Protecting older family members from financial scams is about more than just a single action. It requires building layers of defense through open conversations, smart legal planning, and using technology wisely. The goal is to create a collaborative system to spot trouble early, making it incredibly difficult for a scammer to isolate and exploit a loved one. This guide serves as your family's playbook for securing their financial future and provides actionable advice on how to protect seniors from financial scams.

The Soaring Threat of Senior Financial Scams

Financial scams targeting seniors have evolved far beyond simple cons. This is a sophisticated, multi-billion dollar criminal enterprise. These are not random acts of bad luck; they are calculated, psychological attacks designed to dismantle a lifetime of savings with terrifying speed. Understanding the risks is the first step in senior scam protection.

The numbers are staggering. The Federal Deposit Insurance Corporation (FDIC) estimates these scams drain $27 billion from older Americans every year, with the global damage soaring past $442 billion. In 2024 alone, the Federal Trade Commission (FTC) received 2.6 million fraud reports, and older adults represented the majority of reports for losses over $100,000.

This highlights a crucial point: falling for a scam has nothing to do with intelligence. Today's criminals are masters of manipulation, making financial literacy for seniors more important than ever.

Why Seniors Are a Prime Target for Financial Fraud

Several converging factors put older adults, especially those with significant assets, directly in the crosshairs of financial predators. Recognizing these vulnerabilities is key to building a stronger defense against elderly financial abuse.

- A Lifetime of Savings: They have spent decades building their nest egg through hard work, investments, and home equity. To a scammer, that represents a jackpot.

- A Generation of Trust: Many older adults were raised to be polite. It feels rude to hang up the phone abruptly or question someone who sounds like they're in a position of authority — a social norm that criminals exploit.

- Emotional Triggers: Loneliness, isolation, or the recent loss of a spouse can leave anyone vulnerable. Scammers prey on this, offering fake companionship or a sense of purpose through romance or lottery scams.

- The Technology Gap: While many seniors are comfortable online, they may not be as attuned to the subtle red flags of a phishing email, a spoofed banking website, or a malicious pop-up, which are common tactics for online scams targeting the elderly.

The most devastating scams don't play on greed; they play on trust and fear. A scammer's best weapon is manufacturing a crisis — a grandchild is in jail, an IRS bill is overdue, a "can't-miss" investment is closing now — to short-circuit rational thinking and force an immediate, emotional decision.

Protecting seniors from financial exploitation requires more than just a few warnings. It's about creating a robust framework of legal safeguards, practical tech tools, and, above all, a family culture where talking about money is open and completely non-judgmental. This guide will walk you through real, actionable steps to build that fortress.

Decoding the Tactics of Modern Financial Predators

To protect your family, you must first get inside the mind of the predator. Modern fraud isn't about clever tricks; it's a sophisticated assault on human psychology. Scammers are masters at manufacturing a sense of urgency, faking authority, or building an emotional connection to short-circuit a person's rational thinking.

They don't just ask for money. They weave compelling stories — an unexpected inheritance, a looming legal threat, or a "can't-miss" investment — all designed to trigger a powerful emotional reflex. Once you understand their manipulation tactics, you can spot the red flags of elder fraud long before a single dollar is at risk.

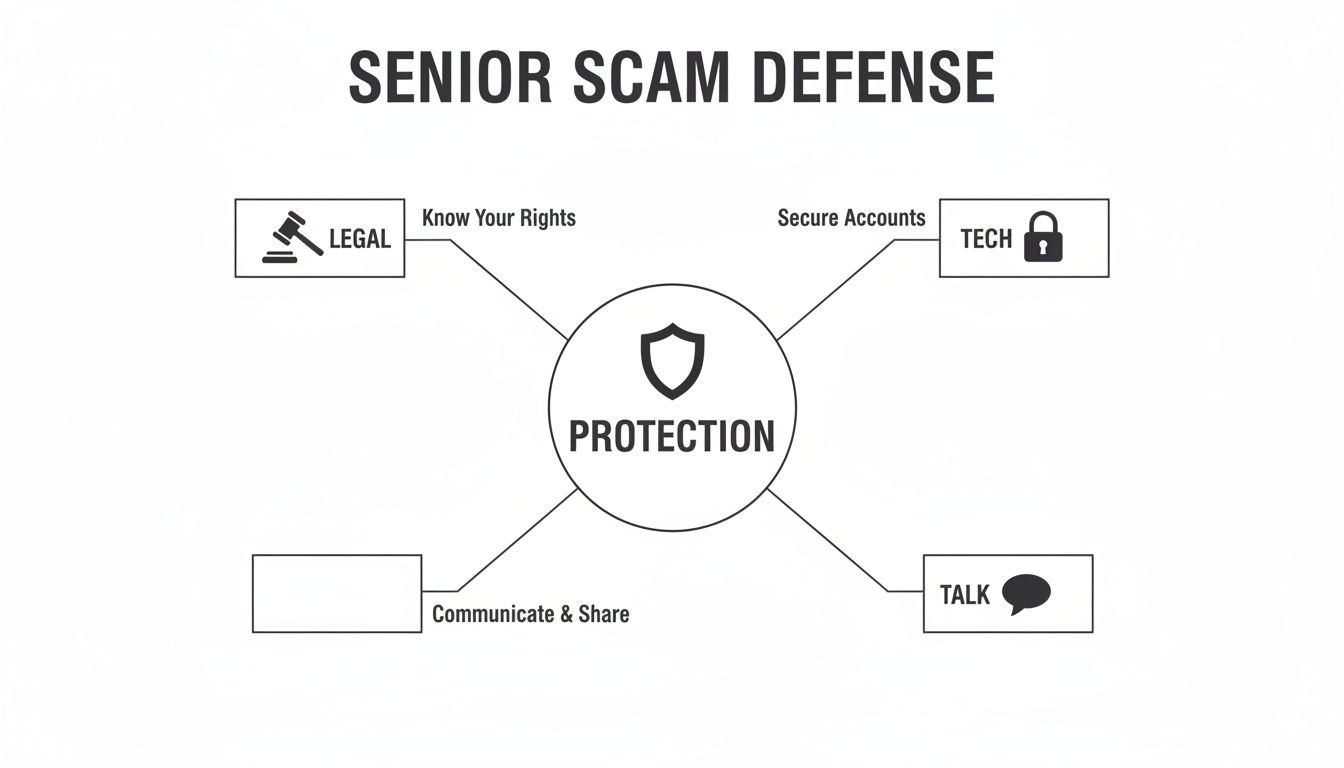

This diagram lays out the core pillars of a solid defense strategy against these criminals.

As you can see, a truly effective shield combines legal safeguards, technical controls, and honest communication. It’s not just one thing; it's a coordinated effort.

The Most Damaging Scam Categories

While the specific scripts change, the most devastating scams usually fall into a few key categories. The first step toward building immunity is recognizing their distinct flavors. Each one pulls on a different emotional lever, but the goal is always the same: to get to your loved one's assets.

Investment Scams

These schemes promise high, guaranteed returns with virtually no risk. Scammers create a powerful illusion of exclusivity, making the senior feel like they're being let in on a secret opportunity that the general public can't access.

A classic example is a fraudster who calls, posing as a wealth manager with a "time-sensitive" chance to get in on the ground floor of a revolutionary tech company or a pre-IPO stock. They'll have professional-looking websites and forged documents to build credibility, all while pressuring the target to act now before the "window" closes forever.

Government and Business Imposter Scams

This is one of the fastest-growing and most financially ruinous threats. Fraudsters will call, text, or email pretending to be from the IRS, the Social Security Administration, or a well-known company like Microsoft or Amazon. Their weapon of choice? Pure fear.

They might claim your parent owes back taxes and that a warrant is out for their arrest unless they pay immediately — often via wire transfer or gift cards. The psychological weight of someone impersonating a federal agent can be overwhelming.

The financial damage from these imposter schemes is staggering. The U.S. Federal Trade Commission (FTC) has seen reports skyrocket. Between 2020 and 2024, reports from adults over 60 who lost $10,000 or more shot up more than fourfold. Even worse, reports of losses over $100,000 increased nearly sevenfold in that same period. You can dig into more data on this growing threat and read about the latest trends in payments fraud.

Romance Scams

Perhaps the cruelest of all, romance scams prey on loneliness. A criminal creates a detailed, fake online persona and can spend weeks or even months building a deep, emotional connection with the senior.

Once that trust is cemented, the "emergency" hits. Suddenly, the scammer needs money for a medical crisis, a business deal that fell through, or a plane ticket to finally come visit. Because of that powerful emotional bond, the victim isn't sending money to a criminal; in their mind, they're helping someone they love.

Recognizing the Red Flags: A Comparison

It’s crucial to understand the subtle differences in how these scams work. One might weaponize fear while another uses affection, but they all share common warning signs of manipulation and fraud.

The table below breaks down the most frequent types of scams aimed at older adults, outlining the common tactics, emotional triggers, and key warning signs for each.

Common Financial Scams Targeting Seniors and Their Hallmarks

By internalizing these patterns, you and your family can stop being reactive and start being proactive. The goal is to recognize the scammer's script the moment they start reading from it, shutting them down before their tactics can take hold.

Building a Proactive Financial Fortress

Knowing about a threat is one thing, but building a system to shut it down is something else entirely. To truly protect seniors from financial scams, you must get ahead of the problem. That means ditching a reactive approach and creating structural and legal safeguards that act as a permanent fortress around their assets.

This isn't about taking away independence. It’s about designing a financial ecosystem with smart, pre-planned defenses. The goal is to make it incredibly difficult for a single moment of vulnerability to turn into a catastrophic loss.

Legal documents often thought of as just estate planning tools can become powerful weapons in the fight against fraud when set up correctly.

Legal Safeguards as Your First Line of Defense

Think of legal frameworks as the foundation of your fortress. They establish clear lines of authority and create a crucial backstop if a senior becomes unable to manage their finances, whether from cognitive decline or the immense pressure of a sophisticated scam.

Putting legal documents in place, like durable financial power of attorney forms, is a fundamental step. This document lets a designated agent — someone you trust implicitly — make financial decisions on their behalf. The key is to make it "durable," which means it stays in effect even if the senior becomes incapacitated.

Another powerful tool is a revocable living trust. While people often use these to avoid probate, a trust can also be a fantastic asset protector. By placing significant assets into the trust and naming a co-trustee (like an adult child or a professional fiduciary), you create a system where major financial moves require more than one person’s approval.

A Power of Attorney (POA) and a trust are not just for end-of-life planning. They are active, living documents that can be used to create a system of checks and balances, safeguarding wealth long before a crisis ever occurs.

Smart Account Structures for High-Net-Worth Families

For families with substantial assets, the sheer complexity of their financial life can be a vulnerability. Scammers love complexity; it creates blind spots. Simplifying and structuring accounts with security as the top priority can dramatically lower your risk.

One of the most effective strategies is account consolidation. Juggling investments and cash across a dozen different institutions is a recipe for disaster — it's nearly impossible to keep an eye on everything. By bringing assets under one trusted financial advisor or institution, monitoring becomes exponentially easier for everyone involved. A single, comprehensive view makes spotting unusual activity much faster.

Another practical tactic is to create a tiered account structure. It works like this:

- Primary Investment and Savings Accounts: This is where the bulk of the assets live. Lock these down with the strictest security protocols, including dual-signature requirements for any withdrawals or transfers over a set amount (say, $10,000).

- Operating Account: This is a separate, lower-balance checking account. Fund it monthly or quarterly with just enough to cover routine expenses like bills and groceries. It insulates the main nest egg. If this account is compromised, the potential loss is strictly limited to the smaller amount it holds.

This structure acts like a financial firewall. A scammer might breach the outer wall (the operating account), but the core assets remain secure behind much stronger, multi-layered protections. It’s a simple but remarkably effective way to contain potential damage.

By combining robust legal documents with thoughtfully structured accounts, you build a fortress that is resilient by design.

Using Technology as Your Financial Watchdog

Technology is often painted as the playground for scammers, but that's only half the story. When used correctly, technology can become your greatest ally — a vigilant, 24/7 watchdog protecting a senior's accounts.

This isn't about spying. It’s about creating a transparent, automated safety net that flags suspicious activity the moment it happens. Most modern banking platforms allow you to work with your loved one to set up a defensive perimeter that respects their independence while massively reducing their risk.

Activate Critical Account Alerts

Scammers thrive in silence. Your first move is to break that silence by making every financial move create a digital "ping." Go into the online banking portal and turn on every relevant notification the bank offers. These can be sent via text, email, or a push notification to multiple family members, creating an instant circle of awareness.

Start by setting up alerts for these specific triggers:

- Transaction Thresholds: Get an immediate notification for any withdrawal, purchase, or transfer over a set amount, like $200.

- Login Attempts: An alert for any successful or failed login from a new device or unrecognized location is a massive red flag and often the first sign of an account takeover attempt.

- New Payees: Set an alert for any time a new person or company is added as a payee. This can stop a scammer from inserting themselves into the system before they move money.

- Large Withdrawals: Any ATM withdrawal over a modest daily limit should trigger an immediate warning.

By turning these on, you shrink a criminal's window of opportunity from days or weeks down to just a few minutes.

Lock Down Digital Access

A strong password is a good start, but it’s nowhere near enough anymore. Multi-factor authentication (MFA) is the absolute, non-negotiable next step for every single financial account. It forces anyone logging in to provide a second piece of proof beyond the password, making it exponentially harder for a fraudster to get in.

But be aware — not all MFA methods are created equal.

The most common type of MFA sends a code via SMS text message, but this is surprisingly vulnerable to "SIM-swapping" scams. A much better option is an authenticator app (like Google Authenticator). The gold standard? A physical hardware security key like a Yubikey, which is nearly impossible for a remote scammer to bypass.

For families managing significant assets, it's worth having a direct conversation with a private banker. They can often set up bespoke rules, like requiring a phone call or a second family member's approval for any wire transfer. You can also look into specialized third-party services that use advanced algorithms to spot unusual financial behavior indicative of exploitation. For those interested, our insights on artificial intelligence and machine learning dive deeper into how this tech is being put to work for security.

Place a Freeze on Credit

This is one of the simplest yet most powerful proactive moves you can make. A security freeze, placed with the three major credit bureaus — Equifax, Experian, and TransUnion — locks down a senior’s credit file. This means if a scammer steals their personal information, they can't open a new credit card or take out a loan in their name.

It’s completely free, and the freeze can be temporarily lifted anytime your loved one needs to apply for legitimate credit. It’s a low-effort, high-impact defense that slams the door on identity theft and fraud.

The Power of a Coordinated Family Defense Team

While technology and legal documents are critical layers of defense, the strongest shield is a human one. Ultimately, the most powerful tool in your arsenal is a united, coordinated team of trusted people committed to protecting your loved one. Scammers succeed by isolating their victims, creating a high-pressure bubble where rational thought disappears. A coordinated team shatters that bubble.

This isn't about forming a committee to micromanage a senior’s finances. It's about a simple agreement among key people — like close family, a trusted financial advisor, and an attorney — to act as a sounding board for one another. This approach transforms scam prevention from a solitary burden into a shared responsibility.

Starting the Conversation Without Causing Conflict

Talking about money and vulnerability is never easy. Many adult children hesitate, fearing they'll make their parents feel patronized or as if their independence is being threatened. The key is to frame the conversation around teamwork and mutual protection against a common, sophisticated enemy.

Avoid any language that sounds accusatory. Instead of asking, "Has anyone suspicious called you?" try a more collaborative approach. You could share a news story about a recent scam and say, "These scams are getting so convincing. I think we should all agree on a plan to protect our family's finances."

Here are a few conversation starters:

- "I was just updating my own account security and it made me think. Could we spend a few minutes next week going over yours together to make sure everything is as secure as possible?" This frames the request as a routine financial health check-up, not a sign of distrust.

- "A friend's parent almost lost a lot of money to a very clever imposter scam. It got me thinking, we should probably have a simple rule in our family for any unexpected money requests." Using a third-party story introduces the topic without making it feel personal or threatening.

- "With everything being digital now, it's just smart to have more than one set of eyes on things. Would you be open to adding me as a 'read-only' user on your main accounts so I can help you watch for anything odd?" This is a great way to offer help that respects their control and autonomy.

Establishing the “Pause and Verify” Protocol

The single most effective strategy your team can implement is a simple but powerful rule: the 'pause and verify' protocol. Scammers win by creating urgency, making victims feel they must act now. This protocol is the perfect antidote.

The rule is straightforward: No unexpected or urgent financial request is ever acted upon without first discussing it with at least one other member of the trusted team. This could be a quick call to an adult child, an email to the financial advisor, or a question for the family lawyer.

This simple act of pausing creates the space needed for logic to overcome emotion. It breaks the scammer's spell of urgency and allows a second, calmer perspective to enter the situation, instantly exposing the fraud for what it is.

The nature of these threats makes a strong defense critical. Investment scams, for instance, are one of the top global threats, snaring 48% of scam victims. With consumers losing an estimated $442 billion to scams in the past year, the stakes are incredibly high. The most effective protection starts with a healthy skepticism of any unsolicited, high-return promise. You can discover more insights about the global state of scams in recent industry reports.

Building this trusted team, with a skilled advisor at its core, is a strategic imperative. If you're in the process of building this defense network, our guide on how to choose a financial advisor provides valuable insights for finding the right partner.

Your Top Questions on Senior Fraud Protection, Answered

Even with a solid plan, you're bound to run into specific situations that demand a quick, clear response. Let’s tackle some of the most common questions families have about protecting their loved ones from fraud.

What’s the Very First Step if I Suspect a Scam?

If you suspect a parent is caught in a scam, your immediate priority is to stop the financial bleeding.

The first call you make should be to their bank's fraud department. Work with your parent, calmly and without blame, to explain what's happening and ask them to place a temporary hold or a high-level alert on all their accounts. This one phone call can slam the door shut on any more losses.

Next, gather every shred of information you can find: names, websites, emails, phone numbers, and any transaction records. Report everything to the FBI's Internet Crime Complaint Center (IC3) and the Federal Trade Commission (FTC). Finally, bring your family's financial advisor and attorney into the loop to assess the damage and reinforce their financial defenses.

How Can I Talk About Scams Without Sounding Patronizing?

This is a tough conversation, but a critical one. The secret is to frame it as a team effort to fight a common enemy — the scammers — not as a judgment on your parent's abilities.

Avoid any language that might make them feel singled out. A great way to open the door is by sharing a news story about how even the sharpest people are being tricked by today's incredibly sophisticated scams.

Use "we" and "us" to build a sense of a shared mission.

For instance, you could say, "These fraud schemes are getting so sophisticated, I've been thinking it would be smart for us to review our financial security together to make sure we're all protected." When you introduce new safeguards like transaction alerts or a family "pause and verify" rule, position them as smart financial habits for everyone, regardless of age. You become an ally, not an accuser.

Local resources can also be a huge help. Attending scam and fraud prevention workshops together can provide the latest defense strategies in a supportive, neutral setting.

What Are the Most Effective Banking Features to Use?

Modern banking offers some fantastic digital tripwires. The most powerful tools are the ones that combine automated alerts with direct controls over how money moves.

Sit down with your loved one and turn on a full suite of custom email and text alerts for these key activities:

- Any transaction over a specific, modest amount (say, $500).

- All international wire transfers or payments.

- The creation of any new payee or bill-pay recipient.

- Any login attempt from an unrecognized device or new location.

For more complex financial situations, it’s worth a conversation with your private banker. They can often set up much stronger protocols, like requiring dual authorization for any wire transfer over a certain dollar amount. This means a second trusted person — like a Power of Attorney or advisor — has to sign off before the money goes out the door.

One of the best, non-invasive tools is read-only online access. Many banks let an account holder grant view-only permissions to a trusted family member. This is a brilliant solution that respects your parent's autonomy while giving you a crucial second set of eyes to spot trouble.

How Do I Protect a Fiercely Private Parent?

This is one of the trickiest and most common challenges. When a parent guards their financial information closely, direct intervention is off the table. The strategy here shifts to building a protective wall around their finances rather than getting inside them.

Start by sharing high-quality articles and resources about the latest scams. You’re just keeping them informed, not prying. You can also offer to help with their general digital security — things like installing good antivirus software, setting up a password manager, or putting a freeze on their credit reports. These are powerful protective layers that don't require you to see a single bank statement.

Ultimately, the most important safeguard for a private parent is a durable Power of Attorney for finances, legally executed and on file with their financial institutions. You may never need to use it. But just knowing that this legal backstop is in place provides an essential safety net if a scam or a health crisis ever leaves them vulnerable. It’s the ultimate protective measure that honors their privacy today while securing their future.

At Commons Capital, we believe that protecting your family's legacy is a collaborative effort that combines smart financial planning with proactive security measures. If you are navigating the complexities of wealth management and seeking a partner to help safeguard your assets, our team is here to provide the expert guidance you need.

Learn more about how we work with families to build a secure financial future at https://www.commonsllc.com.