For decades, the 4 percent rule was a bedrock principle of retirement planning. The guideline is simple: withdraw 4% of your portfolio in your first year of retirement, then adjust that amount for inflation each year after. But what was once a cornerstone is now seen by many experts as a relic. Increasingly considered outdated, the 4 percent rule often fails due to modern market volatility, persistent inflation, and longer lifespans, making it a rigid formula that’s dangerously out of step with the realities modern retirees face.

What Is The 4 Percent Rule And Why Is It Flawed?

Think of your retirement savings as a large reservoir of water that has to last the rest of your life. The 4 percent rule was meant to be a simple, reliable valve on that reservoir, letting you draw a predictable stream of income over a 30-year horizon without running the tank dry.

The concept came from a 1994 analysis by financial advisor William Bengen. He dug into historical U.S. market data going all the way back to 1926 and found that a 4% initial withdrawal rate, with annual inflation adjustments, held up remarkably well. For example, if you retired with a $1 million portfolio, you’d take out $40,000 in year one. If inflation hit 3%, your next year's withdrawal would be $41,200. The idea gained even more traction after the famous 1998 Trinity Study, which confirmed high success rates and cemented the rule’s legacy for a generation of financial planners.

Cracks in the Foundation

Despite its simple appeal, relying on the 4 percent rule today is like navigating a modern highway using a map from the 1990s. The economic world has changed. The rule was born from a specific slice of U.S. history, a period of market performance and interest rates that may not repeat.

The core problem with the 4 percent rule is its rigidity. It operates like a fixed program, failing to adapt to the dynamic and unpredictable nature of modern financial markets and longer human lifespans.

This inflexibility is its greatest weakness. It assumes retirement is a straight, predictable line, but anyone who has lived through the last twenty years knows it’s anything but.

To put this in perspective, here’s a quick summary of how the original thinking stacks up against today’s environment.

The 4 Percent Rule At A Glance

This table makes it clear: the assumptions that made the rule work in the past are the very things we can no longer take for granted.

Modern Challenges to an Old Rule

So, why exactly does this old rule of thumb fall short today? It comes down to a few critical blind spots that can create a false sense of security.

- Market Volatility: The rule forces you to sell assets and withdraw the same inflation-adjusted amount, even when the market is crashing. Selling low crystallizes losses and can permanently cripple your portfolio’s ability to recover.

- Persistent Inflation: Bengen’s model was tested against past inflation. But an unexpected period of high, sticky inflation can make your planned withdrawals feel smaller and smaller, gutting your actual purchasing power.

- Longer Lifespans: People are simply living longer. A plan built for a 30-year retirement becomes a high-stakes gamble when you might need your money to last 35 or even 40 years. The risk of outliving your assets is very real.

- Ignoring Taxes: This is a huge oversight. The rule focuses on the gross 4% figure. It completely ignores that withdrawals from tax-deferred accounts like a 401(k) or traditional IRA are taxable income. Your net withdrawal—the money you can actually spend—is always less.

Why The 4 Percent Rule Is Failing Modern Investors

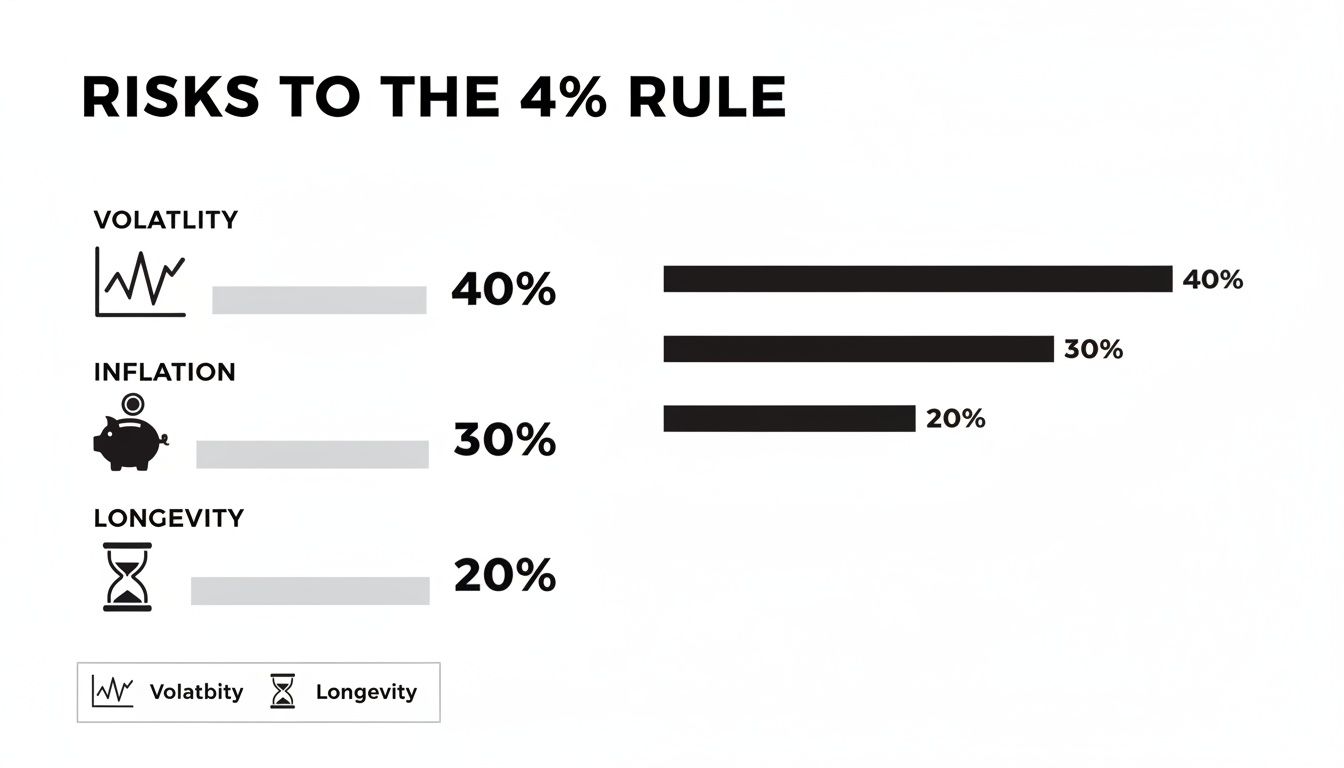

For decades, the 4 percent rule felt like a comforting guarantee—a simple roadmap for retirement. But what worked for previous generations is now cracking under the pressure of today's economy. The truth is, this rigid, one-size-fits-all approach was never built for the world we live in now. Relying on it today introduces serious, and often hidden, risks for anyone planning a retirement that could last for decades.

The rule’s biggest problem is that it can't adapt. It’s a fixed program: withdraw the same inflation-adjusted amount every single year, no matter what’s happening in the market or with your life. This robotic process completely ignores three of the biggest threats facing modern retirees.

The Triple Threat to Fixed Withdrawals

First, we have heightened market volatility. Imagine trying to pull out your scheduled income during a steep downturn, like in 2008 or more recently in 2022. The 4 percent rule doesn't care. It forces you to sell off more of your portfolio when prices are at their lowest just to get the cash you need.

This is one of the fastest ways to destroy a nest egg. You’re locking in losses and permanently depleting the capital you need to recover when the market finally turns around. That damage, especially in the early years of retirement, can be impossible to undo. Experts have a name for this: sequence of returns risk. You can see just how a few bad years at the start can derail an entire plan in our guide on sequence of returns risk in retirement planning.

Second, there’s corrosive inflation. The rule was built using historical US inflation data, which, for long stretches, was pretty mild. But as we’ve seen recently, a burst of high inflation can shrink your purchasing power much faster than anyone planned. A $50,000 withdrawal might feel comfortable one year, but its real-world value can be slashed just a few years later, forcing you to make painful cuts to your lifestyle.

Finally, we’re all living longer. When the rule was created, a 30-year retirement was the standard. Today, thanks to better healthcare, retirements lasting 35, 40, or even 45 years are becoming common. Trying to stretch a portfolio built for 30 years over a 40-year timeline dramatically raises the odds of running out of money. The "safe" withdrawal rate suddenly becomes a high-stakes bet.

Dangerous Blind Spots of the 4 Percent Rule

The 4 percent rule is an oversimplification with dangerous blind spots. It lacks flexibility, assumes your expenses are linear, ignores the crucial impact of taxes, and fails to account for fluctuating market returns. This rigidity creates a tangible risk of outliving your assets. This lack of nuance gives retirees a false sense of security, as the rule completely misses several factors that determine how much money you actually have to live on.

- Ignoring Taxes: This is probably the rule's single biggest flaw. It calculates a pre-tax number. If you pull $100,000 from a traditional IRA or 401(k), you don't get to spend $100,000. A hefty chunk of that is going straight to the IRS and your state, leaving you with far less income than you planned for.

- Assuming Linear Expenses: The rule thinks your spending will be a perfect, straight line that only goes up with inflation. Real life isn't like that. People often spend more in their early, active retirement years on travel and hobbies, while later years can bring sudden, massive healthcare costs that a straight-line budget can't handle.

- Inability to Adapt to Market Returns: A fixed rule can’t react to reality. If your portfolio has an incredible year and grows by 15%, the rule doesn't let you take a little extra. More importantly, if your portfolio drops 20%, the rule still makes you sell assets at the worst possible time, digging the hole even deeper.

At the end of the day, the 4 percent rule is a relic from a different financial era. It just can't account for today's market volatility, tax realities, variable spending, and longer lifespans, making it an unreliable guide for modern investors.

The Global Failure Of The 4 Percent Rule

The 4 percent rule has a dirty little secret: it was born and raised entirely in the United States. Its entire framework is built on the historical performance of U.S. stocks and bonds during a century of unprecedented economic dominance. For anyone with a global portfolio, simply taking this rule and applying it elsewhere is a massive gamble.

When you actually test the rule on the world stage, it doesn't just bend—it breaks. The assumption that what worked in a booming 20th-century America would work just as well in other developed countries is flat-out wrong. In reality, sticking to a rigid 4% withdrawal rate in many other major economies would have been a recipe for disaster.

When The Rule Collapses Abroad

To see just how fragile the rule is, you don't have to look far. Imagine you were a retiree in Japan at the start of the 1990s. The Nikkei index was at its peak, but what came next was decades of economic stagnation, famously known as the "Lost Decades." Someone following the 4 percent rule would have been selling their assets into a falling market, year after year, watching their nest egg evaporate with no end in sight.

It's not an isolated case. Think about a retiree in Germany trying to survive the hyperinflation of the 1920s, or one in the United Kingdom during the 1970s, when high inflation and low growth created a toxic "stagflation" environment. An inflation-adjusted withdrawal plan would have forced them to pull out huge, ever-increasing sums of cash just to buy groceries, gutting their portfolio in just a few years.

These aren't some obscure what-if scenarios; they are the real financial histories of some of the world's biggest economies.

As you can see, the rule gets squeezed from all sides. Market volatility, runaway inflation, and the simple fact that we're living longer all put immense pressure on a strategy that was never built to handle them all at once.

U.S. Exceptionalism: A Dangerous Bet

Basing your retirement plan on U.S. market history is really a bet on "American exceptionalism"—the idea that its markets will always bounce back stronger and outperform the rest of the world. That’s a shaky foundation for anyone's future, especially for a globally diversified investor. The whole point of diversification is to protect yourself when one region falters. Chaining your entire strategy to one country's lucky streak goes against that very principle.

The numbers tell an even starker story. While the 4 percent rule has a decent track record in historical U.S. simulations, it fails spectacularly when applied internationally. A landmark 2010 study that looked at 20 different countries found that the maximum safe withdrawal rate was actually below 3% in more than half of them.

In countries like Spain, Germany, France, and Italy, trying to pull out 4% a year resulted in a failure rate of over 50%. As detailed in the full research on international withdrawal rates, even in high-performing markets like Australia, the safe rate barely scraped by, landing just under 4%.

This data proves that the 4 percent rule is not a universal law of finance. It is a guideline derived from a specific, and potentially unrepeatable, set of historical circumstances in a single country.

At the end of the day, sophisticated wealth management requires a tougher, more globally-minded strategy. The success of the 4 percent rule in the U.S. looks more like a fortunate outlier than a reliable blueprint. For high-net-worth individuals with assets scattered across the globe, betting that this luck will hold isn't a strategy—it's just a risk you don't need to take.

Dynamic Withdrawals: The Smarter Alternative

The biggest problem with the 4 percent rule is its inflexibility. If the rule is a fixed light switch—always on, always drawing the same power—dynamic strategies are more like a smart thermostat, intelligently adapting to the financial weather.

Instead of blindly following a preset formula, these flexible approaches adjust your withdrawal amounts based on what’s actually happening with your money. This offers a far more resilient path through retirement.

These modern strategies move away from the "set it and forget it" mindset, acknowledging that both markets and life are unpredictable. Rather than forcing you to sell assets into a downturn, they give you a framework to reduce withdrawals when your portfolio is struggling and potentially take more when it's thriving. That responsiveness is what preserves capital for the long haul.

The Guardrails Approach

One of the most practical dynamic methods is the "guardrails" strategy. Think of it like bumpers on a bowling lane; they keep your financial plan from veering into the gutter. This approach sets upper and lower bounds for your withdrawal rate, creating a safe corridor for your spending.

It starts with a target withdrawal rate, maybe 4%. Each year, you recalculate this rate based on your portfolio's current value.

- If the market has performed well and your new withdrawal rate drops below a lower guardrail (e.g., 3.2%), you give yourself a "raise" by increasing your withdrawal amount by a set percentage, like 10%.

- If the market has performed poorly and your new rate rises above an upper guardrail (e.g., 4.8%), you take a "pay cut" and reduce your spending by 10%.

- If your rate stays within the guardrails, you simply adjust last year's withdrawal for inflation, just like the traditional rule.

This method helps prevent two of the biggest dangers: selling too many shares when your portfolio is down and failing to benefit from strong market performance. It provides a logical, rules-based way to be flexible without making emotional decisions.

Variable Percentage Withdrawal (VPW)

Another powerful alternative is the Variable Percentage Withdrawal (VPW) method. This strategy is more directly tied to your portfolio's value and your remaining life expectancy. Each year, you withdraw a specific percentage of your current portfolio balance, with the percentage determined by a table similar to those for Required Minimum Distributions (RMDs).

For instance, at age 65, the table might tell you to withdraw 3.8% of your portfolio. If you have $2 million, that’s $76,000. But if the market drops and your portfolio is worth $1.8 million the next year, at age 66 the table might suggest a 3.9% withdrawal. That would come out to $70,200, automatically adjusting your income downward to protect your principal.

The core principle of dynamic withdrawals is simple: tie your spending to your portfolio's real-time ability to support it. This creates a self-correcting system that dramatically reduces the risk of running out of money compared to the rigid 4 percent rule.

These strategies offer a more realistic framework for generating retirement income. They build in the flexibility needed to navigate market cycles—something the original 4 percent rule was never designed to do. For a deeper look at how these models compare, our guide to retirement withdrawal strategies offers a comprehensive overview.

The table below highlights the key differences between the old rule and these smarter, adaptive methods.

Comparing Withdrawal Strategies

Ultimately, dynamic strategies replace the illusion of certainty offered by the 4 percent rule with the real-world resilience needed for a multi-decade retirement. They empower you to react intelligently to market conditions, providing both greater security during downturns and more opportunity during periods of growth.

Going Beyond The 4% Rule: Building Your Real-World Retirement Plan

A successful retirement isn't built on a single rule of thumb. It's assembled piece by piece with a plan that fits your life perfectly. For anyone with significant assets, moving past simple ideas like the 4% rule isn't just a good idea—it's absolutely critical.

A truly robust retirement plan is a core part of comprehensive wealth management. It's about more than just selling off stocks and bonds to generate cash. It’s about making all your resources work together in the smartest way possible to fund your lifestyle, slash your tax bill, and secure your legacy.

A Smarter Way To Tap Your Accounts

One of the biggest levers you can pull is tax-efficient withdrawal sequencing. The order in which you draw from your accounts—taxable, tax-deferred, and tax-free—can dramatically change how long your money lasts.

While every situation is unique, a common and effective game plan looks something like this:

- First, Taxable Accounts: These are often the first to be tapped. Since long-term capital gains get preferential tax treatment, this can be an efficient initial source of cash.

- Second, Tax-Deferred Accounts: Next up are your traditional IRAs and 401(k)s. The goal here is to let them keep growing without a tax drag for as long as you can.

- Last, Tax-Free Accounts: Your Roth IRA and Roth 401(k) are typically the last resort. Every dollar you pull out is tax-free, and leaving them untouched lets them grow into a powerful asset for later in retirement or for your heirs.

This isn't just about saving a few bucks. Carefully managing your withdrawals can help you stay in a lower tax bracket year after year, protecting your portfolio from the corrosive effect of taxes.

Dealing With Complex Assets

For many successful people, a lot of their wealth isn't in plain-vanilla stocks and bonds. A real-world plan has to account for these more complex holdings.

A concentrated stock position—maybe from your career or a family business—is a classic example. It’s a source of great wealth but also significant risk. You need a strategy to carefully diversify over time, not just to reduce risk, but to do so without creating a massive, one-time tax event.

Then you have illiquid assets like private equity investments or real estate holdings. You can’t just sell these on a Tuesday afternoon to pay your bills. A solid plan has to anticipate the cash flow from these assets—or the lack thereof—and build a liquidity cushion with other accounts to cover your needs while these long-term investments do their thing.

Building an income plan around illiquid assets is like managing a city's water supply. You need accessible reservoirs (liquid accounts) for daily demand, while understanding that the larger, distant lakes (illiquid investments) will provide huge resources on a much longer-term schedule.

Layering Your Income And Legacy

Finally, a complete plan layers in every other source of income you have. This could be anything from Social Security and pensions to more unpredictable streams like royalties or income from a business.

By mapping out exactly when these different income streams will start and stop, you get a much clearer picture of how much you actually need to pull from your portfolio each year.

This entire framework should also tie directly into your estate planning goals. For instance, if passing on a tax-free inheritance is a top priority, then preserving your Roth accounts becomes a central part of the income strategy. As you map out your needs, you can dig deeper into how to guaranteed retirement income can fit into the puzzle.

Ultimately, this is the difference between blindly following a rule and engineering a durable, personalized financial machine. It’s about building a plan that accounts for the messy, multifaceted reality of wealth.

Building a Plan That’s Actually Yours

After poking holes in the 4% rule—from its shaky, decades-old assumptions to its stumbles on the world stage—it’s pretty obvious that a simple rule of thumb just doesn’t cut it anymore. These rules are fine for getting a conversation started about retirement, but they’re a poor substitute for a plan that’s been professionally built and put through its paces.

Real financial confidence doesn't come from a one-size-fits-all formula. It comes from grabbing the wheel and steering your own future with a strategy built for the life you actually want to live.

A retirement income plan that lasts has to be both comprehensive and ready to adapt. It needs to map to your specific world—your goals, your comfort with risk, and what you hope to leave for the next generation. This isn't something you can do with a simple calculator.

The Bones of a Bulletproof Plan

Instead of being tethered to a fixed withdrawal number, a modern retirement strategy uses powerful tools to get ready for a whole spectrum of possibilities. It’s about being prepared, not just hopeful. The key pieces look something like this:

Personalized Cash Flow Modeling: This is so much more than a budget. We’re talking about a detailed blueprint that maps out every dollar coming in (pensions, Social Security, rental income) and every dollar going out (healthcare, travel, grandkids’ tuition) for the rest of your life.

Scenario Analysis: This is where we play "what if." What if inflation roars for another five years? What if the market tanks the day after your retirement party? Scenario analysis tests your plan against these tough situations to find weak spots before they become real problems.

Monte Carlo Simulations: It sounds complex, but the idea is simple. This statistical engine runs your portfolio through thousands of different potential market futures—good, bad, and ugly. Instead of a simple "yes" or "no," you get a probability of success, like an 85% chance your portfolio will last until you’re 95.

A personalized strategy doesn't just give you a number; it gives you confidence. By stress-testing your plan against market volatility, inflation shocks, and longevity risk, you can build a resilient income stream designed to last a lifetime.

At the end of the day, making sense of all these moving parts takes more than just good intentions—it takes real expertise. The true value of working with a dedicated advisory firm is their ability to turn your personal goals into a mathematically sound plan that can weather a storm.

By moving past the limits of the 4% rule, you can build a strategy that's genuinely designed to secure your financial future and protect your legacy.

A Few Common Questions About the 4% Rule

We’ve covered a lot of ground, and it’s clear the world has changed since the 4% rule first came on the scene. It’s only natural for retirees and investors to have questions about what this all means for their own plans. Here are some of the most common ones we hear.

Can I Still Use The 4% Rule As A Rough Estimate?

Yes, but with a big dose of caution. Think of it as a way to start the conversation about retirement, not end it. Leaning on the original 4% rule for an actual retirement plan today is a risky bet.

With today’s lower expected market returns and the real possibility of higher inflation, a more conservative number is a much safer place to start. Many financial advisors now point to a withdrawal rate closer to 3% or 3.5% as a more grounded benchmark for that initial planning. The old rule helps frame the problem, but it won’t solve it.

How Do I Choose Between Different Dynamic Withdrawal Strategies?

There's no single "best" choice here—the right strategy really comes down to your personal situation. It depends on your comfort with risk, how much flexibility you have in your spending, and the size of your nest egg.

- The "Guardrails" approach is a popular starting point for many. It strikes a good balance, giving you a relatively stable income stream while still protecting your portfolio from big market swings.

- Other methods, like Variable Percentage Withdrawal (VPW), might be a better fit if you're comfortable with your spending tracking the market's performance more closely.

The best way forward is to sit down with an advisor and model a few different scenarios. This helps you see how each strategy would play out and find the one that fits both your financial goals and your peace of mind.

What Is The Biggest Risk Of Following The 4 Percent Rule Today?

The single biggest danger, without a doubt, is sequence of returns risk. This is the risk of hitting a stretch of bad market returns right at the beginning of your retirement.

The old 4% rule has a critical flaw: it forces you to sell assets at a fixed rate, even when the market is tanking. This can permanently cripple your portfolio and dramatically raise the odds of outliving your money.

When you’re forced to sell more shares at low prices just to generate the same amount of cash, you're locking in losses. This damages your portfolio's ability to bounce back when the market eventually recovers. Dynamic strategies were designed specifically to avoid this trap by cutting back on withdrawals when your portfolio is down.

Navigating retirement income requires more than old rules of thumb; it demands a plan built for your unique circumstances. At Commons Capital, we specialize in moving beyond outdated guidelines to engineer durable, tax-efficient strategies for high-net-worth individuals and families. Discover how we can build a resilient plan tailored to your goals by visiting us online.