Picture this: a reliable paycheck landing in your bank account every single month for the rest of your life, no matter what the stock market is doing. That’s the simple, powerful promise behind guaranteed retirement income, a strategy designed to deliver true financial stability and peace of mind when you need it most.

Think of it as creating your own personal pension, one that ensures your most essential expenses are always covered. This guide provides a comprehensive answer to creating a reliable income stream for a secure retirement.

Why Guaranteed Income Is a Modern Retirement Essential

Not too long ago, many workers could count on a company pension to provide a steady income after they hung up their hats. That world has all but vanished. The dramatic shift away from traditional pensions has left a massive gap, creating a deep sense of anxiety for millions of Americans as they approach their post-work years.

This is exactly the problem that a guaranteed retirement income strategy is built to solve.

Imagine building a solid floor for your retirement finances. This floor covers all your non-negotiable costs—your mortgage, healthcare, utilities, and groceries—with a predictable, recurring payment. Once that foundation is secure, the rest of your savings can be used for the fun stuff like travel or invested for growth, all without the constant, nagging fear of running out of money.

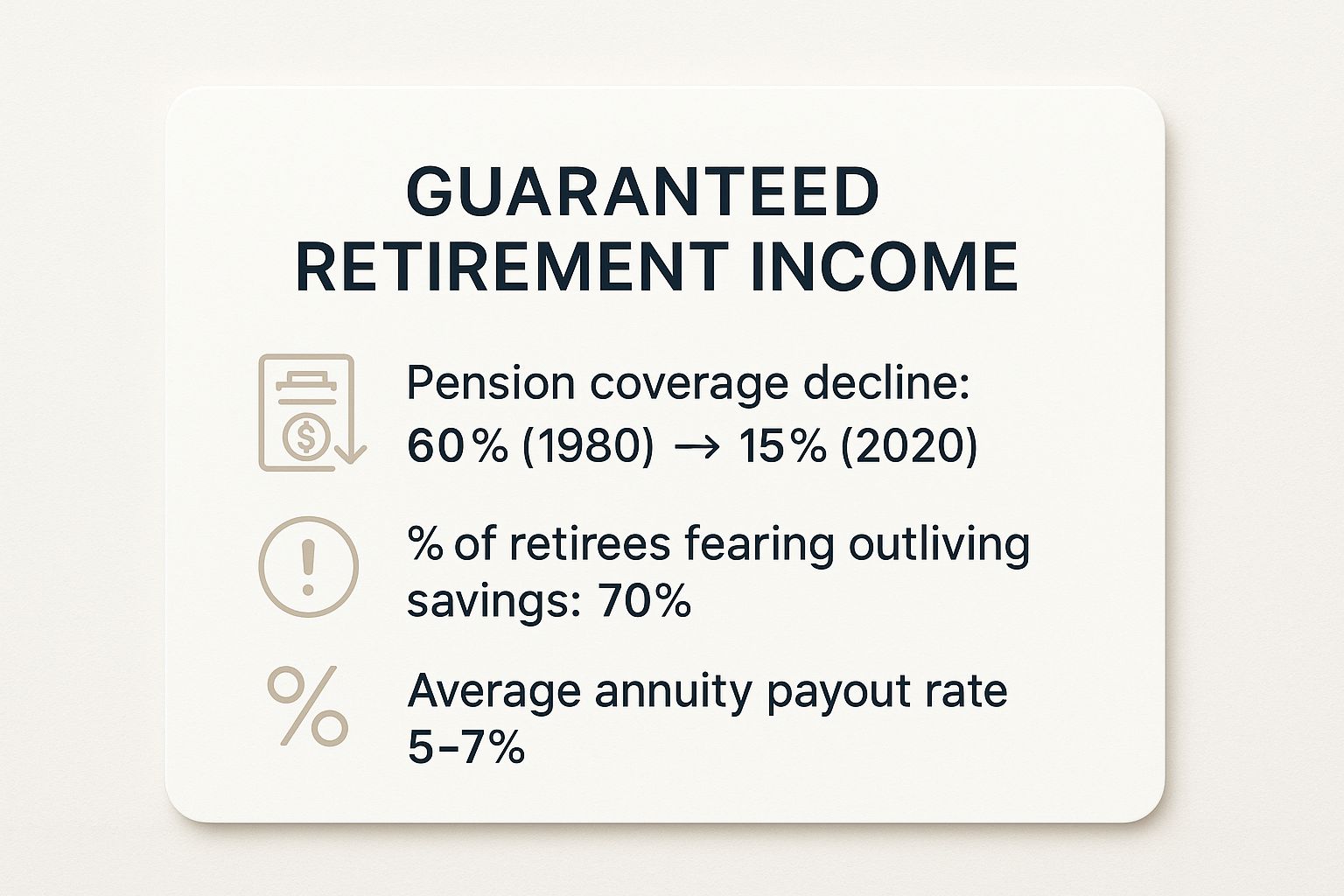

This infographic really captures the modern retirement dilemma: pensions are disappearing, fear is rising, and guaranteed income solutions are stepping in to fill the void.

The data tells a clear story. As the safety net of traditional pensions frays, the fear of outliving savings grows, making these income solutions more critical than ever.

The Growing Need for Financial Security

With people living longer and market volatility feeling like a constant threat, the demand for reliable income streams has surged. Projections show that by 2025, nearly 50% of households nearing retirement may not be able to maintain their standard of living, a direct result of the pension decline.

While annuities are a primary tool for creating this security, a surprising number of people admit they don’t fully understand how they work. Credible sources like The Alliance for Lifetime Income offer great insights into this challenge.

A guaranteed income stream is not just a financial product; it's a psychological safety net. It transforms retirement from a period of financial uncertainty into a time of freedom and confidence.

Learning how to build this security is a critical part of navigating the different phases of retirement. It all comes down to a smart plan for turning a portion of your nest egg into a reliable income source you can count on for decades to come. We’ll dig into the specific tools that make this happen, like annuities, in the sections ahead.

Exploring Your Guaranteed Income Options

When it's time to create a reliable, lifelong income stream, you need to choose the right financial tools for the job. While pillars like pensions and Social Security often form a crucial base, annuities are the main way most people build their own private source of guaranteed retirement income.

Think of an annuity as a personal pension you set up with an insurance company. You give them a lump sum or a series of payments, and in return, they contractually agree to send you a steady paycheck for a set period—often, for the rest of your life.

But not all annuities are created equal. They come in several different flavors, each designed for different needs and comfort levels with risk. Getting to know these core types is the first step toward building the secure future you want.

The Main Types of Annuities

The world of annuities can seem a little complicated at first, but most products fall into one of three main buckets. Each one strikes a different balance between safety, growth potential, and pure predictability. Let’s break them down.

- Fixed Annuities: This is the most straightforward option you'll find. A fixed annuity works a lot like a certificate of deposit (CD) from a bank, offering a guaranteed interest rate for a specific term. Its biggest advantage is absolute predictability. You know exactly how much your money will grow and what your future payments will be, making it a powerful tool for conservative planners. While incredibly safe, their returns are often modest, similar to other low-risk products. For more on stable assets, check out our guide on whether municipal bonds are a good investment.

- Variable Annuities: If a fixed annuity is like a CD, a variable annuity is more like a 401(k). Your money is invested in a menu of sub-accounts, which are essentially mutual funds. This structure gives you the highest potential for growth, but it also comes with market risk. Your account value—and your future income—will rise and fall with the performance of your chosen investments.

- Fixed-Indexed Annuities (FIAs): This hybrid option tries to give you the best of both worlds. An FIA links its returns to a market index, like the S&P 500, giving you a shot at growth. However, it also includes a feature that protects your principal from market downturns. You get to participate in some of the market's upside while enjoying protection against loss, making it a very popular middle-ground choice.

The core decision in choosing an annuity really boils down to one question: How much risk are you willing to take in exchange for the potential of higher returns? Your answer will point you toward the right product for your plan.

For those with significant assets, exploring specialized insurance for high net worth individuals can unlock advanced strategies for income and asset protection that go beyond these standard options.

Comparing Your Annuity Choices

To make the decision a bit clearer, it helps to see how these three annuity types stack up against each other. This table breaks down the key features of fixed, variable, and indexed annuities to help you understand which one best fits your retirement strategy.

As you can see, each path offers a distinct way to secure income in retirement. By understanding these mechanics, you can better align your choice with your personal financial goals and build a foundation for a worry-free future.

The True Value of a Lifelong Paycheck

Securing a guaranteed retirement income provides something that goes far beyond the numbers on a spreadsheet. It delivers a powerful, intangible asset: genuine peace of mind. When you know for a fact that your essential monthly expenses will be covered, no matter what, your entire approach to retirement changes.

This financial bedrock acts as a psychological buffer against market chaos. Instead of watching every dip in the stock market with a knot in your stomach, you can start to see volatility for what it is—an opportunity for your other investments, not a direct threat to your survival.

That stability creates a powerful ripple effect, fundamentally changing how you can manage the rest of your portfolio.

Investing with Renewed Confidence

Once your core living costs are handled by a predictable stream of income, it completely frees up your other assets. Capital that was once on the defensive, held back just in case, can now be put to work for growth. This is a fundamental shift in mindset, moving from preservation to potential.

Picture a retired couple whose guaranteed income easily covers their mortgage, utilities, and healthcare bills. They can now invest their remaining savings more aggressively in equities or other growth-focused assets, knowing a market downturn won’t force them to sell at the worst possible time just to keep the lights on.

This strategy empowers them to chase higher returns, fight back against inflation, and ultimately build a more substantial legacy.

The Freedom to Truly Live

At the end of the day, the real value of a lifelong paycheck is the freedom it unlocks. It’s the ability to travel, dive into a new hobby, or simply spend more time with family without that nagging, constant worry about outliving your savings.

This is the crucial difference between merely existing in retirement and truly living it.

A guaranteed income stream is not just about paying bills; it's about buying freedom. It removes the biggest source of financial stress—the fear of the unknown—and replaces it with confidence and security.

This sense of security is becoming more critical as the retirement savings gap widens. A recent survey revealed that 74% of younger workers struggle to save for retirement due to competing financial priorities. If trends continue, nearly 65% of US workers could be living paycheck to paycheck by 2043, making retirement increasingly difficult. You can explore more about these trends in the Goldman Sachs Asset Management 2025 Retirement Survey.

By creating a stable income floor, you aren't just managing your finances. You're designing a better quality of life for your future self.

Navigating the Risks and Tradeoffs

While the peace of mind that comes with a guaranteed retirement income is a powerful motivator, it’s crucial to understand that no financial product is a magic bullet. These products always involve specific tradeoffs, and recognizing them is the key to making a smart decision.

Think of it as paying a premium for income insurance. You are transferring risk to an insurance company, and that service absolutely has a cost. Before you commit, you have to look at the full picture—the good and the bad—to weigh the price of security against its very real advantages.

The Impact of Inflation Over Time

One of the biggest risks to any fixed income stream is inflation. That’s the silent killer of purchasing power. A monthly payment that feels comfortable today might feel painfully tight in 15 or 20 years as the cost of living climbs.

A fixed payment of $2,000 per month has significantly less buying power after two decades of even modest inflation. This erosion is a critical factor to consider. Thankfully, many modern annuities offer riders or features that can help your income keep pace.

- Cost-of-Living Adjustments (COLAs): You can often add a rider that increases your payments annually, typically by a fixed percentage like 2% or 3%.

- Inflation-Adjusted Payouts: Some products can link your income to an inflation index, like the Consumer Price Index (CPI), giving you a more direct hedge.

Opting for these features will mean your initial payments are lower, but they offer invaluable long-term protection against rising costs. The choice really comes down to how much you prioritize immediate income versus future purchasing power.

Understanding Fees and Liquidity Constraints

Guaranteed income products, particularly annuities, are not free. They come with costs that compensate the insurance company for taking on the risk that you’ll live a very long time. These can include administrative fees, mortality and expense charges, and fees for any optional riders you add. It's vital to get a crystal-clear breakdown of all costs before you sign anything.

The other key tradeoff is liquidity. When you purchase an immediate annuity, you are typically exchanging a lump sum of capital for that future income stream. This means you lose easy access to that principal.

The core tradeoff is often security for liquidity. You are giving up direct control over a portion of your capital in exchange for the certainty that you cannot outlive that income.

For this exact reason, it's almost never a good idea to put all your assets into an annuity. Maintaining a separate, liquid pool of funds for emergencies or large, unexpected expenses is a cornerstone of any balanced retirement plan. It's also important to be aware of how different assets are treated; for instance, you can learn more about if IRAs are protected from creditors in our detailed guide.

How to Build Your Guaranteed Income Plan

Moving from theory to action is where your retirement security really begins to take shape. Creating a durable income plan isn't about guesswork; it’s a deliberate process of matching your most essential needs with income sources you can count on, no matter what the market is doing.

The goal is to build a financial foundation so solid that you can sleep well at night, confident that your core expenses are covered for life.

Calculate Your Essential Income Needs

The first step is a simple but powerful exercise: figuring out your essential, non-negotiable monthly expenses. This isn't your entire budget—it's the absolute bare minimum you need to live on. Think of it as your "financial floor."

To get a clear target for your guaranteed income, you have to separate your needs from your wants. This distinction is the bedrock of a solid plan.

- Essential Expenses (Needs): These are the bills that absolutely must be paid every single month. This includes your mortgage or rent, utilities, property taxes, insurance premiums, healthcare costs, and groceries.

- Discretionary Expenses (Wants): This bucket covers everything else—the fun stuff. Think travel, dining out, hobbies, entertainment, and gifts for family.

Once you’ve tallied up your essential monthly costs, you have your income floor. For example, if your mortgage, insurance, and basic living costs add up to $4,000 per month, that becomes your first target for guaranteed income. This number gives you incredible clarity, helping you decide exactly how much of your portfolio you might need to allocate to an income product like an annuity.

Strategically Timing Your Purchase

Deciding when to lock in your income stream is just as important as deciding how. You don't have to do it all at once. In fact, many people find success by "laddering" their purchases over several years, which helps average out the impact of interest rate fluctuations.

For instance, you might buy one annuity a few years before you retire and another right as you stop working. This approach diversifies your timing and can help you capture more favorable rates over time.

Building a guaranteed income plan is less like flipping a switch and more like assembling a puzzle. Each piece—Social Security, pensions, annuities—is placed strategically to create a complete and secure picture of your retirement.

As you map out your personal strategy, a comprehensive guide to planning for early retirement income can be a huge help in figuring out what a "good" monthly income number looks like, especially if you're aiming to retire early.

Questions to Ask Your Financial Advisor

Shopping for income products isn't like buying a TV. You need to ask the right questions to make sure you're getting what you think you're getting. When you sit down with a financial professional, come prepared with a checklist to cover all the critical details.

- What are all the associated fees, commissions, and surrender charges? Get the full picture.

- What is the financial strength rating of the issuing insurance company?

- How will my income payments be protected from inflation over time?

- What are my options for providing income to my spouse or heir if I pass away?

Globally, retirement systems are adapting to aging populations, and while many have improved, only a minority of American workers have access to annuities or similar guaranteed income products. Yet even a moderate allocation could significantly bolster retirement security for the average worker. Armed with the right information, you can build a plan that truly secures your financial future.

Common Questions About Retirement Income

As you start exploring the world of guaranteed retirement income, it's totally normal for questions to bubble up. You're making some big decisions, and getting clear, straightforward answers is the only way to move forward with real confidence.

So, let's cut through the noise and tackle some of the most common concerns and myths we hear from people planning their future. Our goal is to give you the clarity you need to see how these powerful tools might fit into your own retirement vision.

How Much of My Savings Should Go Toward Guaranteed Income?

There’s no magic number that works for everyone. The best way to think about it is to secure enough guaranteed income to cover your non-negotiable, essential expenses. Think of it as building a reliable "income floor" under your retirement.

This means paying for things like your mortgage or rent, utilities, groceries, and healthcare costs with money you know will be there, no matter what the stock market is doing.

For many retirees, this means allocating somewhere between 25% to 50% of their retirement assets to an income-producing product like an annuity. The rest of the portfolio can then be invested for growth to help fight inflation and pay for the "wants"—like travel, hobbies, and spoiling the grandkids. The right mix is deeply personal and depends on your comfort with risk and what other income sources, like Social Security or a pension, you already have.

What Happens to My Money If I Pass Away Early?

This is one of the most important questions people ask, and for good reason. The good news is that modern income products offer plenty of flexibility to protect your legacy. While a basic "life-only" annuity stops paying when you pass away, most people choose a payout structure that includes a beneficiary.

These options provide a valuable safety net for your loved ones:

- Joint and Survivor Annuity: This ensures that if you pass away first, your spouse will continue receiving payments for the rest of their life. It's a hugely popular choice for couples.

- Period Certain: This feature guarantees payments for a set number of years, like 10 or 20. If you pass away during that time, your beneficiary gets the rest of the payments until the period is over.

- Cash Refund: This option makes sure that if you die before receiving at least the amount you put in, your beneficiary will get the difference back in a lump sum.

These features might slightly lower your monthly payment, but the peace of mind they offer is priceless.

Is My Money Safe If the Insurance Company Fails?

Since annuities are financial contracts backed by an insurance company—not the FDIC—your choice of insurer is absolutely critical. You should only work with highly-rated companies that have a long, proven history of financial stability. You can easily check these ratings with independent firms like A.M. Best, S&P, or Moody's.

Choosing a top-tier, financially sound insurance company is your single best line of defense and the most important step in securing your guaranteed income.

As a second layer of protection, every state has a guaranty association. These associations, funded by member insurance companies, are there to protect policyholders if an insurer fails. They cover claims up to specific limits (which vary by state), providing an important backstop for consumers.

Navigating these decisions is a critical part of building a retirement you can truly count on. At Commons Capital, we specialize in helping clients create robust financial plans that stand the test of time. To learn how we can help you build a reliable income stream for your future, visit us at https://www.commonsllc.com.