Choosing the right financial advisor is one of the most significant financial decisions you'll ever make. But many people start their search in the wrong place: they jump straight into interviewing advisors. The process of how to choose a financial advisor should actually begin with a thorough self-assessment. Before you reach out to a single professional, you need to gain clarity on your own financial situation—your goals, your current standing, and what specific guidance you need. This initial introspection is the critical first step that will guide your entire search.

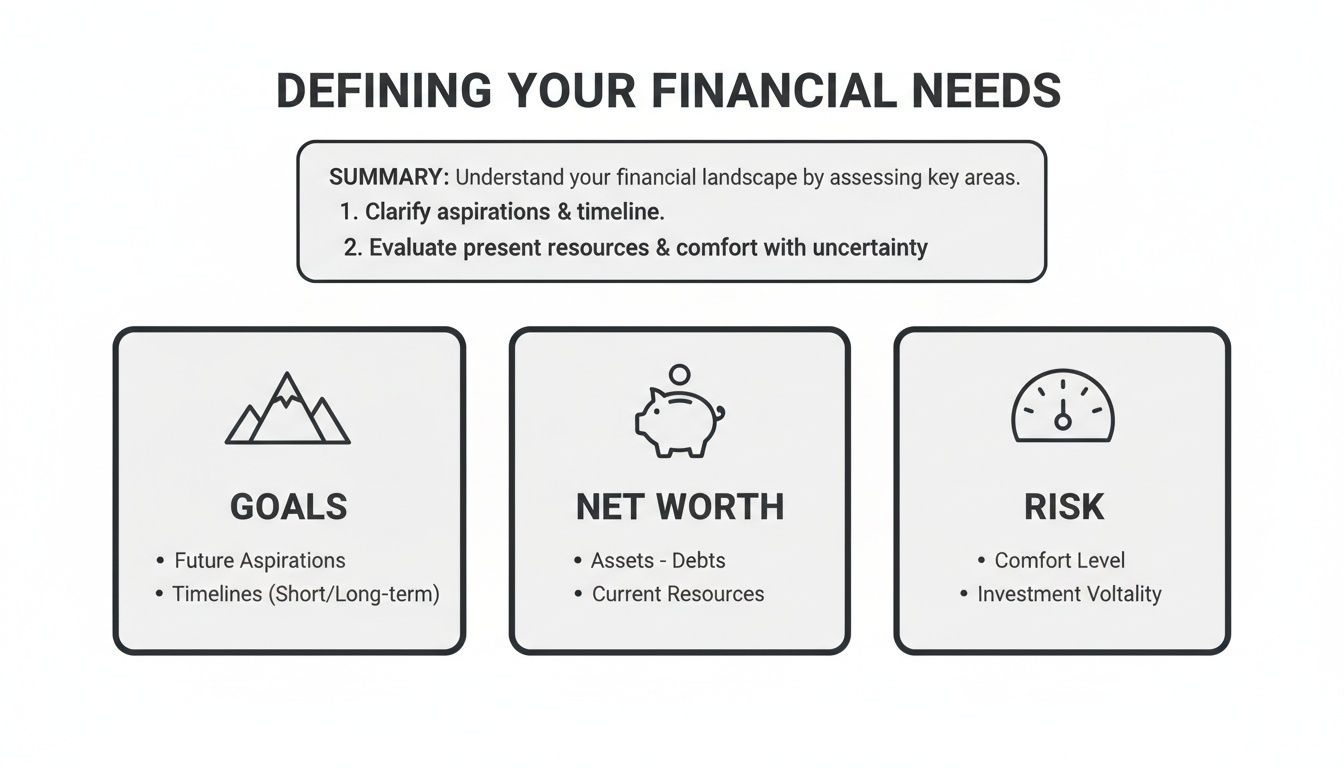

Defining Your Financial Needs Before You Start

Trying to find a financial advisor without first mapping out your own financial territory is like setting sail without a destination. You'll just drift. The most successful advisor-client relationships are built on a foundation of mutual understanding, and that starts with you knowing precisely what you want to accomplish.

So, before you even book a single meeting, take the time to conduct a serious self-assessment. This isn't just a quick glance at your bank account. It involves a deep dive into your ambitions, your current financial health, and your personal comfort level with risk. Documenting this information will not only make your search more efficient but will also empower you to find a true partner for your specific journey.

Articulate Your Specific Financial Goals

Everyone's financial goals are unique because everyone's life path is different. Are you aggressively growing your wealth for an early retirement, or is your primary focus on capital preservation for your children and grandchildren? Perhaps you've recently experienced a major liquidity event—like selling a business or receiving an inheritance—and need guidance on how to manage it wisely.

Think about what's really driving your search. It often falls into a few key areas:

- Retirement Planning: Determining the amount you need to live comfortably and creating a strategy to reach that goal.

- Estate and Legacy Planning: Ensuring your assets are transferred to the people and causes you care about efficiently and with minimal tax impact.

- Managing New Wealth: You've come into a significant sum from a business sale or inheritance. What are the next steps?

- Complex Compensation: Navigating the intricate world of stock options, RSUs, and other forms of equity compensation.

Pinpointing your primary goals helps you filter for advisors who have deep, proven experience in those specific areas. For example, an advisor who excels at generating retirement income might not be the best fit for an entrepreneur navigating a business exit. You need a specialist, not a generalist.

Assess Your Current Financial Standing

With your goals in mind, the next step is to get a sharp, accurate snapshot of where you stand today. This means calculating your net worth (what you own minus what you owe) and, just as importantly, identifying your investable assets. These are the funds you can actually put to work in the market.

A firm grasp of your net worth and investable assets is absolutely crucial. It helps you find firms that are structured to serve clients at your level, ensuring you receive the appropriate attention and expertise.

To get organized, you can use our financial planning worksheets to consolidate this information. Completing this homework provides a concrete baseline to share with potential advisors, making those initial conversations far more productive.

Understand Your Investment Philosophy

Finally, take a moment to reflect on your personality when it comes to money. Your investment philosophy is a blend of your risk tolerance and your general beliefs about how markets behave. Are you someone who can tolerate significant market swings for the chance at higher returns, or does the thought of a market downturn make you want to put your money under a mattress?

Ask yourself a few honest questions:

- How would I really feel if my portfolio took a 20% hit in a bad year?

- Am I more focused on long-term growth, even if it means short-term volatility?

- Do I care about ESG (Environmental, Social, and Governance) factors and want to avoid investing in certain industries?

Knowing your own mindset is key to finding an advisor whose strategy won't give you sleepless nights. It's all about alignment. If you're planning a major life change, like moving abroad, you have another layer of complexity to consider. Resources on financial preparation for expats can help you define those unique needs. Getting all of this sorted out first provides a solid foundation to start your search with confidence.

Understanding Advisor Credentials And Fee Structures

Once you’ve mapped out your financial world, the next step is to understand the advisor’s. The industry can feel like a maze of acronyms and confusing payment models, making it easy to get lost. However, breaking down these elements is key to finding a qualified professional whose interests are truly aligned with yours.

The financial advisory world is growing rapidly—projections indicate the profession will expand by 10.28% between 2019 and 2029, much faster than the average job. For high-net-worth families, this growth makes it even more critical to be discerning. With more advisors than ever, knowing how to identify those with the right expertise and resources is essential.

Decoding The Alphabet Soup Of Credentials

Not all financial advisors are created equal. Their credentials tell a compelling story about their qualifications, areas of focus, and commitment to professional ethics. For clients with substantial assets, certain designations are more than just nice-to-haves; they are essentials.

Here are a few of the most respected credentials you should look for:

- CFP® (Certified Financial Planner™): This is considered the gold standard for comprehensive financial planning. A CFP® professional has completed rigorous coursework, passed a demanding exam, and is bound by a strict code of ethics, including a fiduciary duty to their clients.

- CFA® (Chartered Financial Analyst®): This designation signifies deep expertise in investment management and portfolio analysis. If you require a sophisticated investment strategy, an advisor with a CFA® charter brings a superior level of analytical skill.

- CPA/PFS (Certified Public Accountant/Personal Financial Specialist): This is a powerful combination, merging the deep tax knowledge of a CPA with financial planning acumen. It is incredibly valuable for business owners, executives with complex compensation, or anyone with an intricate estate plan.

These aren't just letters after a name; they represent a significant investment in education and a commitment to a higher standard of practice.

The right professional will take your defined needs—your goals, net worth, and risk tolerance—and use their expertise to build a structured, actionable plan.

Understanding How Advisors Get Paid

This is where the rubber meets the road. An advisor’s compensation model directly impacts the advice you receive, and it’s vital to understand these structures to identify potential conflicts of interest before they become an issue.

There are three primary ways an advisor makes money.

Here’s a quick breakdown of the most common compensation models you'll encounter.

Comparing Financial Advisor Fee Structures

The takeaway is simple: how an advisor is paid reveals a great deal about their loyalties. A fee-only model generally creates the cleanest alignment, as the advisor’s revenue grows only when your assets grow.

The Fiduciary Standard Is Non-Negotiable

This brings us to the single most important concept in your search: the fiduciary standard. When an advisor operates as a fiduciary, they are legally and ethically bound to act in your best interest. Always. It is the highest standard of care in the financial industry, and for you, it should be a deal-breaker.

The alternative is the "suitability" standard, which only requires an advisor to recommend products that are suitable—not necessarily what is best. The difference is subtle but profound. A suitable product might have higher fees that pay the advisor a larger commission, while a better, lower-cost option is overlooked.

When you interview potential advisors, ask them point-blank if they uphold a strict fiduciary responsibility. Insisting on a true fiduciary ensures the advice you receive is untainted by competing incentives. To dig deeper, you can learn more about these crucial distinctions in our article on fiduciary financial advisor vs fee-only models. Making this a non-negotiable rule in your search is one of the most powerful moves you can make to protect your financial future.

How to Vet and Research Potential Advisors

You’ve compiled your shortlist of potential advisors. Now, the real work begins. Moving from a promising name on a list to a trusted partner requires methodical and serious investigation. This isn’t about gut feelings; it’s about conducting due diligence to ensure you’re placing your financial future in capable and trustworthy hands.

Think of this stage as your opportunity to look behind the curtain. Using publicly available information and official documents, you can build a crystal-clear picture of an advisor’s professional history, business practices, and any potential red flags. Let's walk through how to systematically narrow your list to only the most reputable professionals.

Use Regulatory Tools for Background Checks

The first, non-negotiable step is to verify an advisor’s credentials and check for any disciplinary history. Fortunately, financial regulators provide two essential, free tools that make this process straightforward.

- FINRA's BrokerCheck: This is a powerful database that provides a snapshot of an advisor's employment history, licenses, and—most importantly—any customer disputes, regulatory actions, or disciplinary events. A clean record on BrokerCheck is a fundamental requirement.

- SEC's Investment Adviser Public Disclosure (IAPD): This tool allows you to access an advisor's Form ADV, a mandatory registration document. It is packed with details about their business, fee structures, and any conflicts of interest.

Spending just a few minutes on each site can save you years of potential headaches. It's the financial world’s equivalent of a comprehensive background check, and it should not be skipped.

Request and Analyze the Form ADV Part 2

While the IAPD website provides the full Form ADV, I always recommend clients specifically request Part 2 (often called the "brochure") directly from any advisor you're seriously considering. This part is written in plain English and is designed to be a client-friendly disclosure of everything you need to know.

When you receive it, focus on these key areas:

- Services and Fees: It will explicitly state how they are compensated—whether it’s a percentage of assets, a flat fee, or another method.

- Conflicts of Interest: The firm must disclose any potential conflicts, such as receiving commissions for selling certain products.

- Disciplinary Information: It will detail any legal or disciplinary events involving the firm or its key personnel.

- Investment Philosophy: It outlines their general approach to investment strategy and analysis.

This document is your best friend when it comes to transparency. If an advisor is hesitant to provide their Form ADV Part 2 or if the information feels vague, that's a major red flag. Move on.

Evaluate the Firm’s Structure and Stability

Understanding the advisor’s firm is just as important as understanding the advisor. Are they part of a small, independent Registered Investment Advisor (RIA), or do they work for a massive global bank? The firm’s structure directly impacts the service you will receive.

It’s also important to be aware of industry trends. Wealth management is experiencing significant consolidation, with large institutions acquiring independent firms. While RIAs collectively manage over $125 trillion, this growth is increasingly concentrated among larger players, which can sometimes lead to a more standardized, less personal client experience.

Consider this: just 5% of advisors work at firms with fewer than 50 employees, while 29% work at giants with over 10,000 employees. If you are looking for a truly customized strategy, you need to understand how your advisor's firm structure might limit their ability to deliver it. You can discover more insights about independent advisor trends from NBC Securities.

Beyond size, investigate the firm's reputation. Look for reviews, press mentions, and the professional profiles of other team members on platforms like LinkedIn. This broader research helps you gauge the firm's culture and stability—both of which are key ingredients for a successful long-term relationship. As you dig in, you might also find our guide on finding a financial advisor near me helpful for local search tips.

By completing this vetting process, you’ll walk into the interview stage with confidence, knowing your candidates are credible, transparent, and well-regarded.

Key Questions to Ask a Prospective Financial Advisor

You've done the background checks, sifted through credentials, and narrowed the field. Now comes the most important part of finding the right financial advisor: the face-to-face meeting. This is where you go beyond paper qualifications and truly get a feel for the person you might be entrusting with your family's future.

Think of it less like a job interview and more like a series of strategic conversations. You’re not just hiring someone to manage money; you’re looking for a long-term partner. In fact, a PwC study found that 66% of high-net-worth investors want an advisor who truly understands the intricate dynamics of their career, family, and life goals.

This conversation is your chance to see if their philosophy and approach are a genuine match for your own.

Uncovering Their Investment Philosophy

Every advisor operates on a core set of beliefs that shapes their investment strategy. It's absolutely critical that their philosophy aligns with your comfort level with risk and your vision for the future. Don't settle for vague promises about "beating the market"—you need to hear the actual game plan.

Get straight to the point and ask about their strategy. Do they favor passive indexing, active management, or a combination? A great way to see their thinking in action is to ask how they would begin building a portfolio for someone in your exact situation. This moves the conversation from abstract theory to tangible application.

Here are a few questions I always recommend asking to dig deeper:

- How would you approach asset allocation for my family, given our specific goals? Their answer should feel personalized, not like they're pulling a generic model off the shelf.

- What’s your playbook when the market gets volatile? You're looking for a calm, disciplined, long-term perspective—not someone who makes reactive decisions based on headlines.

- What role, if any, do alternative investments play in your clients' portfolios? For those with significant wealth, this question can quickly reveal an advisor's sophistication with more complex assets.

Pay close attention to how they answer. Their explanations should be clear, confident, and understandable. If you leave the meeting feeling more confused than when you arrived, that’s a major red flag.

Assessing Communication and Client Service

The most brilliant financial plan is worthless if you can never get your advisor on the phone. A strong, lasting partnership is built on clear, regular, and proactive communication. Experience shows that when clients feel out of the loop, their confidence in their financial future plummets.

This is the time to set expectations for how the relationship will actually work. Go beyond asking about quarterly reports and dig into the day-to-day accessibility and support you can expect.

A great advisor demonstrates empathy and a comprehensive understanding of your unique situation, providing reassurance and unwavering support during life’s most challenging moments. These qualities lay the foundation for a lasting partnership built on mutual trust and genuine connection.

Get a clear picture of their service model with these questions:

- How often can I expect to formally review my financial plan and investments with you? The bare minimum should be annually, but many top advisors check in more frequently.

- Will I be working primarily with you, or will another team member be my main point of contact? It's important to know if you'll be handed off to a junior associate after signing on.

- What’s the best way to reach you, and what’s your typical response time? This simple question sets the ground rules for communication.

- How do you help your clients understand the strategies you're recommending? A top-tier advisor is also a teacher who empowers you with knowledge.

Their answers will tell you everything you need to know about whether they view clients as true partners or just another account.

Confirming Expertise and Fiduciary Commitment

Finally, you need to tie everything together. This is your chance to connect their credentials to your real-world needs and get a firm, unambiguous commitment to their ethical obligations.

Ask them to share their experience with clients who have faced situations similar to yours. Whether it’s navigating complex executive compensation, planning a business sale, or structuring a multi-generational wealth transfer, they should be able to provide anonymized examples of how they’ve guided others.

Now for the most important question of all. Even if you've already seen their fiduciary status in writing, ask them directly. Look them in the eye and ask:

- Are you a fiduciary at all times when working with me?

- Can you please put that commitment in writing for me?

The response should be immediate and unequivocal. A true fiduciary will not hesitate to say "yes." Any hedging, long-winded explanations about different standards, or attempts to change the subject is a deal-breaker. This single question cuts through all the noise and confirms that the advisor is legally and ethically bound to put your interests first. Always.

Finalizing Your Decision and Starting the Relationship

You’ve done the heavy lifting—the research, the vetting, the interviews. Now, you’re on the cusp of making your final choice for a financial advisor. This isn't just about signing a contract; it's about formalizing a partnership and laying the groundwork for the crucial first few months of the relationship.

Choosing the right advisor is about more than just a gut feeling. It requires a hard look at the legal agreement that will govern your partnership and a clear understanding of the firm's stability for the long haul.

Scrutinizing the Advisory Agreement

Before you sign anything, the advisory agreement deserves your undivided attention. This is a legally binding document detailing the entire scope of your relationship. Treat it with the same seriousness as any other major contract. Don't skim—read every single line.

Pay close attention to these key clauses that truly define the partnership:

- Scope of Services: Does the contract explicitly list every service you discussed? From investment management and tax strategy to complex estate planning, make sure it’s all included.

- Fee Schedule: The agreement must lay out exactly how fees are calculated and when they are billed. It needs to match what you were told verbally, with absolutely no surprises or hidden costs.

- Termination Clause: Understand how you can end the relationship if needed. Are there penalties or required notice periods? A transparent advisor makes this process clear and straightforward.

- Communication Standards: The contract might outline how often you'll meet and receive reports. Ensure this aligns with the expectations you set during your interviews.

If anything in the agreement seems confusing or doesn't reflect your conversations, this is your moment to ask for clarification or request changes. A trustworthy advisor will be happy to walk you through it and make adjustments.

What to Expect in the First 90 Days

The first three months are foundational. This is when your advisor transitions from a candidate to an active, integrated partner in your financial life. This onboarding phase is all about deep discovery and building the strategy that will guide you for years to come.

You should expect a highly structured process. Here’s what it typically looks like:

- Information Gathering: They will begin by methodically collecting all your financial documents—investment statements, insurance policies, tax returns, wills, and trusts.

- Financial Plan Development: Using this information, the advisor will construct the first draft of your comprehensive financial plan. This should be a collaborative process where they present it to you for feedback and refinement.

- Asset Transition: The advisor and their team will handle all the logistics of moving your assets from previous institutions to their firm’s custodian. This should be a seamless, behind-the-scenes process for you.

This period sets the tone for everything that follows. It should feel organized, collaborative, and entirely focused on turning your goals into a tangible, actionable plan.

Addressing the Critical Issue of Succession Planning

Here’s a crucial point that many people overlook: what is your advisor’s long-term plan? The financial advisory world is experiencing a massive demographic shift. A huge number of advisors are approaching retirement, and you need to know what happens to your accounts if yours decides to hang it up.

The industry is facing a talent crunch. A staggering 46% of advisors are planning to retire within the next decade. This generational shift means an estimated 110,000 advisors, who manage 42% of total industry assets, are expected to leave the workforce. You must ask about the firm's succession plan to ensure your wealth strategy has continuity. You can read the full research about advisor satisfaction and retirement trends to understand just how significant this issue is.

A firm with a well-documented succession plan isn't just thinking about its own future; it's demonstrating a deep commitment to its clients' long-term security. It proves your financial legacy is protected from disruption and managed by a team, not just one person.

Don't be shy. Ask direct questions about who would take over your account and what that transition process would look like. A solid plan gives you peace of mind, knowing your financial future is secure for generations to come.

Answering Your Lingering Questions About Choosing an Advisor

Even after doing your homework and sitting through a few interviews, some key questions tend to stick around. It’s completely normal. Choosing someone to manage your family's financial future is a major decision, and it's smart to want absolute clarity before you sign on the dotted line.

This is where we tackle those common, nagging questions head-on. Think of it as the final piece of the puzzle, designed to clear up any lingering uncertainty and help you move forward with confidence.

When Is It Actually Time to Hire a Financial Advisor?

This is probably the most common question I hear: "Do I really need an advisor yet?" There's no magic number that suddenly makes hiring an advisor necessary. The real signal is complexity. When your financial life starts feeling like a tangled web that you can't manage on your own time, that's your cue.

You’ve likely hit that point if any of these situations sound familiar:

- You're navigating a major life event. Selling a business, inheriting a substantial sum, going through a marriage or divorce, or planning your exit strategy for retirement are all game-changers. These moments create financial ripple effects that an expert can help you manage.

- Your compensation isn't just a simple salary. If you're dealing with stock options, RSUs, deferred compensation plans, or other forms of equity, a specialized advisor is crucial for maximizing their value and navigating the tax minefield.

- You're simply feeling overwhelmed. Are you losing sleep over market swings? Do you feel like managing your wealth has become a stressful, second job? If the time and energy spent on your finances are robbing you of your peace of mind, it’s a clear sign to bring in a professional.

Ultimately, the goal is to simplify your life, not just grow your assets. When managing your money starts to detract from enjoying it, that’s when you know it's time.

What Does "Fiduciary" Actually Mean for Me?

We've used the word "fiduciary" frequently, but what does it really look like in practice? It’s far more than a marketing buzzword; it's a legal and ethical promise that directly impacts the quality of advice you receive.

A fiduciary is legally required to act in your best interest, period. They must put your financial well-being ahead of their own compensation or their firm's bottom line. It’s the gold standard of care in our industry.

In your day-to-day relationship, this translates into a few key actions:

- Impartial Advice: A true fiduciary can't recommend an investment just because it pays them a higher commission. Their guidance must be based entirely on what's right for you.

- Radical Transparency: They are obligated to disclose any potential conflicts of interest. If a situation arises where their interests don't perfectly align with yours, they have to tell you upfront.

- Prudent Decision-Making: They must manage your assets with the skill and care that a seasoned professional would reasonably exercise in the same situation.

The fiduciary standard essentially takes the guesswork out of the equation. It provides the peace of mind that the advice you're paying for is untainted by hidden agendas. You know your advisor is sitting on the same side of the table as you.

What If I'm Not Happy with My Current Advisor?

This is a tough one, but it happens more often than you'd think. Maybe you've been with the same advisor for a decade, but the communication has fallen off, performance is lagging, or your family's needs have simply outgrown their capabilities.

If you have that nagging feeling that things aren't right, you need to listen to it. Your financial future is far too important to leave in the hands of someone who isn't a perfect fit. And here’s the good news: switching advisors is much less painful than most people imagine.

- First, get crystal clear on the problems. Pinpoint exactly what’s not working. Is it the communication style? The investment philosophy? The lack of proactive planning? Knowing this will help you find a new advisor who excels where your current one falls short.

- Next, follow the process in this guide to quietly interview and vet new candidates. There's no need to inform your current advisor at this stage.

- Once you've made your choice, your new advisor takes the wheel. They will handle all the transfer paperwork and logistics, making the transition as smooth and seamless as possible for you.

Remember, this is a professional relationship. Making a change to better serve your family’s goals isn’t disloyal—it's a smart, responsible business decision.

At Commons Capital, we are committed to providing the fiduciary-level guidance and specialized expertise that high-net-worth families deserve. If you're ready to partner with a firm that puts your interests first, we invite you to connect with us. Learn more about our approach.