When you hear people discussing the topic of trust vs living trust, it's easy to get tangled in the terminology. The most crucial thing to remember is that a living trust is simply one specific type of trust. A helpful analogy is: all living trusts are trusts, but not all trusts are living trusts. This guide will clarify the key distinctions.

The broader category of "trust" includes various legal arrangements, such as a testamentary trust created through your will, which only becomes active after you're gone. Your choice ultimately boils down to a simple question: when do you want the trust to become effective, and how much control do you wish to retain over your assets?

Understanding the Basics of Trusts and Living Trusts

Before diving into the differences, let's cover the foundational structure that every trust shares. A trust is a legal arrangement built around three crucial roles, all designed to manage and protect assets for the future.

- Grantor: This is you—the person who creates the trust and transfers your assets into it.

- Trustee: The individual or institution you appoint to manage the trust's assets according to your instructions.

- Beneficiary: The person, people, or organization who will ultimately receive the assets from the trust.

A living trust—also known by its legal name, an inter vivos trust—is a trust you create and fund while you're still alive. A significant advantage of this structure is that you can name yourself as the initial trustee, meaning you keep full control over your assets for as long as you live. You'll also name a successor trustee who takes over after your death, ensuring a seamless transfer of assets without court involvement. You can learn more about how this structure avoids probate by exploring insights from estate planning experts.

Key Foundational Differences

The most critical distinction is timing. A living trust is operational during your lifetime, offering immediate flexibility and, just as importantly, privacy.

Other types of trusts, like a testamentary trust, are created by your will and only come into existence after you pass away. This means the assets must first go through the public probate process, which can be time-consuming and costly. To make this clearer, let's break down the core differences in a simple table.

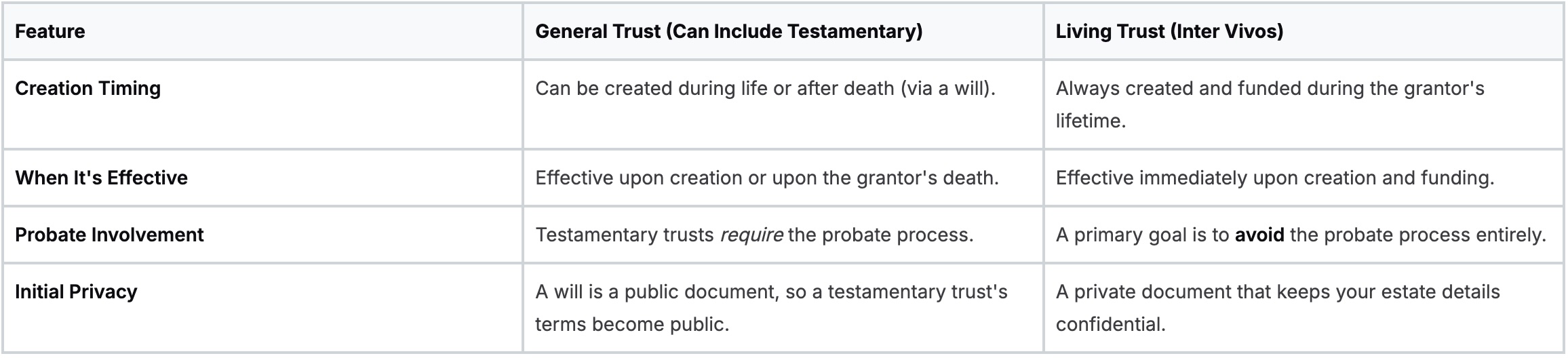

Core Differences: General Trust vs. Living Trust

This table provides a quick, high-level summary of the fundamental distinctions between these two estate planning approaches.

As you can see, the decision isn't just about managing assets—it's about control, privacy, and efficiency. A living trust gives you a head start on all three.

Who's Really in Control? Flexibility and Asset Management

When you dig into the world of trusts, the conversation always circles back to one critical point: control. The line between a revocable and an irrevocable trust determines your power to change your mind and adapt your estate plan as life unfolds. This is at the heart of the trust vs. living trust debate.

Most living trusts are set up to be revocable, and for a good reason. This design gives you, the grantor, the ultimate financial freedom. You can rewrite the terms, move assets in or out, or even dissolve the entire trust whenever you want. No questions asked.

The Power of a Revocable Living Trust

Think of a revocable living trust as a flexible container for your assets. You can name yourself the trustee, which means you keep complete authority over everything inside it. Want to sell the house that's in the trust? You can. Need to change your beneficiaries after a divorce or the birth of a grandchild? You can do that in an afternoon.

This structure is perfect for anyone who wants to organize their estate for a smooth transition after they're gone but isn't ready to give up control today. It also establishes a clear succession plan if you become incapacitated, allowing your chosen successor trustee to manage your affairs without court intervention.

A revocable structure gives you the power to adapt your estate plan to life's inevitable curveballs—a new marriage, a growing family, or a major change in your financial picture. It keeps your plan relevant and perfectly aligned with your current wishes.

When an Irrevocable Trust Makes Sense

In sharp contrast, an irrevocable trust is built to be permanent. Once you sign the documents and fund the trust, those assets are no longer yours to control. You can't just take them back. That sounds incredibly restrictive, but this permanence serves some very powerful goals.

By officially giving up control, you legally sever the assets from your personal estate. This is a common strategy for:

- Asset Protection: Building a wall around your wealth to shield it from future creditors or lawsuits.

- Estate Tax Reduction: Moving assets out of your taxable estate to shrink the potential tax bill for your heirs.

- Qualifying for Government Benefits: Reducing your countable assets to become eligible for programs like Medicaid.

While a revocable living trust lets you stay in the driver's seat, an irrevocable trust offers a different kind of power—protection. As explained in this breakdown of trust privacy and protection benefits on lifegenlawgroup.com, the legal separation created by an irrevocable trust is key to its strength.

Ultimately, your choice boils down to what you're trying to achieve. If your top priority is maintaining control and flexibility throughout your life, a revocable living trust is almost always the answer. But if your main focus is asset protection and sophisticated tax planning, the rigid, permanent nature of an irrevocable trust might be exactly what you need.

Comparing the Financial Costs and Setup Process

When you start comparing trusts, the conversation inevitably turns to money. A living trust almost always has a higher price tag upfront compared to a simple will that includes a testamentary trust, but that initial spend is a strategic investment designed to unlock major savings down the road.

The bulk of the initial cost for a living trust comes from two things: the attorney’s fees for drafting the document and the administrative legwork of moving your assets into it. This crucial step, known as funding the trust, means retitling real estate deeds, bank accounts, and investment portfolios so they are legally owned by the trust, not by you personally.

It might sound like a hassle, but this is the single most important part of the process. A living trust that isn't properly funded is essentially an empty vessel, forcing those assets through the very probate process you were trying to avoid.

Breaking Down the Initial Investment

Setting up a living trust is a meticulous, hands-on process. The cost is a real factor, and it's a key difference when deciding between a living trust and a will. Having an attorney draft and help fund a living trust can run up to $7,000. In contrast, a will is often much less expensive, sometimes under $1,000.

These figures reflect the complexity involved. The higher cost of a living trust accounts for not just drafting the document but also for transferring assets, like a property deed, which can add another $100–$200 per transfer.

A testamentary trust, on the other hand, has almost no upfront cost because it's just a set of instructions tucked inside your will. The real expenses for that type of trust come later—they are paid by your estate during probate, which can diminish the inheritance left for your beneficiaries.

The Long-Term Return on Investment

The true financial benefit of a living trust becomes crystal clear after you're gone. A properly funded living trust is specifically designed to bypass probate, which is the court-supervised process of validating a will and distributing assets.

A living trust's higher initial cost is often an investment in future efficiency. It can save an estate thousands—or even tens of thousands—of dollars by sidestepping court fees, appraisal costs, and executor expenses associated with a lengthy probate.

This is an absolutely critical point in estate planning for wealthy individuals, where probate costs can scale up with the size of the estate. A living trust ensures your assets are transferred privately, quickly, and cost-effectively. It preserves not just your wealth, but also your family’s privacy and peace of mind during an incredibly difficult time. That initial setup fee is buying you a much smoother process later on.

The Critical Role of Probate and Privacy

When you get down to the brass tacks of the trust vs living trust debate, the conversation almost always lands on two huge benefits: avoiding probate and maintaining privacy. For many families, these advantages alone are enough to make a living trust the clear winner, turning what could be a public mess into a quiet, private affair.

Probate is the court-supervised process of validating a will and distributing assets after someone passes away. On paper, it sounds straightforward. In reality, it’s notoriously public, slow, and expensive. Every detail of your will—who gets what, how much they receive, and any special conditions—becomes public record. Anyone can look it up.

This lack of privacy can be incredibly uncomfortable for a grieving family. On top of that, the process itself racks up costs. Court fees, attorney fees, and executor commissions can eat away at the value of your estate, sometimes consuming 3% to 8% of its total worth before your beneficiaries see a dime.

How a Living Trust Protects Your Privacy

A properly funded living trust offers a direct route around all that public exposure. Since the trust legally owns the assets, there's nothing for the probate court to manage. When you pass away, your chosen successor trustee simply steps in to manage and distribute the assets according to the private instructions you left in the trust document.

The entire process happens completely outside the public eye.

A living trust ensures the transfer of your wealth remains a confidential family matter. It shields your beneficiaries from unsolicited financial advice, nosy neighbors, and the public scrutiny that probate practically invites.

This private administration doesn’t just protect your family’s privacy—it also dramatically speeds up the distribution of assets. While probate can drag on for months or even years, a successor trustee can often start distributing assets within weeks. That provides critical financial support to your loved ones exactly when they need it most.

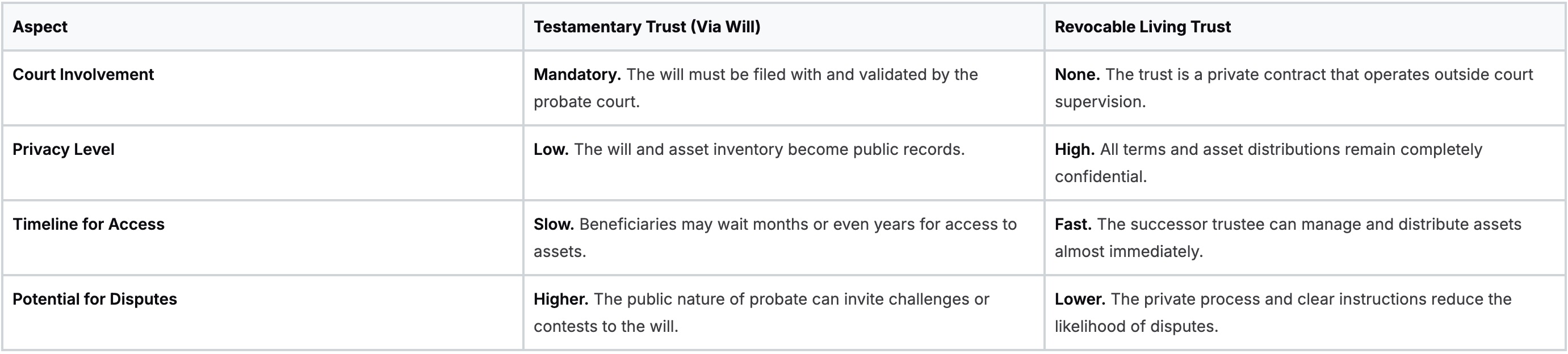

Probate and Privacy Implications Compared

The difference in what your beneficiaries will experience is stark. A will forces them to deal with a court system, wait for legal approvals, and watch as their inheritance details are made public. A living trust allows them to work directly with a trusted individual—your successor trustee—to settle your affairs quickly and privately.

Here’s a clear look at how the two approaches stack up when it comes to the post-death process.

Ultimately, choosing a living trust often comes down to prioritizing your family’s peace of mind. By sidestepping probate, you’re removing a major source of stress, cost, and public exposure from an already difficult time.

How to Choose the Right Trust for Your Needs

Moving from theory to practice means matching your personal goals to the right legal tool. The conversation isn’t really about trust vs. a living trust; it’s about figuring out which specific trust structure—like a revocable living trust or an irrevocable one—actually serves your unique circumstances. Your choice ultimately hinges on your priorities, from avoiding probate to protecting your assets for the long haul.

A revocable living trust is often the go-to choice if your primary goals are straightforward and centered on creating efficiency after your death. This path makes the most sense if you want to ensure your estate sidesteps the public, often costly, and time-consuming probate process.

When a Living Trust Is the Clear Choice

Think about opting for a revocable living trust if you find yourself nodding along with these scenarios:

- You Prioritize Probate Avoidance: Your main objective is to let your assets pass directly to your heirs without court intervention, saving them a great deal of time, money, and stress.

- You Own Real Estate in Multiple States: A living trust neatly simplifies the transfer of out-of-state properties, helping you avoid separate, complex probate proceedings (known as ancillary probate) in each state.

- You Value Privacy: You prefer the details of your estate—who gets what and how much—to remain a confidential family matter, shielded from public record.

- You Want a Plan for Incapacity: A living trust allows your chosen successor trustee to manage your finances seamlessly if you become unable to do so, all without needing a court-appointed conservatorship.

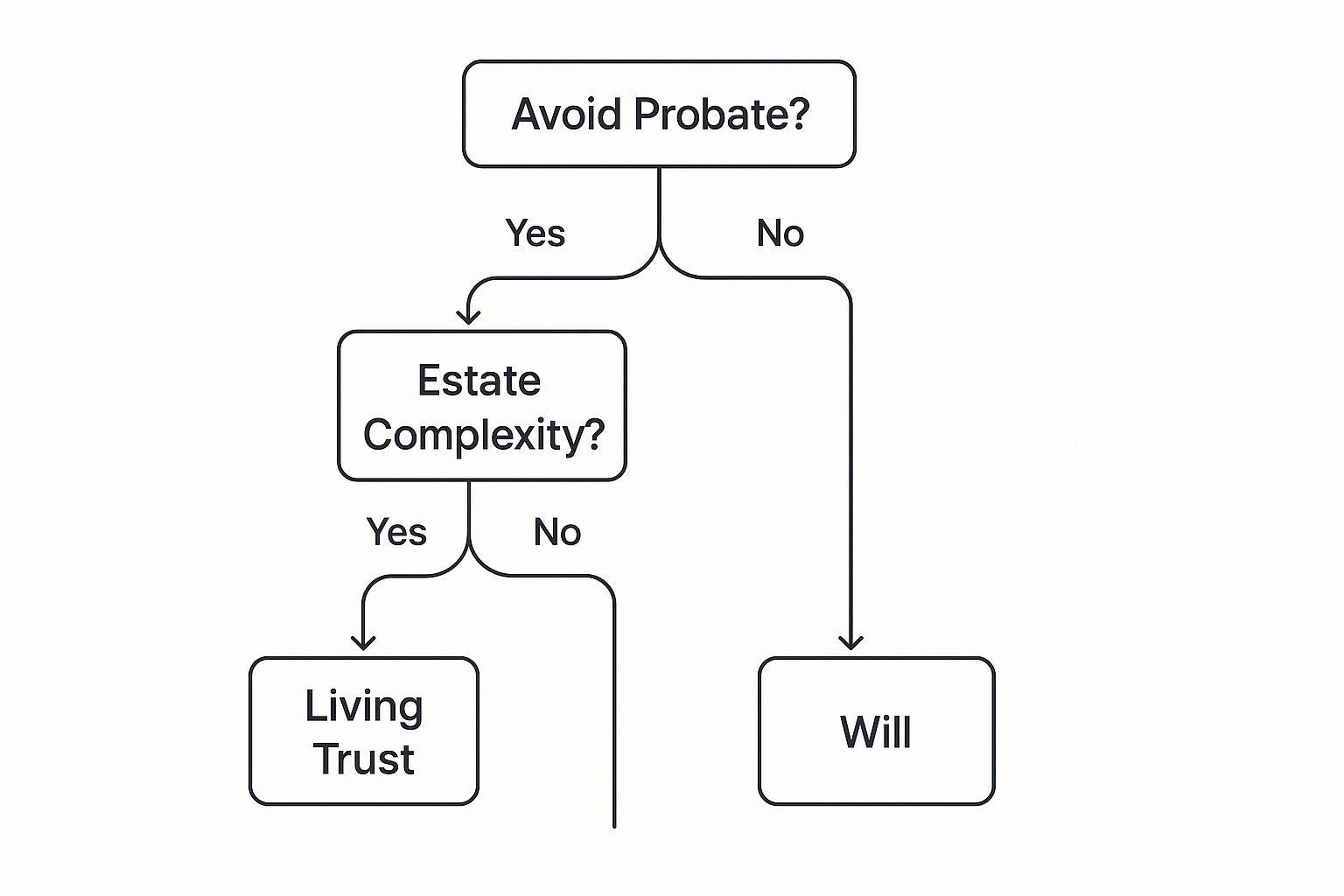

This decision tree can help you visualize the key questions that point toward either a living trust or a simple will.

As the infographic shows, if you're answering "yes" to questions about avoiding probate, managing a complex estate, and keeping things private, a living trust is almost certainly the more effective solution for you.

When Other Types of Trusts Are More Suitable

However, a revocable living trust isn't a silver bullet. Different goals require different tools, and if your financial picture involves more complex challenges, another type of trust might be a much better fit.

For instance, if your primary concern is shielding your wealth from potential future creditors, lawsuits, or the staggering costs of long-term care, an irrevocable trust offers a level of asset protection that a revocable trust simply can't match. By transferring assets into an irrevocable trust, you legally separate them from your personal estate, placing them beyond the reach of certain claims.

Choosing the right trust means looking beyond probate. For high-net-worth individuals, the strategic advantages of asset protection or estate tax mitigation offered by an irrevocable trust can be far more valuable than the simplicity of a revocable trust.

Likewise, for someone with a very straightforward and modest estate, a testamentary trust (which is created through a will) might be perfectly sufficient. This approach is less expensive upfront, but it's crucial to remember it guarantees the estate will go through probate.

Ultimately, the best path forward involves a clear-eyed assessment of your assets, your family dynamics, and your long-term goals. Consulting with a professional can help you navigate these important decisions, and our team is experienced in comprehensive trust and estate planning to guide you.

Making Your Final Estate Planning Decision

So, where does that leave us in the trust vs living trust comparison? The real takeaway isn't about pitting a "general trust" against a "living trust." It's about recognizing that a living trust is a specific, powerful tool within the broader world of trusts, crafted to solve very modern estate planning problems.

Your decision ultimately comes down to what you want your legacy to accomplish.

Let's boil it down. If your main goals are maintaining control over your assets while you're alive, keeping your family's affairs private, and sidestepping the headaches and costs of probate, a revocable living trust is almost always the right instrument. Its flexibility is a huge advantage—you can adapt it as your life changes, and it ensures a seamless, private transfer of wealth when the time comes.

On the other hand, if your financial situation involves more complex challenges, like shielding assets from creditors or navigating sophisticated tax-minimization strategies, then other types of trusts might be a better fit.

Taking the Next Step

No article, no matter how detailed, can substitute for a one-on-one conversation with a legal expert. The single most important step you can take is to sit down with an experienced estate planning attorney. They have the expertise to assess your specific financial landscape, understand your family dynamics, and help you map out your long-term goals.

Taking proactive control of your estate is one of the most empowering financial decisions you can make. It ensures your legacy is protected and your wishes are honored efficiently and privately, providing true peace of mind for you and your loved ones.

By moving forward now, you’re not just organizing paperwork—you’re securing your family’s future and defining your legacy on your own terms. For a deeper look at why this planning is so critical, you can explore our guide on if you need an estate plan.

Your Top Trust Questions, Answered

Working through the specifics of estate planning always brings a few key questions to the surface. Let's tackle some of the most common ones that come up when deciding between trust structures.

Can I Have Both a Will and a Living Trust?

Yes, and you absolutely should. A will and a living trust aren’t competitors; they’re partners in a well-built estate plan. Your living trust handles the assets you’ve moved into it, but a special kind of will, called a pour-over will, acts as a crucial safety net.

Think of it this way: a pour-over will is designed to "catch" any assets you might have forgotten to transfer into your trust or acquired right before your death. When you pass away, the will simply directs those stray assets into your trust, making sure everything is distributed just as you intended. It’s the best way to ensure comprehensive coverage.

Are All Living Trusts Revocable?

The vast majority of living trusts are set up to be revocable, giving you complete flexibility to make changes during your lifetime. But that's not the only option. It's entirely possible to establish an irrevocable living trust right from the start.

Why would someone do that? It usually comes down to very specific, strategic goals:

- Asset Protection: Building a wall around your wealth to protect it from future lawsuits or creditors.

- Estate Tax Reduction: Moving assets out of your taxable estate to minimize the tax burden on your heirs.

- Medicaid Planning: Structuring your finances to meet eligibility requirements for long-term care benefits.

Going the irrevocable route means you permanently give up control over those assets, so it's a significant decision that demands very careful consideration.

Does a Living Trust Protect My Assets from Creditors?

This is a common point of confusion. A standard revocable living trust does not offer any protection from your own creditors. Since you keep full control and can dissolve the trust anytime you want, the law still sees those assets as yours. That means they’re fair game in a lawsuit.

For genuine asset protection, you need an irrevocable trust. By giving up ownership and control, you create a legal separation that can effectively shield those assets from future claims.

Understanding this distinction is one of the most important factors when deciding which trust structure fits your personal needs.

Should I Put My Retirement Account into My Living Trust?

As a general rule, you should not transfer tax-deferred accounts like a 401(k) or an IRA into your living trust. If you do, it’s treated as a full withdrawal, which can trigger a massive income tax bill and potential early withdrawal penalties.

Instead, these accounts are passed to your heirs through beneficiary designations. It is absolutely critical to review and update these designations regularly. They operate independently and will override any instructions you have in your will or trust.

At Commons Capital, we specialize in guiding high-net-worth families through these important financial decisions. To create a strategy that secures your legacy, visit us online to learn more.