The choice between a pension lump sum or an annuity is a critical financial crossroad, often boiling down to a classic dilemma: control versus certainty. Taking the lump sum puts you in the driver's seat, offering total control and flexibility over your retirement investments. An annuity, on the other hand, provides a guaranteed, predictable income stream for life. This guide will help you understand the nuances of this decision, whether you'd rather manage your own capital or lock in a lifelong paycheck.

The Critical Choice: Pension Lump Sum Or Annuity

Deciding how to receive your pension is one of the most significant financial moves you will ever make, fundamentally shaping your retirement lifestyle and the legacy you leave behind. For high-net-worth individuals, the stakes are even higher, as this decision intersects with complex investment strategies, tax planning, and estate considerations. Understanding the core trade-offs is the first step toward making an informed choice.

When facing a financial decision of this magnitude, using essential decision making frameworks can help structure your thinking and evaluate each option objectively. This isn't just about crunching numbers; it’s about ensuring the financial mechanics align with your long-term life goals.

Comparing The Core Concepts

At its heart, you are choosing between two distinct financial philosophies. One path makes you the chief investment officer of your own retirement portfolio. The other provides a clear, predetermined road map with no surprises.

Let’s break down the foundational differences in a simple, side-by-side comparison. This will clarify what makes each option unique before we dive into deeper strategic implications. To learn more about securing your financial future, explore our insights on creating guaranteed retirement income.

How Each Pension Option Actually Works

Before you can decide between a pension lump sum or an annuity, it's crucial to understand their operational mechanics. Each choice comes with its own set of rules that will shape your control, tax obligations, and overall financial freedom. These are not minor details — they fundamentally define the future of your retirement assets.

Opting for the pension lump sum is like being handed the keys to your entire retirement savings. Instead of taking the cash directly — a move that would trigger a significant tax bill — the standard strategy is a direct rollover into an Individual Retirement Account (IRA). This is a critical step. It preserves the tax-deferred status of your money, allowing it to remain invested and grow without an immediate reduction from taxes.

Once the funds are in your IRA, you are in complete control. You and your financial advisor can construct a portfolio that matches your specific goals, whether you’re aiming for aggressive growth, capital preservation, or a balanced approach.

The Annuity: A Stream Of Guaranteed Payments

An annuity, conversely, is a completely different financial instrument. It converts your accumulated pension benefit into a steady, predictable income stream for life. You are essentially trading your large sum of capital for a contractual promise from an insurance company to send you a regular check. This process is called annuitization, and it shifts the risk of outliving your money from your shoulders to the provider.

The monthly payment you receive isn't an arbitrary number. It is a calculated figure based on several key factors, including your life expectancy, the specific type of annuity you select, and the prevailing interest rate environment.

The core trade-off is clear: an annuity provides peace of mind with guaranteed income, while a lump sum offers the autonomy to manage your own financial future. Neither is inherently better; the right choice depends entirely on your personal financial situation and retirement vision.

Let's review the fundamental differences side-by-side.

Core Differences Between Lump Sum And Annuity

This table encapsulates the decision: one path offers control and flexibility, while the other provides security and predictability.

Understanding The Calculations And Options

The size of your lump sum is calculated using a commutation factor, which determines the present-day value of all your future annuity payments. This calculation is highly sensitive to interest rates published by the IRS. When rates are low, lump sum values are higher. Conversely, when rates rise, the value of the lump sum tends to decrease.

With an annuity, you must also make important structural choices that will affect your payment amount and what, if anything, is left for your family.

- Single-Life Annuity: This option provides the highest possible monthly payment, but payments cease upon your death. It is designed purely to provide income for one person's lifetime.

- Joint and Survivor Annuity: This provides income for your lifetime and then continues to pay a portion (often 50% or 100%) to your surviving spouse. This spousal protection comes at the cost of a lower initial monthly payment.

Ultimately, the choice between a lump sum or an annuity comes down to these mechanics. One gives you a checkbook to manage your future, while the other provides a paycheck you cannot outlive.

Strategic Comparison For Affluent Retirees

Deciding between a pension lump sum or an annuity requires more than a surface-level comparison. For affluent retirees, this choice is a strategic one, hinging on how each option performs under various financial pressures. We must analyze these choices through four critical lenses: investment control, risk management, tax efficiency, and estate planning.

This is not about finding a single "better" option for everyone. It is about identifying the superior fit for your specific financial architecture and long-term objectives. Every element presents a trade-off that must be weighed carefully.

Investment Control and Growth Potential

The most significant difference between taking a lump sum versus an annuity is the control you retain over your capital.

When you take a lump sum and roll it into an IRA, you are in complete control. You become the architect of your investment strategy. This freedom allows you to build a diversified portfolio shaped by your growth goals and risk tolerance, opening up the potential for returns that can significantly outpace inflation.

An annuity, on the other hand, is built on a simple premise: you relinquish control for a guaranteed income stream. Once you annuitize, the insurance company manages the capital. Your focus shifts from growing your assets to securing a stable income. The opportunity for market-driven growth is exchanged for peace of mind.

Strategic Differentiator: The lump sum maintains your pension assets as a dynamic tool for wealth creation. The annuity transforms those same assets into a passive income generator, prioritizing security over growth potential.

This preference for flexibility is reflected in broader market trends. According to 2023 BLS data, lump sums were available to over 70% of participants in defined contribution savings and thrift plans, compared to the 12% who had an annuity option. This indicates a clear preference among retirees for moving funds into personalized portfolios. Fidelity offers a more detailed analysis on these lump sum vs. annuity preferences.

Navigating Risk Management

Each path comes with a distinct risk profile, and your choice reflects your retirement philosophy.

A lump sum portfolio is directly exposed to market risk and sequence-of-returns risk. A major market downturn early in retirement can permanently impair the portfolio's ability to provide income, forcing you to sell assets at a loss.

Conversely, an annuity is designed to insulate you from these very risks. It acts as a shield against market volatility and the fear of outliving your money, often called longevity risk. However, it introduces other concerns, most notably inflation risk. A fixed payment that seems adequate today can see its purchasing power erode over a 20 or 30-year retirement.

- Lump Sum Risk Profile: You actively manage market, inflation, and sequence risks.

- Annuity Risk Profile: You transfer market and longevity risk to an insurer but assume inflation and opportunity cost risk.

Optimizing For Tax Efficiency

The tax implications for each option are profoundly different and create unique planning opportunities, especially for high-net-worth investors.

Annuity payments are taxed as ordinary income upon receipt. It is straightforward but offers little room for strategic maneuvering, resulting in a predictable annual tax bill.

A lump sum rolled into an IRA, however, opens up a much more dynamic tax-planning landscape.

- Withdrawal Control: You can manage your annual withdrawals to stay within desired tax brackets.

- Roth Conversions: You have the flexibility to strategically convert parts of your traditional IRA to a Roth IRA, paying taxes now for tax-free growth and withdrawals later.

- Tax-Loss Harvesting: You can use investment losses to offset capital gains, reducing your overall tax burden.

This level of control allows for sophisticated tax strategies that are not available with a standard annuity.

Estate Planning and Legacy Goals

For many affluent individuals, passing wealth to the next generation is a primary objective. In this regard, the two options could not be more different.

With a lump sum, any funds remaining in your IRA upon your death pass directly to your named beneficiaries. It's a straightforward and often substantial legacy, allowing your heirs to continue growing the capital. While inherited IRAs have their own distribution rules, the core asset remains intact to be passed on.

Most single-life annuities, however, leave little to nothing for heirs. Payments cease when the annuitant dies, and the insurance company retains the remaining capital. Options like joint-and-survivor or period-certain annuities can provide for beneficiaries, but they come at the cost of a smaller monthly payment during your lifetime. For those focused on a robust legacy, the lump sum is almost always the more aligned choice.

Modeling The Financial Outcomes And Breakeven Points

Abstract comparisons are helpful, but the decision between a pension lump sum or annuity becomes clearer when you analyze the numbers. It’s about translating financial theory into concrete projections to see the tangible, long-term impact of each choice. This is where we move beyond concepts to calculate the performance thresholds and breakeven points that define success for each path.

By modeling detailed scenarios, we can see how each option performs under different conditions — from living longer than expected to navigating market volatility. These models provide a clear, data-driven framework for understanding the financial trade-offs you face.

The Breakeven Analysis: A Core Calculation

A central question for anyone considering a lump sum is: what investment return is needed to outperform the guaranteed income from the annuity? This is the breakeven point, and calculating it is a critical first step.

Let's say you are 65 and have a choice: a $300,000 lump sum or a $1,470 monthly annuity ($17,640 per year). At first glance, that guaranteed monthly check seems secure, eliminating the fear of outliving your money.

However, a closer look reveals the lump sum's potential. If you live for another 18 years, the total annuity payments amount to $317,520. This represents a minimal 0.6% annual return on the initial $300,000. As Schwab highlights in its analysis of the lump sum versus annuity debate, you could simply store the $300,000, withdraw $17,640 annually, and it would last over 17 years. The performance bar is surprisingly low.

Key Takeaway: The breakeven return is often much lower than anticipated. For many high-net-worth individuals with a well-managed portfolio, achieving a modest annual return that surpasses the annuity's implied rate is an attainable goal.

Simulating A Market Downturn Scenario

One of the strongest arguments against a lump sum is the risk of a market crash early in retirement. This is where sequence-of-returns risk becomes a real threat, as withdrawing from a declining portfolio can cripple its ability to recover. This scenario highlights the annuity's primary strength: stability.

Imagine two retirees, each with a $1 million pension benefit.

- Retiree A (Lump Sum): Takes the $1 million and invests it. The market drops 20% in their first year of retirement, and they withdraw $40,000 for living expenses. Their portfolio is now valued at approximately $760,000.

- Retiree B (Annuity): Annuitizes the $1 million and receives a guaranteed annual income of $50,000 for life. The market crash has zero impact on their income stream.

This simulation makes the annuity's value as a market buffer clear. While Retiree A still has a large portfolio with growth potential, they are starting retirement at a significant disadvantage. Retiree B, in contrast, enjoys complete income predictability. It's vital to understand this risk; you can learn more about managing sequence of returns risk in retirement planning to protect your assets.

Long-Term Projections Across Different Lifespans

The breakeven point is not static; it shifts based on your lifespan. The longer you live, the more payments you collect from an annuity, which can dramatically tilt the scales in its favor.

Let's model this with a $500,000 lump sum versus a $30,000 annual annuity.

This table tells a compelling story. If you live only to age 80, the lump sum is the clear winner. However, if you live to 95, your lump sum portfolio needs to average a consistent 4.3% annual return just to match the annuity's total payout. This is why annuities are often called longevity insurance; their true value is realized over very long time horizons.

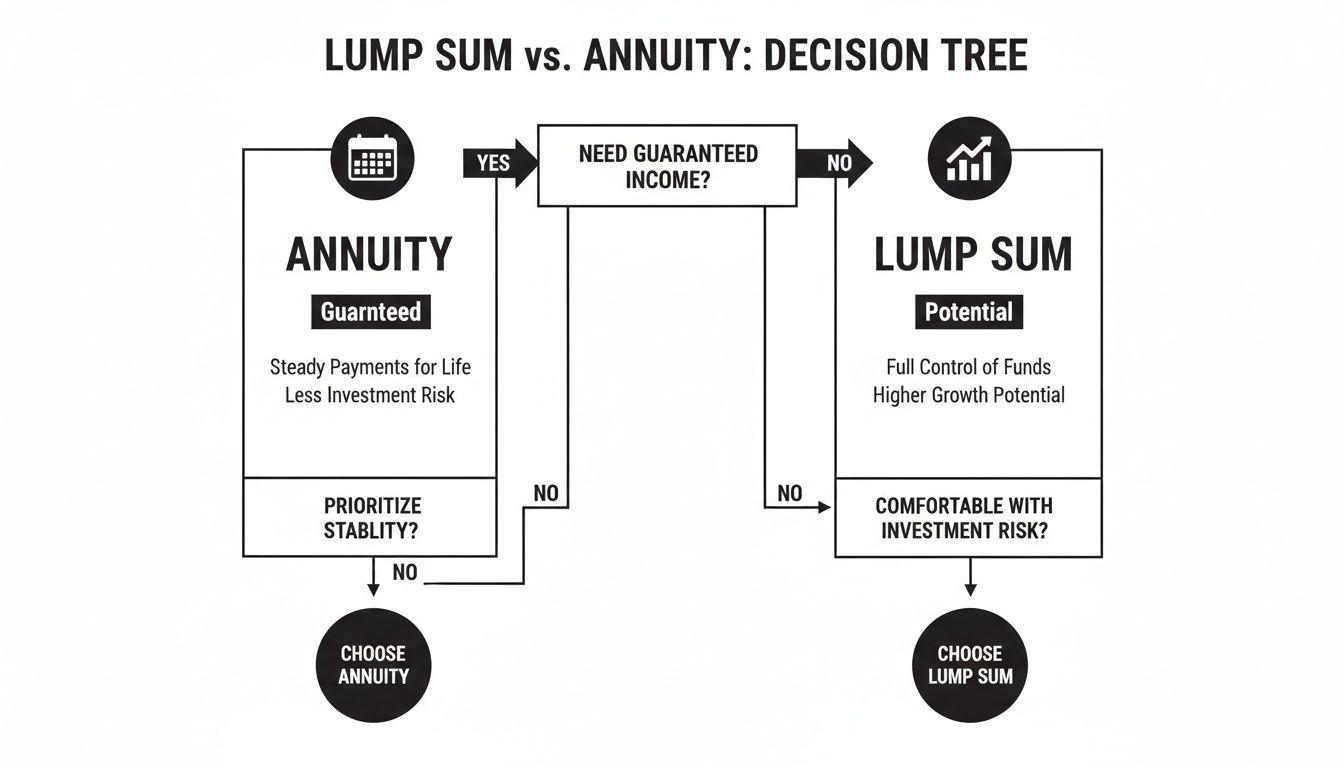

Which Option Fits Your Retirement Profile

The choice between a pension lump sum or an annuity is not just a financial calculation; it is a deeply personal decision. There is no one-size-fits-all answer. The right move depends on your specific financial DNA — your goals, risk tolerance, and vision for the future.

To determine the best fit, let's examine a few distinct profiles of high-net-worth individuals. Seeing how different life objectives align with these pension strategies can make the decision much clearer.

This decision tree provides a quick visual guide, outlining the core trade-off: guaranteed income versus investment potential.

As illustrated, the decision boils down to your priorities. An annuity secures a predictable income floor, while a lump sum opens the door for greater growth and legacy building.

The Legacy Builder

For individuals whose primary goal is to maximize the wealth they pass on, the lump sum is almost always the superior choice. Their main objective is preserving and growing capital for their heirs, a mission for which most annuities are not designed.

By taking a lump sum and rolling it into an IRA, you maintain complete control over the asset. That capital can be invested in a diversified, growth-oriented portfolio. Upon your death, the remaining balance can pass directly to your beneficiaries, becoming a cornerstone of their financial future. A single-life annuity, in contrast, typically offers zero legacy value — payments simply cease.

Strategic Recommendation: The Legacy Builder should strongly favor the lump sum. It aligns perfectly with wealth preservation and transfer, providing the flexibility to create a lasting financial legacy that an annuity cannot match.

The Conservative Retiree

This profile prioritizes security above all else. The greatest fear is outliving their savings, and the main goal is to establish a reliable, lifelong income stream that covers all essential expenses. For this individual, market volatility is a source of stress, not opportunity.

An annuity is engineered for this exact scenario. It converts your pension into a series of guaranteed payments for life, creating a personal paycheck that will never run out. This predictability provides incredible peace of mind, shielding you from market fluctuations and the complexities of managing a large portfolio.

- Priority: Income security and longevity protection.

- Risk Tolerance: Very low; prefers certainty over potential growth.

- Best Fit: An annuity, likely a joint-and-survivor option if married, to ensure a spouse is also protected.

Strategic Recommendation: The Conservative Retiree should lean heavily toward annuitization. The guaranteed income provides the financial stability and risk mitigation that aligns perfectly with their desire for a worry-free retirement.

The Entrepreneurial Investor

This individual may be leaving their primary career, but they are far from done. They remain actively engaged in business or new investment ventures and may need capital to launch a new company, invest in real estate, or manage a business succession. For them, liquidity and control are paramount.

An annuity would be highly restrictive in this case, locking up capital that could be deployed in higher-return opportunities. The lump sum, on the other hand, provides a substantial pool of liquid assets. Once rolled into an IRA, those funds can be managed to support entrepreneurial goals, though withdrawals are still subject to standard IRA rules and taxes.

Strategic Recommendation: The Entrepreneurial Investor needs the flexibility and control that only a lump sum can offer. This option delivers the capital required to pursue new ventures and sophisticated investment strategies, making it the clear choice for anyone who views retirement as a new chapter of financial activity.

Using a Hybrid Strategy for the Best of Both Worlds

The choice between a pension lump sum or annuity does not have to be an all-or-nothing decision. For many high-net-worth individuals, a more sophisticated approach is a hybrid strategy that combines the best features of both. This allows you to secure guaranteed income while retaining the growth potential and control that a lump sum offers.

At its core, this strategy involves creating a reliable "income floor" for your retirement. The idea is to use a portion of your pension assets to generate a guaranteed income stream that covers all your essential living expenses, such as mortgage payments, utilities, healthcare premiums, and property taxes.

Building Your Income Floor

You can construct this foundational income layer by combining your Social Security benefits with an annuity. This creates a bedrock of predictable cash flow that is not dependent on market performance, effectively shielding your essential lifestyle from volatility.

Your employer's pension annuity offer is often a good starting point. In my experience, over 80% of the time, a company's lifetime income quote is more generous than what is available from private insurers. When paired with Social Security, this builds a guaranteed floor that markets cannot affect, freeing up your remaining capital to be invested for growth.

With your essential expenses covered, the rest of your pension can be taken as a lump sum and rolled over into a diversified IRA. This is where your portfolio becomes a "growth engine."

A hybrid strategy changes the question from "which one is better?" to "how can I use both to my advantage?" It is about segmenting your assets to match different goals — security for needs and growth for wants.

The Growth and Flexibility Component

This lump sum portfolio is where you can pursue higher returns, protect against long-term inflation, and plan your legacy. Since the income floor covers your basic needs, you can afford to take on more calculated investment risk with this capital. This structure also provides a psychological cushion, making it easier to remain invested during market downturns.

- Upside Potential: An invested lump sum has the potential to grow significantly over a long retirement.

- Inflation Hedge: Equities and other growth-oriented assets in the portfolio provide a natural defense against the rising cost of living.

- Legacy Planning: Any funds remaining in the IRA can be passed directly to your heirs, often in a more tax-efficient manner.

- Flexibility: This pool of capital is available for large, unplanned expenses or discretionary goals like travel or assisting family.

This balanced model mitigates the primary weaknesses of choosing either option alone. You get the downside protection of an annuity while retaining the significant upside potential and control of a lump sum. For a deeper dive into managing portfolio withdrawals, you can explore various retirement withdrawal strategies.

Answering Your Key Pension Questions

Even after weighing the pros and cons, specific questions often arise when facing the choice between a pension lump sum or an annuity. Let's address some of the most critical ones that high-net-worth individuals frequently ask.

How Do Rising Interest Rates Affect My Decision?

When interest rates go up, the present value of your future pension payments typically goes down. This often results in a smaller lump-sum offer from your employer.

However, there is another side to this. Higher rates mean private market annuities can offer a larger monthly payment for the same amount of capital. It is crucial to compare your employer's annuity offer with what you could purchase on the open market with your lump sum. Your company's pension calculation might be using older, lower rates, potentially making a private annuity a better deal.

What Is The Role Of The Pension Benefit Guaranty Corporation?

The Pension Benefit Guaranty Corporation (PBGC) is a federal agency that acts as an insurer for private-sector defined-benefit pensions, similar to how the FDIC insures bank deposits. If your company’s pension plan fails, the PBGC steps in and guarantees your annuity payments up to a legal maximum. It provides a significant safety net.

A lump sum rolled into an IRA is not covered by the PBGC. Instead, it falls under SIPC protection, which insures against brokerage failure (up to $500,000), not against investment losses.

Can I Take A Partial Lump Sum?

This depends entirely on your specific plan's rules. Some modern plans offer this flexibility, but many traditional defined-benefit pensions are an all-or-nothing proposition.

If your plan does not allow it, you can often create a similar outcome. By taking the full lump sum and rolling it into an IRA, you can then use a portion of those funds to purchase a private annuity. This effectively allows you to build your own customized, guaranteed income floor while keeping the remainder invested.

Beyond these choices, remember that external life events can significantly impact your benefits. For instance, it’s essential to understand the implications of major life changes, such as what happens to your law enforcement pension if you get divorced in Florida, as part of your comprehensive planning.

Making the right decision requires guidance from a professional who understands your unique financial situation. At Commons Capital, we specialize in helping high-net-worth individuals navigate these complex choices to build a secure and prosperous retirement. Contact us today to create your personalized financial strategy.