Investing with a financial advisor isn't just about handing over your money and hoping for the best stock picks. It's about building a strategic partnership with a professional who designs a complete financial roadmap tailored to your life. Think of it as combining expert investment management with personalized guidance to help you cut through the market noise and reach your long-term goals.

What It Really Means to Partner with an Advisor

Imagine you're planning a tough climb up an unfamiliar mountain. You could go it alone with a map and your best guess, but that’s a risky way to get to the summit. Or, you could hire an expert guide—someone who knows the terrain inside and out, sees the hidden dangers, and keeps you on the safest, most direct path.

A financial advisor is that seasoned guide for your financial journey.

Their job goes way beyond simply picking stocks or bonds. A real advisory relationship is built on a deep understanding of what you want out of life, whether that’s funding your kids' college education, retiring without worry, or leaving a meaningful legacy for the next generation.

The Advisor as a Financial Architect

A good advisor is the architect of your financial life. They don't just throw together a portfolio; they draw up a comprehensive blueprint that makes sure every financial decision, big or small, aligns with your ultimate goals.

This process involves a few key roles that are much more valuable than just investment selection. A great advisor will:

- Bring Your Goals into Focus: They help translate vague dreams like "retiring comfortably" into concrete, measurable targets. You'll walk away knowing your target retirement date and exactly how much you need to be saving.

- Manage Risk with Intention: They'll figure out your true comfort level with market ups and downs and build a portfolio that balances growth potential with the right amount of risk, so you can actually sleep at night.

- Act as Your Behavioral Coach: When the market gets scary or irrationally exuberant, a good advisor is the steady hand that keeps you from making impulsive decisions you'll later regret. This is often their most important job.

A well-known study from Vanguard found that advisors can add about 3% in net returns for their clients over time. A huge chunk of that value comes from behavioral coaching—simply keeping investors from reacting emotionally. It's often called the "Advisor's Alpha."

To give you a clearer picture, here's a quick breakdown of the essential functions an advisor performs.

Key Roles Your Financial Advisor Plays

This table offers a quick look at the primary functions a financial advisor performs to help you achieve your goals.

As you can see, the value isn't just in one area but in how these different roles work together to support you.

Beyond the Portfolio

Ultimately, a great advisory partnership touches almost every part of your financial life. They’ll connect your investment strategy to other critical areas like tax planning, estate considerations, and insurance needs. This creates a cohesive plan where everything works in harmony.

This holistic approach ensures your investments aren't just growing in a vacuum—they're structured to support your life's journey in the most effective way possible. The focus shifts from worrying about short-term market swings to confidently building toward your long-term life goals. That's a shift that brings both financial progress and priceless peace of mind.

The True Value of Professional Financial Guidance

Sure, a DIY approach to investing can work for some, but the real benefits of investing with a financial advisor go way beyond just managing a portfolio. It's about having a strategic partner in your corner—someone who brings expertise, discipline, and a big-picture view that most of us simply don't have the time to develop on our own.

This kind of professional guidance doesn't just translate into potentially better returns; it offers invaluable peace of mind.

Your Shield Against Emotional Investing

The stock market is a rollercoaster, and even the sharpest investors can get tripped up by fear and greed. When the market takes a nosedive, the gut reaction is to sell everything to stop the bleeding. On the flip side, during a hot streak, the fear of missing out (FOMO) can tempt you to chase speculative trends right at their peak.

An advisor acts as a critical buffer between you and those impulsive, wealth-destroying decisions. They are the objective voice of reason, gently reminding you of your long-term goals and preventing a temporary market panic from wrecking a financial plan you've spent years building. This behavioral coaching is often where an advisor provides their most significant—if least tangible—value.

A key takeaway is that an advisor's primary role during market volatility is to manage your behavior, not just your portfolio. By helping you stick to a well-thought-out strategy, they prevent the single biggest threat to long-term returns: emotional decision-making.

This disciplined partnership helps you stay invested to capture market recoveries and avoid the classic mistake of buying high and selling low.

Access to Sophisticated Strategies

Another huge advantage of working with a professional is getting access to investment opportunities and strategies that are often out of reach for the average retail investor.

This might include:

- Private Equity and Alternative Investments: These can offer diversification and return potential that isn't tied to the public markets, but they're typically reserved for accredited investors.

- Advanced Portfolio Construction: Advisors use sophisticated tools to fine-tune your asset allocation, balancing risk and reward with a level of precision that goes far beyond a basic mix of stock and bond funds.

- Institutional-Grade Products: They often have access to mutual funds or other investment vehicles with lower fees than what you can find on your own.

These tools allow for a more robust and diversified portfolio, one that’s built to weather different economic storms more effectively.

Creating a Truly Holistic Financial Plan

Perhaps the most powerful benefit is seeing how your investments fit into your entire financial picture. A good advisor doesn't just manage your brokerage account in a silo; they weave it into a comprehensive strategy. This holistic approach connects your investments to every other vital area of your financial life.

This is the essence of true wealth management. You can explore our approach to https://www.commonsllc.com/whatwedo/financial-planning to see how these elements all work together. The goal is to build a seamless system where every financial decision supports the others, creating a powerful engine for long-term growth and security.

The demand for this kind of personalized guidance is on the rise. According to ResearchAndMarkets.com, the global financial advisory market is projected to grow significantly, a trend fueled by market volatility and a greater need for professional advice. An advisor ensures your strategy isn't just about accumulation but about smart wealth management that considers taxes, estate planning, and risk, turning a simple portfolio into a lasting legacy.

How to Find the Right Financial Advisor for You

Picking a financial advisor is one of the most important decisions you'll make for your financial future. This isn't just hiring someone to manage your money; it's about finding a long-term partner who will be in your corner, guiding you through life’s inevitable twists and turns.

The right fit can make all the difference. You're looking for someone whose expertise, philosophy, and even personality click with your own. Let's walk through a practical playbook for looking past the polished marketing and finding a professional who is genuinely right for you.

Start With the Fiduciary Standard

Before you even begin your search, there's one word you need to lock in: fiduciary. It’s a non-negotiable.

An advisor who is a fiduciary is legally and ethically required to act in your best interest. Always. This is a huge distinction because not everyone in the financial world operates this way. Some work under a "suitability standard," which just means their recommendations have to be suitable, not necessarily what's best for you.

A fiduciary duty is the highest standard of care in the financial world. It means the advice you get is purely focused on your well-being, free from conflicts of interest like earning a commission for selling a specific product.

When you meet a potential advisor, ask them point-blank: "Are you a fiduciary at all times?" You want to hear a clear, confident "yes." Anything less is a red flag.

Deciphering the Alphabet Soup of Credentials

The financial industry loves its acronyms, and it can feel like you need a decoder ring to understand them all. But a few key credentials signal a serious commitment to expertise and ethics.

Think of them as a sign of dedication to the craft. Here are the big ones to look for:

- CFP® (Certified Financial Planner™): This is the gold standard for personal financial planning. A CFP® has gone through rigorous training and testing on everything from retirement and investments to insurance and estate planning. They are also held to a strict fiduciary standard.

- CFA (Chartered Financial Analyst): This is a heavyweight designation focused on deep investment analysis and portfolio management. A CFA charterholder has advanced, specialized skills in picking investments and building portfolios.

- CPA/PFS (Certified Public Accountant/Personal Financial Specialist): This credential is a powerful combination. It blends the tax mastery of a CPA with the holistic knowledge of a personal financial specialist, making it a great fit if your financial life has tax complexities.

Essential Questions to Ask a Potential Advisor

Once you have a shortlist, it's time for the interview. This is your chance to get a feel for who they are and how they operate. Don't hold back—this is your money and your future on the line.

The goal is to see if their approach, process, and communication style are a good match for you.

Key Questions for Your Advisor Interview:

- What is your investment philosophy? Are they believers in passive index funds, or are they active managers trying to beat the market? Their answer should make sense to you and align with your own comfort level with risk.

- Who is your ideal client? Advisors often have a niche. Some work with retirees, others with small business owners. Finding an advisor who understands your world is key. Professionals like athletes, for instance, have unique career arcs and need specialized guidance. You can learn more about how a financial advisor for athletes can provide tailored support.

- How do you communicate with clients? Do they send formal quarterly reports, or are they more of a "call me anytime" person? Make sure their style works for you.

- What is your full fee structure? This is a big one. Ask for total transparency. You want a written breakdown of all fees—AUM fees, planning fees, anything else. There should be no surprises, ever.

Verifying Credentials and Background

Trust, but verify. Before you sign on the dotted line, do a quick background check to make sure the advisor has a clean record. It’s easier than you think, and it’s free.

FINRA's BrokerCheck is a fantastic tool from the Financial Industry Regulatory Authority. You can punch in an advisor's name and see their work history, licenses, and any complaints or disciplinary actions.

This simple step gives you peace of mind when investing with a financial advisor, ensuring you’re partnering with a professional you can truly trust.

How Does a Financial Advisor Get Paid?

Figuring out how a financial advisor gets paid is one of the most critical steps in choosing the right one. This isn't just about the cost; the fee structure tells you a lot about an advisor's incentives and whether they're truly aligned with your best interests. When you're investing with a financial advisor, you want to know their success is tied directly to yours.

Let's walk through the most common ways advisors are compensated. Each model has its own pros and cons, and the best one for you really depends on your financial situation and what kind of help you’re looking for.

Assets Under Management (AUM) Fees

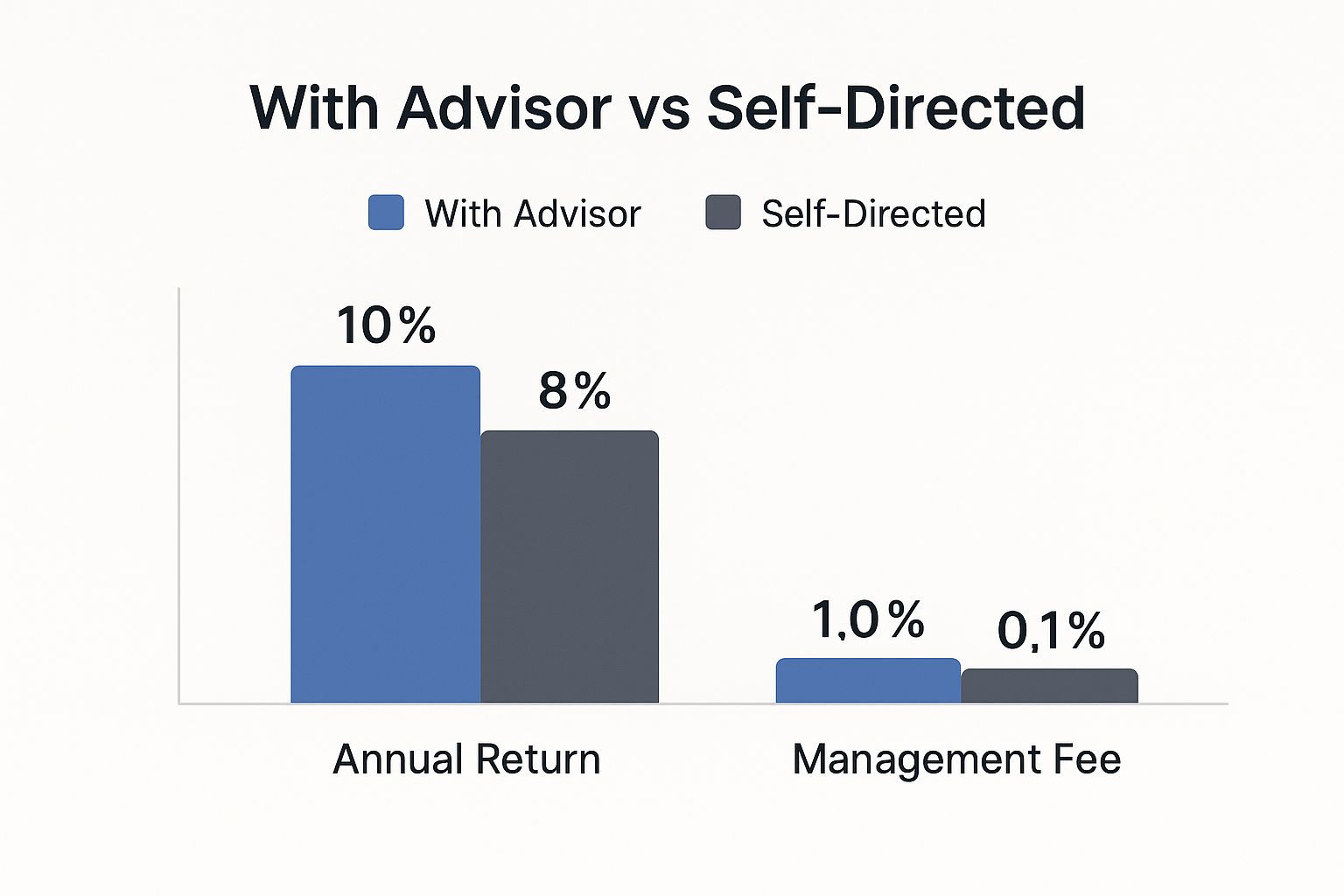

The most common model you'll see is the Assets Under Management (AUM) fee. It’s pretty straightforward: the advisor charges an annual percentage of the total assets they manage on your behalf. For example, if you have $1 million invested with an advisor who charges a 1% AUM fee, your annual cost would be $10,000.

This fee is usually taken directly from your investment account each quarter. The big appeal here is the shared goal—as your portfolio grows, so does your advisor’s compensation. It gives them a real incentive to make smart, long-term decisions that build your wealth. On the flip side, for very large portfolios, that percentage can add up to a significant amount of money. It might also be less cost-effective for someone who just wants a simple "buy-and-hold" strategy with little active management.

This chart gives you a sense of the trade-off investors often consider—paying a management fee in the hopes of achieving higher returns than they might on their own.

The idea is that while professional management comes at a cost, it's designed to generate returns that more than make up for the fee.

Fee-Only vs. Fee-Based: A Crucial Distinction

You'll hear the terms "fee-only" and "fee-based" thrown around, and while they sound alike, they are worlds apart. It's incredibly important to know the difference.

- Fee-Only Advisors: These professionals are paid only by their clients. That payment could be an AUM fee, an hourly rate, or a flat retainer. Crucially, they do not accept commissions or kickbacks for selling you specific financial products. This structure is designed to minimize conflicts of interest.

- Fee-Based Advisors: This is the one that can get tricky. These advisors can earn fees directly from you and get commissions from selling products like insurance or certain mutual funds. This doesn't automatically make them bad advisors, but it does create a potential conflict of interest. Are they recommending a product because it’s best for you, or because it pays them a higher commission?

A Note on Fiduciary Duty: Choosing a fee-only advisor is widely considered a best practice because it aligns with the fiduciary standard. A fiduciary is legally and ethically bound to act in your best interest at all times, which is exactly what you want from someone managing your money.

To make this clearer, let's break down the common fee models in a table.

Comparing Common Financial Advisor Fee Models

Here's a quick overview of how advisors are compensated, which should help you choose the right model for your needs.

Ultimately, the best fee structure is the one that feels fair and transparent to you. Don't be afraid to ask direct questions about how an advisor is paid before you sign anything.

Other Ways Advisors Charge for Their Services

While AUM is the big one, it’s not the only game in town. Depending on what you need, one of these other structures might be a much better fit.

Hourly or Project-Based Fees

Think of it like hiring a lawyer. You pay for the time you use. This is perfect if you don’t need someone managing your portfolio day-to-day but want a professional to help with a specific task—like creating a retirement plan, analyzing a job offer with stock options, or figuring out the best way to tackle debt. Rates often fall between $200 and $500 per hour.

Flat Retainer Fees

This model is gaining a lot of traction, and for good reason. You pay a predictable flat fee—annually or quarterly—for comprehensive financial planning. The cost is fixed, regardless of how much your assets grow. It's a great option for people who want holistic advice that covers everything from investments to taxes and estate planning, all for one clear price.

At the end of the day, there’s no single "best" way for an advisor to be paid. The right choice depends on how complex your finances are, how much you plan to invest, and the kind of relationship you want. The most important thing? Demand total transparency. Make sure you understand exactly how your advisor makes money so you can be confident they have your back.

Your Journey From First Meeting to Long-Term Growth

Starting a relationship with a financial advisor isn't a one-and-done transaction. It’s the beginning of an evolving partnership, a collaborative journey designed to adapt as your life does. Think of it less like buying a product and more like building a roadmap that starts with a deep conversation and continues through years of growth and strategic shifts.

Understanding how this process unfolds from day one helps set the right expectations. You'll see how each step builds on the last, ensuring your financial strategy stays sharp, relevant, and perfectly aligned with where you are—and where you want to go. This isn't about handing over your money and hoping for the best; it’s about building a plan for your future, together.

The Initial Discovery Meeting

Everything kicks off with the discovery meeting, which is arguably the most critical conversation you'll have. This is so much more than a simple handshake and introduction. It’s a deep dive into your financial DNA.

Think of it as a diagnostic session where your advisor gets to know you—your income, your assets, your dreams for retirement, and what you hope to leave behind for your family. The goal here is to get a 360-degree view of your values, how you feel about risk, and what you truly want to achieve with your money.

Crafting Your Personalized Financial Plan

After that initial deep dive, your advisor gets to work translating everything they've learned into a concrete, written financial plan. This document becomes the blueprint for your financial life, laying out specific, actionable steps to get you from here to there.

A solid plan will typically cover:

- Goal Analysis: Clearly defined targets with real timelines, like retiring by 65 with a specific income stream.

- Investment Strategy: A proposed mix of assets tailored to your comfort with risk, all designed to hit your growth targets.

- Risk Management: Smart recommendations for insurance or other tactics to shield your wealth from life's curveballs.

- Financial Projections: Detailed forecasts that model how your wealth could grow over time if you stick to the proposed strategy.

Your financial plan isn't a static document meant to be filed away and forgotten. It’s a living guide—your North Star for every financial decision you make from that point forward.

This kind of detailed planning is especially crucial for certain investors. For instance, a key driver for the growth in financial advisory services is the rising number of high-net-worth individuals (HNWIs). The global HNWI population recently jumped by 5.1%, and these individuals often rely on advisors to navigate complex investments, tax strategies, and estate planning. You can dig into this market trend in a report from ResearchAndMarkets.com.

Strategic Implementation and Ongoing Management

Once you give the green light, your advisor shifts from planning to action. They’ll put the investment strategy into motion—opening accounts, selecting the right investments, and putting your capital to work according to the plan. This is where the blueprint becomes a real, working portfolio.

But the work doesn't stop there. This is where the real partnership begins. Your advisor will keep a close eye on your portfolio, making strategic tweaks as the market zigs and zags or as your own life changes. This proactive oversight is the heart of professional investment management.

The Crucial Review Process

Your financial life is never a straight line. Life happens. You might get a promotion, have a child, inherit money, or decide to launch a business. Any one of these events can have a major impact on your financial plan, which is why regular reviews are so important.

Typically, you’ll meet with your advisor at least once a year for a comprehensive check-in. These meetings are a chance to:

- Assess Progress: See how your portfolio is performing against the goals you set out in your financial plan.

- Discuss Life Changes: Fill your advisor in on any big news that might require a strategy update.

- Re-evaluate Goals: Make sure your long-term objectives are still the same, or adjust them if your priorities have shifted.

- Make Necessary Adjustments: Rebalance your portfolio or update your plan to make sure you're still on the right track.

This cycle of planning, implementing, and reviewing ensures your financial strategy remains a perfect fit for you, year after year. It’s what turns a simple service into a powerful, long-term alliance focused squarely on your success.

Your Role in a Successful Advisory Partnership

The best results don't come from just hiring an advisor and walking away. They happen when it’s a genuine partnership. While your advisor brings the technical expertise and market knowledge, your active participation is what makes the financial plan truly yours—and keeps it on track. Think of yourself as the co-pilot, not a passenger.

This kind of collaboration is crucial because your life isn't static. Promotions, family changes, a sudden inheritance, or a new business idea—these are the real-world events that demand shifts in your financial strategy. Your advisor can only adapt the plan if you keep them in the loop.

Making Your Review Meetings Count

Regular meetings are your chance to grab the steering wheel. To get the most out of these sessions, it’s worth doing a little prep work. Don't just show up; come ready to talk specifics.

Before your next meeting, try this:

- Scan your recent statements. Got questions about performance or why you own a particular investment? Jot them down.

- List out any big life updates. Has your income changed? Family situation different? Are you thinking about your long-term goals in a new way?

- Check in with your gut. How are you feeling about your current strategy? Are you sleeping well at night, or do market swings have you on edge?

This simple preparation turns a routine check-in into a productive strategy session, making sure your money is still working for your life.

Asking the Right Questions

A solid partnership is built on clear communication. Never hesitate to ask questions that help you understand what's happening with your own money and the logic behind it. In a world where financial advisors are projected to manage assets totaling nearly $140 trillion by 2027, your engagement ensures your slice of that pie is managed with your goals front and center. You can read more about this global trend on Statista.com.

Good questions sound like:

- "Can you walk me through why we chose this particular investment?"

- "How does this move us closer to my goal of [retiring early, buying a lake house, etc.]?"

- "What would need to happen in the market for us to rethink this approach?"

When you're an active, informed participant, the relationship becomes more than just a service—it’s a powerful alliance. That proactive involvement is what really unlocks the full potential of working with an advisor and helps you confidently reach the goals that matter most.

Lingering Questions About Financial Advisors?

Even with a clear understanding of the benefits, it’s completely normal to have a few questions before you jump in and start investing with a financial advisor. This is a big decision, and you should feel 100% confident before moving forward.

To help you get there, we’ve pulled together a few of the most common questions we hear from people just like you. Think of this as the final gut-check before you take the next step.

How Much Money Do I Need to Hire a Financial Advisor?

There’s a stubborn myth out there that financial advice is only for the ultra-wealthy. While some old-school firms might have high asset minimums, the industry has changed dramatically to serve a much wider audience.

Today, many advisors have flexible ways to work with clients that don't require a massive portfolio. You can find excellent professionals who offer:

- Project-Based Services: Need a retirement plan built, but not ongoing management? Pay a one-time fee for that specific project.

- Hourly Consulting: Perfect for those just starting out. You can pay for advice by the hour, as you need it, without a long-term commitment.

- Advisors with Lower Minimums: Many fiduciary advisors are genuinely passionate about helping people build wealth from the ground up and have much more accessible starting points.

The real key isn't waiting until you think you have "enough" money. It's about finding an advisor whose business model fits where you are right now.

What's the Difference Between a Financial Advisor and a Robo-Advisor?

This is a fantastic question, especially with both options becoming so popular. A robo-advisor is a great, low-cost tool that uses an algorithm to build and manage an investment portfolio based on a questionnaire you fill out. For simple, set-it-and-forget-it investing, they can be a solid choice.

A human financial advisor, on the other hand, provides a level of comprehensive, personalized strategy that an algorithm just can't touch.

A human advisor offers crucial behavioral coaching during volatile markets, creative tax planning, and guidance on complex estate decisions. It’s the difference between automated portfolio management and true financial stewardship that adapts to your life.

Put simply: a robo-advisor manages your investments. A human advisor helps you manage your entire financial life.

How Often Should I Meet With My Financial Advisor?

Most advisors will schedule at least one big-picture review meeting each year. This is your chance to go over everything—portfolio performance, progress toward your goals, and any adjustments needed for the year ahead.

But a great advisory relationship isn't just a once-a-year chat. Life happens. It’s critical to connect with your advisor whenever you experience a major life event, like a marriage, the birth of a child, a new job, or an inheritance. A good advisor wants to be kept in the loop so they can ensure your financial plan evolves right alongside you.

At Commons Capital, we focus on building lasting partnerships. We provide the expert guidance our clients need to navigate their financial lives and achieve what matters most to them. If you're ready to create a strategic plan for your wealth, we invite you to start a conversation with us.