Looking for a way to add tangible assets to your retirement plan? Buying real estate in an IRA is a powerful strategy that’s catching on with investors who want to diversify beyond the usual stocks and bonds. This investment approach happens through a Self-Directed IRA (SDIRA), which lets you purchase investment properties and watch the rental income and appreciation grow with significant tax advantages.

Why Put Real Estate in an IRA?

For a long time, retirement investing meant Wall Street. But savvy investors are increasingly looking for ways to diversify, and a Self-Directed IRA is the tool that makes it possible. While your standard IRA is limited to stocks, bonds, and mutual funds, an SDIRA opens the door to alternatives—and real estate is one of the most popular choices.

This isn't about buying your future beach house. This is a pure investment play. When you buy real estate in an IRA, you’re combining the wealth-building potential of property with the tax-sheltered growth of a retirement account.

Here’s how it works: all the rental income flows directly back into your IRA, and all property expenses—maintenance, taxes, insurance—are paid directly from the IRA. This keeps everything clean and allows the investment to grow tax-deferred (or completely tax-free, if you're using a Roth SDIRA).

The Key Players: Custodians and LLCs

To get this done, you’ll need two key partners. First is a specialized SDIRA custodian. Think of them as the gatekeeper—a financial institution that holds your SDIRA and makes sure everything stays compliant with IRS rules. They handle the paperwork and reporting, but they won’t give you investment advice.

Many investors also set up an LLC that is owned by their IRA. This popular setup, often called a "checkbook control IRA," gives you much more agility. Instead of waiting for the custodian to approve every transaction, you can write checks for repairs or deposit rent checks directly from the LLC's bank account. This speed is a huge advantage when you need to act fast on a deal or handle an urgent maintenance issue.

The appeal is undeniable. Real estate has become a go-to asset inside SDIRAs, largely because of the steady rental income it can produce. With single-family rentals yielding an average gross rental return of 7.55% annually, it’s easy to see why investors are drawn to this strategy. You can discover more 2025 real estate trends for SDIRAs to see what's on the horizon.

The most important rule to remember is that your IRA owns the property, not you personally. This separation is non-negotiable. It’s what keeps your account’s tax-advantaged status intact and helps you avoid harsh IRS penalties. Every transaction must be at "arm's length," meaning you can't personally benefit from the property until you start taking distributions in retirement.

Understanding this structure is the first step. Once you grasp these fundamentals, you’re on your way to building a more resilient and diversified retirement portfolio.

For a quick overview, here's a look at the main pros and cons you'll want to weigh before diving in.

IRA Real Estate Investing At a Glance

While there are certainly hurdles to clear, the potential for long-term, tax-sheltered growth makes IRA real estate investing a strategy worth considering for the right type of investor.

Building Your SDIRA Investment Foundation

Before you even think about scrolling through property listings, you have to build the right vehicle for the investment. Your standard brokerage IRA—the one holding your stocks and mutual funds—simply can't hold the title to a physical property. It wasn't built for that.

So, the first real step is setting up a Self-Directed IRA (SDIRA).

This means you’ll need to partner with a specialized SDIRA custodian. These aren't the household names you see advertising during the Super Bowl. These firms are specialists, designed from the ground up to handle alternative assets like real estate, private equity, and even precious metals. Picking the right one is a huge decision; they're your partner in making sure every move you make is compliant with IRS rules.

Selecting the Right SDIRA Custodian

Finding a good custodian is about a lot more than just the fees they charge. It’s about finding true expertise and reliable service. You want a team that gets the unique quirks of real estate deals happening inside a retirement account.

When you're vetting your options, here’s what to look for:

- Real Estate Know-How: Do they have a dedicated team that actually understands closings, titling, and how to manage property expenses? Ask them.

- Transparent Fees: Get the full picture. Custodians can charge for account setup, annual maintenance, and individual transactions. Make sure there are no surprises.

- Solid Customer Support: When you hit a snag or have a question, you need someone who picks up the phone and knows what they're talking about. Check reviews and get a feel for their service level.

Once you’ve picked your custodian and opened the SDIRA, it's time to get it funded. This is where you move the money you’ll use for your property purchase into the new account.

Funding Your Real Estate SDIRA

There are two main ways to get cash into your new SDIRA:

- Rollovers and Transfers: You can move money from an existing retirement account, like a 401(k), 403(b), or another IRA. A direct rollover is the cleanest way to do it. The funds go straight from one custodian to the other, never hitting your personal bank account, which is exactly what you want.

- Annual Contributions: You can also fund the account with new money, but you're limited by the annual IRA contribution limits set by the IRS.

The amount of money sitting in retirement accounts is massive. As of the first quarter of 2025, IRAs in the U.S. held an incredible $16.8 trillion in assets. A growing slice of that is being put to work by savvy investors using self-directed accounts to break free from the stock market. You can discover more insights about IRA asset allocation from the Investment Company Institute.

Key Takeaway: Every single penny used for the property—from the down payment to the property taxes to a new water heater—must come from within the SDIRA. Mixing in your personal money is a "prohibited transaction," and the IRS penalties are severe.

Gain Speed and Control with an IRA LLC

For investors who want to be able to move fast, the "checkbook control" model is the way to go. It sounds complicated, but it's pretty straightforward: you create a Limited Liability Company (LLC) that is 100% owned by your SDIRA. Your SDIRA then invests its funds into this new LLC.

This simple step puts you in the manager's seat. Instead of calling your custodian and waiting days for them to approve a payment for a contractor or send an earnest money deposit, you can just write a check directly from the LLC's business bank account.

Think about this real-world scenario: you're in a hot market and a great rental property just came up. It gets multiple offers in the first 24 hours. The seller is going to take the cleanest, fastest offer. With an IRA LLC, you can write the earnest money check right there in the agent's office. An investor who has to wait for their custodian to wire the funds might lose the deal before they even get a response.

That kind of speed can be the difference between landing a fantastic investment and walking away empty-handed. Nailing this foundation is the single most important part of getting ready to buy real estate with your retirement funds.

Avoiding Costly IRA Real Estate Mistakes

Jumping into real estate with your IRA without knowing the rules is like navigating a minefield blindfolded. The IRS has a strict set of guidelines around what they call prohibited transactions, and their entire purpose is to prevent you from getting any personal benefit from your retirement account before you actually retire.

A violation isn't just a slap on the wrist. If the IRS finds you’ve engaged in a prohibited transaction, the fallout is massive. Your entire IRA could be treated as distributed on the first day of the year the mistake happened, hitting you with a huge tax bill and early withdrawal penalties. A single misstep can vaporize years of hard-earned, tax-advantaged growth.

Who Is a Disqualified Person?

The core of these rules boils down to one concept: the disqualified person. This is a broad IRS definition designed to stop any kind of self-dealing. Simply put, the property your IRA owns can't be bought from, sold to, or benefit any of these individuals.

So, who's on this list?

- You and your spouse. This is the big one.

- Your direct family line. This means your parents, grandparents, children, and grandchildren.

- The spouses of your children. Yep, your son-in-law and daughter-in-law are included.

- Your IRA's fiduciaries. Think custodians and financial advisors connected to the plan.

- Businesses you control. Any corporation, partnership, or trust where a disqualified person owns 50% or more.

This isn't a gray area. Your IRA can't buy a house from your dad or sell it to your daughter. You can't even rent the property to your son for his college years, even if he pays fair market rent. The relationship itself makes the deal a non-starter.

The guiding principle here is to maintain an "arm's-length transaction." Every deal, every repair, every decision must be handled as if you were total strangers. Your IRA is a completely separate entity from you, and you have to treat its assets that way.

Real-World Scenarios of Prohibited Transactions

Legal definitions can feel a bit abstract, so let's bring this down to earth. Most investors get into trouble not because they're trying to cheat the system, but from a simple misunderstanding of how deep these rules really go. You absolutely cannot provide "sweat equity."

Imagine this: a tenant calls on a Friday night with a leaky faucet. Your gut instinct is probably to drive over and fix it yourself, saving a few hundred bucks on a plumber. This is a prohibited transaction. Your personal labor is seen as a contribution of value to your IRA, which is strictly forbidden.

Here are a few other common tripwires I've seen:

- Personal Use: Crashing at the property for a weekend while it's between tenants.

- Storing Your Stuff: Using the garage of your IRA's rental to store your old furniture.

- Paying Out of Pocket: Swiping your personal credit card for an emergency repair, planning to pay yourself back from the IRA later. All money must flow directly from the IRA.

- DIY Management: Personally managing the property, screening tenants, or even just mowing the lawn.

The only way to handle maintenance and management is to hire third-party, non-disqualified professionals and pay them directly from the IRA's checking account. Keeping a clean separation between your personal finances and your IRA’s assets is the bedrock of compliance. For more strategies on this, check out our guide on 3 ways to minimize your tax liability.

Common Prohibited Transactions and Permitted Actions

To make this crystal clear, I've put together a simple table comparing what you can and can't do. Think of this as your cheat sheet for staying on the right side of the IRS.

The line between a smart investment and a costly, irreversible mistake is absolute. By respecting the boundaries the IRS has set and treating your IRA's property as a truly separate asset, you'll protect its powerful tax advantages for the long haul.

Acquiring Your First IRA Investment Property

You’ve funded your Self-Directed IRA and you know the rules of engagement. Now for the exciting part—actually buying your first investment property. I have to be clear, though: the process is fundamentally different from a personal home purchase. Every single step, from finding the deal to signing on the dotted line, has to be executed with precision to keep your IRA compliant.

The property search itself will feel familiar. You'll analyze markets, run the numbers on potential cash flow, and do your due diligence just like any other real estate investor. The big difference comes when you’re ready to put in an offer.

Making a Compliant Offer

When you find a property that pencils out, the purchase offer must be made exactly right. The buyer on the contract can't be you. It has to be in the name of your IRA or, if you're using one, your IRA-owned LLC.

For instance, a standard purchase contract would list the buyer as:

- "[Custodian Name] FBO [Your Name] IRA [Account Number]" if you're buying directly through the custodian.

- "[Name of Your LLC]" if you’re using a checkbook control IRA.

This distinction is non-negotiable. It signals right from the start that this is an investment being made by a retirement account, not an individual. And it goes without saying, but all funds for the earnest money deposit must come directly from your IRA's bank account, not your personal checking.

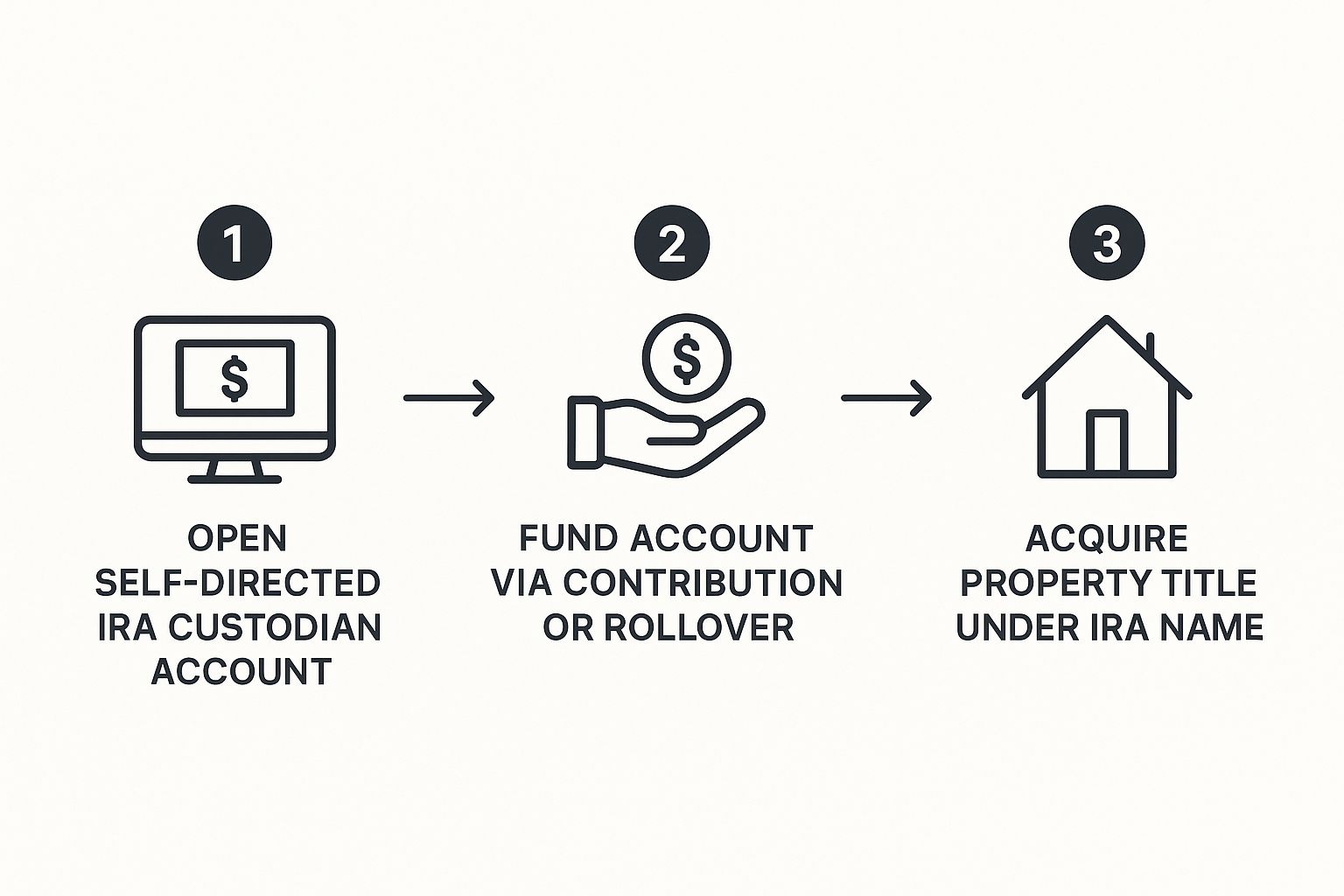

This flowchart lays out the basic steps for buying real estate in an IRA, from setting up the account to getting the keys.

As you can see, the core principle is that the property title must be held by the IRA, reinforcing the arm's-length nature of the transaction.

Demystifying IRA Real Estate Financing

A lot of investors think they need enough cash in their IRA to buy a property outright. While that’s certainly one way to do it, you can also get financing. But it's not the conventional mortgage you'd get for your own home. Your IRA has to use a non-recourse loan.

A non-recourse loan is a very specific type of financing where the lender’s only collateral is the property itself. If things go south and the loan defaults, the lender can seize the property, but they can't touch any other assets inside your IRA or come after you personally. This structure is mandated by the IRS to protect the rest of your retirement savings.

Lenders who specialize in these loans have different criteria than traditional mortgage providers:

- Higher Down Payments: You should expect to put down 30-40% of the purchase price.

- Property-Focused Underwriting: The lender is far more interested in the property’s cash flow and profit potential than your personal credit score.

- Higher Interest Rates: Because the lender is taking on more risk, the interest rates and fees are typically a bit higher.

Of course, interest rates have a major impact on whether a leveraged deal inside an IRA makes sense. For 2025, rates are expected to stay elevated, but some forecasts see a slight softening by year-end, with the average mortgage rate potentially landing around 5.9%. These shifts matter because your borrowing cost directly hits the cash flow and overall profitability of your rental. You can find more insights on 2025 real estate interest rate predictions on rentastic.io.

A Word of Caution: Using debt to purchase property in an IRA can trigger something called Unrelated Debt-Financed Income (UDFI). This income could be subject to the Unrelated Business Income Tax (UBIT). It's a complex area, and I strongly recommend talking it over with a tax professional before you move forward.

The Closing Process

As you head toward closing day, the same rule applies: all funds must come from the IRA. Your IRA custodian will coordinate with the title company to ensure all closing costs, prorated taxes, and the final purchase price are paid directly from your SDIRA.

At the closing table, you'll likely be the one signing the documents, but you’ll do so as the "manager" of the IRA LLC or under a power of attorney for the IRA itself—never as an individual buyer. The final deed will show the IRA or its LLC as the legal owner. This is the last critical step in buying real estate in an IRA and making sure your investment is structured correctly for tax-advantaged growth. Making sure the account is properly funded ahead of time is key; our guide on the backdoor Roth IRA conversion offers some great insights into maximizing your retirement account contributions.

Managing Your Property the Right Way

Once the closing papers are signed, your job description changes. You’re no longer just the buyer; you're the asset manager. But when you’re dealing with real estate inside an IRA, this isn't a hands-on side hustle. It's a hands-off investment, and that distinction is critical.

From this point forward, your number one rule is to maintain a strict financial firewall between your personal funds and your IRA's assets. Every dollar of rent that comes in and every dollar spent on repairs must flow through the right channels. Mixing funds isn't just sloppy bookkeeping—it's a prohibited transaction that could blow up your entire retirement account. Think of your IRA as a completely separate business with its own financial life.

The Financial Command Center: Your LLC Bank Account

If you went with the popular "checkbook control" model by setting up an IRA-owned LLC, your very next move is opening a dedicated business bank account in the LLC's name. This account is the heart of your entire operation.

This isn't just a good idea; it's a practical must-have for clean records and IRS compliance. Everything financial runs through this single account:

- Collecting All Income: Every rent check, late fee, or even quarters from a laundry machine gets deposited directly into this account. No exceptions.

- Paying All Expenses: The mortgage, property taxes, insurance, and that emergency plumbing bill—all of it must be paid directly from this LLC account.

This clear separation creates an undeniable paper trail, proving that all financial activity was handled at arm's length. That’s exactly what the IRS is looking for. A solid financial structure is the bedrock of a successful investment, and a well-thought-out plan makes all the difference. You can see how we approach building these kinds of robust strategies by exploring our approach to financial planning.

Hiring and Paying Third-Party Professionals

Since you can't swing a hammer or manage tenant calls yourself, you'll need a reliable team of third-party professionals. This usually means a good property manager and a roster of go-to contractors and handymen.

Just be careful who you hire. They can’t be "disqualified persons"—which means you can't hire your son's construction company, for instance. Payments also have to follow the rules: every invoice is paid by check or wire straight from the IRA LLC’s bank account. You can never pay a contractor from your personal checking account and plan to "reimburse yourself" later. That's a classic prohibited transaction.

Expert Tip: Have a very clear conversation with your property manager from day one. Make sure they understand the property is owned by a retirement account and that every single penny must flow through the designated IRA bank account. This simple step can prevent a lot of accidental compliance headaches.

Understanding Unrelated Business Income Tax (UBIT)

Now we get into one of the trickier parts of IRA real estate: the Unrelated Business Income Tax (UBIT). While rental income is usually considered passive and tax-free inside an IRA, taking on debt to buy the property changes the game.

If you used a non-recourse loan for the purchase, a portion of your net income is now classified as Unrelated Debt-Financed Income (UDFI). This slice of your profit is subject to UBIT, which is taxed at steep corporate or trust rates—often as high as 37%.

Here’s a simple way to think about it: the IRS views the profits generated by the bank's money (the loan) as active business income, not passive investment income. The tax is calculated based on the ratio of debt to equity. For example, if your property is 50% financed with a loan, then roughly 50% of your net rental income could get hit with UBIT.

This tax can take a serious bite out of your returns, so it’s absolutely essential to factor it into your financial models from the very beginning. It doesn't kill the deal, but it's a real cost you have to plan for.

Thinking About Your Profitable Exit Strategy

Every savvy real estate investor knows you make your money when you buy, but you realize it when you sell. When you're using an IRA to hold the property, having a crystal-clear exit plan from day one is non-negotiable. It's not just about selling at the top of the market; it's about making sure every last cent of profit flows back into your retirement account, ready to keep growing with those powerful tax advantages.

When you're ready to sell, the mechanics are basically the purchase process in reverse. As the manager of your IRA's LLC, you'll be the one listing the property, fielding offers, and negotiating the final price. But here’s the critical difference: at the closing table, the proceeds don't get wired to your personal bank account. They must go straight back into your Self-Directed IRA.

This is where the magic happens. A normal real estate sale could leave you with a hefty capital gains tax bill. But inside an IRA? No immediate tax bill. The entire profit—every single dollar of appreciation—stays sheltered inside your retirement account.

This means 100% of your earnings are immediately available to be rolled into the next deal, compounding your wealth at a pace that’s simply not possible in a taxable account.

Cashing Out When You Retire

Ultimately, the whole point is to turn these profits into retirement income. How you get your hands on the cash depends entirely on whether your SDIRA is a Traditional or a Roth account. Getting this right is the key to creating a tax-smart income stream for yourself down the road.

Here's a quick breakdown of how distributions work for each:

- Traditional SDIRA: When you start taking money out of a Traditional SDIRA in retirement (that’s after age 59½), those distributions are taxed as ordinary income. All those real estate gains that grew tax-deferred for years will finally be taxed at whatever your income tax rate is at the time you withdraw.

- Roth SDIRA: This is where things get really exciting. As long as you’ve had the Roth SDIRA for at least five years, all your qualified distributions are 100% tax-free. Yes, you read that right. The entire profit from your real estate investment can be pulled out without sending a dime to the IRS.

Think about it: you sell an IRA-owned property and walk away with a $200,000 profit. If that happened in a Roth SDIRA, the entire $200,000 can eventually become tax-free income in your pocket. In a standard brokerage account, you’d lose a big chunk of that to capital gains taxes right off the bat.

Planning your exit before you even buy helps you sync up your investment with your real financial finish line. When you know exactly how the proceeds will be treated and taxed, you can make smarter decisions that maximize what you actually get to keep and build a more secure retirement.

Burning Questions About IRA Real Estate

When you start digging into real estate investing with an IRA, a lot of specific questions bubble up. It's a powerful strategy, but the rules are strict. Let's tackle some of the most common questions investors ask when they're first getting started.

Can I Use My Existing IRA to Buy Property?

This is probably the most frequent question, and the short answer is no. You can't just call up your broker at a typical firm and use your standard IRA to buy a rental house. Those accounts are built for traditional assets like stocks and bonds, not physical property.

To get started with buying real estate in an ira, your first move is opening a Self-Directed IRA (SDIRA). You'll need to find a specialized custodian that handles these accounts. From there, you can fund your new SDIRA by rolling over money from an existing IRA or even an old 401(k) from a previous employer.

What If I Accidentally Use Personal Funds?

This is a huge one. Dipping into your personal checking account to cover an expense for your IRA-owned property—even a small one—is a major misstep. The IRS calls this a prohibited transaction, and it's a fast way to get into serious trouble.

This act of "self-dealing" can have disastrous consequences. The IRS could invalidate your entire IRA, treating it as if you cashed out the whole thing at once. That means immediate income taxes on the full value of the account, plus early withdrawal penalties if you're under 59 ½. One simple mistake could literally dismantle your IRA's tax-advantaged status.

Any personal use of an IRA-owned property is strictly forbidden. The asset must be held for investment purposes only. You, your spouse, your children, and other disqualified persons cannot live in, vacation at, or derive any personal benefit from the property at any time.

How Does Rental Income Work?

All the money your property generates has to flow directly back into the IRA. This means rent checks must be made out to the IRA, not to you, and deposited straight into the IRA's dedicated bank account.

The beauty of this is that the income grows within the IRA, either tax-deferred (in a Traditional IRA) or completely tax-free (in a Roth IRA). You don't pay income tax on that rental income year after year, which lets the cash compound and get reinvested much faster.

Navigating the complexities of buying real estate in an IRA requires expert guidance to ensure you stay compliant and maximize your returns. The team at Commons Capital specializes in structuring sophisticated investment strategies for high-net-worth individuals. To build a robust and compliant real estate portfolio within your retirement plan, contact us today.