Learning how to reduce capital gains tax often comes down to three core strategies: holding assets for longer than a year, strategically selling losing investments to offset gains, and making the most of tax-advantaged accounts. It’s amazing how simple timing and a bit of forethought can slash what you owe, turning a potential tax headache into a savvy financial move. This guide will walk you through several effective methods for minimizing your tax liability.

Getting the Capital Gains Tax Fundamentals Right

Before diving into complex strategies, you need a rock-solid grasp of the basics. This isn't about finding obscure legal loopholes; it’s about understanding how small details create big savings.

At its heart, capital gains tax is just a tax on the profit you make from selling an asset—stocks, real estate, a business—for more than you paid for it. The real key to minimizing this tax is knowing the rules of the game.

The most important distinction to make is between short-term and long-term capital gains. This isn't just jargon; it's a fundamental fork in the road that determines how much tax you'll actually pay. The difference boils down to one simple question: how long did you own the asset before selling?

The Power of a Single Day

If you hold an investment for one year or less before selling, you've got a short-term capital gain. These profits are taxed at your ordinary income tax rate, the same as your salary. For high-net-worth individuals, that can climb as high as 37% federally. Ouch.

But if you hold that same asset for more than one year—even just by one extra day—the profit is treated as a long-term capital gain. This is where the magic happens.

Long-term capital gains get much better treatment, with tax rates of 0%, 15%, or a maximum of 20% for the highest earners. This is the government's way of rewarding long-term investors, and it's the cornerstone of any serious tax reduction strategy.

Simply holding investments for more than a year to get those preferential long-term capital gains (LTCG) tax rates is one of the most powerful tools in your arsenal. The difference between paying up to 37% on a gain versus a maximum of 20% is massive, and all it takes is patience.

To give you a clearer picture, here’s a quick breakdown of how the two compare.

Long-Term vs Short-Term Capital Gains at a Glance

This table simplifies the core differences you need to know.

As you can see, the financial incentive to hold assets for the long term is significant. It's a foundational principle every investor should build their strategy around.

How Your Assets Are Valued for Taxes

Another piece of the puzzle is your cost basis—essentially, the original value of an asset for tax purposes. This includes not just the purchase price but also any commissions or fees you paid. Your taxable gain is what's left after you subtract the cost basis from the sale price.

A higher cost basis means a lower taxable gain, so tracking it accurately is non-negotiable.

This concept becomes particularly important when selling a large asset, like a business. How you structure the deal—as an asset sale versus a stock sale, for instance—can dramatically change the cost basis and, consequently, your final tax bill. If you're in that position, it's worth digging into the asset purchase vs. stock purchase considerations to make the right call.

Using Tax-Loss Harvesting to Offset Gains

Tax-loss harvesting is one of the most practical and powerful tools in an investor's toolkit for managing their tax bill. This isn't just theory; it's a hands-on strategy you can use to turn market dips into tangible tax advantages.

The core idea is simple: you deliberately sell underperforming assets at a loss. That loss is then used to offset the capital gains from your winning investments, directly lowering your overall liability. When executed properly, it allows you to maintain your desired market exposure while systematically reducing what you owe the IRS.

How It Works in Practice

The mechanics are refreshingly straightforward. Capital losses are first used to wipe out capital gains. If your losses exceed your gains for the year, you can then use up to $3,000 of that excess loss to reduce your ordinary income, which is often taxed at a much higher rate.

Any remaining losses beyond that aren't wasted. They can be carried forward indefinitely to offset gains or income in future years, creating a compounding benefit that makes this a cornerstone of any tax-smart investment plan.

Let’s walk through a quick scenario:

- Your Gains: You sell Stock A and realize a $20,000 long-term capital gain.

- Your (Paper) Losses: You own Stock B, which happens to be down $15,000.

- The Move: You sell Stock B to "harvest" that $15,000 loss.

- The Outcome: The $15,000 loss directly cancels out $15,000 of your gain, leaving you with a taxable gain of only $5,000.

Without this move, you'd be on the hook for taxes on the full $20,000. To put this into action, you can use specific tools to identify assets that have declined in value that make spotting these opportunities much easier.

Navigating the Wash-Sale Rule

Of course, there's a catch. The biggest trap you can fall into with tax-loss harvesting is the wash-sale rule. The IRS put this in place to prevent investors from selling a security at a loss just to claim a tax deduction, only to buy it right back again.

A wash sale is triggered if you sell a security at a loss and, within 30 days before or after the sale (a 61-day total window), you do any of the following:

- Buy a "substantially identical" security.

- Acquire a contract or option to buy a substantially identical security.

- Acquire a substantially identical security for your IRA or Roth IRA.

If you trigger this rule, the IRS won't let you claim the tax loss. The simple way to avoid this is to wait at least 31 days before repurchasing the same or a very similar asset.

A common workaround is to reinvest the proceeds into a different but similar investment. For example, you might sell an S&P 500 ETF from one provider and immediately buy an S&P 500 ETF from another. This keeps your money in the market while still successfully capturing the loss.

For a deeper look into the mechanics, you can read more about various tax-loss harvesting strategies in our detailed guide.

Key Takeaway: The wash-sale rule is a 61-day window. To successfully harvest a loss, you must avoid repurchasing a substantially identical security for 30 days before and 30 days after the sale.

Maximizing Tax-Advantaged Retirement Accounts

It's easy to think of your retirement accounts as just a place to park savings. In reality, they are probably the most powerful tools you have for tax-efficient investing.

Accounts like 401(k)s, Traditional IRAs, and Roth IRAs are built-in shields, allowing your investments to grow year after year without the constant drag of annual capital gains taxes. For anyone serious about building long-term wealth, mastering these accounts is non-negotiable.

But not all accounts are created equal. Each one offers a different flavor of tax savings, and the right mix for your plan depends entirely on your income—both now and what you expect it to be in the future.

The Power of Tax-Deferred Growth

Employer-sponsored plans like a 401(k) or a Traditional IRA give you a significant benefit right out of the gate. Your contributions are usually made with pre-tax dollars, which has the immediate effect of lowering your taxable income for the year. For high earners, that's an instant win.

Once the money is inside the account, it's in a protected bubble. You can buy, sell, and rebalance your heart out without triggering a single tax bill. The IRS only comes knocking when you start taking distributions in retirement.

The real magic of tax-deferred accounts is compounding. By putting off taxes, more of your money stays invested and working for you. Over decades, this can lead to dramatically more growth than you’d ever see in a standard taxable brokerage account.

The Ultimate Tax Shelter: A Roth IRA

Tax deferral is great, but the Roth IRA takes things to a whole other level. With a Roth, you contribute with after-tax dollars, so there's no upfront tax deduction. The payoff for this is massive.

Every qualified withdrawal you make from a Roth IRA in retirement is 100% tax-free. That includes your original contributions and, more importantly, every penny of investment growth. You can completely sidestep capital gains tax on decades of compounding. It’s hard to beat that.

- Tax-Free Growth: Your investments grow entirely sheltered from the IRS.

- Tax-Free Withdrawals: You won't owe a dime in federal income or capital gains tax on qualified distributions.

- No Required Minimum Distributions (RMDs): Unlike its traditional counterparts, a Roth IRA has no RMDs for the original owner, giving you far more control and flexibility in retirement.

If your income is too high to contribute directly, don't assume a Roth is off the table. A backdoor Roth IRA conversion is a well-established strategy that allows high earners to access these incredible tax-free benefits.

Strategic Planning for Maximum Benefit

So, how do you weave these accounts into your overall financial plan? It often boils down to a simple question: Do you expect your tax rate to be higher now or in retirement?

- If you anticipate being in a lower tax bracket in retirement, a Traditional 401(k) or IRA is a smart move. You grab the tax deduction now while your income is at its peak.

- If you think you'll be in a higher tax bracket later on, the Roth IRA is usually the clear winner. You pay taxes now at your current, lower rate and enjoy all that tax-free income when you need it most.

For 2024, the 401(k) contribution limit is $23,000, with an extra $7,500 catch-up for those 50 or older. For IRAs, the limit is $7,000, with a $1,000 catch-up. Maxing out these contributions is one of the simplest and most effective moves you can make to lower your tax bill while securing your future.

Applying Advanced Gifting and Charitable Strategies

Beyond the standard playbook of portfolio management, your generosity can be a surprisingly powerful tool for tax planning. For investors with a philanthropic streak or a goal of transferring wealth efficiently, certain strategies offer a compelling dual benefit.

These aren't just feel-good gestures. They are calculated financial decisions that let you support the people and causes you care about while creating significant tax advantages that can directly slash your capital gains exposure. The secret lies in knowing how to use your most appreciated assets—the ones that have grown significantly in value—to their full potential.

Donate Appreciated Assets Directly

One of the most effective yet often overlooked strategies is donating appreciated assets, like stocks you've held for more than a year, directly to a qualified charity. So many investors make the classic mistake of selling the stock first and then donating the cash. This is a costly error.

When you sell the asset yourself, you trigger a capital gains tax event on the profit. But by donating the asset directly, you secure two major tax wins:

- You eliminate capital gains tax. You completely sidestep the capital gains tax you would have owed on the growth. The charity, as a tax-exempt entity, can sell the asset without facing any tax liability.

- You get a full deduction. You can typically claim a charitable deduction for the asset's full fair market value on the date of the donation, not just what you originally paid for it.

This one-two punch makes it a far more efficient way to give.

Scenario: Imagine you want to give $50,000 to your favorite cause. You happen to own stock now worth $50,000 that you bought years ago for only $10,000. If you sell it, you'll likely owe capital gains tax on the $40,000 profit. Donate the stock directly, though, and you avoid that tax entirely and still get to deduct the full $50,000.

Strategic Gifting to Family Members

Gifting can also be a savvy way to reduce the overall tax hit on an appreciated asset within your family. The idea is to move an asset from your hands (likely in a high tax bracket) to a family member—like an adult child—who is in a much lower one.

When you gift an asset, the recipient also inherits your original cost basis. That means when they eventually sell it, they’re the one on the hook for the capital gains tax. But if they're in a 0% or 15% long-term capital gains bracket, the tax bill will be a fraction of what you would have paid in the 20% bracket.

Of course, this requires careful planning around the annual gift tax exclusion limits. For 2024, you can gift up to $18,000 per person without needing to file a gift tax return, which allows for a systematic transfer of assets over time.

Using Donor-Advised Funds for Flexibility

What if you want to make a big charitable impact now but need more time to decide exactly which organizations to support? A Donor-Advised Fund (DAF) is the perfect solution. Think of it as your own personal charitable investment account.

You can make a large contribution of appreciated stock to the DAF in a single year, locking in an immediate tax deduction and avoiding the capital gains tax. Those assets can then be invested inside the DAF and continue to grow, tax-free. From there, you can recommend grants from the fund to your chosen charities over several years, on your own timeline.

This strategy is especially powerful in years when you have unusually high income. It lets you "bundle" several years' worth of giving into one, maximizing your deduction when it helps you the most. It effectively separates the timing of your tax benefit from the timing of your actual gifts, giving you incredible flexibility and control.

Leveraging Specialized Investment Vehicles

When you have a significant capital gain, specialized investments can be a game-changer. They come with powerful, built-in benefits designed to defer or even completely wipe out your capital gains tax liability.

For savvy investors, especially those deep in the real estate world, these strategies can turn what would have been a hefty tax bill into a fantastic long-term growth opportunity.

Two of the most impactful tools out there are Qualified Opportunity Funds (QOFs) and the classic 1031 exchange. While both are rooted in real estate and tax deferral, they operate very differently and come with their own strict rulebooks. Knowing when and how to use these powerful tools is crucial for maximizing your returns.

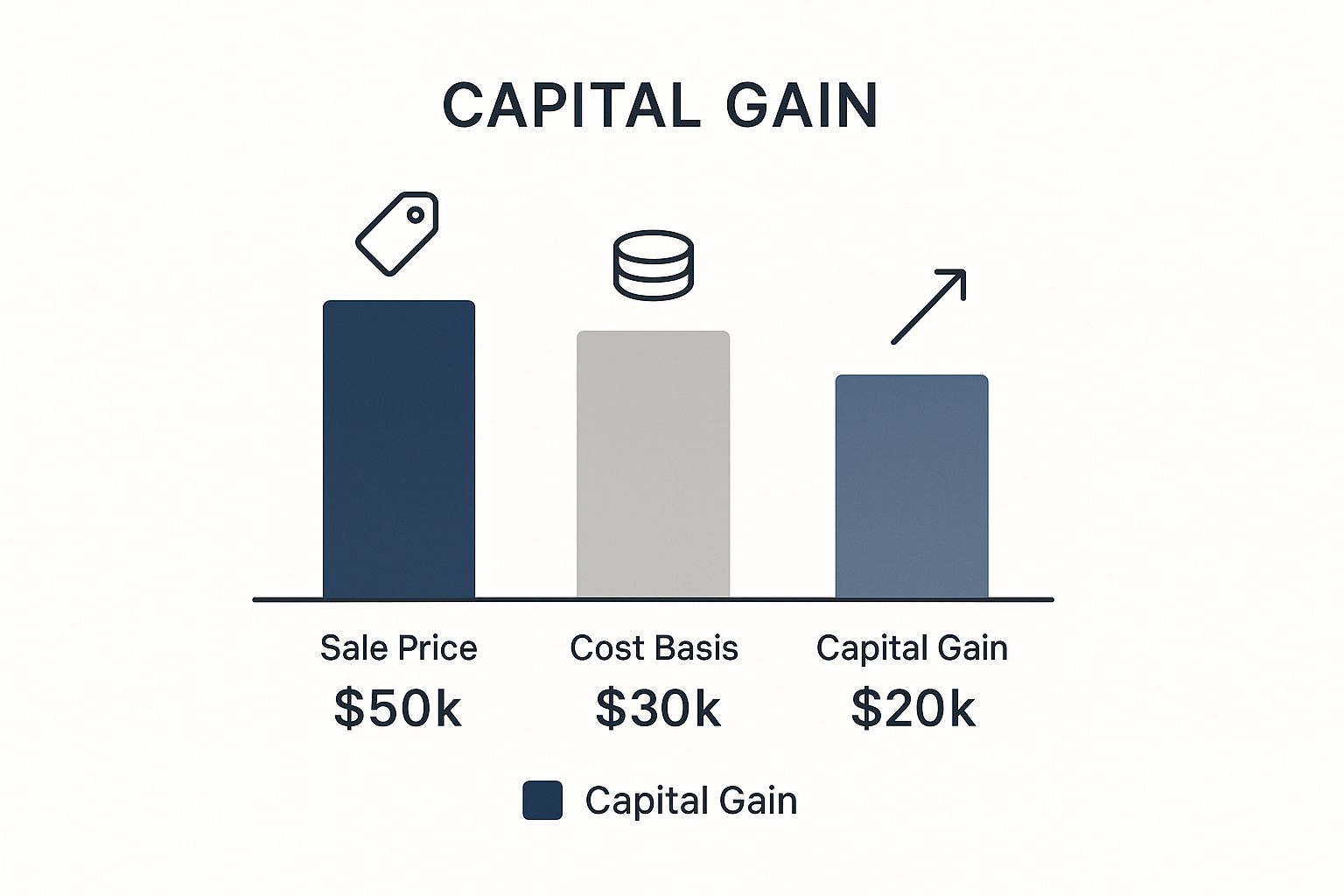

This graphic gives a quick breakdown of how a capital gain is calculated—it's the difference between your sale price and your cost basis that determines your taxable profit.

As you can see, that $20,000 profit is the number you need to tackle with a smart strategy, and that's where things like QOFs and 1031 exchanges come into play.

Unpacking Qualified Opportunity Funds

Introduced by the Tax Cuts and Jobs Act of 2017, Qualified Opportunity Zones are designated economically distressed areas. The government created them to incentivize new investment, and in return, investors get some pretty sweet tax perks. By reinvesting your capital gains into a Qualified Opportunity Fund (QOF) that invests in these zones, you unlock a unique set of benefits.

Here’s the rundown:

- Tax Deferral: You get to put off paying tax on the original capital gain. The bill isn't due until you sell your QOF investment or until December 31, 2026, whichever happens first.

- Tax-Free Growth Potential: This is the real kicker. If you hold onto your QOF investment for at least 10 years, any appreciation on the QOF investment itself can be 100% tax-free.

This makes QOFs more than just a way to delay taxes; they're a vehicle for creating an entirely new stream of tax-free wealth. The catch? You have to move fast. You must reinvest your eligible gains into a QOF within 180 days of the sale, so timing is everything.

The Power of the 1031 Exchange

For anyone who's been in real estate for a while, the 1031 exchange is a familiar and time-tested strategy for deferring capital gains. Named after Section 1031 of the IRS code, it lets you sell an investment property and roll the entire proceeds into a new "like-kind" property without having to pay taxes on the gain right away.

This is how real estate investors can continuously scale their portfolios, deferring capital gains pretty much indefinitely. In theory, you could keep doing 1031 exchanges your entire life. When you pass away, your heirs could inherit the properties with a stepped-up basis, which might just eliminate the deferred tax liability for good.

It's crucial to remember that a 1031 exchange is tax-deferred, not tax-free. You're effectively kicking the tax can down the road, which allows your pre-tax profit to keep working and compounding for you.

But be warned: the rules are ironclad. You have a very tight window to identify a replacement property—just 45 days from the sale of your original property. And you have to close on that new property within 180 days total. If you miss either of those deadlines, the exchange is busted, and your gain becomes taxable immediately.

Comparing QOFs and 1031 Exchanges

Both QOFs and 1031 exchanges are powerful tools for deferring capital gains, but they serve different goals and fit different scenarios. A 1031 is strictly for like-kind real estate swaps, while a QOF lets you invest gains from any asset (like stocks or a business sale) into a designated fund.

Let's break down the key differences.

Tax Deferral Strategy Comparison

Choosing the right path depends entirely on your financial picture and what you're trying to achieve.

And these aren't the only creative real estate strategies out there. For example, many investors don't realize the unique tax-sheltering benefits of buying real estate in an IRA. The key is always to match the right strategy to your specific financial goals and the type of gain you're managing.

Common Questions About Reducing Capital Gains Tax

Navigating the world of capital gains is notoriously complex, and it’s natural for even the most experienced investors to have questions. Getting the details right is critical for making smart financial decisions that actually support your long-term goals.

Here are a few of the most common questions we hear from clients, broken down with clear, direct answers to help you manage your portfolio with more confidence.

Can Investment Losses Offset Regular Income?

This is a big one, and the short answer is yes—but with a pretty tight limit. The main reason to harvest a capital loss is to cancel out a capital gain. It works like this: long-term losses offset long-term gains first, and short-term losses offset short-term gains. Simple enough.

Now, if you have more losses than gains in a given year, you can use that excess loss to reduce your ordinary income (like your salary). But the IRS caps this deduction at just $3,000 per year for individuals or married couples filing jointly.

Any losses left over after that aren't gone for good. You can carry them forward indefinitely to use against gains or income in future years. This is what makes tax-loss harvesting such a valuable long-term strategy, even if you don't have huge gains to offset right now.

Key Insight: While you can use investment losses to reduce your taxable income, the direct offset against your salary is limited to $3,000 annually. The real power comes from using those losses to neutralize much larger capital gains.

What Is the Difference Between Tax Avoidance and Tax Evasion?

It is absolutely essential to understand the bright line between legal tax planning and illegal activity. The distinction isn't blurry at all; it's black and white.

- Tax Avoidance: This is simply the legal use of the tax code to minimize what you owe. Every strategy in this guide—holding assets for over a year to get the long-term rate, using tax-advantaged accounts, harvesting losses—is a form of tax avoidance. You're playing by the rules the government itself created.

- Tax Evasion: This is the illegal act of not paying taxes that are rightfully owed. We’re talking about willfully misrepresenting your finances by underreporting income, faking deductions, or hiding money offshore to keep it off the IRS’s radar.

The penalties for tax evasion are severe, including massive fines, interest on back taxes, and even jail time. A smart financial plan is always focused on legal and ethical tax avoidance, never evasion.

How Often Should I Review My Portfolio for Tax Savings?

There's no magic number here, but being proactive always beats being reactive. One of the biggest mistakes we see is people waiting until December to start thinking about taxes. By then, you've left money on the table.

A more systematic approach yields much better results. We generally recommend a few key review periods:

- Quarterly Check-Ins: A quick look every quarter keeps you on top of market moves. It helps you spot potential tax-loss harvesting opportunities as they pop up, instead of scrambling at the last minute.

- Mid-Year Review: June or July is the perfect time for a deeper dive. You have a good picture of your income and investment performance for the year, which gives you plenty of runway to make strategic adjustments.

- Year-End Planning: The October-to-December window is your final chance to make moves that will impact your current year's tax bill. This is when you'd execute any final tax-loss harvesting, make charitable gifts of appreciated stock, or top off retirement accounts.

Of course, big life events—a major change in income, selling a business, receiving an inheritance—should trigger an immediate portfolio review. These moments can completely change your tax picture and demand a new strategy.

Can I Gift Stocks to My Kids to Avoid Capital Gains Tax?

Gifting appreciated stock to your kids or other family members in a lower tax bracket can be a very savvy move. But it's important to know that this strategy doesn't eliminate the tax—it shifts it.

When you gift an asset, the person receiving it also inherits your original cost basis. So, when they eventually sell the stock, they are on the hook for the capital gains tax. The savings come from the fact that their tax rate will likely be much lower than yours. For instance, if your child is in the 0% long-term capital gains bracket, they could potentially sell that stock and pay no federal tax on the gain whatsoever.

Just be mindful of the annual gift tax exclusion. For 2024, that's $18,000 per person. If you gift more than that to a single individual in one year, you might have to file a gift tax return.

At Commons Capital, we specialize in creating financial plans that are not only designed for growth but are also highly tax-efficient. If you're looking for guidance on how to reduce capital gains tax and make your wealth work smarter for you, we invite you to connect with our team. Explore how our expertise can help you achieve your financial goals at https://www.commonsllc.com.