If you've spent years investing in your company's stock through your 401(k), you might be sitting on a huge tax time bomb without even realizing it. The good news? A little-known IRS rule called Net Unrealized Appreciation, or NUA, could be the key to defusing it. The Net Unrealized Appreciation (NUA) strategy is a powerful tax play that lets you treat the growth on that company stock as a long-term capital gain instead of ordinary income. That distinction might sound small, but it can slash your tax bill by tens, or even hundreds, of thousands of dollars.

Unlocking Major Tax Savings With Company Stock

For a lot of long-tenured employees, company stock makes up a huge slice of their retirement portfolio. Watching that stock grow over the years is a fantastic feeling, but it also creates a looming tax problem.

Normally, when you pull money out of a traditional 401(k) or a rollover IRA, every single dollar is taxed as ordinary income. With federal rates climbing as high as 37%, that can take a massive bite out of your hard-earned savings.

This is where the Net Unrealized Appreciation (NUA) strategy completely changes the game. It gives you a way to separate your appreciated employer stock from the rest of your 401(k) funds when you leave your job or retire. By taking this specific step, you fundamentally alter how the IRS taxes the gains on that stock.

The Two Tax Components of NUA

To really get how NUA works, you have to think about your stock's value in two separate pieces:

- The Cost Basis: This is what the stock was worth when it was originally purchased for you inside the 401(k). When you execute the NUA strategy, this amount is taxed as ordinary income in that year.

- The Net Unrealized Appreciation: This is all the growth — the difference between the stock's current market value and that original cost basis. This is the prize. The NUA portion qualifies for the much lower long-term capital gains tax rates, which currently sit at 0%, 15%, or 20%.

This tax treatment is a game-changer. By isolating the appreciation and subjecting it to favorable capital gains rates, you sidestep the higher ordinary income tax that would have applied to the entire amount in a standard IRA rollover.

A Powerful Real-World Illustration

Let's put some numbers to this to see just how dramatic the savings can be.

Imagine you retire with $1 million worth of company stock in your 401(k). The original cost basis for that stock is just $150,000. That means you have $850,000 in pure NUA.

If you just did a standard IRA rollover, the entire $1 million would eventually be taxed at your ordinary income rate as you take distributions. But with the NUA strategy, only the $150,000 cost basis is hit with ordinary income tax upfront. The other $850,000 gets the preferential long-term capital gains treatment when you sell it.

As some financial analyses have shown, this simple move could result in over $143,000 in tax savings. Understanding how this fits into your broader financial picture is a key part of comprehensive retirement planning.

To make this even clearer, let's compare the two approaches side-by-side.

NUA Strategy Vs IRA Rollover At A Glance

This table breaks down the tax treatment of our $1 million example, highlighting where the savings come from. It’s a simplified look, but it powerfully illustrates the core benefit of the NUA rule.

As you can see, the NUA strategy shifts the bulk of the asset's value from the high-tax ordinary income column to the low-tax capital gains column. For the right person, this isn't just a minor optimization — it's a foundational strategy for preserving wealth in retirement.

How to Actually Pull Off an NUA Distribution

Executing the Net Unrealized Appreciation (NUA) strategy requires you to follow the IRS playbook to the letter. One wrong move, and the whole tax benefit can disappear, turning what should have been a huge win into a costly mistake. Think of it as a precise flight plan for your retirement funds — every step must be completed in the right order.

The whole point is to separate your highly appreciated company stock from the rest of your 401(k) assets when you take the money out. While your other investments, like mutual funds, can be rolled over into a traditional IRA to keep growing tax-deferred, the company stock has to follow a completely different route.

The All-Or-Nothing Lump-Sum Rule

It all starts with a lump-sum distribution. This is a non-negotiable requirement from the IRS. It means you have to take out your entire vested balance from all your employer's similar retirement plans (like all your 401(k)s) within one calendar year.

You can't just pick out the company stock or take out the money in chunks over several years. For instance, if your 401(k) holds $800,000 in mutual funds and $200,000 in company stock, the full $1,000,000 must exit the plan in the same tax year to qualify. This has to be triggered by a specific event, like leaving your job or turning 59½.

The In-Kind Transfer: Where Most People Mess Up

This is the step where so many well-intentioned NUA attempts go off the rails. You must transfer the actual employer stock shares in-kind straight into a taxable brokerage account. "In-kind" just means moving the shares themselves — not selling them first and moving the cash.

Crucial Warning: Whatever you do, do not roll the company stock into an IRA first. Even if the shares sit in that IRA for a single day before you move them to a brokerage account, you've permanently lost the NUA treatment. The shares have to bypass the IRA completely.

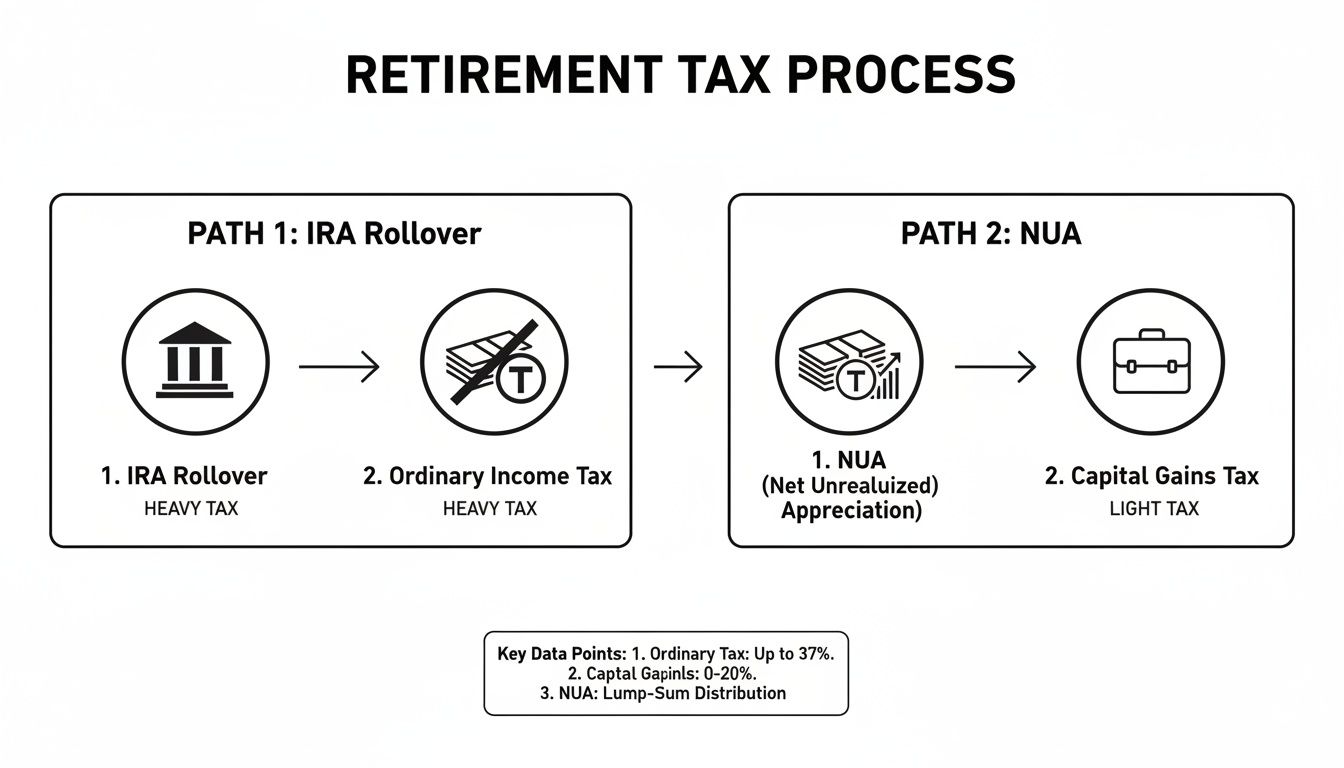

This diagram shows the two very different paths your retirement money can take and the tax bill that comes with each.

As you can see, the NUA path sends your employer stock toward friendly capital gains tax rates, while a standard IRA rollover subjects everything to higher ordinary income tax down the road.

Breaking Down the Tax Hit

Once the distribution is done, two separate tax events are triggered. You have to understand both to see how the NUA strategy really saves you money.

- Tax on the Cost Basis: The original price you paid for the stock, known as the cost basis, is taxed as ordinary income in the year you do the distribution. This creates an immediate tax liability, and it can be a big one, so you need to plan for it.

- Tax on the NUA: The growth part — the NUA itself — isn't taxed right away. Instead, it qualifies for long-term capital gains tax rates whenever you decide to sell the shares, even if you sell them the very next day.

That immediate tax hit on the cost basis is the price you pay to unlock the much lower capital gains rate on the much larger appreciation amount. For anyone sitting on stock with a very low basis, this is an incredible trade-off. You can learn more about managing these types of accounts by exploring what to do with your 401(k) after leaving a job.

By getting these mechanics down — the lump-sum rule, the in-kind transfer, and the two-part tax treatment — you'll have the foundation you need to pull off this powerful strategy and sidestep the common, irreversible mistakes.

Figuring Out If You're Eligible For The NUA Strategy

The Net Unrealized Appreciation (NUA) strategy isn't some universal tax break you can just opt into. It’s a specialized tool with very strict IRS guidelines, really only meant for people in a handful of specific financial situations. Before you can even think about its powerful benefits, you have to clear a series of non-negotiable hurdles.

Think of it like a locked door. To open it, you need the right key — and in this case, the key is what the IRS calls a "triggering event." Without one of these qualifying life events, the NUA option is completely off the table, no matter how much your company stock has grown.

The Four Essential Triggering Events

The IRS is crystal clear on what counts as a valid reason to take the kind of lump-sum distribution that makes NUA possible. You absolutely must meet at least one of these four conditions:

- Separation from Service: This is the big one for most people. It means you’ve quit, retired, or been laid off from the company whose stock you hold in your 401(k).

- Reaching Age 59½: Even if you’re still working, hitting this age milestone officially unlocks your ability to use the NUA strategy.

- Total and Permanent Disability: If you become permanently disabled (as the IRS defines it), this also serves as a qualifying event.

- Death: If the account holder passes away, their beneficiary can choose to use the NUA strategy on the company stock they inherit.

It's critical to understand that the distribution has to happen after one of these events. For example, you can't take the distribution at age 58 and then try to claim eligibility a year later when you turn 59½.

The timing and sequence of events are everything. A triggering event must come before the lump-sum distribution, and both must happen in the same tax year for the NUA strategy to work.

Who Is The Ideal Candidate For An NUA Strategy?

Just meeting the triggering event criteria isn’t the whole story. The NUA strategy is most powerful for a very specific type of retiree or employee. The ideal candidate usually has a unique mix of circumstances that really cranks up the potential tax savings.

You are likely a strong candidate if this sounds like you:

- You have a ton of highly appreciated company stock. The strategy’s value is directly tied to the massive gap between what you paid for your stock (its cost basis) and what it’s worth today.

- You're a long-tenured employee, executive, or early team member. These are the people who often pile up huge amounts of company stock over many years at a very low average cost.

- Your 401(k) is heavily weighted towards this employer stock. When a huge chunk of your retirement nest egg is in this one stock, the tax leverage you get from NUA becomes incredibly significant.

For instance, picture a long-term employee who accumulated 1,000 shares of stock in their 401(k) at an average cost of just $20 per share. That's a total cost basis of $20,000. If that same stock is now trading at $244.45 per share, the position has exploded to $244,450. That creates a staggering NUA of $224,450. This kind of widening gap has become more and more common, especially with the market's performance since 2009, making the NUA strategy a hot topic for today's retirees. You can find more real-world examples by exploring insights on NUA in 401(k) rollovers.

Seeing The NUA Strategy In Action

The theory behind Net Unrealized Appreciation (NUA) is interesting, but seeing how it plays out with real money is what truly matters. When you can trace every dollar, abstract tax rules suddenly become very concrete savings.

Let's walk through a detailed scenario. This will throw a spotlight on the dramatic difference in tax outcomes between a standard IRA rollover and a well-executed NUA distribution.

Meet Ana, Our Case Study

Let’s meet Ana, a 62-year-old executive on the verge of retirement after a long, successful career. Her 401(k) has grown to a healthy $1,200,000. Inside that account, a significant chunk — $700,000 — is company stock that has appreciated beautifully over the years. The remaining $500,000 is held in various mutual funds.

Now for the critical detail: the stock's cost basis. The company's contributions over the years have left her with a total cost basis of just $100,000.

This simple fact creates a massive NUA of $600,000 ($700,000 market value minus the $100,000 basis). With Ana in the 32% federal income tax bracket and the 15% long-term capital gains bracket, she’s facing a major decision with two very different paths.

Path 1: The Standard IRA Rollover

The most common advice, and the easiest path, is to simply roll her entire $1,200,000 401(k) into a traditional IRA. It's clean, simple, and avoids any immediate tax hit. All her money continues to grow tax-deferred.

But this simplicity comes with a hefty long-term price tag. Every single dollar Ana eventually pulls from that IRA — whether from the original stock, the mutual funds, or future growth — will be taxed as ordinary income. At her 32% rate, that $700,000 in company stock would eventually create a tax bill of $224,000.

Path 2: Executing the NUA Strategy

Sensing a huge opportunity, Ana decides to explore the NUA route. She and her financial advisor put together a plan to execute a lump-sum distribution, carefully following the rules.

Here’s their game plan, step by step:

- Split the Assets: She instructs her 401(k) administrator to divide the distribution. The $500,000 in mutual funds is rolled over directly into a traditional IRA. This move is tax-free and keeps that portion of her money growing tax-deferred.

- Move the Stock In-Kind: The $700,000 of company stock is transferred in-kind — as actual shares, not cash — directly into a taxable brokerage account. This is the key that unlocks the powerful NUA tax treatment.

This transaction triggers an immediate, but manageable, tax event. Ana must pay ordinary income tax, but only on the stock’s $100,000 cost basis.

Upfront Tax Liability:

$100,000 (Cost Basis) x 32% (Ordinary Income Rate) = $32,000

Paying $32,000 today might sting a little, but it's the price of admission to a much better tax situation down the road. The $600,000 NUA is now set up to be taxed at the much friendlier 15% long-term capital gains rate whenever she decides to sell.

Let's assume she sells the stock right away to diversify.

Deferred Tax Liability (Realized on Sale):

$600,000 (NUA) x 15% (LTCG Rate) = $90,000

The Final Tally: A Clear Winner

Now we can put the total tax impacts side-by-side to see the bottom line.

By choosing the NUA strategy, Ana locks in a stunning $102,000 in tax savings on her company stock. And this isn't some far-fetched scenario. A Fidelity Charitable NUA case study showed a retiring executive in a similar spot saved $68,320 immediately by using this powerful rule, which is laid out in IRC Section 402(e)(4).

Beyond the Basics: Advanced NUA Strategy and Common Pitfalls

Pulling off the Net Unrealized Appreciation (NUA) strategy is a big win, but the real art is weaving it into your entire financial life. You have to look beyond the transaction itself and see the ripple effects on your estate, state taxes, and even future healthcare costs. It's a high-stakes move where one wrong step can be costly and, worse, irreversible.

Thinking through these advanced angles is what separates a decent tax-saving move from a brilliant, wealth-enhancing one. It’s about playing chess with your financial future, not checkers.

How NUA Plays into Your Estate Plan

For anyone with significant assets, the NUA strategy has a powerful estate planning tool baked right in: the stepped-up basis. When you pass away holding NUA stock in a taxable brokerage account, your heirs get a clean slate. They inherit those shares with a new cost basis equal to the stock’s market value on your date of death.

This is a game-changer. All that built-in capital gain — both the NUA and any growth since you took the distribution — is completely wiped out for tax purposes. Your beneficiaries can sell the stock the next day and owe nothing in capital gains tax on decades of appreciation, keeping more of your legacy intact.

Don't Forget About State Income Taxes

The federal tax benefits of NUA are clear-cut, but things get murky when you cross state lines. It’s a huge mistake to assume your state treats capital gains as kindly as Uncle Sam does.

Some states tax capital gains at the same high rates as ordinary income. If you’re in a state like that, the tax-saving allure of the NUA strategy can fade pretty quickly.

Crucial Tip: You absolutely have to run the numbers based on your specific state's tax code. A strategy that looks like a home run on your federal return might turn into a single once you factor in state taxes, sometimes making a traditional IRA rollover the smarter play.

The Hidden Hit to Your Medicare Premiums

Here’s a curveball most people don’t see coming: the NUA strategy can jack up your Medicare premiums. That upfront tax you pay on the stock's cost basis creates a one-time spike in your modified adjusted gross income (MAGI).

That spike can launch you into a higher Income-Related Monthly Adjustment Amount (IRMAA) bracket two years down the road. This means you could face hundreds or even thousands of dollars in extra surcharges on your Medicare Part B and Part D premiums. You have to weigh the long-term tax savings from NUA against the short-term pain of higher healthcare costs.

A Checklist of Common NUA Pitfalls

Even the best-laid NUA plans can go sideways because of simple execution errors. Steering clear of these common blunders is non-negotiable.

- Violating the Lump-Sum Distribution Rule: This is an all-or-nothing deal. You have to distribute your entire vested balance from all similar employer plans within a single calendar year. Just taking the stock or spreading the distributions over two years will blow up the whole strategy.

- The Infamous IRA Rollover Mistake: Whatever you do, do not roll your company stock into an IRA, not even for a minute. The shares have to be moved in-kind straight to a taxable brokerage account. This is probably the most common — and most painful — mistake people make, and there’s no undo button.

- Losing Track of Your Cost Basis: It’s your job to know the cost basis of that stock. Without it, you can’t figure out how much ordinary income tax to pay upfront or the capital gain when you sell. Guard the records from your plan administrator like gold.

- Ignoring Concentration Risk: The NUA strategy solves a tax problem, but it creates an investment one. You’ve now got a massive chunk of your wealth tied up in a single stock. That’s a huge risk. For more on this, check out our guide on strategies for managing a concentrated stock position.

Is The NUA Strategy The Right Move For You?

Deciding to use the Net Unrealized Appreciation (NUA) strategy is a major financial crossroads, not a simple yes-or-no question. It demands a hard look at your entire financial picture, weighing some powerful tax benefits against very real risks and trade-offs. The right choice depends entirely on your unique circumstances.

This decision really boils down to a few key variables. Getting them right can be the difference between a savvy tax-saving maneuver and a costly misstep. The goal is to see if the numbers, your timeline, and your personal risk tolerance all point in the same direction.

Key Factors in Your Decision

To start, you need a clear-eyed assessment of your situation. The NUA strategy is most compelling when there's a massive gap between your company stock’s cost basis and its current market value. A high NUA-to-basis ratio is the engine that drives the tax savings.

Your current and expected future tax brackets are also critical. If you’re in a high tax bracket now but expect to be in a lower one during retirement, paying ordinary income tax on the basis upfront might be less appealing than just deferring all the taxes with a standard IRA rollover.

The core question is: Does the long-term benefit of paying capital gains tax on the appreciation outweigh the immediate sting of paying ordinary income tax on the cost basis?

You also have to think about your need for liquidity and income. Pulling the trigger on NUA creates an immediate tax bill, which you must be prepared to pay out of pocket. It also moves a significant asset out of your tax-deferred retirement account, which completely changes your future income streams and how they’re taxed.

Weighing Risk and Diversification

Executing the NUA strategy solves a tax problem but creates an investment one: a highly concentrated stock position. Holding a huge chunk of your wealth in a single company’s stock exposes you to serious volatility and risk. This is a critical factor that people often overlook when they're chasing tax savings.

You have to be brutally honest with yourself about your comfort level with this risk. Ask yourself:

- Can I afford for this stock to tank? If the stock’s value drops significantly after the transfer, the tax benefits of the NUA strategy could shrink dramatically or even get wiped out completely.

- Does this fit my long-term investment goals? A diversified portfolio is usually the bedrock of sound retirement planning. The NUA strategy, at least initially, runs directly counter to that principle.

- Do I have a plan to diversify later? Selling the stock to reinvest in a broader mix of assets is a common follow-up step. But you have to be ready for the capital gains tax that sale will trigger. This is a complex decision, similar to those you might face when you convert a 401(k) to a Roth IRA.

Ultimately, the NUA strategy is a powerful but highly specialized tool. The complexity and high stakes demand professional guidance. Working with a qualified financial advisor is essential to run the numbers for your specific situation and make sure this move aligns perfectly with your long-term wealth objectives.

Common Questions About The NUA Strategy

Even after you get the hang of the basics, a move as big as using the Net Unrealized Appreciation (NUA) strategy is bound to bring up some specific questions. Let's tackle the ones that come up most often to help you nail down the final details.

What Happens If I Sell The Stock Immediately After Transfer?

This is where the magic of the NUA rule really shines. If you sell your company stock the moment it hits your brokerage account, the NUA portion gets taxed at friendly long-term capital gains rates. That holds true no matter how long the stock was sitting in your 401(k).

Just keep in mind, any new appreciation — any gains the stock makes after landing in your brokerage account — plays by the usual rules. Sell within a year of the transfer, and that new slice of profit is a short-term capital gain, taxed just like ordinary income.

Can I Use The NUA Strategy For A Portion Of My Employer Stock?

No, and this is a deal-breaker. Getting this wrong is a costly mistake. The entire NUA strategy hinges on taking a lump-sum distribution.

That means you have to clear out the entire vested balance from all of that company's qualified plans (think every 401(k) and pension plan you have with them) within a single calendar year. You can’t just pick your favorite, most appreciated shares and leave the rest. It's an all-or-nothing deal.

What If My Company Stock Value Goes Down After The NUA Transfer?

This is the big risk you have to get comfortable with. Once those shares are in your taxable brokerage account, you’re on the rollercoaster of market ups and downs. If the stock takes a nosedive after you make the move, the tax savings you were hoping for can shrink quickly.

If the stock’s value drops below what you originally paid for it (your cost basis), the tax advantage could get wiped out completely. It's a stark reminder of why it’s so important to talk with your advisor about concentration risk and have a solid plan to diversify once the transfer is complete.

How Does The NUA Strategy Affect Required Minimum Distributions?

Here’s another huge plus for the NUA strategy. When you move company stock out of a tax-deferred plan like a 401(k) and into a regular brokerage account, you’re shrinking the pot of money that will be subject to Required Minimum Distributions (RMDs) down the road.

This sets off a couple of positive chain reactions:

- You could dramatically lower your taxable income once you hit the age where RMDs are mandatory.

- Keeping your retirement income in check can also help you sidestep or minimize those pesky Medicare IRMAA surcharges on your premiums.

Getting these details right is what separates a smart financial move from a potential headache.

The ins and outs of the NUA strategy show just how valuable professional advice can be. At Commons Capital, we specialize in helping high-net-worth individuals navigate these kinds of complex decisions to protect and grow their wealth. https://www.commonsllc.com