It’s tough to even think about stepping away from a business you’ve poured your life into. I get it. But succession planning for small business isn’t just some distant exit strategy—it’s the single most important plan you can create to protect everything you’ve built.

Your legacy, your employees, and your own financial future all depend on it. Without a plan, you're essentially leaving the fate of your company to chance.

Why Succession Planning Is Your Most Important Strategy

For most small business owners, the daily grind is all-consuming. Long-term planning often gets pushed to the back burner. It’s so easy to think, "I'll deal with that later."

But putting off your succession plan is one of the biggest gambles you can take with your business. This isn't just about retirement; it's a critical safeguard against the unexpected, ensuring a smooth transition no matter what life throws your way.

A well-crafted plan does far more than just name who's next in line. It creates a clear roadmap for the transfer of leadership, guarantees operational continuity, and shores up the company’s financial stability. It's a proactive move that protects both your company's value and its unique culture.

The Coming 'Silver Tsunami'

The need for this kind of planning is becoming more urgent by the day. We’re in the middle of a massive demographic shift, often called the "silver tsunami."

Think about these numbers: in 2025, over 4.2 million Americans are turning 65. On top of that, more than half of all small business owners are already aged 55 or older. This retirement wave is forcing a huge number of owners to think about their next chapter, all at the same time.

This means if you're considering selling or transitioning your business, so are thousands of your peers. A documented, thoughtful succession plan makes your business far more attractive and resilient in what’s quickly becoming a very crowded market.

A succession plan is like insurance for your legacy. You hope you won’t need it unexpectedly, but you'll be profoundly grateful it’s there when the time comes. It transforms uncertainty into a structured, manageable process.

The Real Cost of Procrastination

Let me paint a picture I’ve seen play out too many times. The owner of a successful local manufacturing firm has a sudden health crisis, forcing an abrupt departure. Without a plan, chaos erupts.

Key employees don't know who's in charge, nervous clients start looking elsewhere, and the family is left to make monumental decisions under incredible stress. The business, once a pillar of the community, sees its value plummet as uncertainty takes over.

This isn't a hypothetical scare tactic; it’s the reality for countless businesses that fail to prepare. The absence of a plan almost always leads to a painful fallout:

- Internal Conflict: Disagreements erupt among family members, partners, or key employees over who should take the reins.

- Loss of Value: A forced or rushed sale nearly guarantees you'll get a lower price than you would with a planned transition.

- Operational Disruption: Without a clear leader and defined processes, daily operations can quickly fall into disarray.

- Damaged Legacy: The business you worked so hard to build could falter or even shut its doors for good.

Effective succession planning is also a cornerstone of your personal financial strategy. It's crucial to integrate your business exit with your overall financial goals. To see how these two critical areas overlap, explore our insights on wealth management for business owners. By preparing now, you not only secure the future of your business but also solidify your own financial well-being for the years ahead.

Defining Your Vision Before You Plan Your Exit

Before you even think about the paperwork, we need to talk about the destination. Too many business owners jump straight into the legal and financial weeds of succession planning. That’s a mistake. The best plans start with a brutally honest look at what you really want for yourself and for the company you poured your life into.

This first step is all about setting your compass. It ensures your exit isn't just a transaction but a genuine reflection of your legacy. This process breaks down into two equally critical parts: getting a real number on what your business is worth and clarifying what a "successful" exit actually looks like to you.

What Is Your Business Really Worth?

Every owner has a gut feeling about what their business is worth. Now it's time to ground that feeling in reality. A formal business valuation gives you the objective data you need for any serious conversation, whether it's with a family member, a key employee, or an outside buyer.

For most small businesses, valuations typically fall into a couple of main buckets:

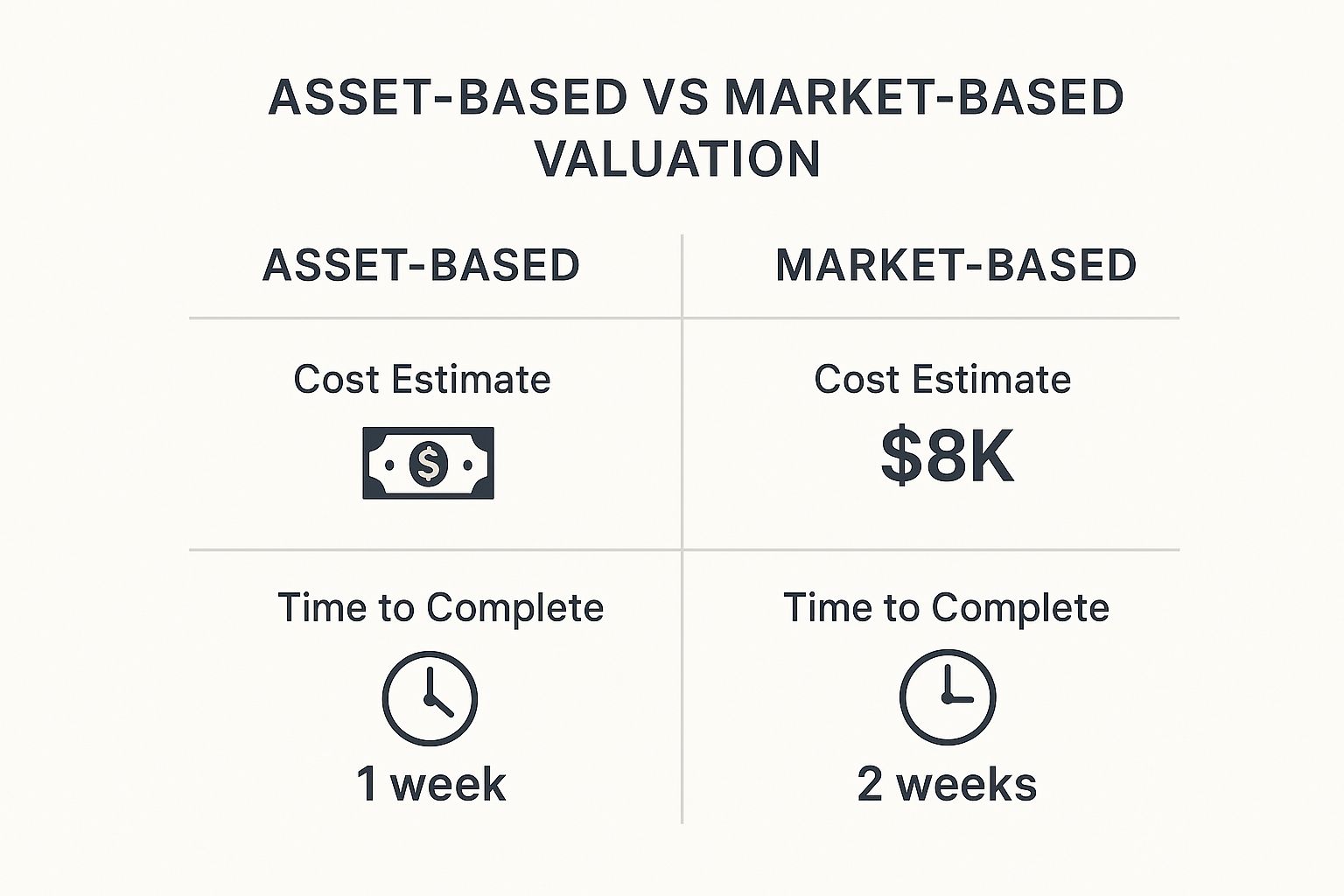

- Asset-Based Valuation: This is the most straightforward method. You simply add up all your assets (cash, equipment, real estate, inventory) and subtract your liabilities (debts, loans). It’s a clean balance sheet calculation, often used when tangible assets are the main source of the company's value.

- Market-Based Valuation: This approach is a lot like pricing a house. You look at what similar businesses in your industry and region have sold for recently. These "comps" give you a realistic picture of what the market is willing to pay right now.

While you can do some homework on your own, investing in a professional valuation is almost always money well spent. An expert provides an unbiased, defensible number that successors, banks, and lawyers will take seriously.

This infographic gives you a sense of the cost and timeline involved for these two common approaches.

As you can see, a market-based valuation generally costs more and takes longer, but it's often the most accurate reflection of your company's true market price.

Aligning Your Personal Goals With Your Business Exit

The numbers tell you what's possible, but your personal goals tell you what's right. This is where you have to move beyond the spreadsheet. A successful exit isn't just about the final sale price; it's about what that transition allows you to do next.

Your personal definition of a "successful" exit is the true north of your succession plan. A high sale price means little if it comes at the cost of your legacy or family relationships.

Think about it this way. The owner of a precision machine shop might be laser-focused on getting the highest possible price from an outside buyer. Her goal is simple: fund a comfortable retirement and make a clean break. Maximum financial return is her definition of success.

On the other hand, the founder of a beloved local bookstore might have a completely different priority. For her, success means preserving the shop's unique culture. A lower-priced sale to a long-time employee who shares her vision is a far greater win than a bigger offer from a chain that would gut everything she built.

Key Questions To Define Your Succession Vision

To get clear on your own priorities, you need to ask yourself some tough questions. Your answers will become the blueprint for the entire plan.

- What does your ideal post-business life look like? Do you want to stay involved as a consultant? Or do you want to hand over the keys and never look back?

- How important is it to maintain the company's culture and values? Are you okay with a new owner making significant changes?

- What's your timeline? Are you aiming for a quick exit in the next year, or a gradual, five-to-ten-year handover?

- Who do you want to benefit most? Is the top priority your family’s financial security? Rewarding loyal employees? Ensuring the business remains a pillar of the community?

Thinking through these questions honestly is the first—and most important—step. It's how you align the financial reality of your business with your personal vision for the future, setting the stage for an exit that truly honors all your hard work.

Choosing Your Successor and the Right Transition Path

Deciding who will take over your business is probably the single most personal—and high-stakes—choice you'll make in this entire process. This isn't just about cashing out; it's about passing on your legacy, your vision, and years of hard work. The right person can build on what you've created, while the wrong one can see it all unravel.

At the same time, you have to figure out how you're going to make the transition. For most small business owners, it boils down to four main routes: passing it to family, selling to your management team, creating an employee stock ownership plan, or selling to an outside buyer. Each option comes with its own unique mix of financial outcomes, control, and impact on your company’s culture.

Identifying and Vetting Potential Successors

Whether you're looking at a family member, a key manager, or an outside buyer, you have to be brutally objective. Emotion is the enemy here, especially when family is involved. A potential successor needs way more than the right last name or a few years of experience; they need the right blend of leadership, vision, and a deep understanding of how the business actually works.

As you think about who could take the helm, it's helpful to get some insights into what future leaders look like. This isn’t just about their current skills, but about their potential to grow into the role.

Use a structured approach to evaluate anyone on your shortlist. Here are the non-negotiables:

- Leadership and Vision: Can they genuinely inspire a team? Do they have a clear strategic vision for the future that still honors the company's roots?

- Financial Acumen: Do they truly get the numbers? I'm talking about everything from profit margins to cash flow management.

- Operational Expertise: Do they know the nuts and bolts of the business? Can they solve problems and make tough calls under pressure?

- Cultural Fit: Do they live and breathe your company’s core values? This is absolutely critical for keeping your team and your clients happy.

The Family Business Dilemma

For many founders, the dream is to pass the business down to the next generation. It’s a powerful idea, but it's a path riddled with potential landmines. The biggest risk? Letting personal family dynamics poison professional decisions.

The stats on this are pretty sobering. The truth is, most family businesses just don't make it.

Only about 30% of family businesses survive into the second generation. That number plummets to just 12% by the third generation, and a tiny 3% make it to the fourth.

To have any chance of succeeding, a family handover has to be treated like a formal business deal, not a casual inheritance. Your son, daughter, or nephew has to earn the job on merit and be held to the same standards as any outside candidate.

Comparing Small Business Succession Pathways

Your personal goals, financial needs, and desired timeline will point you toward the right transition path. There's no single "best" option—only the one that's best for you.

The table below breaks down the pros and cons of the four main succession pathways, helping you see at a glance which one might align best with your priorities.

Each of these paths leads to a very different future for both you and your company. Take the time to honestly assess what matters most to you—is it the money, the legacy, or the people? Your answer will make the choice much clearer.

A Closer Look at Your Options

Management Buyout (MBO)

An MBO is where your existing managers buy the company from you. This can be a fantastic way to keep the company culture intact, since the new owners are already deeply invested. The biggest hurdle is usually money. Your management team probably doesn't have the cash for a full buyout, so you may need to offer seller financing or help them secure outside loans.

Employee Stock Ownership Plan (ESOP)

An ESOP is a special type of employee benefit plan that gives your team an ownership stake. It’s a great way to reward loyal employees, and it comes with some serious tax breaks for you as the seller. But setting one up is a complex and expensive legal process, making it a better fit for larger small businesses with a solid track record of profitability.

Outside Sale

Selling to an external third party—whether it’s a competitor or a private equity firm—is often the route to the biggest payday. It gives you a clean exit. The trade-off, however, is that you give up almost all control over the company's future. If getting the highest price is your number one priority, this is a path that requires meticulous preparation to maximize your final valuation.

Turning Your Vision into an Actionable Succession Plan

With a clear vision and a potential successor in mind, it's time to get everything down on paper. This is the moment your succession planning for small business transitions from a good idea into a concrete, formal document. Think of this plan as the official roadmap for the handover—it’s the single source of truth that will guide everyone involved.

A well-documented plan isn't just about ticking boxes. It eliminates any gray areas, sets crystal-clear expectations, and provides a framework that can hold up under both legal and financial scrutiny. Without one, even the best intentions can easily get lost in confusion or conflict.

Assemble Your Transition Team

You didn't build your business alone, and you definitely shouldn't try to transition it alone. This is not a solo mission. Pulling together the right team of professional advisors is critical to make sure your plan is sound from every possible angle.

Each member of this trio brings a unique and vital expertise to the table:

- Your Attorney: They are the architect of the legal transfer. Their job is to draft the core documents, like buy-sell agreements or trusts, ensuring the ownership change is legally airtight and protects you from disputes down the road.

- Your Accountant: They handle the numbers and, just as importantly, the tax implications. They'll structure the deal to be as tax-efficient as possible for both you and your successor, keep an eye on cash flow, and verify the business's financial health during the transition.

- Your Financial Advisor: They’re the bridge between your business exit and your personal financial life. They make sure the proceeds from the sale align with your retirement goals, estate plan, and overall wealth strategy.

Having these three pros work in concert covers all your bases. It's the best way to prevent costly oversights that could put the transition—or your own financial future—at risk.

What Goes Into a Written Succession Plan?

Your plan needs to be detailed, clear, and comprehensive. Think of it as the ultimate instruction manual for the person taking over. When you start building your actionable succession plan document, leveraging additional business resources can give you a great starting point with templates and checklists so you don’t miss a thing.

At a minimum, your plan needs to cover a few key areas to map out the entire process from start to finish.

The Transition Timeline and Milestones

A vague timeline is an open invitation for delays and uncertainty. Your plan needs a detailed schedule with specific, measurable milestones. This isn't just about picking a final date; it's about breaking down the journey into manageable steps.

For instance, a 3-year handover timeline might look something like this:

- Year 1: The successor starts shadowing you in key financial meetings and major client negotiations. A key milestone could be them successfully leading three major client renewals on their own.

- Year 2: The successor takes the reins of day-to-day operations. The real test? You take a one-month vacation with zero operational contact from the office.

- Year 3: The formal, legal transfer of ownership is executed. The final milestone is getting all legal documents signed and financial transactions completed.

This approach creates real accountability and makes the massive process of letting go feel controlled and intentional.

Clearly Defined Roles and Responsibilities

During a transition, confusion over who's responsible for what can create friction fast. Your plan must spell out, in no uncertain terms, the roles of everyone involved.

This means defining:

- The Owner: What are your specific duties during the handover? Will you stick around as a consultant? For how long and in what capacity?

- The Successor: What specific authority do they have at each stage? When do they get the final say on big decisions?

- Key Employees: How will they support the transition? How will their own responsibilities shift as the new leadership steps in?

A great plan anticipates questions and answers them before they're even asked. By clearly defining roles, you empower your team and prevent the kind of power vacuum that can derail a transition.

The Communication Strategy

How you communicate the succession plan is just as important as the plan itself. A well-designed communication strategy keeps morale high and stops the rumor mill from spinning out of control.

Your plan should map out:

- When to tell employees: Announcing too early can create months of anxiety, but waiting too long can feel like a betrayal. Timing is everything.

- What to communicate: You need to craft a clear, consistent message that emphasizes stability, continuity, and opportunity for the team.

- How to inform key stakeholders: Don't forget your most important clients, suppliers, and your bank. They need a separate, tailored communication plan to reassure them.

Being transparent builds trust and ensures that everyone—from your team to your top customers—feels confident about the company's future. This kind of proactive communication is the hallmark of a truly professional and well-executed succession.

Managing the Transition and Protecting Your Legacy

A perfectly drafted succession plan is only as good as its execution. This is where the rubber meets the road—the final, critical phase where your vision becomes reality.

Managing the transition is about more than just signing papers. It's a delicate process of transferring knowledge, empowering your successor, and navigating the very real human emotions tied to letting go of a business you’ve poured your life into.

Successfully managing this handover ensures the business not only survives your departure but is positioned to thrive for years to come. It’s the last, most important step in protecting your legacy and seeing your hard work pay off.

Implementing a Phased and Structured Handover

A sudden, abrupt handover is a recipe for chaos. The most successful transitions I've ever seen happen gradually, over a planned period, allowing your successor to grow into the role with your guidance. A phased approach minimizes disruption and builds confidence with your team and your clients.

This means systematically transferring responsibilities. It’s not about dumping everything on them on day one. Instead, you need a deliberate handoff of duties, key relationships, and all the unwritten rules of how your business really works.

The goal of a transition isn't just to hand over the keys; it's to transfer the wisdom. This means mentoring your successor through real-world challenges, not just showing them the balance sheet.

For instance, you might start by having them lead internal team meetings. From there, they could progress to co-managing a few key client accounts. Finally, you give them full authority over strategic financial decisions. Each step is a building block, solidifying their capabilities and your team's trust in their leadership.

Overcoming the Emotional Hurdles of Letting Go

For many founders, stepping away is one of the hardest things they’ll ever do. Your identity is deeply intertwined with the business you built. It's completely normal to feel a mix of pride, anxiety, and even a sense of loss.

Acknowledging these feelings is the first step to managing them. Here are a few strategies that have helped other owners navigate this emotional journey:

- Define Your Next Chapter: Have a clear plan for what you'll do post-exit. Whether it's travel, a new hobby, or consulting, having something to look forward to makes letting go much easier.

- Set Clear Boundaries: If you agree to stay on as an advisor, define your role and timeline explicitly. This prevents you from unintentionally undermining the new leader by hanging around too much.

- Focus on the Legacy: Shift your perspective from what you're losing to what you're preserving. A successful transition is the ultimate validation of your life's work.

Properly managing your personal finances is also absolutely key to reducing the stress that comes with a transition. Knowing your financial future is secure provides immense peace of mind. For a deeper look, explore our insights on wealth management for business owners.

Why So Many Business Sales Fail

The unfortunate reality is that many small business sales fall through. While small businesses employ nearly half of the U.S. workforce, only about 30% of those that go on the market actually find a buyer.

It gets worse. On major business marketplaces, the median close rate from 2018 to 2022 was a stark 6.46%, highlighting just how tough these deals can be. A structured succession plan dramatically improves these odds by making your business a much more attractive, buttoned-up asset.

Keeping Your Team Engaged and Motivated

Your employees are the lifeblood of your company, and their anxiety during a transition is real. They'll be worried about their jobs, the company's direction, and what the new leadership will be like. Your job is to manage this uncertainty with clear, consistent communication.

Be transparent about the timeline and introduce your successor early in the process. Frame the transition as an opportunity for growth and stability, not an ending. When your team sees a thoughtful, organized plan in action, their confidence in the future will grow, ensuring the business you built continues to be a great place to work long after you're gone.

Frequently Asked Questions About Succession Planning

Even with a clear roadmap, questions about succession planning for small business are bound to come up. It's a complex process with a lot of moving parts. We've pulled together some of the most common questions we hear from business owners to give you the clarity you need to move forward.

When Is the Best Time to Start Planning?

The simple answer? Yesterday. The next best time is right now.

Ideally, you should start thinking about succession at least five to ten years before your planned exit. That might sound like a long time, but it gives you the runway you need to identify and groom a successor, structure the business for a smooth transfer, and handle all the legal and financial details without being rushed.

A longer timeline also does something else—it makes your business more valuable. A company with a documented, well-thought-out succession plan is a much more stable and attractive asset than one facing an uncertain future.

A lot of owners see succession planning as an "end of career" task. The smart ones see it as a continuous "business strategy" task. The sooner you start, the more control you have over the outcome.

What Are the Biggest Tax Implications?

This is a huge one, and the honest answer is: it depends entirely on your situation. Tax implications can vary dramatically based on your business structure (LLC, S-Corp, etc.) and the path you choose for your exit.

Just to give you an idea of the moving parts:

- Selling to a third party: This often triggers a significant capital gains tax. A good accountant can help you plan ahead to minimize this liability.

- Gifting to family: You can use the annual gift tax exclusion to transfer shares over time, but a large transfer might eat into your lifetime gift and estate tax exemption.

- ESOPs: Employee Stock Ownership Plans offer substantial tax benefits, including the potential to defer capital gains tax on the sale of your stock.

Because the rules are complex and always changing, this is not a DIY project. Getting a tax professional who specializes in business transitions on your team is non-negotiable.

How Do I Keep My Plan Current?

A succession plan is not a "set it and forget it" document. Think of it as a living, breathing part of your business strategy. Your life changes, your business evolves, and the market shifts, so your plan has to keep up.

It needs regular check-ups to stay relevant. At a minimum, you should formally review and update your plan:

- Annually: A quick review to make sure it still aligns with your short-term goals.

- Every three to five years: A more in-depth review with your full advisory team.

- After any major life or business event: This could be a key employee leaving, a big change in your company's valuation, new tax laws, or shifts in your personal family situation.

Regular updates ensure your plan remains a powerful tool, ready to be activated whenever you need it most.

Navigating your business exit while aligning it with your personal wealth goals is a major undertaking. At Commons Capital, we specialize in helping business owners create financial strategies that protect their legacy and secure their future. Schedule a consultation with us today to ensure your transition is as successful as the business you built.