Strategic asset allocation is the blueprint for your investment portfolio. It's a long-term strategy that establishes a target mix of different asset classes—like stocks, bonds, and cash—based on your personal financial goals, risk tolerance, and investment timeline. This isn't about chasing market trends; it's a disciplined framework for creating a balanced foundation that is responsible for driving over 80% of your long-term returns.

This guide will explain what strategic asset allocation is, why it's crucial for your success, and how you can implement it.

The Blueprint For Long-Term Investing Success

Imagine building a house without a blueprint. You might end up with a beautiful kitchen, but the foundation could be a complete disaster. Investing without a plan is much the same—it can lead to a portfolio that looks good for a little while but crumbles at the first sign of market turbulence. Strategic asset allocation is that essential blueprint.

The core idea is simple: different assets behave differently depending on market conditions. When stocks are soaring, bonds might offer modest returns. But when stocks take a nosedive, high-quality bonds often act as a stabilizing force, shielding your portfolio from the worst of the decline.

From Theory to Reality: A Practical Example

Let’s look at a quick example. A younger investor with a high-risk tolerance and a 30-year horizon until retirement might choose an aggressive strategic allocation, such as 80% stocks and 20% bonds. This mix is built for maximum growth potential over the long haul.

Conversely, an investor nearing retirement would likely opt for something more conservative. Think 40% stocks and 60% bonds, a mix designed to preserve capital and generate steady income. The fundamental strategy is identical; only the percentages change to match different goals and risk profiles.

This adaptability is what makes strategic asset allocation a powerful and enduring framework for building wealth.

The Guiding Principles of This Investment Strategy

The power behind this strategy comes down to a few straightforward, yet potent, ideas. It forces a shift in focus from trying to pick individual "winner" stocks to getting the overall portfolio structure right. This isn't about timing the market; it’s about time in the market.

To understand what makes this approach effective, here's a rundown of its core principles.

Core Principles of Strategic Asset Allocation

This systematic approach is one of the most important concepts in modern finance.

Strategic asset allocation is the most important decision an investor makes. Research consistently shows that the choice of asset mix, not security selection or market timing, is the primary determinant of portfolio performance over time.

This structured method is a cornerstone of sound financial planning and a central piece of sophisticated portfolio construction, often explored when learning about what is private wealth management. The goal is always the same: to build a resilient portfolio that can systematically generate returns while managing risk in a way that aligns with your personal journey.

Why Your Asset Mix Is Your Most Important Decision

Many investors spend their time hunting for the next breakout stock or trying to perfectly time the market. While this feels proactive, it's often a distraction from the single biggest factor determining long-term success.

The hard truth is this: your most important investment decision happens long before you buy a single share. It all boils down to your target asset mix. Your answer—your strategic asset allocation—is the real engine that drives your portfolio’s performance. Getting this blueprint right is what separates disciplined investors from those just chasing trends.

The Overwhelming Evidence for Allocation

Decades of financial research all point to the same conclusion. While picking hot stocks and timing the market make for great headlines, their actual impact on your returns is surprisingly small. The real work is done by the deliberate mix of asset classes you establish from day one.

A landmark study changed how the investment world thinks about this, showing that approximately 93.6% of a portfolio's return variability is due to its asset allocation policy. In other words, deciding how much to put into stocks, bonds, and other assets matters far more than trying to pick individual winners.

This finding underscores that setting the right long-term mix of asset classes—equities, bonds, cash, and alternatives—is vastly more influential in investment outcomes than trying to beat the market through frequent trades or selection of specific securities.

This shifts the entire focus. Instead of searching for a needle in a haystack (the next big stock), the goal becomes building a stronger, more resilient haystack—a well-constructed portfolio.

How Asset Mix Manages Risk and Return

Picture a portfolio made up entirely of high-growth tech stocks. In a bull market, it could soar. But when the tech sector hits a rough patch, that same portfolio could suffer devastating losses, potentially wiping out years of gains in a flash.

Now, consider a portfolio with a strategic mix: maybe 60% in global stocks, 30% in government and corporate bonds, and 10% in real estate or other alternatives. When the stock market falters, the bond portion often acts as a cushion, preserving capital and smoothing out the ride. This balance reduces wild swings, leading to more consistent, predictable growth. A core pillar of this approach is using sound investment diversification strategies to protect and grow your wealth.

This isn't just about dodging losses; it’s about building a structure that can weather any economic storm. Different assets react differently to global events:

- During high inflation: Assets like commodities and real estate tend to hold up well.

- During a recession: High-quality government bonds are often seen as a safe haven, rising in value as investors flee to safety.

- During economic expansion: Stocks typically lead the charge, capturing the upside of a growing economy.

By holding a combination of these, your portfolio is never riding on a single economic outcome. It’s built for resilience, allowing you to stay invested and let your wealth compound through full market cycles—the ultimate key to reaching your financial goals.

The Building Blocks of a Strategic Portfolio

A solid strategic asset allocation isn't built from a single material. It's constructed from distinct, carefully chosen components that each play a specific and vital role. Think of it like a championship sports team—you need both powerful offensive players to score points and a rock-solid defense to protect your lead. A well-built portfolio needs different asset classes to perform in different market conditions.

The real magic happens when you combine assets that don't all move in the same direction at the same time. This intentional design helps smooth out the bumps in your investment journey, ensuring a dip in one area doesn't throw your entire financial plan off course.

Equities: The Growth Engine

When most people think of investing, they're thinking of equities. Stocks, as they're more commonly known, represent ownership in publicly traded companies. For most long-term portfolios, stocks are the primary engine for growth.

Historically, equities have delivered higher returns than other major asset classes over the long haul. That growth potential is what you need to outpace inflation and meaningfully build your wealth. But that potential comes with a trade-off: higher volatility. Stock prices can, and do, swing dramatically in the short term.

A well-calibrated equity allocation is the cornerstone of any growth-focused strategy. The art of strategic asset allocation is figuring out the right percentage of stocks that fits your timeline and your comfort with that inevitable market turbulence.

Fixed Income: The Stabilizer

Fixed income, or bonds, acts as the portfolio's defensive line. When you buy a bond, you're essentially lending money to a government or a corporation. In return, they agree to pay you back with interest over a set period.

The main job of bonds is to provide stability and a predictable stream of income. High-quality bonds often zig when the stock market zags, acting as a critical shock absorber during volatile periods. This inverse relationship is what cushions the portfolio against steep drops.

Bonds are the counterbalance to the volatility of stocks. Their stability provides the necessary foundation that allows the growth-oriented parts of your portfolio to function effectively without exposing you to excessive risk.

This stabilizing effect is fundamental to maintaining the discipline required for a long-term strategic approach.

Cash and Equivalents: The Safety Net

Often overlooked, cash and cash equivalents (like money market funds) are the portfolio's ultimate safety net. While they won't generate much growth, their real value lies in providing liquidity and preserving capital. Think of this as your "dry powder," ready to be deployed for opportunities or emergencies.

Holding a strategic amount of cash ensures you won't be forced to sell other assets at the worst possible time just to cover an unexpected expense. It also gives you the flexibility to rebalance your portfolio or invest when the market presents a rare opportunity.

Alternative Investments: The Diversifier

Beyond the traditional trio of stocks, bonds, and cash lies the world of alternative investments. These assets can add another powerful layer of diversification because their performance is often disconnected from public stock and bond markets. Learning how to diversify your portfolio with these tools is a critical step for any serious investor.

This category is broad, covering a wide range of assets with unique risk and return profiles.

- Real Estate: Investing in physical property or Real Estate Investment Trusts (REITs) can provide rental income and potential appreciation.

- Commodities: Assets like gold, oil, and agricultural products can be a hedge against inflation. Gold, in particular, is often seen as a safe-haven asset during times of economic uncertainty.

- Private Equity: This involves investing in private companies not listed on public exchanges. It offers high growth potential but comes with higher risk and less liquidity.

- Private Credit: Lending money directly to companies can offer attractive yields that aren't directly tied to public market swings.

Incorporating non-traditional assets requires careful due diligence, but they can significantly enhance a portfolio's resilience. To ensure your portfolio is truly well-rounded, explore these powerful investment diversification strategies. By thoughtfully combining these building blocks, you create a portfolio that's designed not just to grow, but to endure.

Strategic Versus Tactical Asset Allocation

If you're a serious investor, you've likely heard the terms "strategic" and "tactical" asset allocation. They might sound similar, but they represent two very different philosophies. Confusing them can lead to a disjointed, ineffective investment plan that undermines your long-term financial goals.

Think of it like this: your strategic asset allocation is your overall voyage plan. It's the big-picture course you plotted from start to finish, designed based on your ship’s capabilities and predictable seasonal weather. This is your foundational, buy-and-hold strategy.

Tactical asset allocation, on the other hand, involves smaller adjustments along the way. It’s changing course slightly to avoid a temporary storm or speeding up to catch a favorable current. These are short-term, opportunistic moves made within the larger framework of your main voyage plan—they aren't a replacement for it.

The Core Philosophies Compared

At its core, strategic asset allocation is a long-term, disciplined approach built on the belief that your asset mix is the primary driver of returns. It demands patience and a steady hand, requiring you to stick to your predetermined plan regardless of short-term market noise. This is the bedrock of your portfolio, designed to stand firm for years.

Tactical asset allocation is far more active. It allows for intentional, temporary shifts away from your strategic targets to capitalize on perceived market inefficiencies or short-term trends. For example, if you believe emerging markets are temporarily undervalued, a tactical move might be to increase your allocation to them from 5% to 8%, with the full intention of returning to the original 5% later. This approach requires more hands-on management and market analysis.

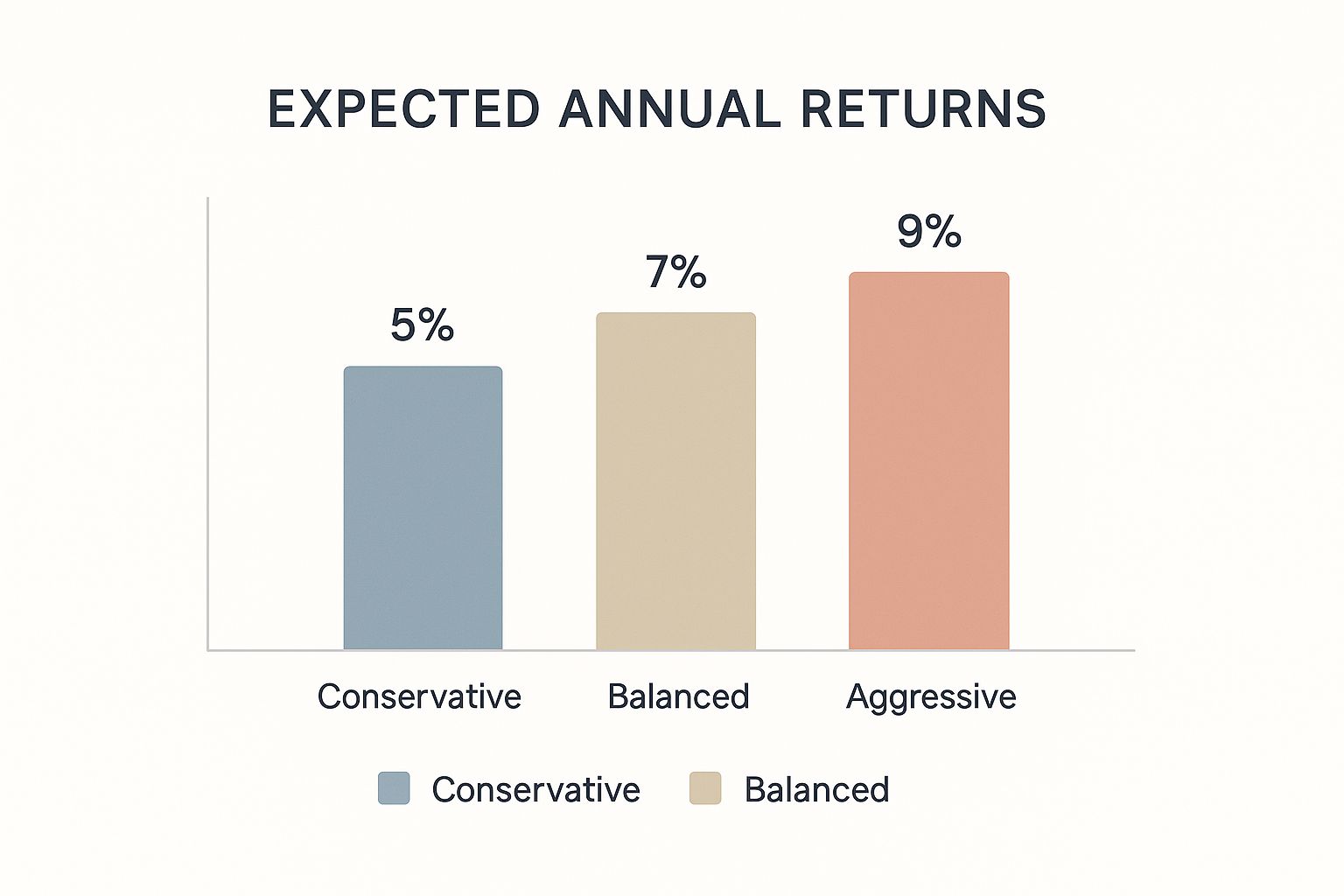

This chart illustrates how the expected annual returns for different strategic portfolio types align with their risk profiles, highlighting the fundamental trade-off between risk and reward.

As the visualization shows, a more aggressive strategic mix comes with the expectation of higher returns, but this is always coupled with greater risk. It’s a stark reminder of just how critical it is to choose the right long-term strategy from the outset.

Working Together, Not Against Each Other

It’s a common misconception that you must choose one approach over the other. The reality is, these two strategies can work together beautifully. Your strategic allocation is always the foundation—the non-negotiable blueprint for your financial future. Tactical shifts can then be layered on top as minor, calculated adjustments.

Strategic allocation sets the long-term direction, while tactical allocation refines the journey. One provides the discipline, the other provides the flexibility.

Without that solid strategic foundation, a purely tactical approach just becomes market timing, which is notoriously difficult to pull off successfully over the long run. The disciplined framework of a strategic plan ensures that even if a tactical bet doesn’t pan out, your core portfolio remains intact and aligned with your ultimate financial objectives.

Strategic vs Tactical Asset Allocation Compared

The table below highlights the key differences between setting a long-term course and making short-term adjustments along the way.

Ultimately, understanding both is key. The strategic plan is your map, and tactical moves are the skilled navigation needed to handle the changing seas.

The 60/40 Portfolio: A Timeless Example in Action

To understand what strategic asset allocation looks like in practice, there's no better case study than its most famous application: the 60/40 portfolio. For decades, this deceptively simple formula—60% in stocks, 40% in bonds—was the undisputed gold standard for balanced investing. It's the blueprint that has guided countless pension funds and individual retirement accounts.

Think of the 60/40 model as the perfect real-world example of strategic diversification. It pairs a growth engine (stocks) with a stabilizer (bonds), creating a portfolio designed to capture market upside while cushioning the inevitable downturns. This isn't about chasing the highest possible return every single year; it's about generating consistent, competitive growth over the long haul with less volatility.

Why This Simple Mix Works

The logic behind the 60/40 split is elegant in its simplicity. Stocks are the horsepower, tapping into economic growth to drive capital appreciation. Bonds, on the other hand, act as the portfolio’s shock absorbers. Historically, when stocks have stumbled, high-quality bonds have often held their ground or even gained value.

This negative correlation is the secret sauce. When panic hits and investors rush to sell stocks, they often flock to the perceived safety of government bonds, pushing bond prices up. That dynamic means one part of your portfolio is working to offset losses in another, smoothing out the entire ride.

The 60/40 portfolio’s strength comes from its built-in discipline. It forces a balance between risk and reward, preventing investors from getting too exposed to any single asset class and the stomach-churning volatility that can come with it.

This built-in risk management is exactly what has made the 60/40 portfolio a benchmark for generations of investors looking for a sensible, middle-of-the-road approach.

A Long History of Performance

The 60/40 portfolio isn't just a neat theory; it has a long and proven history of delivering. It has successfully navigated countless market cycles—bull runs, recessions, high inflation, and geopolitical shocks. Its long-term performance is a testament to the power of a disciplined strategic approach.

As one of the most studied models in finance, the 60/40 split has long been a guidepost for institutional investors. Extensive research drawing on a 122-year global dataset found that the 60/40 portfolio delivered remarkably stable and competitive returns over the long run, often averaging between 6% and 8% annually. You can read the full research about the 60/40 portfolio’s performance to dig into the data yourself.

This track record proves a critical lesson: a simple, well-designed strategic plan can often beat more complex, actively managed strategies over time, largely because it takes emotion and guesswork out of the picture.

The Role of Rebalancing

A key part of making the 60/40 strategy work is periodic rebalancing. This is the disciplined process of selling some assets that have performed well to buy more of those that have lagged, bringing your portfolio back to its original 60/40 target.

For example, let's say a great year for stocks pushes your portfolio to 70% stocks and 30% bonds. Rebalancing means you would:

- Sell 10% of your stock holdings, locking in some of those gains.

- Use that cash to buy bonds, bringing your bond allocation back up to the 40% target.

This process forces you to systematically sell high and buy low without ever trying to time the market. It's the practical mechanism that keeps your portfolio's risk profile in check and enforces the discipline at the very heart of strategic asset allocation.

How To Implement Your Own Strategy

Shifting from theory to practice is where a good idea becomes a great investment plan. Building a strategic asset allocation isn't about complex financial models; it's about honest self-assessment, simple math, and long-term discipline.

We can break the process down into three straightforward phases: laying the foundation, building the frame, and performing regular maintenance on your financial house.

Phase 1: Define Your Investor Profile

Before investing a single dollar, you must know who you are as an investor. This is the most important step, and it requires a candid look at your goals, timeline, and feelings about the market.

- Financial Goals: What is this money for? Are you saving for a retirement 30 years away? A down payment on a house in five years? Or ensuring your wealth lasts for the next generation? Your goals set the target.

- Time Horizon: How long can you leave this money untouched? A longer runway—think 20+ years—generally means you can afford to weather more short-term storms in pursuit of higher long-term growth.

- Risk Tolerance: This is the gut-check question. How would you really feel if your portfolio dropped 20% in a single month? Your emotional capacity to stick with the plan during a downturn is just as critical as your financial capacity.

Nailing this down ensures your strategy is built on personal reality, not a generic formula.

Phase 2: Select Your Target Asset Mix

With a clear investor profile, you can design the actual mix of assets. This is the heart of strategic asset allocation—creating a personalized recipe for your portfolio by assigning specific percentages to stocks, bonds, and perhaps some alternatives.

Here are a few classic examples:

- An Aggressive Profile (a young investor with high risk tolerance) might aim for 80% stocks and 20% bonds.

- A Moderate Profile could use the timeless 60% stocks and 40% bonds model.

- A Conservative Profile (someone near retirement with low risk tolerance) might flip that to 30% stocks and 70% bonds.

The goal is to pick a mix that makes logical sense for your profile and gives you the highest probability of hitting your goals. Many people find that investing with a financial advisor helps bring the clarity and expertise needed to dial in these crucial percentages.

Phase 3: Commit to Periodic Rebalancing

Once your portfolio is running, the final piece is maintenance. Over time, the market's natural movements will cause your chosen mix to drift. This is where rebalancing comes in.

Rebalancing is simply the act of periodically selling a little of what has done well and buying a little of what has lagged to bring your portfolio back to its original target.

Rebalancing is the mechanism that enforces the "buy low, sell high" mantra without emotion. It systematically trims your winners and adds to your underperformers, keeping your risk level consistent with your original plan.

Let’s say a hot stock market pushes your 60/40 portfolio to a 70/30 mix. To rebalance, you would simply sell some stocks and use the proceeds to buy bonds, getting you back to your 60/40 target. The key is to do this on a set schedule—annually or semi-annually works for most—to take emotion and guesswork completely out of the equation.

Still Have Questions?

Even a straightforward investment approach can bring up a few practical questions. Let's walk through some of the most common ones that come up when investors start putting this strategy into practice.

Think of this as a quick way to clear up the details so you can feel confident in your long-term plan.

How Often Should I Review My Strategy?

A strategic asset allocation is designed to be a "set it and forget it" plan for the most part, so you don't need to tinker with it based on every market headline.

A good rule of thumb is to give your portfolio a thorough review once a year. You should also check in after any major life event—like a new job, marriage, or as you near retirement. The goal isn't to second-guess the strategy, but to rebalance back to your targets and ensure the plan still fits your life.

Is This Strategy Good For Young Investors?

Absolutely. Strategic asset allocation is a flexible framework. For a young investor with decades ahead and a higher tolerance for risk, the strategy would simply lean heavily toward growth assets like stocks—maybe an 80% or 90% allocation.

The real power here is the discipline it provides. It helps a young investor stick with that aggressive allocation through the market’s inevitable ups and downs, which is crucial for capturing the full benefit of long-term growth and compounding.

This is where the strategy really shines. A disciplined approach prevents reactive, emotional decisions during market downturns—often the biggest destroyer of long-term wealth.

How Does This Perform In A Downturn?

During a market downturn, the stock portion of your portfolio will take a hit. But this is where the "allocation" part of the strategy proves its worth. The bond portion often stays stable or may even go up, acting as a valuable cushion that reduces the overall volatility of your investments.

Beyond that, the rebalancing discipline forces you to do something that feels counter-intuitive but is incredibly powerful: you sell some of what's done well (the bonds) to buy more of what's fallen in value (the stocks). It’s a systematic way to "buy low" without ever trying to guess the market bottom.

Can I Use ETFs To Build My Portfolio?

Yes, without a doubt. Exchange-Traded Funds (ETFs) and mutual funds are perfect tools for building a strategic portfolio. They give you instant, broad diversification across an entire asset class with a single purchase, like an S&P 500 ETF for US stocks or a global bond fund.

In fact, using just a few low-cost, broad-market ETFs is one of the most efficient and effective ways for almost anyone to build a globally diversified, strategic portfolio.

Building and maintaining a strategic asset allocation tailored to your unique financial situation is the cornerstone of long-term success. At Commons Capital, we specialize in creating personalized investment strategies for high-net-worth individuals and families to help them achieve their most important goals.

Learn how our private wealth management services can work for you.