Welcome to your essential guide on the Mega Backdoor Roth limits for 2026. This strategy remains one of the most powerful tools for high-net-worth individuals, families, and business owners looking to supercharge their tax-free retirement wealth. It’s a sophisticated method designed to bypass the income restrictions that typically prevent high earners from contributing directly to a Roth IRA.

Unlocking a Hidden Retirement Savings Vehicle

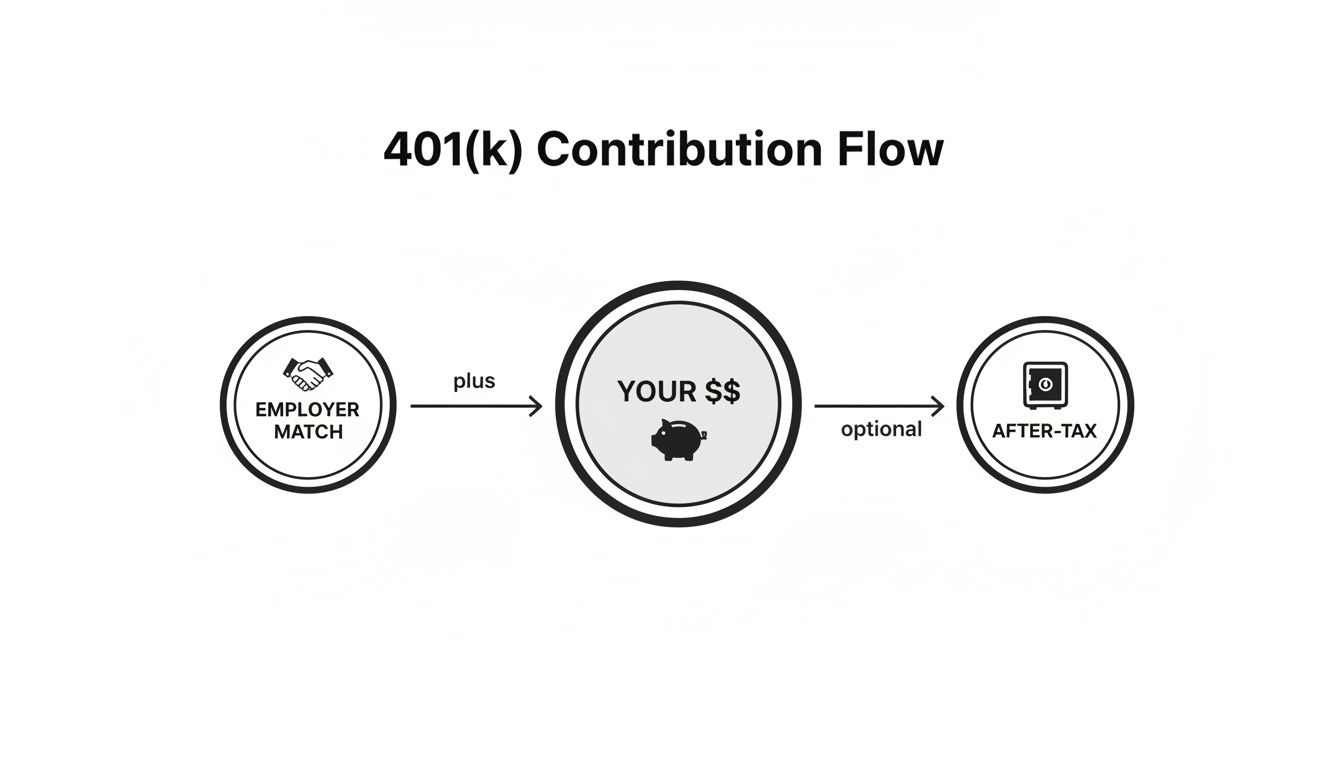

Think of your 401(k) as having three distinct contribution buckets. The first is for your standard pre-tax or Roth 401(k) contributions. The second holds any matching funds from your employer. The third, and most frequently overlooked, is the bucket for after-tax contributions.

The Mega Backdoor Roth strategy is all about leveraging that third bucket. It allows you to contribute after-tax money into your 401(k) up to the maximum legal limit set by the IRS, and then — the crucial step — convert those funds into a Roth account.

Once the money is in a Roth account, all future growth is completely tax-free. For high earners who are phased out of direct Roth IRA contributions due to their income, this is a game-changer. The entire strategy hinges on the significant gap between what you can personally contribute from your salary and the total amount the plan can legally accept.

Understanding the Contribution Gap

For 2026, the Mega Backdoor Roth strategy lets you capitalize on that contribution gap. While you can personally defer up to $24,500 from your paycheck (as either pre-tax or Roth contributions), the total amount allowed in your 401(k) from all sources — including your contributions, employer contributions, and after-tax funds — soars to a projected $72,000.

This creates a potential savings window of $47,500 or more, which can be filled with after-tax dollars and then promptly converted to a Roth. It's a direct path to tax-free savings that sidesteps the usual income limits.

The core idea is to convert after-tax 401(k) contributions into a Roth account, where all future investment growth becomes tax-free. This simple move transforms a standard retirement plan into a formidable wealth-building tool.

This is not the same as the standard backdoor Roth IRA. That strategy deals with much smaller annual contribution limits. To learn more about the differences, read our guide on the backdoor Roth IRA conversion process. The "mega" version offers a significantly larger runway for building a tax-free nest egg, making it a critical strategy for serious long-term financial planning.

Calculating Your 2026 Contribution Potential

Knowing the IRS rules is one thing, but applying them to your personal finances is where the real value lies. To maximize a Mega Backdoor Roth, you need to identify three key numbers that determine exactly how much you can contribute each year. It's a simple calculation that reveals your personal capacity for after-tax contributions.

The formula is surprisingly straightforward: start with the total 401(k) plan limit, subtract what you and your employer have already contributed, and the remainder is your maximum after-tax contribution room.

The Three Key Numbers for Your Calculation

To determine your contribution potential, you'll need three specific figures from your 401(k) plan.

- The Overall Plan Limit: For 2026, the IRS has set the total amount that can go into a defined contribution plan from all sources at $72,000. This is the absolute ceiling and includes your deferrals, employer contributions, and after-tax funds.

- Your Employee Deferral Limit: This is the amount you contribute directly from your paycheck. In 2026, the maximum you can contribute is $24,500.

- The Catch-Up Contribution (If Applicable): If you are age 50 or older, the IRS allows an extra "catch-up" contribution, projected to be around $8,000 for 2026.

With these figures, the math is simple:

$72,000 Total Limit - (Your Contributions + Employer Contributions) = Your Maximum After-Tax Contribution Room

This flowchart helps visualize how the pieces fit together. Your personal deferrals and the company match are contributed first, and the remaining space up to the $72,000 ceiling is what you can fill with after-tax money.

Real-World Calculation Scenarios

Let's apply this formula to a few realistic scenarios for high earners.

The table below breaks down a few common situations. Note how a more generous employer contribution reduces the room available for after-tax contributions, but there is almost always some space available.

These examples demonstrate that understanding the math is the first step toward building a significant tax-free retirement fund.

Here's how we arrived at those numbers:

Scenario 1: A 45-Year-Old Business Owner

Let's imagine Alex, a 45-year-old business owner. He maxes out his personal 401(k) deferral, and his company provides a solid 5% match on his $400,000 salary.

- Total 401(k) Limit: $72,000

- Alex's Contribution: $24,500 (maxing out his personal deferral)

- Employer Match: $20,000 (5% of $400,000)

- Total Contributions So Far: $24,500 + $20,000 = $44,500

Now, let's find his after-tax room: $72,000 - $44,500 = $27,500.

Alex can contribute an extra $27,500 in after-tax dollars, which he can then convert to a Roth. Understanding these mechanics is crucial, and you can learn more from our guide on how tax-deferred retirement accounts work.

Scenario 2: A 52-Year-Old Executive

Now, let's consider Sarah, a 52-year-old executive. She also maxes out her contributions, including her catch-up. Her company offers a generous profit-sharing plan instead of a traditional match.

- Total 401(k) Limit: $72,000 (The overall limit does not increase for those over 50)

- Sarah's Deferral: $24,500

- Sarah's Catch-Up: $8,000

- Employer Profit-Sharing: $25,000

- Total Contributions So Far: $24,500 + $8,000 + $25,000 = $57,500

Let's see what's left for Sarah: $72,000 - $57,500 = $14,500.

Even with a significant employer contribution, Sarah still has $14,500 of room for an after-tax contribution.

The increase to $72,000 for 2026, up from $69,000 in 2025, represents a 4.3% inflation-linked adjustment. This continues a decade-long trend that has seen total 401(k) limits climb by 28% since 2016. For high-net-worth families, this extra room provides a fantastic opportunity to accelerate wealth-building.

Confirming Your 401(k) Plan Is Compatible

Before you can utilize the generous mega backdoor Roth limits in 2026, you must confirm that your 401(k) plan supports it. While this strategy is incredibly powerful, its availability depends on the specific features your employer has included in their plan.

Not all 401(k) plans are created equal. Most offer standard pre-tax and Roth deferrals, but the options required for this advanced strategy are far less common. You need to look under the hood to ensure the right components are in place.

To execute a mega backdoor Roth, your plan must have two non-negotiable features.

The Two Pillars of a Compatible Plan

Your first step should be to obtain a copy of your plan's Summary Plan Description (SPD). This document outlines every feature and rule. If you can’t locate it, a quick email to your HR department or plan administrator should suffice.

Once you have the SPD, look for two key provisions:

- It must accept after-tax contributions. This is the most crucial requirement. The plan must allow you to contribute money after taxes are taken out, separate from your regular Roth 401(k) contributions. This distinct contribution type lets you fill the gap up to the $72,000 total plan limit.

- It needs a path for conversion. Making after-tax contributions isn't enough; you need a way to move that money into a Roth account. Your plan must offer at least one of these two options:

- In-Plan Roth Conversions: This allows you to convert after-tax funds to the Roth 401(k) portion of your account without ever leaving the plan.

- In-Service Distributions (or Rollovers): This feature allows you to roll your after-tax contributions out of the 401(k) and into an external Roth IRA, even while you are still employed.

- Can I make voluntary after-tax contributions beyond my normal $24,500 employee deferral limit?

- Does the plan permit me to move those after-tax contributions into a Roth account while I'm still employed here?

- If so, is that done through an in-plan conversion or by rolling it over to a Roth IRA?

- The ADP Test: This test examines regular pre-tax and Roth 401(k) contributions made from employee paychecks to ensure the average HCE savings rate is not disproportionately higher than the average for NHCEs.

- The ACP Test: This is the critical test for a mega backdoor Roth. It evaluates employer matching funds and, most importantly, employee after-tax contributions. If HCEs are the only ones making after-tax contributions, it can easily skew the results and trigger a failure.

- Implement a Safe Harbor 401(k) Design: This is often the cleanest solution. By committing to specific employer matching or non-elective contributions, the plan can automatically pass the ADP and ACP tests, allowing HCEs to contribute the maximum without fear of test failures.

- Enhance Employer Contributions to Boost Participation: A more generous employer match can encourage NHCEs to save more. Increased participation raises their average contribution percentage, creating more room for HCEs under ACP testing limits.

- Set Strategic After-Tax Contribution Limits: Some plans proactively cap the amount of after-tax money HCEs can contribute. A carefully calculated limit can prevent the plan from failing the ACP test, ensuring HCEs can at least get some after-tax money in rather than having it all returned.

- In-Plan Roth Conversion: This keeps everything within your existing plan. You simply shift the after-tax money into the Roth 401(k) bucket.

- In-Service Rollover to a Roth IRA: This approach moves your after-tax contributions out of your 401(k) and into a separate Roth IRA that you own and control.

- First, Confirm Your Plan's Eligibility: Before anything else, verify that your 401(k) plan allows for both after-tax contributions and in-service conversions or rollovers.

- Calculate Your Max Contribution: Run the numbers. Start with the $72,000 total plan limit for 2026. Subtract your planned employee contributions and your employer's contributions to determine your personal after-tax contribution room.

- Partner with Your Financial Advisor: This is a strategic decision. Work with an advisor to model how increased Roth savings will impact your long-term tax projections, estate plan, and overall wealth trajectory.

- The Backdoor Roth IRA: This is a smaller-scale strategy. You make a non-deductible contribution to a Traditional IRA and then immediately convert it to a Roth IRA. The amount is capped by the annual IRA limits, typically around $7,000.

- The Mega Backdoor Roth: This is the larger strategy. It uses the 401(k) system to funnel tens of thousands of dollars in after-tax money — up to the overall plan limit of $72,000 for 2026 — and then converts that massive sum into a Roth account.

If your SPD confirms your plan has both of these pillars, you are ready to proceed.

Questions to Ask Your Plan Administrator

SPDs can be dense and difficult to understand. If you're struggling to find a clear answer, go directly to your plan administrator or HR contact with a few simple questions.

The most direct approach is to ask: "Does our 401(k) plan allow for both non-Roth after-tax contributions and in-service conversions or distributions of those specific funds?" This question cuts through the jargon and addresses the two core requirements.

Here are a few more pointed questions that can help:

Their answers will provide a definitive "yes" or "no."

The Gold Standard: Auto-Conversion

While reviewing your plan’s details, look for a premium feature known as auto-conversion. Some modern 401(k) plans, especially at larger companies, offer to automatically convert your after-tax contributions to Roth with each paycheck.

This feature is the gold standard because it eliminates the risk of generating taxable gains. If your after-tax money sits in the account and earns interest before conversion, those earnings are taxable. An auto-conversion feature moves the money instantly, ensuring every dollar of future growth is tax-free.

Navigating Critical Nondiscrimination Testing

For high earners and business owners, a successful mega backdoor Roth strategy involves more than just knowing the contribution limits. You must also adhere to IRS regulations, which is where nondiscrimination testing comes into play.

These are mandatory annual audits designed to ensure a 401(k) plan does not unfairly benefit a company's highest earners over other employees.

Failing these tests can halt a mega backdoor Roth strategy. If the plan is deemed top-heavy, the company may be forced to refund the very after-tax contributions you intended to convert, torpedoing your savings goals and creating an administrative headache.

Understanding ADP and ACP Tests

The two primary compliance hurdles are the Actual Deferral Percentage (ADP) test and the Actual Contribution Percentage (ACP) test. These tests compare the savings rates of highly compensated employees (HCEs) to those of non-highly compensated employees (NHCEs).

A failed ACP test is a common roadblock. When this occurs, the plan must take corrective action, which usually involves refunding "excess" after-tax contributions to the HCEs.

Case Study: A Failed ACP Test

Consider Mark, a small business owner eager to maximize his retirement savings. His company’s 401(k) plan allows after-tax contributions. After reaching his normal deferral limit, he contributes an additional $30,000 in after-tax funds, ready for a Roth conversion.

The problem? Most of his employees are NHCEs who contribute very little to their 401(k)s and make zero after-tax contributions.

At year-end, the plan’s compliance testing fails the ACP test. The average contribution rate for HCEs — driven almost entirely by Mark — is far too high compared to the NHCEs.

The result: The plan administrator is forced to refund $25,000 of Mark's after-tax contribution. He not only loses a massive Roth opportunity but also receives the money back as taxable income, creating an unexpected tax bill.

This scenario highlights why smart plan design is essential for anyone considering the mega backdoor Roth limits in 2026.

Proactive Solutions for Plan Compliance

Fortunately, business owners can design their plans to remain compliant while still enabling a powerful mega backdoor Roth strategy. The goal is to create a framework where HCEs can contribute heavily without unbalancing the plan.

Here are three effective solutions:

By addressing these compliance hurdles from the start, you can design a plan that not only unlocks the mega backdoor Roth but keeps it accessible year after year.

Getting the Timing Right on Your Conversions to Maximize Tax Benefits

Smart execution transforms after-tax contributions into a powerhouse for tax-free growth. When it comes to execution, timing is everything. The goal is to move after-tax funds into a Roth account as quickly as possible to avoid a common and costly tax trap.

Any investment earnings your after-tax money generates before it’s converted are taxable. This means every day you wait, you risk reducing the tax efficiency of the entire strategy.

For example, if you contribute $40,000 in after-tax funds and it grows to $41,500 before you convert it, the $1,500 gain will be taxed as ordinary income. The faster you move the funds, the less chance there is for taxable growth to accumulate.

Comparing Your Conversion Options

After making after-tax contributions, you have two primary paths for moving the money into a Roth environment. The best choice depends on your 401(k) plan's rules and your personal financial situation.

Your plan will either allow you to convert the funds inside the 401(k) itself or roll them over to an external Roth IRA.

Both methods achieve the ultimate goal, but their differences are significant. To understand the nuances, it helps to know how to convert a 401(k) to a Roth IRA.

The choice between an in-plan conversion and an in-service rollover comes down to a trade-off between investment options, creditor protection, and withdrawal flexibility. Getting this right is key to making the mega backdoor Roth strategy work for your long-term plan.

In-Plan Conversion vs. In-Service Rollover

To help you decide which path to take, let's compare the options.

The right choice depends on your priorities. If you want total control over your investments and easy access to contributions, a rollover to a Roth IRA is likely your best bet. However, if you value the robust creditor protection of federal law and the simplicity of keeping everything in one place, the in-plan conversion is an excellent choice.

Tying This Strategy into Your Long-Term Wealth Plan

The mega backdoor Roth is more than a clever way to save for retirement; it’s a foundational component of a resilient long-term wealth strategy. It improves your entire financial picture — from managing taxes in retirement to the legacy you leave behind.

By methodically moving money into a Roth account, you build a powerful reservoir of tax-free capital, creating crucial tax diversification. Just as important as asset diversification, tax diversification gives you incredible flexibility in retirement by providing access to different pools of money — taxable, tax-deferred, and tax-free.

This flexibility allows you to strategically manage your income and tax bracket year by year. You can withdraw from your Roth accounts to cover expenses without pushing yourself into a higher tax bracket, a significant advantage when facing unexpected costs or market volatility.

A Cornerstone of Your Estate Plan

Beyond your own retirement, the mega backdoor Roth is a powerful estate planning tool. Unlike traditional 401(k)s and IRAs, Roth accounts owned by the original contributor are not subject to Required Minimum Distributions (RMDs). This means your money can continue to grow, untouched and tax-free, for your entire life.

This lack of RMDs provides far more control, allowing you to preserve and grow your wealth. When the time comes, these accounts can be passed on to your heirs as a tax-free inheritance.

Your beneficiaries will inherit a Roth account that provides them with tax-free income for years, offering a powerful financial head start and preserving your legacy in one of the most efficient ways possible.

This dual-purpose tool secures your financial independence while creating a tax-advantaged inheritance for the next generation.

Your Action Plan for 2026

To effectively integrate the mega backdoor Roth limits for 2026 into your financial life, follow these key steps:

Successfully using this strategy is about connecting today’s contributions to a ripple effect of future benefits, providing tax-free income in retirement and a tax-free legacy for your loved ones.

Your Mega Backdoor Roth Questions, Answered

Even straightforward financial strategies can have complexities. When it comes to the mega backdoor Roth limits for 2026, a few questions frequently arise.

Is My Income Too High for This Strategy?

"My income is too high for a normal Roth IRA. Can I still do a mega backdoor Roth?"

Yes, absolutely. This strategy is specifically designed for high earners.

The income limits that prevent direct Roth IRA contributions do not apply to this 401(k)-based approach. As long as your 401(k) plan allows after-tax contributions and conversions, your income is not a factor. It is one of the last great ways for high earners to build a significant tax-free retirement fund.

What if My 401(k) Plan Doesn’t Allow It?

"What can I do if my job's 401(k) plan won't let me make after-tax contributions?"

This is a common roadblock. If your employer's plan lacks the necessary features, you are stuck with that specific 401(k). However, you are not entirely out of options.

The best workaround often comes from self-employment or "side hustle" income. You can establish your own Solo 401(k) for that business income and design it with all the necessary features, including the ability to make after-tax contributions and process in-plan conversions.

This creates a personal vehicle for the mega backdoor Roth that is entirely separate from your W-2 job's restrictive plan, giving you back control.

How Often Should I Convert the Money?

"Should I convert my after-tax money to Roth right away, or wait?"

The best practice is to convert the funds as quickly as possible. Any growth your money earns while in the after-tax account is taxable as ordinary income upon conversion.

To avoid this tax drag, move the money immediately after it hits the account. Many modern 401(k) providers offer an "auto-convert" feature that does this for you with every paycheck, ensuring that virtually 100% of your after-tax contribution begins its tax-free growth journey from day one.

What’s the Difference Between a “Backdoor” and “Mega Backdoor” Roth?

"I've heard of both. Are they the same thing?"

They sound similar but are two very different strategies operating on completely different scales.

The "mega" in the name says it all. It allows for dramatically larger contributions, making it a far more powerful wealth-building tool for high-net-worth individuals.

Navigating sophisticated strategies like the mega backdoor Roth is a cornerstone of effective wealth management. At Commons Capital, we specialize in helping high-net-worth families and individuals implement advanced financial plans that align with their long-term goals. To explore how we can optimize your retirement and legacy planning, visit us at https://www.commonsllc.com.