If you're an entrepreneur approaching a major sale, a family managing wealth across generations, or an investor whose assets have become too complex for traditional wealth management, you've likely hit a turning point. You may be asking, "What is a multi-family office and do I need one?" You’re realizing you need something more — and that something might just be a multi-family office (MFO).

What Is a Multi-Family Office in Simple Terms?

Imagine a financial command center built exclusively for one of the world's wealthiest families. They have their own dedicated team of in-house experts handling every detail, from investments and taxes to estate planning and legal matters. That's a single-family office (SFO).

A multi-family office, or MFO, offers that same elite, all-in-one service, but it makes it accessible by serving a select group of high-net-worth families together.

Think of it like a financial "co-op." This model gives you the sophistication and power of your own private team without the immense overhead of building and staffing one from the ground up. For many, the need becomes clear when coordinating different advisors — lawyers, accountants, investment managers — starts to feel like a second full-time job. An MFO is designed to solve that problem.

The Purpose of a Multi-Family Office

An MFO exists to manage the entire scope of a family’s financial life, bringing strategy and execution together under one roof. Unlike a traditional advisor who might just focus on your portfolio, a true MFO ensures every piece of your financial puzzle fits together and works in harmony.

Typically serving between 10 to 50 unrelated families, an MFO provides a suite of comprehensive services while pooling resources to operate efficiently. Where an SFO is reserved for a single family, an MFO opens the door to this level of service for those with net worths often starting in the $25–$100 million range.

The real value of an MFO isn't just managing money; it's simplifying complexity. It replaces a scattered team of separate advisors with one cohesive, expert unit focused solely on your family's goals. It creates a framework that supports you today and for generations to come.

To help you see where MFOs fit in the broader landscape, here’s a quick comparison of the most common wealth management models.

Wealth Management Models at a Glance

This table shows that as wealth and complexity grow, the need for a more integrated and comprehensive service model increases significantly.

Who Is the Ideal Candidate for an MFO?

While every family's situation is different, a few common scenarios often act as a trigger, signaling it’s time to look into a multi-family office. If any of these sound familiar, the integrated support an MFO provides could be a game-changer for you.

- Entrepreneurs Nearing a Liquidity Event: Selling a business or going through an IPO creates sudden, massive complexity. An MFO helps structure the event for tax efficiency and builds a comprehensive plan for the proceeds before the ink is even dry on the deal.

- Families Managing Generational Wealth: When your goal is to preserve and grow wealth across multiple generations, an MFO brings the essential governance, education, and strategic planning needed to make it happen.

- Investors with Complex Global Assets: Juggling private equity, international real estate, hedge funds, and other alternative investments requires a level of oversight that most traditional advisors simply aren't equipped to handle.

These individuals and families need more than just investment advice; they need a true strategic partner. You can learn more about how our dedicated family office services address these specific and complex challenges.

The Core Services That Define a Multi-Family Office

Think of a multi-family office (MFO) less as a money manager and more as your family’s dedicated financial quarterback. Its real power isn't just in one service, but in how it pulls together all the pieces of your financial life that traditionally operate in separate silos. Instead of juggling a disconnected team of advisors, an MFO gives you a single, cohesive unit focused entirely on your family’s unique goals.

The services are built to cover every angle of a complex financial picture. It’s this all-in-one approach that moves beyond basic investment advice to create a truly unified strategy.

Investment Management and Consolidated Reporting

The foundation for most MFOs is a highly personalized investment program. This isn't just about managing a stock and bond portfolio; it's about orchestrating your family's entire balance sheet, from public markets to private, hard-to-access deals.

Key investment functions usually include:

- Asset Allocation: This means designing a strategy that perfectly aligns with your family’s goals, appetite for risk, and need for cash across every single account and entity you own.

- Access to Private Markets: MFOs provide due diligence and a pathway into institutional-quality private equity, venture capital, real estate, and private credit — opportunities that are typically out of reach for most individual investors.

- Consolidated Reporting: This is a crucial, and often overlooked, game-changer. Imagine getting a single, clear report showing your entire financial world. Instead of trying to piece together statements from different banks, brokerage accounts, and private investments, you get one unified snapshot of total assets, liabilities, and performance.

This holistic reporting transforms a scattered collection of assets into a clear, manageable picture. It allows for much smarter, more strategic decisions across the board.

For instance, if you're thinking about a major real estate purchase, you can see its impact on your total liquidity and asset mix in real-time — not weeks later after chasing down documents. This unified view is fundamental to managing significant wealth effectively.

Tax and Estate Planning

For families with substantial wealth, the number one priority is often preserving it for the next generation. MFOs excel at building and executing long-term strategies designed to minimize tax hits and ensure a smooth transfer of assets. Their approach is proactive, not reactive.

This goes far beyond simply drafting a will. MFOs coordinate with top legal and tax experts to put advanced techniques into action.

- Strategic Tax Planning: This could involve optimizing where your assets are held for tax purposes, managing capital gains, or structuring a business sale to drastically reduce your tax bill. The goal is to make tax efficiency a core part of every single financial move.

- Multi-Generational Estate Planning: MFOs help design and manage trusts, family limited partnerships (FLPs), and other sophisticated structures to pass wealth down efficiently. They also play a big role in preparing the next generation to handle the responsibilities that come with that wealth.

Multi-family offices also bring a level of sophistication to estate planning that is essential for complex assets, like cryptocurrencies, where a standard will often falls short. For anyone holding digital assets, it's critical to look into specialized crypto inheritance planning) to make sure they're managed and transferred correctly.

Family Governance and Lifestyle Management

Finally, a true MFO understands that wealth is about more than just numbers on a spreadsheet. It’s deeply tied to family dynamics and personal goals. They provide services that support the very human side of wealth.

Family Governance is all about creating a framework for making decisions as a family. This often involves educating younger generations about financial stewardship and running family meetings to get everyone aligned on a shared mission and set of values. Done right, this helps prevent conflict and makes sure the family's legacy lasts.

Lifestyle Management, sometimes called administrative services, handles the nitty-gritty financial complexities of daily life. This can include:

- Bill payment and managing cash flow.

- Philanthropic planning and running a family foundation.

- Risk management, which means reviewing insurance coverage for everything from property and liability to unique assets like art collections or classic cars.

By taking these critical but time-sucking tasks off your plate, an MFO frees up your time and mental energy to focus on what actually matters to you. It’s this blend of high-level strategic thinking and detail-oriented execution that truly defines the value of a multi-family office.

MFO vs. SFO vs. Traditional Wealth Management

When you’re managing significant wealth, the landscape of options can feel pretty crowded and confusing. It’s crucial to get a handle on how a multi-family office (MFO) is different from a private bank, a traditional wealth manager, or a single-family office (SFO). Each one has its own set of pros and cons, and the right choice really boils down to your family’s specific needs, complexity, and what you’re trying to achieve long-term.

A good way to think about it is through a simple home-building analogy. A traditional wealth manager is like buying a high-quality model home — it's efficient, well-built, and takes care of the standard needs, but you can’t really change the floor plan.

An SFO, on the other hand, is like hiring an architect to design and build a custom mansion from the ground up. You have absolute control over every single detail, but the cost, time, and sheer management headache are enormous.

A multi-family office (MFO) is the sweet spot in between: the semi-custom home. It gives you the sophisticated, personalized design and high-end features of a custom build but does it more efficiently. How? By sharing the foundational costs — the architect, engineer, and project manager — with a few other homeowners. You end up with a tailored result without having to build the entire operation from scratch yourself.

Comparing Costs and Customization

The biggest differences between these models really come down to two things: what you pay and how personalized the service is. A traditional wealth manager mostly sticks to investment management and some basic financial planning, charging a fee based on your assets under management (AUM). Their services are solid, but they're often standardized because they have to serve a wider client base.

At the complete opposite end of the spectrum is the single-family office (SFO). It offers unmatched customization and privacy because its entire staff — from the CEO and CIO down to the accountants and admins — works for just one family. But all that control comes with a hefty price tag. The operating costs for an SFO are the main reason they're really only practical for families with investable assets well over $250 million.

This is where an MFO strikes a powerful balance. By spreading overhead costs across several families, it can deliver a deeply personalized and integrated range of services at just a fraction of the cost of an SFO. This efficiency is exactly what makes the MFO model a smart, accessible solution for families who have outgrown traditional wealth management but don't need or want the expense of a private SFO.

Asset Thresholds and Breadth of Services

Often, the minimum asset level required is what decides which options are even on the table for you. While traditional advisors might work with clients who have $1 million to invest, MFOs generally serve families with $25 million or more in net worth. That higher entry point reflects the comprehensive nature of what they do, which goes far beyond just managing a portfolio.

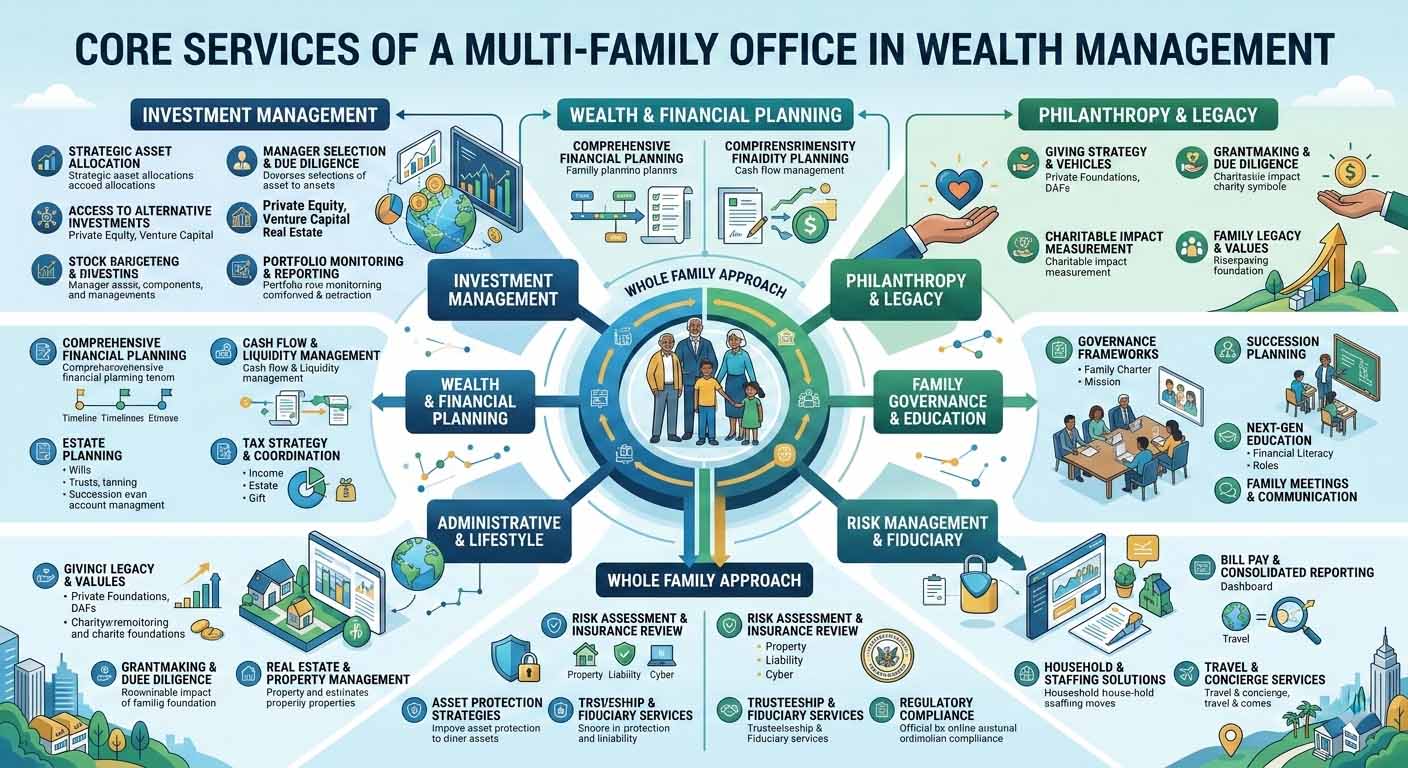

This infographic breaks down the core service areas of a multi-family office, showing how it pulls all the different financial disciplines together.

The diagram really shows how an MFO acts as a central hub, coordinating investment management, comprehensive planning (think tax, estate, risk), and even lifestyle services to create one unified strategy. For many high-net-worth families, this integrated approach is the key thing that sets it apart from other advisors.

The financial efficiency of an MFO becomes crystal clear when you look at operating costs. SFOs managing over $1 billion in assets can have annual operating costs averaging $6.6 million. Even smaller SFOs with under $250 million AUM can run close to $1 million a year. MFOs slash these figures by sharing talent and technology, which makes elite services realistic for families in the $25–$100 million range who are focused on long-term, multi-generational planning.

The core question is not just about assets, but complexity. If your needs involve coordinating multiple legal entities, intricate estate plans, private investments, and philanthropic goals, the integrated nature of an MFO offers value that a standalone wealth manager cannot replicate.

This is a key point to think about when you're deciding if a multi-family office is the right fit. For those who want a deeper look at some of the foundational services that overlap, you might find our guide on the essentials of private wealth management helpful.

Ultimately, choosing between these models is all about finding the right balance of customization, cost, and comprehensive oversight that fits your family’s unique financial journey.

When Do You Need a Multi-Family Office? A Practical Checklist

It's one thing to talk about multi-family offices in theory. But how do you know if your financial life has actually hit the point where one makes sense for you?

This isn't about hitting a specific net worth number. It's about complexity. I've built this checklist around the common growing pains I see that signal it's time for a more integrated approach. If you find yourself nodding "yes" to several of these points, there’s a good chance you’ve already outgrown traditional wealth management.

MFO Suitability Checklist

Use this checklist to evaluate if your financial complexity and goals align with the services of a multi-family office. The more checks you have, the more likely an MFO is a good fit.

If you've checked off several boxes, it’s a strong signal. You’re likely dealing with a level of complexity where the fragmented, traditional model starts to break down, and the integrated, holistic approach of an MFO becomes not just a luxury, but a necessity.

How to Choose the Right Multi-Family Office for Your Family

Picking a multi-family office (MFO) is one of the most critical financial decisions your family will ever make. This isn't just about hiring another advisor. You’re choosing a long-term partner who will be deeply woven into your family's financial and personal life for years, maybe even generations, to come.

So, where do you start? Before you even think about interviewing firms, the most important work happens internally. Your family needs to get on the same page about its mission, its core values, and what you all consider non-negotiable. Is the top priority preserving wealth across generations, or is it about making the biggest philanthropic splash possible?

Getting that internal clarity is your compass for the entire process. It’s what moves you from just asking "what is an MFO?" to defining what the right MFO looks like for your family.

Vet Their Expertise and Experience

Once your family’s priorities are crystal clear, it’s time to start rigorously assessing a firm's hands-on experience. Don’t get distracted by a glossy brochure or a slick presentation. You need stone-cold proof that they have successfully handled situations just like yours.

A firm’s track record is everything. It’s the strongest signal you have of their ability to manage your specific, complex needs.

Dig in with pointed questions. Have they dealt with:

- Concentrated stock positions from a major business sale or years of executive compensation?

- Cross-border assets and the tangled web of tax rules that come with them?

- Complex family dynamics, like bringing the next generation up to speed or mediating different goals?

- Unique investments such as private equity deals, real estate developments, or venture capital funds?

A team that has “seen it all before” is going to be far more valuable than one learning on the job with your family’s money. Their answers should be specific, detailed, and backed up by real-world stories of how they’ve helped other families.

Scrutinize Fees and Fiduciary Duty

You absolutely have to understand how an MFO makes its money. This is non-negotiable, as it ensures their interests are truly aligned with yours. The two most common models are a fee based on assets under management (AUM) or a flat retainer. AUM is a percentage of the assets they manage for you, while a retainer is a fixed annual cost, usually tied to your family's complexity.

The single most important question you can ask is: "Are you a fiduciary 100% of the time?" A true fiduciary is legally and ethically bound to act in your best interest. That's the gold standard in this business.

This commitment is your best defense against conflicts of interest, like a firm pushing a product simply because they get a kickback for selling it. For a more detailed script, our guide on the essential questions to ask a wealth manager can give you a solid framework for this critical conversation.

Conduct Thorough Due Diligence

The final stage is a deep dive into the firm's culture, team, and client relationships. This is where you move beyond the "what" and get to the "who."

Key Due Diligence Steps:

- Interview Key Team Members: Don't just meet the lead advisor. Insist on talking to the specialists in tax, estate planning, and investments who you'll be working with day-to-day.

- Check Client References: Ask to speak with at least two or three current clients with situations similar to yours. Ask them the tough questions about communication, proactivity, and how the firm handles problems when they arise.

- Assess Cultural Fit: Remember, this is a long-term partnership. Does their communication style, their values, and their general vibe feel like a natural fit for your family? Trust your gut.

Taking the time to walk through this process will empower you to move from simply understanding what an MFO is to confidently choosing the right long-term partner for your family's future.

Common Questions About Multi-Family Offices

As you start to picture what working with a multi-family office might look like, a few practical questions always come to mind. We get these all the time from families exploring this world for the first time, so let's get you some quick, clear answers.

What Does a Multi-Family Office Typically Cost?

Most MFOs use a fee structure based on a percentage of your assets under management (AUM). You can generally expect this to be somewhere in the range of 0.50% to 1.00% per year. That percentage often gets smaller as your assets grow.

Some firms, particularly those that handle a lot of administrative and lifestyle support, might charge a flat annual retainer instead. This is usually based on how complex your family's situation is, not just your portfolio size, which gives you predictable costs no matter what the market is doing. The key is to get a completely transparent breakdown of what you're paying for.

Can I Keep My Existing Advisors if I Join an MFO?

Yes, in many cases, you absolutely can. A good MFO understands the value of relationships you've built over years with a trusted CPA or attorney. They often step in to act as the "quarterback," coordinating with your existing team to make sure everyone is aligned and working from the same strategic playbook.

It’s worth noting, however, that some MFOs prefer to handle everything in-house. They believe it creates better efficiency and focus. You’ll want to ask about their specific approach during your initial conversations to make sure it aligns with what you want.

The entire point of a multi-family office is to simplify your life, not make it more complicated. A quality MFO will work with you to find a model — whether it's collaborative or fully integrated — that genuinely serves your family and honors the relationships you already have.

Is My Net Worth High Enough for an MFO?

There isn't a single magic number, but most MFOs start looking for a minimum of around $25 million to $30 million in investable assets. That threshold is there because it allows the firm to deliver the incredible depth of service that defines what an MFO really is.

That said, some are flexible. They might make an exception if your financial life is particularly complex or if you're about to have a major liquidity event, like selling your business. It's often less about a hard-and-fast number and more about whether your situation has reached a level of complexity that needs the kind of integrated oversight an MFO provides.

What Is the First Step to Engage with an MFO?

It all starts with a discovery call or meeting. Think of it as a no-pressure conversation where you get to lay out your family's situation, what you're trying to achieve, and what's causing you headaches right now. It's just as much an opportunity for you to size them up and learn about their philosophy and expertise.

You should be ready to talk about:

- Your current financial picture and how complex it is.

- Your long-term goals for your wealth, from preservation and growth to your family's legacy.

- The challenges or frustrations you’re having with your current setup.

If it feels like there’s a good fit on both sides, the next step is usually a deeper dive where the firm gathers the details needed to put together a formal proposal.

At Commons Capital, we know that navigating the world of significant wealth is complex. If you think your family might be ready for a more strategic and unified approach, we'd welcome a conversation. Learn how our advisory services can bring clarity and confidence to your financial future.