Navigating the world of wealth management can feel overwhelming, especially for high-net-worth individuals and families with complex financial landscapes. The key to success often lies in finding the right professional guide, which makes knowing what to look for in a financial advisor the most critical first step. This guide moves beyond the basics, offering a detailed roadmap to help you identify an advisor who not only manages your assets but truly partners with you to achieve your long-term goals.

We will explore seven essential criteria, from understanding fiduciary duties to aligning investment philosophies. Each point is designed to provide actionable insights, helping you make a confident and informed decision that fits your unique financial journey. Whether you are a business owner planning an exit, a professional athlete managing significant income, or an investor seeking sophisticated strategies, this article provides a clear framework for your search. This isn't just about finding someone qualified; it's about finding the right partner for your financial future. Our deep dive into credentials, fee structures, and communication styles will empower you to select a trusted advisor who can help safeguard and grow your wealth for years to come.

1. Credentials and Professional Qualifications

When considering what to look for in a financial advisor, their credentials should be your first checkpoint. Professional certifications are not just letters after a name; they represent a rigorous commitment to expertise, ethical conduct, and continuous learning in the complex world of finance. For high-net-worth individuals, whose financial landscapes are often intricate, these qualifications provide a crucial baseline of trust and competence.

Certifications like the CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst) indicate an advisor has passed demanding examinations, met extensive experience requirements, and adheres to a strict code of ethics. This ensures they possess a comprehensive understanding of financial planning, from investment strategy and estate planning to retirement and tax implications.

Key Insight: An advisor's credentials are a direct reflection of their dedication to their profession and their clients. They signal a proven ability to navigate sophisticated financial challenges, a critical factor when significant assets are at stake.

How to Verify and What to Ask

Verifying an advisor's credentials is a straightforward but essential due diligence step. Never take certifications at face value; always confirm them with the issuing body.

- Verify Online: Use official websites like the CFP Board's "Find a CFP Professional" tool or the CFA Institute's member directory. For brokerage-affiliated advisors, FINRA's BrokerCheck is an indispensable resource for reviewing employment history and any disciplinary actions.

- Ask About Specializations: Inquire about their continuing education. An advisor focused on tax-efficient strategies for business owners or complex estate planning for families should have recent coursework to back it up.

- Match Credentials to Your Needs: A CFA charterholder is ideal for complex investment portfolio management, while a CFP professional offers a more holistic view of your entire financial life. Ensure their expertise aligns with your primary goals.

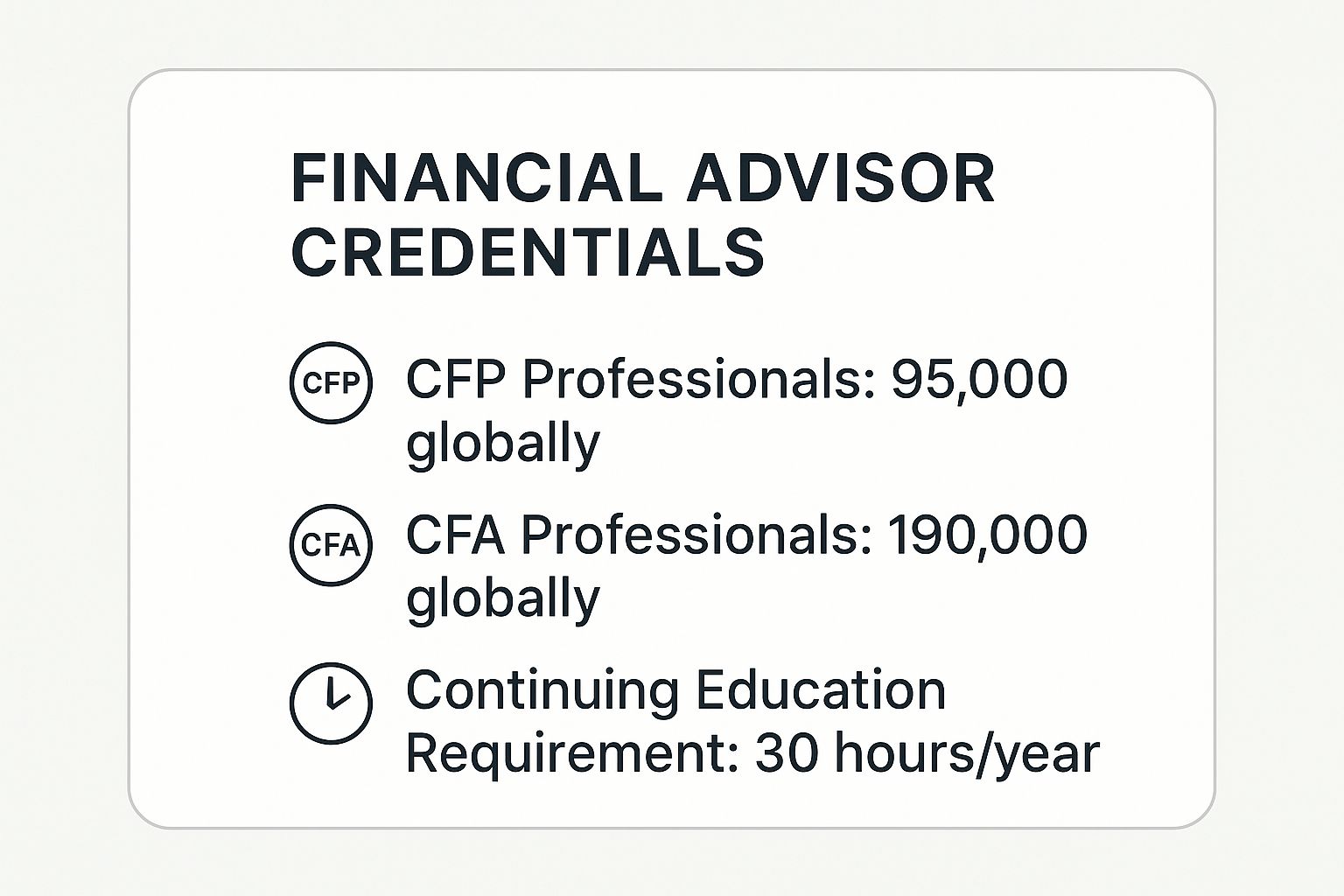

This summary box highlights the global reach and educational demands of top-tier financial certifications.

The data underscores that while thousands of professionals hold these designations, they represent a select group committed to the highest standards, including a significant annual education requirement to stay current. This ongoing learning is non-negotiable in a constantly evolving financial market.

2. Fee Structure and Transparency

Understanding how a financial advisor is compensated is a critical element of what to look for in a financial advisor. The fee structure not only impacts the total cost of service but, more importantly, can reveal potential conflicts of interest. For high-net-worth clients, whose financial strategies often involve complex products and significant capital, fee transparency is non-negotiable for building a relationship based on trust and aligned interests.

An advisor's compensation model dictates how they make money, which can influence the advice they provide. The primary models include fee-only, where the advisor is paid directly by the client; commission-based, where they earn money from selling specific financial products; or a hybrid of the two. A transparent advisor will proactively and clearly disclose all potential costs and how their compensation might affect their recommendations.

Key Insight: The fee structure is the foundation of the advisor-client relationship. A clear, transparent model, especially a fee-only one, minimizes conflicts of interest and ensures the advice you receive is driven solely by your financial goals, not by a potential commission.

How to Verify and What to Ask

Probing an advisor's compensation model is a necessary step to protect your interests and ensure you're receiving unbiased guidance. A trustworthy advisor will welcome these questions and provide straightforward answers.

- Request Form ADV Part 2A: This regulatory document, filed with the SEC, is a brochure that details the advisor's services, fees, and any conflicts of interest. Ask for it upfront and review it carefully.

- Ask for a Fee Schedule: Inquire about a detailed written breakdown of all fees. This should include asset management fees (AUM), hourly rates, project-based fees, and any other potential charges for transactions or administrative services.

- Clarify Their Fiduciary Status: Ask directly, "Are you a fiduciary at all times?" A fiduciary is legally and ethically bound to act in your best interest. While fee-only advisors are typically fiduciaries, it is essential to get explicit confirmation.

Models like those promoted by the National Association of Personal Financial Advisors (NAPFA) champion the fee-only approach, which is often preferred for its inherent transparency. For example, an advisor charging a 0.75% AUM fee on a $2 million portfolio would cost $15,000 annually. Understanding this total cost allows for a clear evaluation of the value being delivered, ensuring there are no hidden charges that could erode your returns over time.

3. Fiduciary Standard vs. Suitability Standard

Understanding the legal and ethical framework an advisor operates under is a crucial step when looking for what to look for in a financial advisor. This distinction, primarily between the fiduciary and suitability standards, dictates how they must approach recommendations and manage potential conflicts of interest. For high-net-worth clients, whose financial affairs are complex, this difference can have significant long-term consequences on wealth preservation and growth.

The fiduciary standard is the highest legal duty of care, obligating an advisor to act solely in their client's best interest at all times. This means they must proactively avoid conflicts of interest and disclose any that are unavoidable. In contrast, the suitability standard only requires that a recommendation be "suitable" for a client's circumstances, which could still allow for higher-commission products to be favored over more cost-effective alternatives. Registered Investment Advisors (RIAs) are legally bound to the fiduciary standard, offering a layer of protection that is paramount for sophisticated investors.

Key Insight: Choosing an advisor who operates under a fiduciary standard aligns their legal duty directly with your financial success. This framework minimizes conflicts of interest and ensures that every piece of advice is structured to serve your best interest, not their bottom line.

How to Verify and What to Ask

Confirming an advisor's legal standard of care is a non-negotiable part of your due diligence. A true fiduciary will be transparent about their obligations and should have no hesitation in putting their commitment in writing.

- Request a Fiduciary Oath: Ask the advisor directly, "Do you act as a fiduciary at all times?" and request they sign a fiduciary oath or provide a written confirmation of their status. This simple step creates clarity and accountability from the outset.

- Review Form ADV: For RIAs, Part 2 of their Form ADV brochure details their services, fees, and any potential conflicts of interest. It explicitly states their fiduciary duty. You can access this document through the SEC's Investment Adviser Public Disclosure (IAPD) website.

- Understand "Dual Registration": Some advisors are dually registered as both an RIA representative (fiduciary) and a broker (suitability). Ask them to clarify in which capacity they would be working with you and how they manage the shift between these roles.

This summary box highlights the clear distinction between the two standards, emphasizing the client-centric nature of the fiduciary duty.

The data underscores that while both standards aim to protect investors, the fiduciary standard imposes a much stricter, more comprehensive obligation on the advisor. This commitment to placing client interests first is the bedrock of a trusting and effective advisory relationship.

4. Investment Philosophy and Strategy

An advisor's investment philosophy is the bedrock of their approach to managing wealth. It's their core belief system about how markets work, how to balance risk and reward, and how to build durable portfolios. For individuals with substantial assets, understanding this philosophy is paramount, as it dictates every decision made with your capital and is a key factor when considering what to look for in a financial advisor.

This philosophy determines whether an advisor favors active management (stock picking) or passive strategies (index-tracking), their approach to asset allocation, and how they react to market volatility. A well-defined philosophy, such as the factor-based investing pioneered by Eugene Fama or the low-cost indexing championed by Vanguard, provides a consistent, evidence-based framework that prevents emotional, reactive decision-making during turbulent times.

Key Insight: A coherent investment philosophy ensures your portfolio is managed with discipline and a long-term perspective, not on market fads or fear. It is the strategic blueprint that should align perfectly with your personal risk tolerance, time horizon, and ultimate financial objectives.

How to Verify and What to Ask

Probing an advisor's investment philosophy reveals their discipline and ensures their strategy is a good fit for you. It's not enough for them to say they want to make you money; you need to understand how they plan to do it.

- Ask for a Simple Explanation: Request that they explain their investment philosophy without using jargon. Can they articulate their core principles clearly and concisely? A competent advisor should be able to explain complex ideas in an accessible way.

- Request Real-World Examples: Ask for a historical example of how their philosophy guided their decisions during a specific market downturn, like the 2008 financial crisis or the 2020 COVID-19 crash. This demonstrates their strategy in action.

- Discuss Alignment with Your Goals: Your risk tolerance is unique. Discuss how their philosophy adapts to different client needs, from aggressive growth to conservative wealth preservation. For more detailed information, you can learn more about investing with a financial advisor on commonsllc.com.

- Inquire About Evidence and Data: A strong philosophy is typically supported by academic research and historical data. Ask what evidence their strategy is built upon. This separates disciplined approaches from speculative guesswork.

5. Communication Style and Availability

Beyond investment returns and strategic plans, the quality of your relationship with a financial advisor hinges on clear and consistent communication. When considering what to look for in a financial advisor, their communication style and availability are paramount. For high-net-worth individuals managing complex financial lives, a breakdown in communication can lead to missed opportunities or costly misunderstandings. The right advisor acts as a true partner, proactively keeping you informed and being accessible when you need them most.

An advisor's ability to translate intricate financial jargon into plain, understandable language is a critical skill. They should adapt their communication method, frequency, and level of detail to your specific preferences, ensuring you feel confident and in control of your financial strategy. Whether you prefer detailed quarterly reports, brief weekly emails, or direct phone access for urgent matters, their process should align seamlessly with yours.

Key Insight: A great advisor communicates with you, not at you. Their availability and responsiveness are direct indicators of the level of service and personal attention you can expect, especially during volatile market conditions or significant life events.

How to Verify and What to Ask

Evaluating an advisor's communication protocol during the vetting process is non-negotiable. This is your chance to set clear expectations and test their client service philosophy before making a commitment.

- Establish Expectations Upfront: Directly ask about their standard communication frequency. Will you have scheduled reviews quarterly, semi-annually, or annually? How do they handle market updates or changes to your portfolio between scheduled meetings?

- Test Responsiveness: During your initial consultations, pay close attention to how quickly they respond to your emails or calls. This initial experience is often a reliable preview of their ongoing accessibility.

- Inquire About Their Process: Ask them to describe their client onboarding process and how they keep clients informed. Do they provide access to a client portal for 24/7 portfolio viewing? Who is your primary point of contact, and what is the procedure if they are unavailable?

- Discuss Emergency Protocols: What happens if you have an urgent financial need outside of business hours? Firms like Morgan Stanley may offer dedicated client relationship managers, while local RIAs often provide direct cell phone access for this exact reason.

6. Experience and Track Record

When evaluating what to look for in a financial advisor, their experience and track record provide crucial context beyond certifications. An advisor's history is a testament to their ability to navigate real-world market volatility and complex client situations. For high-net-worth investors, this means seeking a professional who has not just years of service, but years of relevant experience guiding clients with similar financial profiles through various economic cycles.

Experience isn't merely about tenure; it's about demonstrated resilience and wisdom. An advisor who successfully guided clients through the 2008 financial crisis or the recent pandemic-induced downturn has proven their ability to provide steady counsel under pressure. This kind of battle-tested expertise is invaluable when your significant assets are on the line.

Key Insight: A proven track record is the ultimate evidence of an advisor's philosophy in action. It demonstrates their capacity to turn theoretical knowledge into tangible, positive outcomes for clients, especially during periods of market stress.

How to Verify and What to Ask

Digging into an advisor's experience requires asking specific, pointed questions that go beyond their resume. Your goal is to understand how their past performance and client history align with your future needs.

- Inquire About Market Cycles: Ask them to describe how they advised clients during a major market downturn, like 2008 or March 2020. What specific strategies did they employ to protect capital and capitalize on recovery?

- Request Client Case Studies: Ask for anonymized examples of clients with financial situations similar to yours. How did the advisor help them achieve their goals, whether it was multi-generational wealth transfer, business succession, or managing a sudden liquidity event?

- Discuss Their Ideal Client: Understanding who they typically serve reveals their specialization. An advisor focused on corporate executives will have a different skill set than one who primarily serves professional athletes or entrepreneurs.

- Check Their Background: Reviewing the professional backgrounds of an advisory team can provide insight into the depth of their collective experience. You can see how our team’s deep experience benefits clients by exploring the profiles on our site. Learn more about the Commons Capital team.

By thoroughly vetting an advisor's experience, you ensure they have the practical skills and historical perspective necessary to steward your wealth effectively.

7. Services Offered and Specializations

A crucial aspect of what to look for in a financial advisor is the specific scope of services they provide. An advisor's offerings determine whether they can manage your entire financial picture or if you'll need multiple professionals. For high-net-worth individuals with multifaceted financial lives, a mismatch between your needs and their services can lead to costly gaps in strategy.

Comprehensive wealth management extends beyond simple investment advice to include retirement planning, tax optimization, estate planning, and insurance analysis. Some advisors, like those in the NAPFA network, typically offer this holistic approach, while others may specialize in niche areas such as planning for a divorce (CDFA) or maximizing retirement income (RICP). Understanding this distinction is key to finding the right fit.

Key Insight: The ideal advisor offers a suite of services that mirrors the complexity of your financial life. Aligning their specializations with your primary goals from the outset prevents fragmented advice and ensures a cohesive, long-term strategy.

How to Verify and What to Ask

Clarifying an advisor's service model and areas of expertise is a vital part of the discovery process. Use your initial meetings to dig deeper than the surface-level descriptions on their website.

- Define Your Needs First: Before you even speak to an advisor, list your most pressing financial goals. Are you focused on business succession, managing a recent inheritance, or creating a tax-efficient retirement income stream? Knowing this helps you filter candidates effectively.

- Ask About Their Strongest Areas: Directly inquire, "What types of client situations or problems are you best at solving?" Their answer will reveal their core competencies and whether they align with your needs. Learn more about the comprehensive financial planning services that cover these diverse areas.

- Understand the Service and Fee Structure: Ask which services are included in their standard fee and which might incur additional costs. A truly comprehensive planner should integrate tax and estate planning discussions into their core investment strategy without needing separate retainers.

- Inquire About Their Professional Network: No single advisor can be an expert in everything. Ask about their network of professionals, such as CPAs and estate attorneys. A well-connected advisor who collaborates with other experts can provide immense value and a more integrated financial plan.

7-Key Criteria Comparison for Financial Advisors

Making Your Final Decision with Confidence

Navigating the landscape of financial advisory services can feel overwhelming, but your journey to find the right partner is now equipped with a powerful framework. This is not a decision to be taken lightly; it is one of the most critical choices you will make in securing your financial legacy. The process of understanding what to look for in a financial advisor moves beyond a simple checklist and becomes a strategic exercise in due diligence.

By systematically evaluating the seven key pillars we have explored, you transform a potentially confusing search into a clear, methodical process. From verifying credentials like the CFP® or CFA to demanding absolute transparency in fee structures, each step empowers you to filter out noise and focus on substance. The distinction between a fiduciary and a broker operating under a suitability standard is not a minor detail; it is the bedrock of a trusting relationship.

Synthesizing Your Findings for a Confident Choice

As you consolidate your research from multiple interviews, a clear picture of your ideal partner will emerge. It is crucial to move beyond the individual data points and assess how they fit together to serve your unique needs.

- Aligning Philosophy with Your Goals: Did the advisor’s investment philosophy resonate with your personal risk tolerance and long-term vision? A strategy that sounds impressive on paper is worthless if it causes you to lose sleep at night or deviates from your core objectives.

- The Communication Commitment: Reflect on the quality of your interactions. Was the advisor an active listener? Did they explain complex concepts in a way that you understood and felt comfortable with? This initial communication style is often a direct preview of your long-term relationship.

- A Partnership, Not a Transaction: The best advisor is more than a portfolio manager. They are a strategic partner, a financial quarterback who coordinates with your other professionals, like attorneys and accountants, to ensure every piece of your financial puzzle fits together seamlessly. This is the difference between simple investment management and true wealth management.

Your financial future is far too important to leave to chance or a gut feeling alone. This decision demands the same level of intellectual rigor and strategic planning that you apply to your business or career. By prioritizing a fiduciary commitment, transparent fees, a compatible investment strategy, and a proven track record, you are not just hiring an advisor; you are forging a partnership dedicated to building and preserving your wealth for generations. Making this deliberate, well-researched choice is the first and most important investment you can make in your own success.

At Commons Capital, we embody these principles, providing dedicated, fiduciary-level wealth management tailored to the unique complexities of high-net-worth individuals, families, and institutions. If you are seeking a partner who aligns with the rigorous standards outlined here, we invite you to learn more about our approach. Explore how our team can help you navigate your financial future with confidence by visiting us at Commons Capital.