of individual stocks.

Bonds for Stability and Income

Think of bonds as loans you make to a government or corporation in exchange for regular interest payments. They are generally less risky than stocks and provide a stable anchor for your portfolio. When the stock market gets wild, high-quality bonds often hold their value or even increase, providing a much-needed buffer.

Cash Equivalents for Liquidity

This includes assets that are easy to get to, like high-yield savings accounts or money market funds. Holding a small portion of your portfolio in cash gives you liquidity for emergencies and allows you to jump on investment opportunities as they arise without having to sell your long-term holdings.

The goal is not to avoid risk entirely—that would mean missing out on growth. The goal is to manage risk intelligently by balancing different asset classes in a way that aligns with your personal investment philosophy.

Expanding Beyond the Core

Once your core portfolio is established, you might consider allocating a smaller slice to alternative investments. These can offer even more diversification and potentially higher returns, though they often come with higher risk and are harder to sell quickly.

Such investments could include:

- Real Estate: Either through direct ownership of property or through Real Estate Investment Trusts (REITs).

- Private Markets: Investing in private companies or funds that aren't available on public stock exchanges.

- Commodities: Things like gold or oil, which can act as a hedge against inflation.

Using Your Inheritance for Real Estate

For a lot of people, the idea of a sudden financial windfall immediately sparks dreams of buying a home or investing in property. It’s a natural instinct. Using an inheritance to get into real estate can be a powerful move, giving you both a tangible asset and a place to build your life. But jumping into the property market without a solid game plan can quickly turn that dream into a financial headache.

Figuring out what to do with inheritance money when it comes to real estate means taking an honest look at your personal goals and your entire financial picture. Property is a classic illiquid asset—you can't just convert it into cash overnight. That’s why it’s so important to understand exactly how a big purchase like this fits into the rest of your portfolio.

Primary Home or Investment Property?

The first big fork in the road is deciding what this property is for. Is this the home you're going to live in, or is it an asset you want to generate income? These two paths have completely different financial and lifestyle implications.

Buying a primary residence can bring a huge sense of emotional security and stability. It's a place to put down roots, and every mortgage payment builds equity for you instead of a landlord. That said, ownership comes with a whole host of costs beyond the mortgage itself:

- Property Taxes: An ongoing expense that can—and usually does—go up over time.

- Homeowners Insurance: A non-negotiable recurring cost to protect your asset.

- Maintenance and Repairs: Experts suggest budgeting 1-3% of the home's value every single year for upkeep. Think leaky roofs, broken water heaters, and routine maintenance.

- Utilities and HOA Fees: These can easily add hundreds of dollars to your monthly budget.

An investment property, on the other hand, is all business. The goal here is simple: generate enough rental income to cover the mortgage, taxes, and all other expenses, hopefully leaving you with positive cash flow each month. While it can be a fantastic source of passive income and long-term appreciation, it also means you’re becoming a landlord. That comes with its own set of responsibilities, like managing tenants, handling late-night repair calls, and dealing with potential vacancies.

A Simpler Route: Real Estate Investment Trusts (REITs)

What if you like the idea of real estate returns but not the reality of unclogging toilets? This is where Real Estate Investment Trusts (REITs) come into play. The easiest way to think about a REIT is as a mutual fund for real estate.

REITs let you invest in a whole portfolio of income-producing properties—like apartment complexes, office towers, or shopping malls—just by buying shares on the stock market. You get the benefits of diversification and potential dividend income without ever having to screen a tenant.

This approach is a fantastic way to get real estate exposure in your portfolio while keeping your money liquid. You can buy and sell REIT shares just as easily as any other stock.

Making an Informed Decision

Real estate has long been a go-to for people investing inheritance money, and for good reason. In fact, about 44% of family offices are planning to increase their real estate investments, which signals strong confidence in property as an asset class. This trend really underscores how property, especially alongside other tangible assets, can provide the kind of diversification that modern investment strategies demand. You can dig deeper into these wealth trends in Knight Frank's latest report.

Ultimately, whether you decide to buy a home for yourself, an investment property to rent out, or shares in a REIT, the decision has to be part of your bigger financial plan. Sit down with your financial advisor to analyze the market, calculate the total cost of ownership, and make sure the purchase truly aligns with where you want to be in the long run. A smart, well-timed real estate investment can become a cornerstone of your financial legacy for years to come.

Creating Your Own Legacy and Philanthropic Plan

Receiving an inheritance is a powerful experience. It’s a tangible link to the legacy someone left for you, and it naturally gets you thinking about the legacy you’ll one day leave behind. This moment is the perfect opportunity to dust off your own financial and estate plans, making sure the assets you’ve just received are protected and will pass on according to your wishes.

A common question we hear is what to do with inheritance money to make a real, lasting impact. The first step, surprisingly, is often an internal one: getting your own affairs in order. A significant jump in your net worth means your old will or trust is almost certainly out of date. Updating these documents isn't just a suggestion; it’s an essential move to safeguard these new assets for your own heirs.

Updating Your Estate Plan for New Assets

That inheritance is now part of your estate. Without clear, updated instructions, it could end up being distributed in ways you never would have wanted, creating confusion or conflict down the road. A refreshed plan ensures a smooth transition of wealth to the next generation.

Here are a few key actions to discuss with your estate planning attorney:

- Revise Your Will: This is where you’ll formally document how the inherited assets should be handled.

- Update Beneficiary Designations: Go through all your accounts, especially any new ones, and make sure the correct beneficiaries are named. This simple step can bypass a lot of legal complexity later.

- Consider a Trust: For more complex situations, a trust can offer far greater control over how and when assets are distributed. It can also provide powerful protection from creditors or legal challenges.

Getting these foundational pieces right is the bedrock of any thoughtful legacy. For a deeper dive into this process, you can explore our detailed guide on estate planning for wealthy individuals.

Honoring a Loved One Through Philanthropy

Beyond securing your own family’s future, you might feel a pull to use a portion of the inheritance to make a positive impact—often as a way to honor the person who made the gift possible. Philanthropy is a way to transform financial gain into a meaningful legacy that truly reflects your values.

There are several smart ways to approach charitable giving:

- Direct Donations: The most straightforward path is making a one-time or recurring gift to a charity you care about.

- Donor-Advised Fund (DAF): Think of this as a charitable investment account. You contribute assets, get an immediate tax deduction, and then you can recommend grants from the fund to your favorite charities over time. It’s flexible and powerful.

- Private Foundation: For larger-scale, long-term philanthropy, establishing a private foundation gives you and your family a formal structure to manage your charitable work for generations.

By thoughtfully integrating philanthropy into your financial plan, you can create a lasting tribute that extends far beyond monetary value, turning your inheritance into a powerful force for good.

Your Inheritance Questions, Answered

Even with a solid plan in place, inheriting money brings up a lot of specific questions. Think of this section as a quick reference guide, giving you straightforward answers to some of the most common things people wonder about.

How Long Should I Wait Before Making Big Decisions?

It's tempting to want to put the money to work right away, but financial experts almost universally recommend waiting at least six months to a year before making any major moves.

This "cooling-off" period is absolutely essential. It gives you time to grieve without the added pressure of life-altering financial choices, helping you avoid emotional decisions you might regret later. Use this time to work with your advisory team and build a real plan. While you're figuring things out, the best place for the money is in a secure, liquid account—like a high-yield savings account—where it’s safe and earning some interest.

Will I Have to Pay Taxes on This?

For most people in the United States, the answer is a relieving no. There is no federal inheritance tax. The federal estate tax is a different beast entirely—it’s paid by the estate itself, not you, and only kicks in if the estate's value is above a very high threshold (think many millions of dollars). This affects only a tiny fraction of estates.

However, where you live matters. It's crucial to know that six states currently do have a state-level inheritance tax that you, the beneficiary, are responsible for paying. Those states are Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. The tax rate often depends on your relationship to the person who passed away.

Tax laws are a maze, and they're always subject to change. This is not the place for DIY. Always talk to a qualified tax professional to understand exactly what your obligations are based on your specific situation.

Should I Use the Inheritance to Pay Off My Mortgage?

This is the classic head-versus-heart dilemma. When you run the numbers, the answer often leans toward investing.

Think of it this way: if your mortgage rate is 4% but you could reasonably expect an average return of 7% from a diversified investment portfolio over the long term, you come out ahead by investing. The math is pretty clear on that front.

But—and this is a big but—the emotional weight that lifts when you own your home free and clear is a powerful and perfectly valid reason to pay it off. There’s a real, tangible peace of mind that comes with being completely debt-free. A good financial advisor won't just show you the math; they'll help you weigh that feeling against the potential for greater wealth.

A popular middle-ground approach is to recast your mortgage. You make a significant lump-sum payment to lower your monthly bill and shorten your loan term, then invest the rest. You get a bit of both worlds: a lighter financial load and the growth potential of the market.

Navigating the complexities of a significant inheritance requires experienced guidance. At Commons Capital, we specialize in helping individuals and families create durable financial strategies to protect and grow their wealth. Contact us today to learn how we can help you build your legacy.