Effective wealth management for business owners is a completely different ballgame than typical financial planning. It demands a specialized strategy that weaves your business growth, personal wealth, and legacy into a single, cohesive blueprint.

Why? Because traditional advice almost always fails entrepreneurs. It simply can't account for the unique financial world you live in, where personal and company assets are deeply tangled together. This guide provides a comprehensive framework for entrepreneurs seeking to translate business success into lasting personal wealth.

Why Standard Financial Advice Fails Entrepreneurs

For most people, a financial plan follows a familiar, predictable path: earn a steady paycheck, save a percentage, invest in a diversified 401(k), and aim for a fixed retirement date. That model works just fine for employees with stable incomes and a clean line between their personal and professional finances.

But for a business owner, that approach isn't just ineffective—it can be downright counterproductive.

Your financial world is built differently. Instead of a predictable salary, you have fluctuating cash flow. Instead of a standard, diversified portfolio, your single greatest asset is often a highly concentrated position in your own company. This reality makes standard financial advice feel like trying to fit a square peg in a round hole.

The Entrepreneur's Unique Financial DNA

The core conflict is simple: your personal wealth and your business's health are two sides of the same coin. A decision to reinvest profits directly impacts your personal liquidity. A personal financial goal might throttle your company's growth. This intertwined reality is a blind spot for most conventional financial advisors.

For example, a typical advisor might look at your ownership stake and immediately recommend selling a large chunk to diversify. For you, that "concentrated stock position" is your life's work. A specialized plan for wealth management for business owners understands this. It focuses on smart de-risking strategies that don't force you to prematurely sell the very asset you're still busy building.

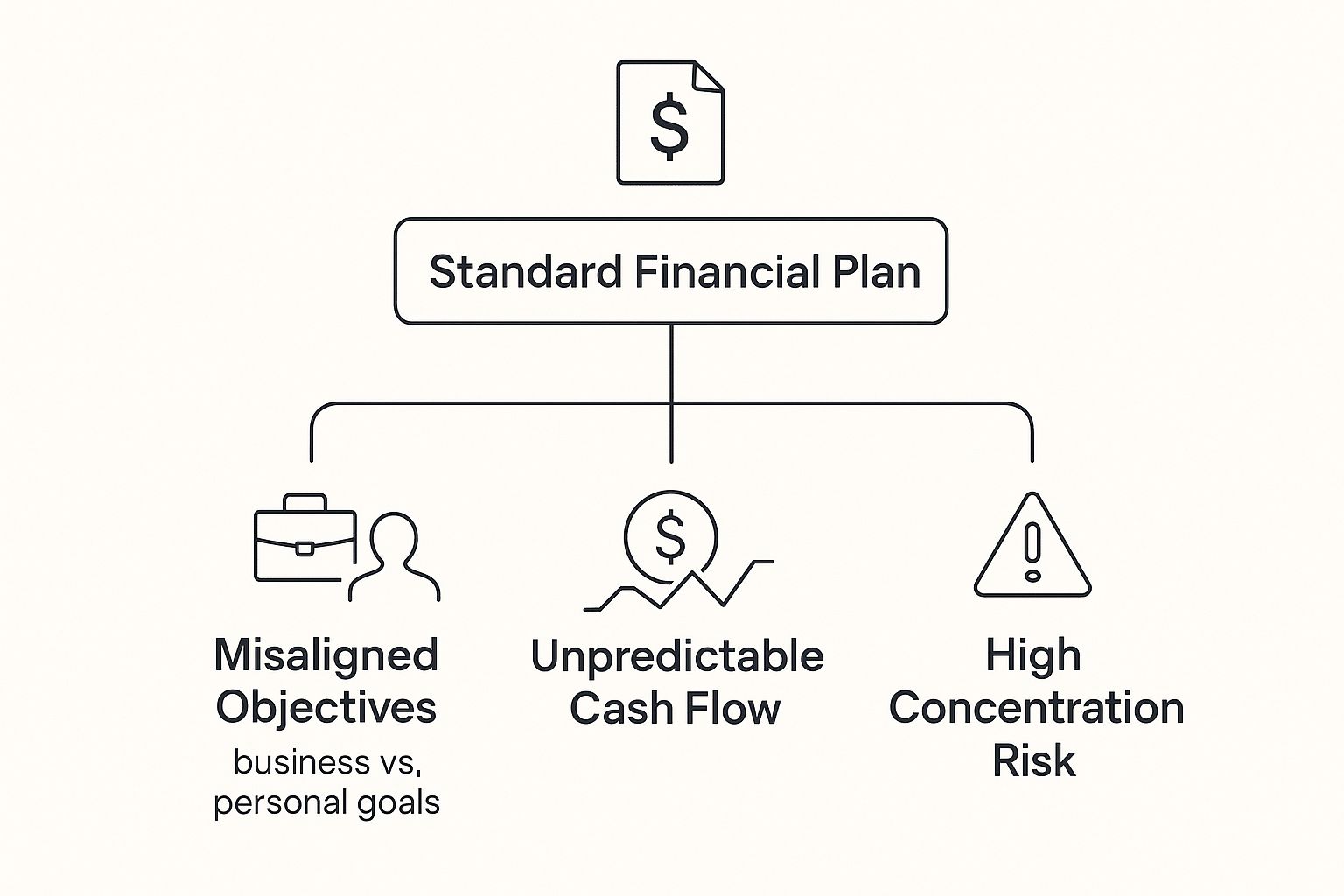

This diagram breaks down the core reasons standard financial plans so often miss the mark for entrepreneurs.

As the visual shows, the combination of misaligned goals, unpredictable cash flow, and high concentration risk creates a financial puzzle that standard models just aren't designed to solve.

Misaligned Goals and Unseen Risks

Entrepreneurs are a massive engine of the global economy. According to the Global Wealth Report, global financial wealth recently hit an all-time high of approximately $305 trillion, and business owners represent a huge slice of that pie. These founders often hold a complex blend of financial and real assets tied directly to their companies. For more on these global wealth trends, both BCG and UBS offer some deep insights.

This unique asset structure creates specific challenges that generic advice completely overlooks:

- Liquidity Events: Your planning doesn't revolve around monthly savings goals. It’s built around future liquidity events, like a sale, merger, or IPO.

- Tax Complexity: Your tax situation is a world away from a W-2 employee's. It involves business deductions, entity structures (like an S-Corp vs. LLC), and qualified business income.

- Succession Planning: Your "retirement plan" is really an exit strategy. It might involve selling the business, passing it to the next generation, or transitioning it to a key management team.

Ultimately, you need a financial strategy that’s built around your business’s lifecycle, not just your personal age. The sections that follow will explore exactly how to build a wealth blueprint that truly aligns with your entrepreneurial journey.

Building Your Integrated Wealth Blueprint

Think of your wealth strategy as the master blueprint for your entire financial life. It’s not just an investment portfolio; it’s a detailed plan connecting your day-to-day business operations to your long-term personal legacy. For an entrepreneur, these two worlds are inseparable, and your financial plan must reflect that reality.

A proper blueprint for wealth management for business owners accounts for every variable—from business cash flow and tax liabilities to your family’s future security. This plan has to be built on four core pillars that work together, creating a resilient financial structure that ensures no single point of failure can jeopardize everything you’ve built.

The Four Pillars of Entrepreneurial Wealth

To truly build a durable financial future, your strategy has to integrate four distinct yet interconnected areas. Neglecting any one of them is like building a house with a weak foundation—it might stand for a while, but it won’t withstand the inevitable storms. Each pillar requires a specialized focus tailored to the unique challenges and opportunities that come with owning a business.

The table below breaks down these four essential components. It clarifies where to focus and what the ultimate goal is for each part of your plan.

The Four Pillars of an Entrepreneur's Wealth Strategy

This structured approach transforms your financial life from a series of disconnected accounts into a powerful, coordinated system designed for growth and protection. It's about making sure your business serves your life, not the other way around.

Pillar 1: Integrated Financial Planning

The first step is to treat your personal finances with the same rigor you apply to your business. Think of your integrated financial plan as your personal business plan, complete with clear objectives, key performance indicators (KPIs), and a strategic vision. This is the central document that guides all other financial decisions.

This plan must address critical questions that standard financial advice ignores. How will you pull profits from the business in a tax-efficient way? What is your strategy for funding both business growth and personal goals like your children’s education? Answering these requires a deep dive into your complete financial picture, which is why a comprehensive guide on business owner financial planning can be an invaluable starting point.

Business owners control an astonishing 30% of all financial wealth in the United States, which amounts to approximately $22 trillion in assets. This massive figure highlights why a specialized, integrated approach is not a luxury, but a necessity for managing such significant and complex wealth.

Pillar 2: Strategic Investing

While your business is likely your most powerful wealth-creation engine, relying on it entirely creates immense risk. Strategic investing for an entrepreneur is all about systematically de-risking your personal balance sheet. This means building a diversified portfolio of assets completely independent of your company.

This goes beyond a simple mix of stocks and bonds. It often involves exploring alternative investments like real estate, private credit, or even venture capital. The goal is to create separate, durable income streams that provide financial stability regardless of your business’s inevitable ups and downs. Beyond the daily grind, adopting proven strategies for financial success is essential to truly build an integrated wealth blueprint that supports your long-term goals.

By intentionally building wealth outside your primary company, you gain something invaluable: financial freedom. It gives you the flexibility to make business decisions based on strategy, not personal financial need. This diversification is your best defense against the unexpected.

Investing Beyond Your Own Company

As an entrepreneur, your business isn't just a company; it's the primary engine that built your wealth. But keeping all your financial eggs in that one basket, no matter how successful it is, is a massive gamble. Real financial resilience is built by creating wealth outside of your business, giving you a bedrock of stability that can weather market shifts, industry disruption, or an unexpected downturn.

Effective wealth management for business owners is all about strategically de-risking your personal balance sheet. It’s a deliberate process of building secondary wealth engines that grow and produce income on their own. This kind of diversification offers a level of freedom and security that capital locked inside your company simply can't provide.

Why Diversification Is Non-Negotiable

Concentration risk is the silent threat that prevents too many successful entrepreneurs from achieving lasting financial independence. While pouring every spare dollar back into your business feels like the most logical path to growth, it leaves your entire net worth exposed to a single point of failure.

Think of your personal wealth as a sturdy table. If your business is the only leg holding it up, any wobble in the company could bring the whole thing crashing down. By building other legs—investments in real estate, private markets, and public securities—you create a foundation that stays solid even if one support gets shaky.

The primary goal of investing beyond your business is to separate your personal financial destiny from your company's. This separation is what transforms business success into enduring family wealth.

This strategy isn't about taking your foot off the gas in your business. It's about strengthening your financial position so you can continue to lead your company from a place of strength, not desperation.

Exploring Advanced Investment Strategies

For business owners, investing often goes well beyond a simple mix of stocks and bonds. Your unique financial position can unlock access to alternative assets that offer distinct benefits, including potential tax advantages and higher returns. Many savvy entrepreneurs use these markets to build truly robust portfolios.

Here are a few key areas that are central to this strategy:

- Private Equity: This involves investing directly into private companies, which can offer much higher growth potential than public markets. As an entrepreneur yourself, you have a unique lens for evaluating these kinds of opportunities. To learn more, check out our detailed guide on private equity investment strategies.

- Direct Real Estate: Owning commercial or residential properties is a classic move for a reason. It can provide a steady stream of cash flow, offer tax benefits through depreciation, and deliver long-term appreciation. This tangible asset class is often a cornerstone of an entrepreneur’s diversified portfolio.

- Private Credit: This asset class involves lending money directly to companies. It often provides attractive yields with lower volatility compared to public debt markets, making it a powerful way to generate consistent income outside of the stock market.

The Growing Trend Toward Alternatives

The move to diversify into alternative assets isn't just a niche strategy; it's a major global trend among sophisticated investors. Global assets under management (AUM) recently soared to an unprecedented $162 trillion, with the United States holding a commanding 54.2% of that total.

Within that landscape, private equity is a real standout, accounting for $9.7 trillion and growing at an impressive clip of 12.3% annually. This data highlights a clear shift by smart investors, including business owners, to allocate capital beyond traditional markets. You can discover more insights about these wealth management statistics.

Ultimately, building wealth beyond your company is a discipline. It requires a commitment to allocating capital to a thoughtfully constructed portfolio of external assets. This disciplined approach is the key to converting your hard-earned business success into a legacy of financial security that can stand the test of time.

Fortifying Your Wealth with Tax and Asset Protection

Making money in your business is one thing. Keeping it is a completely different ballgame. For any entrepreneur, two of the most critical pillars of a lasting financial foundation are smart tax planning and ironclad asset protection. These aren’t just boring defensive moves; they're how you proactively ensure the value you’ve worked so hard to create actually stays with you and your family.

A real wealth management strategy for a business owner has to go way beyond simple bookkeeping. It's about architecting your business and personal finances to minimize the drag of taxes and shield what you've built from threats like lawsuits, creditors, or a nasty economic downturn. You're essentially building a financial fortress around your life's work.

Architecting Your Financial Defenses

Your first line of defense is how your business is legally structured. The decision to be an S-Corporation, an LLC, or another entity type has massive implications for both your tax bill and your personal legal exposure. Each one strikes a different balance between liability protection and tax treatment, making it a foundational choice you should revisit as your business grows.

An S-Corp, for instance, lets you pass profits and losses straight to your personal income, dodging corporate tax rates. An LLC, on the other hand, gives you strong liability protection while offering a ton of flexibility in how you choose to be taxed. Getting this right can literally save you tens of thousands of dollars a year and keep your personal assets safe if the business ever gets sued.

Supercharging Retirement Savings

One of the most powerful tax-slashing tools an entrepreneur has is a supercharged retirement plan. Forget the standard 401(k)s available to regular employees—business owners can use specialized accounts that allow for much, much higher contribution limits. This lets you dramatically accelerate your tax-deferred growth.

These plans are absolutely essential for building wealth completely separate from your company:

- SEP IRA (Simplified Employee Pension): This plan lets you contribute up to 25% of your compensation, maxing out at a hefty $69,000 in 2024. It’s simple to set up and manage, which makes it a fantastic starting point.

- Solo 401(k): If you have no employees (other than a spouse), this plan is a total game-changer. You can contribute as both the "employee" and the "employer," potentially socking away over $69,000 per year, plus extra catch-up contributions if you're over 50.

A well-structured retirement plan does double duty: it cuts your taxable income today while building a diversified pool of assets that has nothing to do with your business operations. This strategy is a cornerstone of creating true financial independence.

Protecting What You've Built

Asset protection is the art of arranging your finances so that it becomes incredibly difficult for a future creditor to take what's yours. As a business owner, your public profile can make you a target. This isn't an optional extra; it's a flat-out necessity. The whole goal is to create a firewall between your personal wealth and your business liabilities.

This usually involves using legal tools to create protective barriers. Trusts, for example, can hold assets like your house or investment accounts, legally separating them from you as an individual. That can be the crucial move that shields your family’s home from a lawsuit aimed at your business.

For entrepreneurs with valuable intangible assets, knowing how to guard your innovations is key to long-term wealth. You can explore a strategic blueprint for intellectual property protection to get a better handle on this. Protecting your IP is every bit as vital as protecting your physical property.

At the end of the day, tax planning and asset protection are two sides of the same coin: wealth preservation. When you weave these strategies into your financial plan, you’re doing more than just growing your net worth—you’re making sure it lasts.

Designing Your Ultimate Business Exit Strategy

For every founder, the business exit isn't just an endpoint—it's the single largest financial event of their life. This is the moment your years of sweat, risk, and innovation get converted into tangible, personal wealth.

Yet, so many entrepreneurs treat their exit as a distant problem, pushing off the planning until it's far too late and leaving immense value on the table.

A successful exit isn’t a last-minute scramble. It’s a continuous process that should be woven into your wealth management for business owners strategy from the very beginning. Thinking about how you will eventually leave the business forces you to build a stronger, more valuable, and more resilient company today.

It’s all about building with the end in mind.

Reframing Your Exit as a Process

First things first: stop thinking of your exit as a single transaction. It's much more effective to view it as a long-term project with clear phases: preparation, valuation, negotiation, and transition. Each phase requires deliberate action years in advance to get the best possible outcome.

Whether you plan to sell to a third party, pass the company to family, or transition ownership to your management team, the fundamentals are the same. You have to build a business that can thrive without you at the center of every decision. This means systemizing operations, developing a strong leadership team, and ensuring your financials are clean and transparent.

What Buyers Are Really Looking For

When a potential buyer or successor looks at your business, they aren't just buying your past performance. They're buying its future potential. A high valuation is driven by specific, tangible factors that reduce their risk and signal sustainable profitability down the road.

These are the key value drivers that really move the needle:

- Recurring Revenue: Subscription models, long-term contracts, and a loyal customer base are far more valuable than one-off sales. Predictable income is king.

- Strong Management Team: A business that depends entirely on its owner is a risky purchase. A capable leadership team that can run the company post-sale is a massive asset.

- Clean Financials: Organized, accurate, and easily understandable financial records inspire confidence and make the due diligence process much smoother.

- Diversified Customer Base: Relying on just a few large clients is a major red flag for buyers. A broad and stable customer base reduces what we call "concentration risk."

Focusing on these areas not only makes your business more attractive to a potential buyer but also makes it a healthier, more profitable company in the meantime. To get a deeper understanding of the entire process, our guide on how to sell a business provides a detailed roadmap.

Structuring the Deal for Maximum Return

Finally, remember that how the deal is structured is just as important as the final price tag. The structure determines how much you actually take home after taxes and other considerations. An all-cash deal is straightforward, but other structures might offer greater tax advantages or long-term upside.

Your exit strategy is the ultimate culmination of your life's work. Planning for it thoughtfully ensures your business legacy is secure and your financial future is maximized, transforming entrepreneurial success into generational wealth.

Options like an earn-out, where part of the payment is tied to future performance, or seller financing can make a deal more attractive to buyers while potentially increasing your total payout. A skilled wealth advisor can model these scenarios to help you understand the true financial impact of each option, ensuring your exit is as profitable as it is successful.

Finding the Right Financial Partner

Choosing a wealth advisor is one of the most critical decisions you'll ever make as an entrepreneur. This isn't just about hiring someone to manage a stock portfolio; it’s about bringing on a strategic partner who truly gets the messy, complicated world where your business finances and personal life collide.

The right advisor is a game-changer. The wrong one can lead to costly tax mistakes, fumbled opportunities, and a legacy left to chance.

A true partner in wealth management for business owners goes way beyond picking stocks. They need to have lived and breathed the entrepreneurial journey—from managing lumpy cash flow and planning for a massive liquidity event to structuring a tax-smart exit. This kind of specialized expertise isn't a "nice-to-have"; it's the absolute foundation of a successful relationship.

Core Qualifications of a Top Advisor

When you're vetting potential partners, you have to look for specific, tangible qualifications that prove they can handle your complex financial reality. Don't settle for a generalist. Your situation is far too specialized for a one-size-fits-all approach.

Your checklist should include these non-negotiables:

- A Fiduciary Commitment: This is the absolute baseline. A fiduciary is legally and ethically bound to act in your best interest. No exceptions. Always get their fiduciary status confirmed in writing.

- Deep Expertise in Business Succession: They must have real, demonstrable experience guiding other owners through the exit process, whether it's a sale, a family transfer, or a management buyout.

- Advanced Tax Planning Knowledge: They should be fluent in the strategies that matter to you, like SEP IRAs, Solo 401(k)s, and sophisticated ways to mitigate capital gains taxes on your eventual sale.

- Experience with Concentrated Positions: Your company is likely a huge, concentrated position in your net worth. The advisor must have a proven methodology for de-risking that position without stifling the company's growth.

Asking the Right Questions

Once you've confirmed the basics, it’s time to dig deeper. Your goal is to cut through the polished sales pitch and understand how they actually think and operate. A few sharp, insightful questions can reveal whether an advisor truly has the chops you need.

An advisor who can't speak your language—the language of business valuation, exit multiples, and owner compensation—can't effectively manage your wealth. Their fluency in your world is as important as their financial credentials.

Try asking something like, "Can you walk me through a case study of a business owner you helped navigate a successful exit?" or "How do you approach balancing aggressive reinvestment in my company with the need for personal diversification?"

Their answers will tell you everything you need to know about their real-world experience and strategic mindset. It's also worth noting that the best firms are leaning into technology to better serve their clients. A PwC report projected global assets under management would approach $145.4 trillion, warning that only firms using modern digital platforms for portfolio and risk management will thrive. As you can learn more about these asset management trends, it's smart to ask how a firm's technology benefits you directly.

Making a confident, informed decision on who to trust with your future is the final, critical step in securing your legacy.

Questions We Hear All the Time

Even with a perfect plan on paper, the real world of wealth management brings up a lot of questions for founders. Here are a few of the most common ones we hear from entrepreneurs, along with some straight answers to help clear things up.

When Is the Right Time to Hire a Wealth Manager?

This is the big one. The answer has nothing to do with hitting a specific net worth and everything to do with hitting a specific level of complexity.

You’ll know it’s time when your business and personal finances are so tangled up that the decisions feel too big and too interconnected to handle alone. It’s that moment you’re staring at a major choice—like how to reinvest a huge profit, whether to fund a massive capital expense, or when you start seriously thinking about your exit.

Getting a professional involved early doesn't just build a better foundation; it helps you sidestep the kind of costly mistakes that can haunt you for years.

How Is This Different from Regular Financial Planning?

Standard financial planning is built for employees. It’s a great tool, but it assumes a predictable, steady paycheck and focuses on straightforward goals like saving for retirement. It's simply not designed for a founder's world.

Wealth management for a business owner is a completely different game. It’s dynamic and has to juggle moving parts that a typical financial plan never touches:

- Wildly Fluctuating Cash Flow: Your income isn't a neat, tidy salary. We need strategies built for inconsistent liquidity.

- Business Valuation as an Asset: Your company isn't just a job; it's likely the biggest number on your personal balance sheet. Its value needs to be actively managed.

- An Exit, Not a Retirement: You don’t just get a gold watch. Your "retirement" is a complex transaction that determines the future of your company and your family.

- Next-Level Tax Strategy: Your tax picture is a web of business entities, unique deductions, and often, a huge concentration of stock in your own company.

It’s an integrated approach that connects your company’s health directly to your personal financial security.

What Are the Biggest Financial Mistakes Owners Make?

Entrepreneurs are masters of their craft, but that laser focus can sometimes lead to a few predictable financial blind spots. A good wealth strategy is specifically designed to protect you from these common traps.

The three we see most often are: 1) Mixing personal and business finances, which creates a legal and accounting nightmare. 2) Failing to diversify, leaving nearly all of your wealth tied up in the business (immense risk!). 3) Putting off exit planning until it's too late, which almost always means leaving money on the table or having a messy succession.

Every one of these mistakes can seriously chip away at the wealth you've spent a lifetime building. Proactive planning is the only real defense.

What Does a Wealth Manager for an Owner Typically Cost?

Pricing models can vary, but the most common structure is a fee based on Assets Under Management (AUM). This fee usually falls somewhere between 0.5% to 1.5% a year, with the rate often scaling down as your portfolio gets larger.

For specific, one-off projects like mapping out a complex succession plan, some advisors might offer a flat-fee or project-based price instead.

The most important thing to confirm, regardless of the model, is that your advisor is a fiduciary. This isn't just jargon; it’s a legal standard that obligates them to always act in your best financial interest. It's a non-negotiable layer of trust and protection.

At Commons Capital, we live and breathe the complex financial world of entrepreneurs. We get that your wealth is woven into the very fabric of your business, and we build strategies that honor your life's work while securing your family's future.

If you’re ready for a financial partner who actually speaks your language, let's connect.