When you decide to sell your business, one of the most significant factors — if not the biggest — is how the deal is structured. It’s a decision that will echo through your bank account for years, as it almost single-handedly determines your final tax bill. Understanding the selling business tax implications from the start is crucial for a successful exit.

The most critical distinction boils down to this: will your profit be treated as a long-term capital gain or as ordinary income? The difference in tax rates can be staggering, often over 15%. Getting this right is the first, and most important, step toward a financially successful exit.

Your Blueprint for a Tax-Efficient Business Sale

Navigating the tax maze when selling a business is one of the most high-stakes financial events in any owner's life. The structure of the sale isn’t just a detail for the lawyers to hash out; it’s the very blueprint that dictates how much of your hard-earned money you actually get to keep. Every decision, from how the purchase price is allocated across assets to the legal form of the transaction, has a direct and powerful impact on what you'll owe Uncle Sam.

This guide is your roadmap. We’ll start with the foundational concepts, the language of the deal. Understanding these key terms and principles is what empowers you to have meaningful conversations with your accountants and attorneys, letting you make choices that are right for you.

Core Concepts to Master Early

Before getting into the more complex strategies, you need to have a solid grip on the fundamentals. The overarching goal is simple: structure the deal to get as much of the sale proceeds as possible taxed at the lower long-term capital gains rates, while steering clear of the much higher ordinary income rates. For businesses operating or selling in different jurisdictions, local regulations add another layer; for instance, understanding details like the UAE's corporate tax framework can be crucial for international sellers.

Here are the key pillars we’ll build on:

- Capital Gains vs. Ordinary Income: This is the big one. We'll break down why one is your best friend and the other can take a serious bite out of your net proceeds.

- Asset Sale vs. Stock Sale: These are the two primary ways to sell a business. We'll demystify them and explain why what’s good for the buyer is often not so great for the seller (and vice-versa).

- Depreciation Recapture: This is a classic "gotcha" for sellers. We’ll show you how those tax deductions you took over the years can come back as a surprisingly large tax bill when you sell.

- Your Business Entity's Role: Whether you’re an S-Corp, C-Corp, or LLC matters — a lot. We'll explore how your entity type directly shapes your tax outcome.

When you understand these core elements from the get-go, you transform from a passenger into the pilot of your own deal. This knowledge lets you ask the right questions and steer the transaction toward a structure that truly aligns with your financial goals.

To help you get a quick handle on these topics, here’s a high-level summary of the key tax concepts you’ll encounter.

Key Tax Concepts at a Glance When Selling a Business

Think of this table as your cheat sheet. These are the main levers that will determine the final tax impact of your sale, and understanding them is the first step toward building a smarter, more profitable exit strategy.

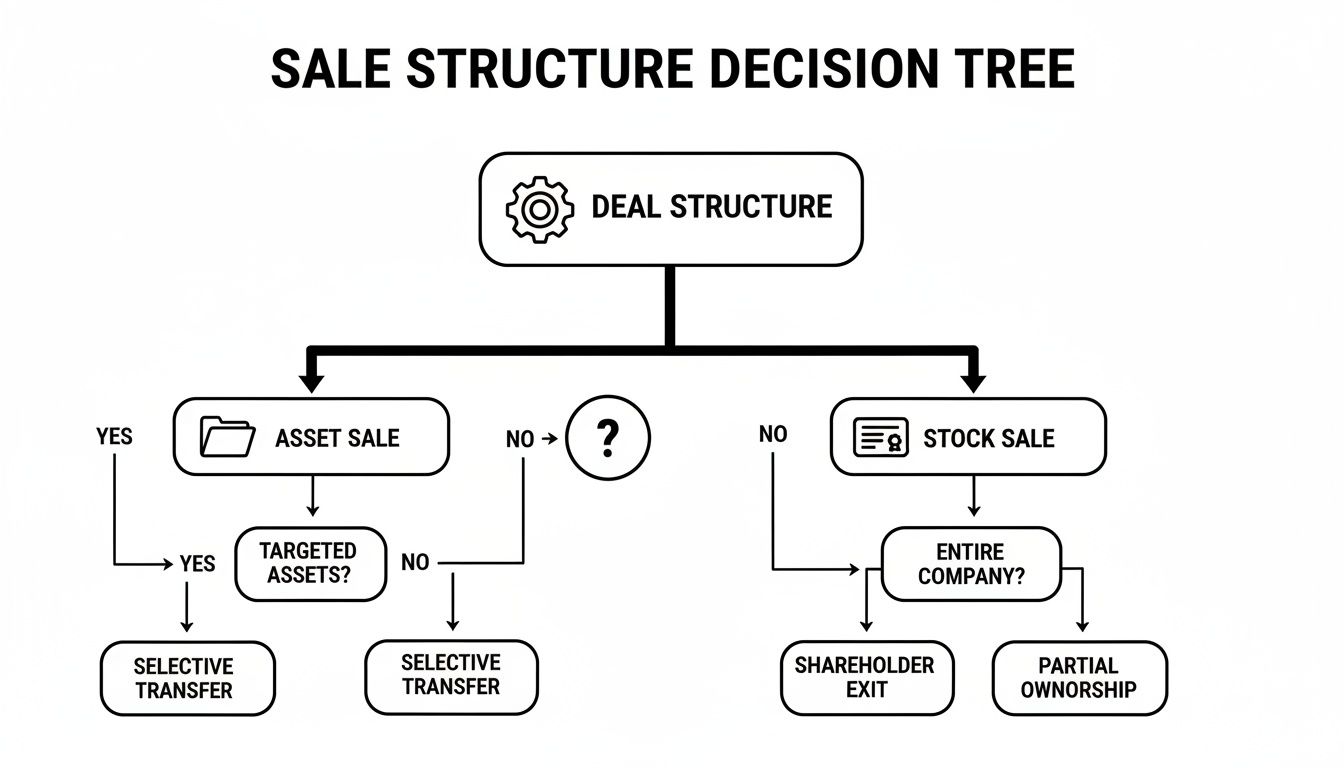

Asset Sale vs Stock Sale: The Defining Choice for Your Tax Outcome

When you're selling a business, no single decision has a bigger impact on your final tax bill than how you structure the deal. It’s the ultimate fork in the road. Are you going to sell the individual assets inside your company, or are you selling the shares of stock that represent ownership of the whole thing?

This one choice creates a natural tension between you and your buyer because what’s best for you financially is often the exact opposite of what’s best for them. Getting a handle on this dynamic is the first, and most important, step in negotiating a deal that doesn’t leave you with a nasty tax surprise.

This decision tree lays out the two main paths a sale can take. It shows how choosing an asset versus a stock sale completely changes the transaction's DNA and, consequently, the tax implications. The key takeaway is that this single choice dictates who gets the better end of the tax stick, setting the stage for some serious negotiation.

The Seller’s Perspective: Why a Stock Sale Is Usually the Goal

For most business owners, a stock sale is the holy grail. It’s cleaner, simpler, and almost always lands you in a better place come tax time.

Think of your business as a car. A stock sale is like handing over the title and the keys. The buyer takes the entire car — the engine, the rust spots, the loan you still owe on it, everything. They become the new owner of the legal entity, and you walk away with cash for your shares.

The biggest win here is that your entire profit is usually treated as a long-term capital gain, assuming you’ve owned the business for more than a year. Those gains are taxed at much friendlier rates than regular income. Of course, you also have to factor in local specifics, as things like the Share Transfer Stamp Duty in Hong Kong can add another layer to the costs.

The Buyer’s Perspective: The Allure of the Asset Sale

Now, flip the coin. Buyers almost always push for an asset sale.

Using our car analogy again, an asset sale is like the buyer walking into your garage and saying, "I'll take the engine, the tires, and the custom sound system, but you can keep the car loan and that weird dent in the passenger door."

They get to cherry-pick the assets they want and, more importantly, leave behind any liabilities they don’t. It’s a clean start for them.

But the real prize for the buyer is a little piece of tax magic called a “stepped-up basis.”

- What is a Stepped-Up Basis? This allows the buyer to record the assets they just bought on their own books at the new, higher price they paid — not your original, lower cost.

- Why Does It Matter? A higher basis means bigger depreciation and amortization deductions for them down the road. It’s a direct financial benefit that lowers their future tax bills for years to come, which is why they will fight hard for it.

This is the central conflict in most deal negotiations: Buyers want the future tax shield from an asset sale's stepped-up basis. Sellers want the immediate, lower tax rate that comes with a capital-gains-focused stock sale.

The Tax Trap of an Asset Sale: Depreciation Recapture

For you, the seller, an asset sale is a lot more complicated — and usually more expensive. The total purchase price has to be split up and allocated to all the different assets being sold, and each category gets taxed differently. Some of your profit, like the portion for goodwill, might get the favorable capital gains rate, but other parts will be hit at higher ordinary income rates.

The most painful part is often depreciation recapture. Remember all those years you took depreciation deductions on your equipment and machinery to lower your taxes? The IRS hasn't forgotten. They view those deductions as a benefit you’ve already enjoyed.

When you sell an asset for more than its depreciated value on your books, the IRS "recaptures" those past benefits. They do this by taxing a chunk of your gain — up to the total amount you previously depreciated — as ordinary income. This can turn what you thought would be a low-tax gain into a high-tax nightmare, catching many sellers completely off guard.

Federal Tax Rates When Selling Your Business

Once you've grappled with the big asset vs. stock sale decision, it’s time to get down to brass tacks: the actual federal taxes you'll be looking at. The tax implications of selling a business aren't based on one single number. Think of it more like a cocktail of different rates and rules that apply to different pieces of the sale price. Getting a handle on this mix is the only way to figure out what you'll really walk away with.

Long-Term Capital Gains Tax

Everyone wants to talk about long-term capital gains. And for good reason. When you sell assets — including your company's stock — that you've held for more than a year, the feds give you a much better deal than on your regular paycheck. For 2024, those rates are 0%, 15%, or 20%, all depending on your total income. The entire game of structuring a smart deal is about pushing as much of the sale price as possible into this bucket.

But wait, there's more.

The Sneaky Surtax: Net Investment Income Tax

For most founders who've built a valuable business, the taxman isn't done at 20%. A common and painful surprise is the Net Investment Income Tax (NIIT). It’s an extra 3.8% tax that hits investment income — and yes, the gain from your business sale usually counts — once your income crosses a certain threshold.

This can feel like a penalty for success, but you absolutely have to bake it into your projections from the start. For many sellers, the real top federal rate on their capital gains isn't 20%, it's 23.8% (that’s 20% + 3.8%).

The NIIT is the perfect example of why a quick Google search on tax rates can be so misleading. It's the layers of tax that get you, and that’s precisely why you need someone in your corner who lives and breathes this stuff.

Depreciation Recapture: The Taxman Taketh Back

I mentioned this earlier, but it’s a trap in asset sales that deserves its own spotlight. Depreciation recapture is the IRS’s way of saying, "Hey, all those tax deductions you took on your equipment over the years? We want some of that back." It flips what should be a low-taxed capital gain into a high-taxed ordinary income gain.

Let’s make it real.

- You bought a machine for $100,000.

- Over five years, you claimed $80,000 in depreciation, lowering its "book value" (or basis) to just $20,000.

- In the business sale, that machine is sold for $90,000.

Your total gain is $70,000 (the $90,000 sale price minus your $20,000 basis). But here's the kick in the teeth: the IRS "recaptures" the depreciation you took. The first chunk of your gain, up to the $80,000 you wrote off, gets taxed as ordinary income. Since your gain was only $70,000, that entire amount is hit with your higher, ordinary income tax rate. Poof. The capital gains treatment vanishes on that piece of the deal.

How Your Business Structure Can Make or Break Your Tax Bill

The legal entity you chose when you started your company now plays a massive role in how this all shakes out.

- S-Corporations and LLCs (taxed as partnerships): These are known as "pass-through" businesses. When you sell, the gains and losses flow right through the company to your personal tax return. It’s generally a simpler path that avoids the dreaded double-taxation.

- C-Corporations: This is where things get dangerous. A C-Corp is its own taxpayer, which creates a huge risk of double taxation. In an asset sale, the corporation pays corporate tax on the gain first. Then, when the company distributes the cash to you, the owner, you get hit again with personal capital gains tax on that dividend. It's a brutal one-two punch that can wipe out a huge portion of your proceeds.

Understanding these rules isn't optional. The good news is that there are smart strategies for almost every situation, and it’s always worth exploring how you might be able to offset capital gains with some foresight. Ultimately, the way your entity type and deal structure interact will determine the number that matters most: the cash that actually lands in your bank account.

Advanced Tax Strategies to Maximize Your Proceeds

Knowing the basic tax rules for selling a business is one thing. Actually using advanced strategies to keep more of your money is what separates a good exit from a truly great one. Once you have a handle on the fundamentals — like the difference between an asset and a stock sale — you can start exploring the powerful techniques that savvy sellers use to delay taxes, lower their overall bill, and walk away with more cash.

These aren't some shady loopholes; they're established parts of the tax code built for specific situations. The key is planning ahead to make sure your deal structure lines up with these provisions. Doing it right can have a massive impact on your final take-home number.

Let’s dig into a few of the most effective strategies out there.

Spreading the Gain with an Installment Sale

One of the most straightforward yet powerful tools in the shed is the installment sale. Instead of getting paid in one giant lump sum, you and the buyer agree to spread the payments out over several years. It seems simple, but this timing shift can work wonders for your tax bill.

By receiving the money over time, you can often avoid getting slammed into the highest tax brackets in the year of the sale. For example, taking payments over three years instead of one could keep your income below the line for the 3.8% Net Investment Income Tax (NIIT) each year. That alone can add up to some serious savings. It’s a classic move that gives you control over when you recognize the income, which is a cornerstone of smart exit planning.

The Power of Qualified Small Business Stock

For founders and early investors in the right kind of C-corporation, the Qualified Small Business Stock (QSBS) exclusion is probably the most incredible tax break on the books. Seriously, it’s a potential grand slam. If you check all the right boxes, you might be able to exclude up to 100% of your capital gains from federal income tax.

The QSBS exclusion lets you shield up to $10 million or 10 times your original investment in the stock (whichever is greater) from federal capital gains tax. This is a game-changer that can save eligible sellers millions of dollars.

Now, the IRS doesn't just hand this out. You have to meet some very specific, non-negotiable rules:

- The stock must be from a domestic C-corporation.

- The company must have had gross assets of $50 million or less when the stock was issued.

- You need to have acquired the stock directly from the company itself.

- You must have held the stock for more than five years.

Using the 338(h)(10) Election

So, what happens when your buyer is dead-set on an asset sale to get that "stepped-up basis," but you’re pushing for a stock sale to get better tax treatment? In certain cases, you don’t have to be at a standstill. A special tax move called a Section 338(h)(10) election can be the perfect compromise.

This election is only an option when a corporation is buying the stock of an S-corporation or a corporate subsidiary. It cleverly allows the deal to be treated as a stock sale for legal purposes (you sell your shares) but an asset sale for tax purposes. The buyer gets the stepped-up basis they want, making their future depreciation deductions much bigger. Meanwhile, the seller often still recognizes the gain mostly at favorable capital gains rates, dodging the double-taxation nightmare of a typical C-corp asset sale.

It's complex, for sure, but it’s a fantastic tool for bridging what can be a major gap between buyer and seller goals. A deep dive into various tax strategies for business owners can shed more light on how these sophisticated options fit together.

Comparison of Advanced Tax Mitigation Strategies

To help put these strategies into perspective, here's a quick look at how they stack up against each other. Each one serves a different purpose and is best suited for a particular type of deal and seller.

Choosing the right approach — or even a combination of them — depends entirely on your company’s structure, your personal financial situation, and the buyer's needs. There's no one-size-fits-all answer, which is why working with experienced advisors from the very beginning is so critical.

Don't Forget About State, Local, and International Taxes

If you're only thinking about what you'll owe Uncle Sam when you sell your business, you're making a massive — and potentially very expensive — mistake. The tax implications of selling your company stretch far beyond Washington, D.C. State and local governments have gotten much more assertive about taking their slice of the pie from big deals like this.

Ignoring these obligations is a sure-fire way to watch your hard-earned net proceeds get eaten away by unexpected tax bills. It happens more often than you'd think.

The biggest factor here is pretty simple: where your company actually operates. Selling your business while you live in a no-income-tax state like Florida or Texas can give you a huge financial leg up. But if you're in a high-tax state like California or New York, you could be looking at another 10% or more of your profits going straight to state taxes alone.

The Tangled Web of Nexus and Apportionment

Things get even more complicated if your business has a footprint in more than one state. This is where you'll run into two key concepts that states use to claim their right to tax a piece of your sale: nexus and apportionment.

Think of it this way:

- Nexus: This is just a fancy word for a connection. If your business has a link to a state, that state can probably tax you. This connection can be triggered by a physical office, having employees there, hitting a certain sales threshold, or even just having salespeople who travel there regularly.

- Apportionment: Once a state establishes nexus, they can't just tax your entire profit. They use apportionment formulas to figure out what percentage of your business's income — including the gain from your sale — they're entitled to. These formulas usually look at the share of your company's property, payroll, and sales that are located within that state.

So, let's say your headquarters is in Texas, but you have a sales team hitting the pavement in California and a warehouse in Illinois. You can bet that all three of those states will argue they deserve to tax a portion of your sale. You absolutely need a clear, multi-state tax plan to sort this out and avoid nasty surprises and penalties later on.

One of the most common and costly mistakes I see sellers make is failing to properly account for state nexus and apportionment rules. It’s a messy puzzle, and you really need an expert to help you put the pieces together correctly.

Going Global With Your Business Sale

For companies that operate internationally, the tax picture gets even more complex. Selling a business with foreign subsidiaries, customers, or even just a remote team abroad means you have to dive deep into international tax laws and treaties. It's a whole different world.

Every country plays by its own rules when it comes to taxing the sale of business assets or stock within its borders. Capital gains tax rates can vary wildly from one country to the next, which can have a huge impact on what you actually take home. As of 2024–2025, top corporate tax rates ranged from nearly 0% in some places to over 30% in others. You can explore these global corporate tax rates to get a sense of the landscape.

To make things even more interesting, major policy shifts like the OECD/G20's Pillar Two framework have introduced a 15% global minimum tax for large multinational companies. This can limit the old strategy of using low-tax countries to shelter proceeds from a sale.

If you don't coordinate your U.S. and foreign tax planning, you can easily get hit with double taxation — where both the U.S. and another country tax the exact same gain. Tax treaties exist to prevent this, but they're incredibly nuanced. A successful international sale hinges on having a single, cohesive strategy that accounts for your tax duties in every single country your business touches.

Assembling Your Expert Deal Team for a Tax-Smart Exit

Let's be clear about something: navigating the tax implications of selling your business is not a solo mission. It’s a team sport, and trying to go it alone is one of the biggest gambles you can take with your financial future. The real key to a successful, tax-efficient exit is building a coordinated team of pros, all working toward one goal: maximizing what you keep.

This "deal team" is your front line against costly, irreversible mistakes. You’ve spent a lifetime building this asset. Getting these experts involved early ensures the sale lines up perfectly with your long-term financial goals, your estate plan, and whatever you plan to do with the proceeds.

The Core Members of Your Advisory Team

Each advisor brings a unique and critical skill set to the table. It’s their collaboration that turns a standard transaction into a strategically brilliant exit. You need to know who does what to make sure all your bases are covered.

Your team should absolutely include these experts:

- CPA or Tax Advisor: Think of this person as your strategic tax quarterback. They'll model the financial outcomes of different deal structures, get deep into the weeds on purchase price allocation, and keep you compliant with a maze of federal, state, and local tax laws.

- M&A Attorney: Your attorney handles the legal machinery of the sale. They're the ones drafting and negotiating the purchase agreement, managing the grueling due diligence process, and structuring the deal to shield you from future liabilities — all while making sure the legal framework supports the tax strategy.

- Wealth Manager: This advisor is focused on what comes after the deal closes. They help you figure out how the mountain of cash from the sale will plug into the rest of your financial life. This means everything from investment strategies to estate planning and any charitable goals you might have.

- Valuation Expert: An independent valuation expert gives you a defensible, objective number for what your business is actually worth. This isn't just for setting a realistic asking price; it's crucial for backing up the transaction if the IRS ever comes knocking.

Getting this team in place early is non-negotiable. Their combined expertise gives you a 360-degree view of the deal, ensuring legal decisions support tax goals and the final number in your bank account aligns with your personal financial plan.

Ultimately, a great sale isn't just about the headline price — it’s about your net, after-tax proceeds. Our guide on how to sell a business walks through the entire process and hammers home why having the right experts in your corner is so important.

Your Top Questions About Business Sale Taxes, Answered

When you're staring down the barrel of a business sale, the tax questions can feel overwhelming. It’s a lot to process. Let's walk through some of the most common questions I hear from owners just like you.

Can I Actually Avoid Paying Taxes When I Sell My Business?

The dream of a completely tax-free exit is, unfortunately, usually just that — a dream. But that doesn't mean you have to hand over a massive chunk of your life's work to the IRS. Smart planning can dramatically cut down your tax bill, or at least push it down the road.

For instance, if you're eligible, a strategy like Qualified Small Business Stock (QSBS) can be a home run, potentially wiping out the federal capital gains tax on your sale entirely. For everyone else, an installment sale is a common and powerful tool. It lets you spread the payments you receive over several years, which means you spread out the tax hit, too. This can keep you in a lower tax bracket and make managing your newfound liquidity much less stressful.

What’s the Big Deal About Goodwill vs. a Non-Compete Agreement?

Ah, the classic negotiation point. While both goodwill and non-compete payments are part of the deal, the IRS treats them very differently, and it matters a lot for your bottom line.

- Goodwill: This is the golden ticket for sellers. The profit you make from selling your company's goodwill — its reputation, customer lists, and brand — is taxed at the much lower long-term capital gains rates.

- Non-Compete Agreement: Any money the buyer pays you specifically to keep you from competing is taxed as ordinary income. That means it gets hit with your highest marginal tax rate, the same as your salary.

You can probably see where this is going. The buyer wants to allocate more of the price to the non-compete, because they get a better tax deduction. You, the seller, want to push as much as possible into goodwill to keep your tax bill low.

The purchase price allocation is one of the most critical negotiation points in an asset sale. As the seller, you want to fight for a higher allocation to goodwill. The buyer will want the opposite. It’s a tug-of-war where every dollar re-allocated has a direct impact on your net proceeds.

How Long Do I Have to Own My Business to Get Long-Term Capital Gains Rates?

This one’s straightforward but absolutely critical. To lock in those favorable long-term capital gains rates, you need to have owned the business assets or your company stock for more than one year.

If you sell even one day short of that one-year-and-a-day mark, all your profit is considered a short-term capital gain. And short-term gains are taxed just like ordinary income — at your highest rate. Timing is everything.

Getting the tax strategy right when you sell your business can be the difference between a good outcome and a great one. It requires a team that understands the nuances and can build a plan tailored specifically for you. The advisors at Commons Capital live and breathe this stuff, helping owners design strategic exits that protect and grow their wealth. To see how we can help you walk away with the most from your sale, take a look at our services at https://www.commonsllc.com.