On the field or court, you compete with a team of elite coaches, trainers, and specialists. Your financial life demands that same level of specialized expertise. Standard financial advice, built for a 40-year corporate career, simply doesn't apply to a professional athlete. You need a playbook designed for your unique career arc—from a large signing bonus to post-career planning. A financial advisor for professional athletes is a critical part of that team.

Why Athletes Need a Different Kind of Advisor

Would you ask a general personal trainer to be your team’s offensive coordinator? They understand fitness basics, but they lack the specialized knowledge to read a defense or design game-winning plays. That’s what happens when an athlete uses a financial advisor who doesn’t live and breathe the sports world. A generalist sees a high-income client. A specialist—a true sports and entertainment wealth advisor—sees your entire financial game clock, from signing day to a retirement that could last decades.

Their work goes beyond picking stocks; it's about tackling the core financial challenges that define your career: short career windows, income volatility, and complex contract structures.

Career-Length Planning and Income Volatility

The biggest difference is the timeline. Your earning window is incredibly compressed. While most professionals have careers spanning decades, research on pro athlete career longevity shows the average career in pro sports lasts just a few years.

This reality means you must generate and protect a lifetime's worth of wealth in a short time. That money needs to support you through a retirement that could easily last 40, 50, or even 60 years.

The goal isn't just to manage a big salary for a few years. It's to convert that burst of high income into a lifetime of financial security. This requires a different playbook for saving, investing, and cash flow.

Sudden Wealth Planning and Intense Pressure

Landing a multimillion-dollar contract brings what’s known as sudden wealth planning, but for an athlete, it's more complex. The wealth is public, bringing a tidal wave of pressure.

- Family and Friends: You almost instantly become the financial hub for your circle, leading to difficult conversations.

- Predatory "Opportunities": Your inbox will be flooded with unsolicited investment pitches and business ideas from unqualified people.

- Lifestyle Inflation: The temptation to immediately upgrade everything—cars, houses, vacations—can risk your long-term security.

A qualified financial advisor for professional athletes acts as your first line of defense, helping you build a disciplined framework to handle these pressures from day one.

The Difference in Strategy

The gap between a traditional financial plan and one for an athlete is massive. One is a career marathon; the other is a sprint followed by an ultra-marathon of retirement.

Traditional vs. Athlete Wealth Management

| Financial Factor | Traditional Professional | Professional Athlete |

|---|---|---|

| Career Length | 30-40+ years | 3-10 years on average |

| Earning Curve | Income peaks in 50s/60s | Income peaks in 20s/30s |

| Income Stability | Generally predictable | Volatile; based on contracts, incentives, endorsements |

| Tax Complexity | Primarily single-state filings | Multi-state "jock taxes," complex bonus structures |

| Retirement Horizon | Planning for 20-30 years | Planning for 40-60+ years |

The strategies that work for a doctor or lawyer don't apply here. Choosing the right advisor is one of the most critical financial decisions of your career. It’s about finding a partner who truly understands your world, the pressures you face, and the incredible opportunities you have.

Managing Income from Draft Day to Retirement

For a professional athlete, financial life is defined by volatility. Income isn't a predictable salary; it's a mix of signing bonuses, performance incentives, endorsement deals, and off-season income drops. A standard budget can’t keep up.

This is where a sports and entertainment wealth advisor becomes a critical part of your team. They help you build a financial system that turns unpredictable income into a stable, growing asset base. The goal is to create a foundation strong enough to withstand an injury, a trade, or your eventual transition out of the game.

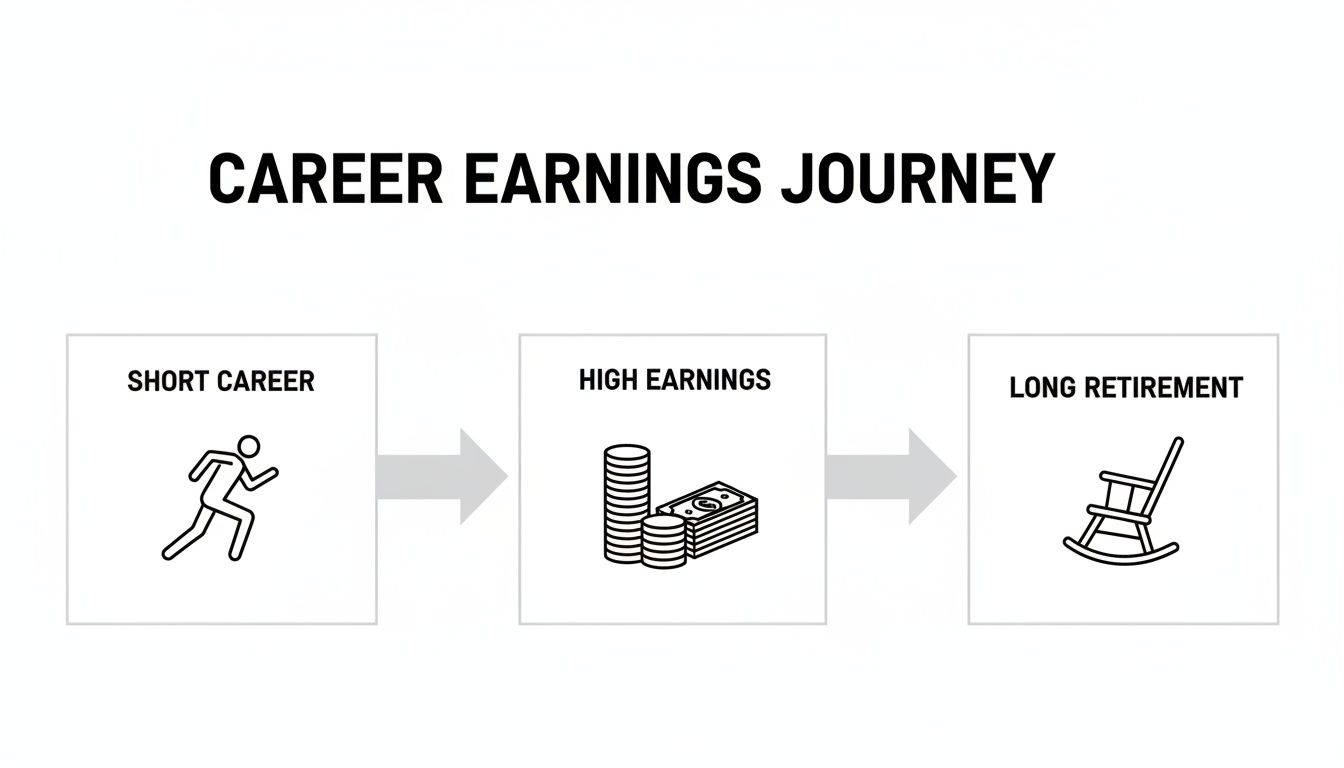

The chart below shows the unique financial path of a professional athlete: a short, high-earning career that must fund a very long retirement.

This visual highlights the core challenge of wealth management for professional athletes. You have a compressed time frame to earn and invest enough to support a retirement that can last more than four times your playing career.

Your Personal Salary Cap

One of the most effective tools for handling large, uneven paychecks is a personal salary cap. It works like a team's budget but for your personal finances, creating a line between lifestyle spending and long-term investment capital.

Instead of letting spending habits inflate with every bonus, you pay yourself a fixed "annual salary." This is the money you live on. Any income above that is automatically sent to other accounts with specific jobs.

By paying yourself a consistent salary, you break the cycle of lifestyle inflation. It transforms unpredictable windfalls from temptations into powerful tools for accelerating your long-term financial goals.

The Power of Financial Buckets

With a personal salary cap, a "bucket strategy" automates where every dollar goes. Your advisor helps structure separate accounts, each with a clear purpose. When a check hits, funds are automatically distributed.

This method takes emotion out of your finances. You never have to decide what to do with a bonus; the system is set.

- Tax Bucket: The first and most important bucket. A large slice of every payment, often 30-40% or more, is set aside for federal, state, and "jock" taxes.

- Investment Bucket: Your wealth-building engine. The majority of your after-tax income flows here, funding a diversified portfolio for a multi-decade retirement.

- Lifestyle Bucket: This receives your "personal salary" and covers day-to-day expenses like housing, cars, food, and travel.

- Emergency Fund: A crucial safety net holding 12-24 months of living expenses in a safe, liquid account to protect you from a career-ending injury or lockout.

This financial discipline is becoming more common. A recent study shows today's young pros are prioritizing their future, allocating an average of 36% of their earnings to savings and investments. You can read more about how young athletes manage their money in the full report.

Contract Structures and Tax Implications

That headline number on your contract is a milestone, but it’s not what you’ll take home. A pro contract has major tax consequences. This is where a financial advisor for professional athletes becomes non-negotiable, working to protect your after-tax pay from the moment a deal is on the table.

This process means diving deep into every line of your compensation, turning dense legal language into a clear financial game plan. It’s critical that your advisor, agent, and accountant operate as a single unit.

Understanding Your Contract Structure

Your pay is more than a base salary. An expert in wealth management for athletes and entertainers will dissect these components to boost your bottom line:

- Signing Bonuses: This is often your biggest single check. Strategically timing when you receive it can dramatically change your tax bill.

- Incentive Clauses: Getting paid for playoffs or performance benchmarks is all taxable income. A good plan anticipates this cash and has tax funds set aside.

- Deferred Compensation: By agreeing to get part of your salary later, often post-retirement, you can potentially push the tax hit into a lower tax bracket.

It's not about the gross number on the contract; it's about the net amount that funds your future. A proactive tax strategy can be the difference of hundreds of thousands, or even millions, of dollars over your career.

Looking at general contract templates can help you understand the types of clauses that appear in legal agreements and make sense of your own specialized athletic contract.

Demystifying the Dreaded Jock Tax

The "jock tax" is an income tax states and cities charge non-resident athletes for money earned while playing there. Without a plan, it becomes a multi-state tax nightmare.

A sports and entertainment wealth advisor works with a tax pro to track these "duty days" and file what can be a dozen or more state tax returns. They also ensure you get credits for taxes paid to other states to avoid being double-taxed.

Proactive Tax Reduction Strategies

Winning the tax game requires a year-round offense. A financial advisor who understands your unique career will use specific plays to lower your tax burden. Dive deeper into these tactics in our guide on the best tax strategies for high-income earners.

Key strategies include:

- Establishing Residency: Living full-time in a state with no income tax (like Florida, Texas, or Nevada) means a big chunk of your income could grow tax-free at the state level.

- Maximizing Retirement Accounts: Your advisor will help you max out every tax-advantaged retirement account available, like a league 401(k) or a SEP IRA for endorsement income.

- Structuring Endorsements: Setting up an LLC or S-Corp for your business activities can unlock powerful deductions for business-related expenses.

Building Wealth Beyond the Playing Years

The real win isn't your last contract; it's what your wealth can do long after the final whistle. This is where the game shifts from aggressive wealth accumulation to smart, long-term preservation. It's time to build a championship-level defense to protect what you've earned for generations.

The goal is to build a diversified, self-sustaining financial machine that works for you. This means looking beyond stocks and bonds and tapping into the modern investment landscape now open to elite athletes.

Expanding Your Investment Playbook

The old-school "60/40" portfolio is just the starting point. Your high net worth unlocks access to opportunities most people never see. A sports and entertainment wealth advisor can help you vet a broader universe of assets designed for long-term income and growth.

- Private Equity: Invest directly in private companies not traded on the stock market for the potential of higher returns.

- Venture Capital: Fund early-stage startups with explosive growth potential. It's higher risk, but the rewards can be massive.

- Strategic Real Estate: Acquire income-producing properties like apartment complexes or commercial buildings to generate steady, passive cash flow.

The modern sports investment landscape has evolved. Athletes are gaining economic power beyond contracts through equity deals, ownership stakes, and sophisticated alternative investments.

From Personal Brand to Business Empire

Your name is a valuable asset. Making the leap from endorser to owner is a critical part of modern wealth management for professional athletes. Instead of taking a check to promote a product, you can use your influence to negotiate an equity stake, aligning your success with the company's growth.

Protecting Your Legacy

Building a legacy requires careful estate planning to ensure your wealth is transferred smoothly and tax-efficiently. This legal framework is your financial armor, including trusts, wills, and powers of attorney. Smart planning also means preparing for the unexpected, which could involve exploring legal structures like guardianship for athletes and performers managing high-value careers.

A well-designed estate plan makes sure your financial legacy supports your family for decades. To go deeper, check out our guide on building generational wealth.

Red Flags in Advisors Who Target Athletes

Your high profile and large paychecks make you a target. For every solid financial advisor for professional athletes, there are dozens of unqualified—or predatory—people looking to get your money. Knowing what to watch for is your best defense.

An estimated 78% of former NFL players face financial distress just two years into retirement, often due to mismanagement or bad advice. Vetting anyone managing your money is crucial. Spotting these red flags can save you from a career-ending financial loss.

Pressure Tactics and Unrealistic Promises

One of the biggest red flags is an advisor who promises the world. If it sounds too good to be true, it is.

Watch for these warning signs:

- "Guaranteed" High Returns: No real investment comes with a guarantee of high returns without equally high risk. Phrases like "can't-miss" or "a sure thing" are a salesman's language.

- Pressure to Act Immediately: A predator creates a false sense of urgency. A true pro wants you to take your time and understand the investment.

- Focus on High-Commission Products: If an advisor keeps pushing specific products, their paycheck may be tied to that sale, not your success.

A fiduciary advisor's loyalty is to you. A salesperson's loyalty is to their commission. Know the difference before you sign anything.

Lack of Transparency and Isolation Attempts

A trustworthy advisor works in the open; a shady one prefers the shadows. They may try to cut you off from your team (agent, attorney) to operate without oversight.

Pay close attention to these behaviors:

- Vague Fee Structures: You should get a simple document explaining how your advisor gets paid. Ask them point-blank: "Are you a fee-only fiduciary?"

- Discouraging Second Opinions: A great advisor is confident and encourages discussion with your team. Someone who discourages this is trying to consolidate power.

- Requesting Control of All Assets: Be cautious of anyone asking you to wire all your money to an account they control. Your assets should be held by a neutral third-party custodian like Fidelity or Charles Schwab.

The Fiduciary Standard is Non-Negotiable

The single most important question you can ask is whether an advisor is a fiduciary. A fiduciary is legally required to act in your best interest. Always. Many brokers only meet a "suitability standard," meaning their recommendation is merely suitable, not necessarily the best option. For a professional athlete, working with anyone who isn't a full-time fiduciary is an unnecessary risk.

Assembling Your Championship Financial Team

Winning with your money is a team sport. After handling sudden wealth, navigating taxes, and mapping out a long-term strategy, the last piece is putting the right pros in your corner.

Think of your financial life like a franchise. You're the owner; your sports and entertainment wealth advisor is the GM. Our job is to be that central hub, coordinating with your agent, attorney, and accountant so everyone is aligned on one goal: your lasting financial security.

A Partnership for a Lasting Legacy

At Commons Capital, our sports and entertainment practice is built to solve the unique financial challenges athletes face.

This isn't just about managing money. It's about building a durable financial legacy. It’s a partnership focused on turning your hard-earned success into generational security.

When you work with a dedicated financial advisor for professional athletes, you get a partner who sees blind spots before they become problems. See our detailed guide on choosing the right financial advisor for athletes.

Your career was defined by excellence. Your financial future should be, too.

Your career demands excellence, and your financial future deserves the same. At Commons Capital, our specialized sports and entertainment practice is designed to help you navigate these unique challenges and build a lasting legacy. Learn about our sports and entertainment practice.