Think of your family’s most valuable assets—the vacation home, an investment portfolio, the family business. Right now, they might feel like separate pieces scattered across a table, each managed differently and exposed to its own set of risks. A family limited liability company (FLLC) is what brings all those pieces together, creating a single, protected financial picture.

It’s a specialized version of a standard LLC, but it's built specifically for families who want to protect their wealth and pass it down smoothly through the generations. More than just a legal filing, it’s a powerful tool for building a lasting legacy.

What a Family Limited Liability Company Really Is

An FLLC isn't just a box to hold assets. It’s a strategic framework that separates control from ownership, which is the key to its power. This entire structure is laid out in a critical document called the operating agreement.

The Two Key Roles Inside an FLLC

This dual-role system is what makes the FLLC so effective for succession planning.

- Managing Members: These are typically the senior family members—parents or grandparents—who put the assets into the FLLC in the first place. They might only own a small percentage of the company, but they keep 100% of the voting and management control. They’re the ones calling the shots on buying, selling, or managing everything inside the FLLC.

- Non-Managing Members: This is usually the younger generation—children and grandchildren. They receive ownership shares over time, often as gifts, but they are passive owners. They don’t have a say in the day-to-day decisions, but they get to share in the financial growth of the assets.

This setup ensures that the family members with the most experience continue to steer the ship, even as they begin to hand over ownership to their heirs.

Why It's More Than Just a Business Structure

At its core, a family LLC pulls the best features from different types of legal entities. You get the bulletproof liability protection of a corporation, which means members' personal assets are shielded from the FLLC's debts or any lawsuits that might arise. If a property owned by the FLLC is part of a legal dispute, creditors can't typically come after a family member's personal home or savings.

At the same time, it operates with the tax advantages and flexibility of a partnership. Profits and losses "pass through" to the members, who report them on their personal tax returns. This setup cleverly avoids the double taxation that plagues traditional C-corporations, where the company is taxed first, and then shareholders are taxed again on their dividends.

A well-structured FLLC acts as a financial fortress. It not only safeguards assets from external threats but also establishes a clear, unified governance system that can prevent internal family disputes for decades to come.

Ultimately, creating an FLLC is about building a centralized, protected, and controlled home for your family's wealth. It’s a formal way to teach financial responsibility to the next generation while making sure the assets you’ve worked so hard to build are managed wisely long into the future.

The Core Benefits of an FLLC

Knowing the basic structure of a family limited liability company is one thing, but seeing its real-world advantages is where its true value becomes clear. An FLLC isn't just a box to hold assets; it's a dynamic tool built for the specific, high-stakes goals of preserving and transferring wealth. Its benefits all work together to create a resilient financial legacy.

These advantages are precisely why the family limited liability company is a go-to structure for family enterprises around the world. These businesses are serious economic forces—the top 500 alone generate roughly US$8.8 trillion in revenue, according to a study from EY. The FLLC structure is what helps protect and grow that wealth from one generation to the next.

Let's break down the three core benefits that make the FLLC a cornerstone of modern financial strategy for high-net-worth families.

Superior Asset Protection

Think of your family's assets—real estate, investments, business interests—as a collection of priceless paintings hanging in one big, open gallery. A lawsuit against a single family member could put the entire collection at risk. An FLLC is like putting each painting in its own secure vault, all housed within a single fortified building.

The FLLC creates a legal wall separating the company's assets from the personal liabilities of its members. If a family member faces a lawsuit, divorce, or bankruptcy, their creditors generally can't just seize the assets owned by the FLLC.

Instead, a creditor might only get what's called a "charging order" against that member's interest. This order only entitles them to receive distributions if and when the FLLC's managers decide to make them. Since the managers have full discretion over distributions, this makes the member's interest a very unattractive target for creditors, giving the family a powerful shield.

Strategic Wealth Transfer and Tax Efficiency

One of the most powerful features of an FLLC is how it helps pass wealth to the next generation in a remarkably tax-efficient way. Senior family members can gift ownership shares (the non-managing kind) to their children or grandchildren over time, often taking advantage of the annual gift tax exclusion.

Because these gifted shares are non-managing and aren't easily sold on the open market, they often qualify for valuation discounts. This means the taxable value of the shares can be significantly lower than the actual value of the assets they represent.

This discounting strategy is a game-changer. It allows you to transfer more wealth to your heirs while using up less of your lifetime gift and estate tax exemption. It’s a methodical way to pass down assets without triggering a massive tax bill.

This kind of strategic gifting is a vital piece of the puzzle. This allows you to transfer more wealth while minimizing your gift and estate tax exposure, a key component of comprehensive estate planning for high-net-worth families.

Centralized Management and Control

As a family’s portfolio grows, so does its complexity. Juggling multiple properties, investment accounts, and business interests can get messy and inefficient fast. An FLLC neatly consolidates all these assets under one professionally managed roof.

This structure allows senior members, acting as managers, to keep complete control over all investment and management decisions. They can roll out a unified strategy for the family's entire portfolio, ensuring everything is handled with consistency and a long-term vision. This is especially useful in a few key situations:

- Real Estate Portfolios: Managing a dozen rental properties becomes streamlined when one entity handles all the income, expenses, and maintenance decisions.

- Investment Accounts: A single, cohesive investment strategy can be applied across all assets, rather than trying to coordinate dozens of separate accounts.

- Family Businesses: It provides a crystal-clear line of authority for business operations, heading off potential confusion and conflict among family members.

This centralized control doesn't just protect the assets; it also serves as a training ground. Younger generations get a front-row seat to how major decisions are made, preparing them for future leadership roles while the experienced managers keep the ship steady.

To wrap it all up, let's look at these benefits in a quick summary.

FLLC Benefits At a Glance

The table below summarizes the core advantages a Family Limited Liability Company offers for high-level wealth management and succession planning. Each benefit plays a distinct but complementary role in building a lasting family legacy.

Ultimately, these benefits combine to create a structure that is not only financially sound but also adaptable enough to grow with your family for decades to come.

How to Structure and Govern Your FLLC

A family limited liability company is only as strong as its governing rules. While filing articles of organization with the state is what officially creates the FLLC, the document that truly gives it life, purpose, and staying power is the operating agreement.

Think of this agreement as the constitution for your family's financial enterprise. It’s the single document that dictates every aspect of how the FLLC will function—from day-to-day decisions to long-term succession. Without a well-crafted operating agreement, an FLLC is just an empty legal shell.

Defining Member Roles and Responsibilities

First things first, the operating agreement needs to clearly define who does what. This is where you establish the roles of its members, which are almost always divided into two distinct classes. This split is the very foundation of the FLLC’s ability to centralize control while distributing ownership.

- Managing Members: These are the decision-makers. Usually, they’re the senior family members who contributed the initial assets. They hold the exclusive power to manage, invest, sell, or lease the FLLC’s property. They are the pilots of the financial ship.

- Non-Managing Members: These members are passive owners. This is typically the role for the younger generation. They hold an economic interest in the FLLC's assets and benefit from their growth, but they have no voting rights or say in management decisions.

This two-tiered structure is brilliant because it allows parents or grandparents to maintain complete operational control over the family’s wealth, even after they’ve gifted away a majority of the ownership interests. The operating agreement must spell out these powers and limitations with absolute clarity.

Crafting the Core Provisions of Your Operating Agreement

A comprehensive operating agreement is far more than a simple template you download online. It’s a customized document that has to address the unique dynamics and goals of your family. It needs specific, legally sound provisions that govern the most critical areas of the FLLC’s operation.

Key provisions you absolutely must include are:

- Capital Contributions: This details which assets each member contributed to form the FLLC and their initial ownership percentage.

- Profit and Loss Allocations: Defines how income and losses will be distributed among the members. This can be different from their ownership percentages if structured correctly.

- Distribution Rules: States when and how distributions of cash or assets will be made, giving managers full discretion to retain earnings for reinvestment or other business purposes.

- Management Powers: Explicitly lists the duties and authorities of the managing members.

- Transfer Restrictions: Creates strict "buy-sell" provisions that prevent members from selling or transferring their shares to non-family members without the consent of the managers. This is vital for keeping the assets within the family line.

A robust operating agreement acts as a pre-emptive conflict resolution tool. By addressing sensitive issues like buyouts, divorce, and succession upfront, it provides a clear, legally binding roadmap to navigate future challenges without causing family discord.

The strength of these governance dynamics directly impacts the company’s success. It’s not just theory. Research in the 2025 KPMG Global Family Business Report shows that family enterprises with strong generational entrepreneurial focus—often operating as FLLCs—are 43% more likely to outperform their competitors.

Ultimately, structuring and governing a family limited liability company is a detailed process that demands professional guidance. An experienced attorney can help you draft an operating agreement that not only complies with state law but also reflects your family’s vision, protecting your legacy and ensuring a smooth transition of wealth for years to come.

Steps to Form Your FLLC

Bringing a family limited liability company from concept to reality isn't something you do overnight. It’s a deliberate process that follows a clear path, and while the exact rules can differ a bit from state to state, the core steps are universal. Think of it like building a custom home: you need a solid blueprint and the right team of builders before you even think about laying the foundation.

Getting this process right is absolutely non-negotiable if you want the FLLC to deliver on its promise of asset protection and tax advantages. Cutting corners or rushing through the setup can create serious legal headaches down the road.

Assemble Your Professional Team

The very first move—before a single document is filed—is to get your experts in the room. Forming an FLLC is not a DIY weekend project. It demands a coordinated effort from legal and financial professionals who live and breathe the complexities of estate planning and corporate law.

Your team should include:

- An Estate Planning Attorney: This person is the architect of your FLLC. They'll draft the all-important operating agreement and make sure the entire structure is built to achieve your long-term wealth transfer goals.

- A Certified Public Accountant (CPA): Your CPA is your tax strategist. They will navigate the financial setup, advise on gift tax implications, and ensure the FLLC stays compliant year after year.

- A Financial Advisor: This advisor helps you see the big picture, making sure the FLLC and the assets you place in it align perfectly with your broader investment strategy and financial plan.

Execute the Foundational Legal Steps

With your advisory team in place, you can get down to the brass tacks of creating the legal entity. This is where you establish the company and write the rulebook for how it will operate.

- Select and Register a Name: Your FLLC needs a unique name that isn't already taken in your state. Your attorney will handle the search and file the registration, which usually has to include a tag like "LLC" or "Limited Liability Company."

- File the Articles of Organization: This is the official birth certificate for your FLLC. It's a public document, typically filed with the Secretary of State, that contains basic info like the company’s name, address, and organizers.

- Draft the Operating Agreement: As we've mentioned, this is the most critical document of all. It's the internal constitution that dictates everything—from who has management control and how distributions are handled to the strict rules on transferring ownership. This document is absolutely essential for the FLLC to work as intended.

Fund and Finalize the FLLC

Once the legal shell is built, the final stage is to bring it to life by funding it and setting up its financial plumbing.

Funding the FLLC is the formal process of transferring assets—like real estate, brokerage accounts, or business interests—out of individual family members' names and into the company's name. Meticulous record-keeping here is key to proving the FLLC is the true owner.

After the assets are transferred, you'll tackle the last few administrative tasks:

- Obtain an Employer Identification Number (EIN): You'll need this federal tax ID from the IRS to open bank accounts and file tax returns.

- Open a Dedicated Bank Account: All FLLC money must flow through a bank account held exclusively in the company’s name. Mixing personal and company funds is a cardinal sin that can shatter the FLLC's liability shield.

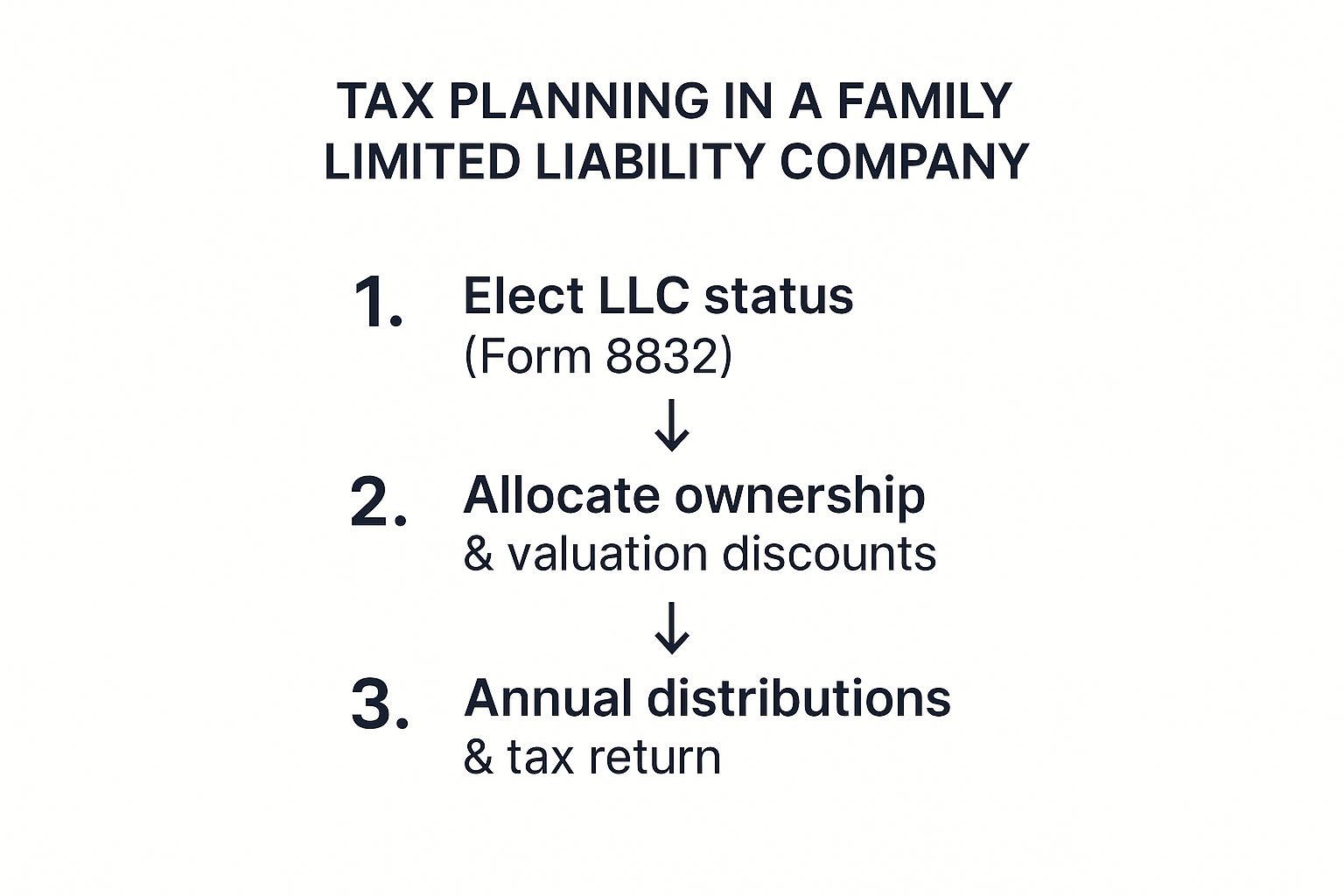

This visual shows a simplified flow for key tax planning decisions within a family limited liability company.

The infographic highlights how foundational tax elections lead to strategic wealth transfer through valuation discounts and culminate in annual financial management. Following these steps diligently with professional guidance ensures your FLLC is built on a solid foundation, ready to serve your family for generations.

Real-World FLLC Use Cases

The theory behind a family limited liability company is one thing, but seeing it in action reveals its true power. High-net-worth families don’t just set up FLLCs for the sake of it; they use them to solve very specific, often complex, challenges tied to managing, protecting, and passing on their wealth.

Let's walk through three common scenarios where an FLLC becomes an indispensable tool, turning abstract legal concepts into tangible, real-world advantages.

Consolidating a Family Real Estate Portfolio

Picture a family that has, over decades, acquired a mix of properties—a vacation home, a few rental units, and maybe a small commercial building. Each asset is owned differently, maybe by individual family members or separate trusts. This creates a messy reality of separate deeds, bank accounts, and decision-making headaches.

An FLLC cuts through that complexity. By transferring all those properties into a single family LLC, the family can instantly streamline its operations.

- Simplified Management: Suddenly, rent collection, maintenance bills, and property taxes all flow through one entity. Bookkeeping becomes clean and straightforward.

- Unified Decision-Making: The designated managing members call the shots. Whether it's renewing a lease or selling a property, there's a clear, consistent strategy for the whole portfolio.

- Liability Protection: This is a big one. If a slip-and-fall happens at one rental property, the lawsuit is contained within the FLLC. Creditors can't go after the other properties in the portfolio or, more importantly, the personal assets of family members.

This centralized structure isn't just about efficiency today. It also makes it far easier to pass ownership to the next generation by simply gifting membership interests in the FLLC.

Managing a Diversified Investment Portfolio

It's common for a family's wealth to be scattered across stocks, bonds, private equity, and other investments held in multiple accounts. Getting all those moving parts to work together toward a common goal can feel like herding cats, especially with several family members involved.

Placing these investments into an FLLC creates a structured framework for professional management. The managing members can now execute a single, unified investment philosophy. Instead of trying to balance a dozen different risk profiles and strategies, the FLLC’s portfolio is managed as a whole to meet the family's long-term financial objectives. It also simplifies gifting—transferring shares of the FLLC is much cleaner than gifting individual blocks of stock.

The FLLC transforms a scattered collection of assets into a single, cohesive family enterprise. This structure is a foundational tool for the growing number of family offices dedicated to preserving multi-generational wealth.

This trend is accelerating. A recent Deloitte report noted a significant rise in single family offices worldwide, estimating around 8,030 in 2024—a 31% jump from 2019. It highlights just how critical sophisticated structures like FLLCs have become for managing complex family fortunes.

Ensuring Smooth Business Succession

For a family-owned business, passing the torch to the next generation is a make-or-break moment. An FLLC offers an elegant way to handle succession, letting senior members gradually transfer ownership without giving up control before they're ready.

Here’s how it works: the senior generation can gift non-managing shares to their children over several years, using tax-efficient strategies to do so. All the while, the seniors remain the managing members, running the business day-to-day and mentoring their successors. This process ensures stability and properly prepares the next generation for leadership. Our expert family office services are designed to help structure these kinds of complex, long-term plans.

By the time the founders are ready to retire, a huge chunk of the business ownership may have already been transferred, smoothing the transition and dramatically reducing potential estate tax burdens. It's a strategic, patient approach that avoids the kind of abrupt change that can derail an otherwise successful family business.

Avoiding Common Risks and Pitfalls

A family limited liability company can be a powerful fortress for your wealth, but its protections aren't automatic. Real success hinges on diligent management and a clear-eyed view of the potential challenges. If you aren't proactive, that fortress you're trying to build could end up being little more than a house of cards.

One of the quickest ways to undermine an FLLC is to ignore corporate formalities. Simply forming the company isn't enough; you have to operate it as a separate legal entity. That means maintaining separate bank accounts, keeping meticulous financial records, and holding regular meetings with documented minutes.

When you blur the lines, you give creditors an opening to argue the FLLC is just an extension of your personal finances. If a court agrees, it could "pierce the corporate veil," leaving the very assets you wanted to shield completely vulnerable to claims.

Navigating IRS Scrutiny

Let's be honest: the tax advantages of a family limited liability company are a huge draw, especially the valuation discounts on gifted shares. But this is exactly what puts FLLCs on the IRS's radar. The agency scrutinizes these structures to make sure they have a legitimate business purpose beyond simply dodging taxes.

To stand up to that scrutiny, you have to do things by the book:

- Get Professional Appraisals: Never guess the value of your assets or the right discount. You need a qualified, independent appraiser to determine the fair market value of both the FLLC’s assets and the gifted shares.

- Document Everything: Keep crystal-clear records showing a legitimate, non-tax reason for creating the FLLC. This could be anything from centralizing management to liability protection.

- Have a Real Business Purpose: The FLLC needs to be more than a passive holding company. It should actively manage its assets, which helps prove it’s a genuine business entity and not just a tax-saving shell.

The IRS has a history of successfully challenging FLLCs that were thrown together hastily, especially when formed right before a death. Cases like Estate of Powell v. Commissioner are a stark reminder that courts will disregard structures that look like a last-ditch effort to slash estate taxes.

Preventing Internal Family Conflicts

An FLLC can be a fantastic tool for uniting a family around shared financial goals, but it can just as easily become a source of bitter conflict if you're not careful. The operating agreement is the bedrock of the entire structure, and it needs to be crafted with real foresight to head off potential arguments before they ever start.

Think about it. What happens when a younger family member wants to cash out their shares? Or when a major disagreement over an investment paralyzes decision-making? A vague or incomplete agreement leaves you with no roadmap, paving the way for disputes that can damage family relationships for years.

A well-written agreement provides a clear, legally binding process for handling these exact scenarios. By addressing these issues upfront, the operating agreement is transformed from a potential landmine into a tool for family harmony.

A Few Common Questions About FLLCs

As you explore whether a family limited liability company is right for you, a few questions almost always come up. Here are some straightforward answers to the inquiries we hear most often.

What's the Real Difference Between an FLLC and a Trust?

While they both live in the world of estate planning, an FLLC and a trust are built for different jobs. Think of an FLLC as a family-owned business designed for actively managing assets and transferring wealth with control and liability protection. A trust, on the other hand, is a legal agreement where a trustee holds assets for beneficiaries, following a specific set of instructions you lay out.

The good news is, you don't have to choose. They often work best as a team. It's quite common for a family trust to be a member of the FLLC, giving you the asset protection of the company and the clear succession plan of the trust, all in one strategy.

An FLLC is a tool for consolidating, protecting, and managing assets with a business-like structure. A trust is a tool for dictating exactly how and when those assets are distributed to heirs over time.

What's the Investment to Set Up and Maintain an FLLC?

The costs generally break down into two phases.

- Initial Setup: This is where the bulk of the investment happens. You're not just filing paperwork; you're creating a foundational legal document for your family's wealth. Legal fees for a well-drafted, customized operating agreement and state filings can start at a few thousand dollars and go up to $10,000 or more, depending on how complex your assets and family dynamics are.

- Ongoing Maintenance: After the setup, the annual costs are much more manageable. You'll typically have modest state filing fees, accounting costs for tax preparation, and possibly fees for professional appraisals if you're gifting shares to family members.

Should I Put My House in an FLLC?

This is a common question, and the answer is almost always a firm no. Putting your personal home into an FLLC is generally not recommended because it can backfire from a tax perspective.

The biggest issue is the potential loss of the capital gains exclusion on the sale of a primary residence. This is a huge tax benefit that lets individuals exclude up to $250,000 of profit (or $500,000 for married couples) when they sell their main home. Once you transfer the house to an FLLC, you typically lose your eligibility for this tax break. For this reason, your personal residence should almost always stay separate from the business and investment assets you place inside the FLLC.

At Commons Capital, we specialize in helping high-net-worth families navigate these complex financial structures to build and preserve their legacies. If you're ready to explore how a tailored strategy can work for you, visit us at our website.